Syngene has published its Annual Report. It was a tough year, with revenue growth slowing down to less than 5 %. Operating margin held steady for the yar, though net margin declined and PAT was down. Growth came largely from Europe, with USA and other export markets disappointing. The Mangalore facility continues to struggle, and holds the key to Syngene’s future performance.

Given below are a few things I picked up from the report, and then some more:

Performance

-

In the first half, performance was muted driven by a sectoral downturn in U.S. biotech funding that affected Discovery Services division while the second half saw a recovery as funding returned.

-

The Company reported 4 % year-on-year growth in revenue from operations. Growth was primarily driven by large molecule development and manufacturing services which saw a solid uptick with its revenue share increasing to 25 % in FY25 from 21 % in FY24.

-

During the year, Syngene underwent an unprecedented 111 audits, including client and regulatory inspections.

-

It joined ten other Indian CRDMOs to launch the Innovative Pharmaceutical Services Organization (IPSO).

-

A key highlight of the year was the strategic acquisition of a biologics manufacturing facility in Baltimore, Maryland in the United States. The US based site acquired from Emergent for USD 36 million will support monoclonal antibody manufacturing and is expected to be operational in the second half of FY26. This site will increase the company’s total single-use bioreactor capacity to 50,000L.

-

Unit 3 acquired from Stelis Biopharma (for Rs.563.20 crore) in the later part of FY24 was operationalized this year providing an additional 20,000 liters of installed biologics drug substance manufacturing capacity and also a commercial scale, high speed, fill-finish unit – an essential capability for drug product manufacturing.

-

A key dynamic for the year was the marked increase in customer RFP’s as they explored alternative options to rebalance their CRDMO business exposure away from China.

-

Approximately one-third of RFPs opted for a “China independent supply model”

-

The AR says Syngene has been achieving a high success rate of conversion and that the pipeline of pilot studies has a good momentum going into FY26.

-

Syngene’s share of the global CRDMO market is currently less than one percent. India holds only a 2-3 % share, or USD 3.6 Bn, of the USD 145 Bn global CRDMO market. This highlights the opportunity size and scope for growth.

-

Expansion of capacity and capabilities in Discovery Services continued at the Bengaluru and Hyderabad campuses.

-

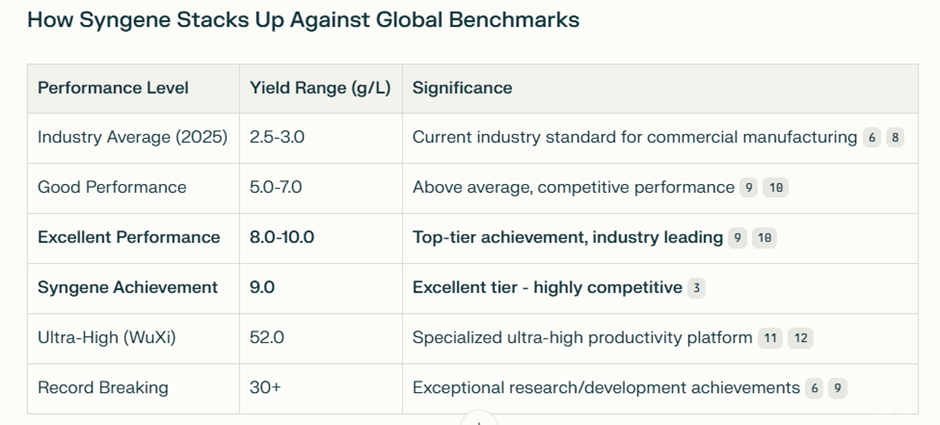

The Large Molecule CDMO pursued high yielding cell line development and achieved a yield of 9g/l. More on this later.

-

Discovery services witnessed challenging demand in the first half followed by growth in the second half supported by conversion of pilot projects.

-

Dedicated centers delivered a stable performance.

-

In Research Services, clients shifting research from China to India favoured pilot-scale engagements to initiate relationships. Of 13 such pilots, six have converted to long-term partnerships, with five still in progress. Research Services recorded moderate growth in FY25. Over the next one year, Research Services plans to achieve a globally competitive efficiency and scale through improving productivity and automation.

-

Throughout FY25, the company operated dedicated centers for three global pharmaceutical leaders – Amgen, Baxter, and Bristol Myers Squibb.

-

Syngene Amgen Research & Development Center (SARC): In a cryptic statement, the AR says in December 2024 Amgen “updated the engagement agreement…therefore, these dedicated facilities will henceforth no longer be referred to as SARC”. In other words, the relationship has been downgraded.

-

Baxter Global Research Center (BGRC): Team size increased by 15 % and infrastructure expanded. Successfully delivered five complex New Product Development (NPD) projects, including both large and small molecule programs.

Trends

-

The report says “Digital transformation and adoption of Artificial Intelligence (AI) are reshaping the CRDMO landscape by accelerating discovery, improving development precision, and enhancing manufacturing efficiency” (more on this later).

-

Large pharma companies are facing rising cost pressures and a patent cliff - about USD 93 Bn in revenue from both biologics and small molecules is expected to go off patent between 2024 and 2028

Guidance

We expect FY26 to be a transient year with uncertain short-term macro environment building in the recovery of biotech funding, Big Pharma restructuring and tempering of urgency on the Biosecure Act. Reported revenue growth is likely to be in the mid-single digits. Operating EBITDA margin is expected to be around the mid-20s for FY26. Effective tax rate is expected to increase to 26 % in FY26 as the SEZ units come out of tax holidays. With increase in depreciation and effective tax rates, the management anticipates a year-on-year decline in PAT in FY26.

What is missing from the Annual Report

Meaningful data. There is no mention of segment wise revenues, proper reactor capacities, capacity utilization, number of molecules or projects worked upon and the stage they are in, share of Top 5 / Top 10 customers, dossiers filed or approved, share of Top 5 / Top 10 products or projects, etc. Even the number of clients continue to be mentioned as “400 plus”.

Going beyond the report, I was intrigued by the following two statements and decided to dig deeper.

The Large Molecule CDMO pursued high yielding cell line development and achieved a yield of 9g/l. How big an achievement is this really? Turns out, it is a fairly decent achievement - until you see what Wuxi Biologics has achieved.

AI says even at 9g/L, Syngene ranks among the top 10 - 15 % of global CDMOs in terms of Cell Line productivity. WuXi Biologics has achieved ultra-high yields by using continuous processing platforms, while Syngene is using the more “conventional” methods.

And now the last (and the most important) point.

The report days “Digital transformation and adoption of Artificial Intelligence (AI) are reshaping the CRDMO landscape by accelerating discovery, improving development precision, and enhancing manufacturing.” Turns out, this statement is true. There is evidence that several leading CRDMOs and their pharma clients have reported double-digit cuts in cycle time, higher first-time-right rates and sizeable cost savings after deploying AI, digital twins, electronic batch records (EBRs) and predictive analytics. Lonza reports design–make decision time cut from “several months” to a few weeks. Design of Experiment work compressed from 3 to 4 weeks to less than 1 week. Right-first-time batches have gone up from 70 % to 90 %. Aurigene reports average discovery cycle time reduced by 40 %, costs down 10 % and model accuracy up 30 %. GSK reports release cycle for vaccine batches shortened from more than 30 days to 15-18 days. Others report batch record review time has been cut upto 80 %. There are various other data points as well.

All this sounds great. But the question is how much of the benefit actually accrues to CDMOs, and how much gets passed on to clients and even the end consumers (i.e. patients)? When your revenue model is based on headcount deployed or time spent on the project, automation can sometimes be a bane rather than a boon. The discovery and development part of the business may face the same problems that I.T. giants are facing. I am trying to understand this.

(Disc.: No change since my previous post)