Hi…

My assessment of the CDMO space is, it’s an upcoming trend in Pharma Sector, like a sub-sector. Pharma is evolving from a small chemical-based medicines to biology-based medicine, like CRISPR, Cell & Gene Therapy, CAR-T, monoclonal antibodies, which is also evident from the fact that, “The FDA approved significantly more biologic NMEs in 2022 than small molecule NMEs (24 compared to 17).” & " Over the past 10 years, the number of molecules in the R&D pipelines has more than doubled, with growth rates for small(chemical) and large(biological) molecules are around 5% and 12% CAGR resp."

What gives me confidence in the CDMO space is, Biologics manufacturing is increasingly relying on biopharmaceutical CDMO. The percentage manufactured exclusively in-house, for example, declined from 57.6% in 2006 to only 29.7% in 2023. Over one-fifth (20.3%) of pharma respondent indicated they will offshore a majority (over 50%) of their biomanufacturing operations to India, China, or another lower cost country over the next five years. The number of CDMOs in the past three years alone has expanded by around 20%. The reason is, COST & LABOUR. For reference, the labour cost in Syngene is 25-26%, which is ~35% of operating cost which is a significant cost. It is cheaper & more time efficient to do R&D outside US/EU. For example, on average biosimilar development takes just 3-5 years in India verses 7 years in the West and costs on average 10X less.

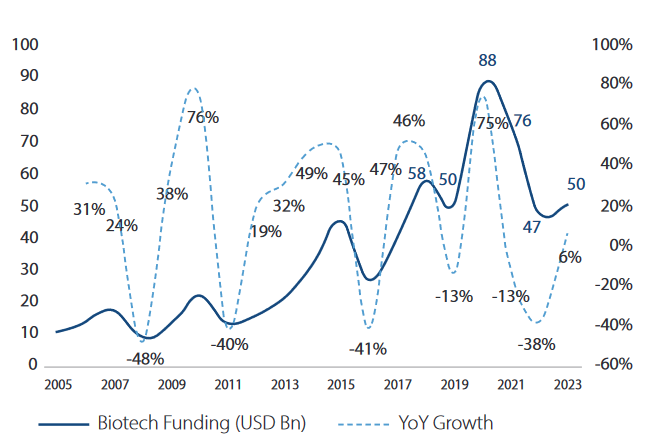

Now, what happened during COVID is, due to govt push & lured by the higher profitability scenario, many VCs jumped into this space. And the number of companies with active R&D pipelines globally has grown from nearly 4800 in 2020 to over 5500 in 2023 of which 67% of overall contribution to Pharma Pipelines is by Emerging Biopharma while large pharma has contributed 23%. Now the situation is, government is no longer interested in pushing the R&D in pharma. Funding from VCs has also dried, which usually go to the emerging/startup biopharma companies. Plus, the big pharma is operating against backdrop of continuing inflationary pressures, rising capital costs, patent expiries, ongoing Federal Trade Commission (FTC) transaction scrutiny etc.

In the absence of new funding, the small emerging pharma is left with limited cash which is expected to over in next 12-18 months. Hence, there is frugalness with spending. One more thing is, these emerging small biotech companies has limited capabilities to scale up the R&D themselves. Hence, they are very much dependent on the outsourcing for commercialising their molecule. I am of the view that, in the next 12-18 months we will see M&A in the biotech space and also since big pharmaceutical companies are sitting on $700 billion for acquisitions and investment.

With China the situation is, labour cost is rising & there is distrust with the Chinese company regarding IP protection. Plus, there is growing need to diversify the supply chain. Sajal Sir commented in the above video that, German regulators are afraid to go visit CHINA for auditing CDMO companies due to China’s Espionage laws. Even US FDA auditors were not allowed to do the auditing of the manufacturing units there. In absence of that, the certification will expire and import from CHINA will be stopped. The BIOSECURE Act is like nail in the coffin for Chinese CDMO. Multiple MNC pharma have closed their R&D centers in China. But they are leveraging China’s R&D workforce via other routes, such as co-development or licensing deals. Also, China’s innovation in biopharma sector relies on returnee scientists. However, if sino US relationship does not improve, there might be less scientists interested in going back to China to work in China’s biopharma industry.

Why INDIA?.. In my view India has two unique advantages, Skilled low-cost labour & Respect for the International laws & IP protection. The 2022, marked a watershed moment in India’s rise in reputation of biologics production – notably, Covid vaccines, the Serum Institute, Bharat biotech, Biocon and, on the CDMO side, Syngene helping transform the country’s reputation. We are already the pharma capital of the world.

The opportunity size as per various industry estimates is,

Global CDMO market was valued at $224.6 billion in 2023 & is projected to grow at 6-7% over next five-six years. While Goldman Sachs in its latest report has projected 11-12% growth in global CDMO. Indian CDMO market is expected to grow at a CAGR of 14.67% from $19.63 billion in 2023 to $44.63 billion by 2029.

On the domestic front various companies are expanding or plan to expand in the CDMO space. Like, Murugappa group company Tube Investments of India is planning to spend 285Cr for setting up subsidiary in CDMO. Such reputed group entering into a space where they don’t have prior history indicates towards the opportunity size. Nirma group is also trying to enter CDMO which is a new industry for them.

On the global stage, Thermo Fisher, had acquired Patheon in 2017 to add CDMO offerings & bought PPD, a major Contract Research Organization. Larger strategic consolidations have picked up in the past year, with a number of notable deals including Pfizer-GBT, Amgen-Horizon, GSK-Bellus, Merck Prometheus, and Pfizer-Seagen.

I think that, Pharma is going through transformation. Earlier due to technological constrains most of the novel drugs were from chemical entities. Going forward, we would see increasingly, new drugs are coming from biological entities. The advantages/disadvantages of the chemical drug is significantly different from biological drug.

There is commentary in the CPHI Annual Report-2023 linked above, which I also find insightful that is,

“While pandemic and geopolitical pressures have subsided, inflation, higher interest rates, a capital supply/demand imbalance in emerging pharma, and a clogged IPO funnel have marshalled in a period of softening demand for services generally across the industry. Resultantly, emerging pharma generally have migrated towards cash preservation mode. There are signs of an improving VC funding environment, but this needs to coincide with increasing pharma M&A and a more healthy IPO environment. We believe softer demand, particularly from emerging pharma and in earlier phases of development, will extend for a period of 12-18 months.”

Thanx…

P.S. While reading please keep in mind that, there might be biasness towards INDIA & Indian CDMO Space.

@VALUE2017 I like all the three companies, excellent management, long history, positive cashflow. Syngene is an Integrated player, earlier it was in only in research & development. Now they are also venturing into the manufacturing space. Liberala is an example. Laurus & Neuland, I still have to evaluate.