just gone through the thread in twitter. so can we expect some derating once they hype is dried up and company continues linear growth ?

Let us see what the management has said about Mangalore from time to time.

As early as in the DRHP filed by Syngene in April 2015, Mangalore was mentioned. “We are in the process of setting up a manufacturing facility in Mangaluru to manufacture novel small molecules for companies in pharmaceutical, agrochemical and other industrial sectors”.

The FY16 Annual Report goes into the details about this – “We will invest USD 100 mn in the upcoming commercial scale manufacturing facility taking shape at Mangalore. This facility is spread across 40 acres in the Mangalore SEZ. It will manufacture Active Pharmaceutical Ingredients and Intermediates (API); non-pharma novel molecules including advanced intermediates, agro chemicals and performance / speciality chemicals meant for supplies in various scales. The API facility will be designed to develop processes for pre-clinical, clinical and commercial launch scale material. Other capabilities will include scale-up of the product from lab to pilot and commercial manufacturing. The facility will meet national and international regulations and shall be built as per cGMP and other appropriate regulatory guidelines. We are currently in the process of obtaining necessary permits and regulatory approvals to commence building and this facility is expected to be operational by FY19”’

So the facility was expected to be “operational” by FY19 – i.e. after 3 years. In reality, the facility became operational a year late in end FY20 (that’s ok) but then the management said “facility is ready but regulatory validation and qualification will take time”:

See July 2020 concall – “The real priority for the year is, having now completed the building stage … is now to complete the qualification. So, the order of the hour through the rest of this year is qualifying the plant and then also starting to win those sorts of regulatory inspections and approvals”.

This “qualification” consumed another year. But then they said qualification is done but regulatory approval is not !

Annual Report FY21 – “Towards the end of the financial year, we completed the qualification activities for our API manufacturing plant at Mangalore and the facility has been awarded GMP certification by the Indian regulatory authority. The focus is now on gaining other key regulatory approvals over the next two years”.

Whoa! Wait for regulatory approval which takes another two years. Why couldn’t all this be done faster? It’s already 5 years since work on Mangalore started…

This was answered in July 2021 concall – “You can’t trigger that until you’ve got a product. We’re signalling to you now that we’ve got at least one program in place that, will take us up to 24-months to complete and by then we’ll be at the point where the regulators would want to come and inspect it”.

This “trigger” event is now expected by end - FY24.

Annual Report FY22 – “The Company has small molecule commercial manufacturing facility in Mangalore. The Company remains focused on securing USFDA and other major regulatory approvals for the facility. The approval is expected in FY24”.

And after that also, there will only be a gradual scale up which will take at least 3 – 4 years to achieve full revenue levels.

One can count how many years this is from April 2015 when the company first spoke about Mangalore. Market seems to have been “pricing in” Mangalore since eternity. I totally agree with what @ankush12495 has said in his Twitter thread. The reader can decide for himself if this is simply investors’ ignorance of how this industry works, or the company is guilty of selective & limited disclosures, letting the misunderstanding persist. Draw your own conclusions.

(Disc.: No positions.)

35 Likes

Facility was announced in FY15. However, if you check the construction only started in second half of FY18.

From the annual report

Secondly, coming to generics. Again if one reads FY21 annual report. They have mentioned till the time NCE molecules scale up and commercialize, they will Manufacture generic molecules in non regulatory space

Here from FY21 Annual Report

Finally,

Without any nce molecule to Manufacture how can one trigger an audit? One can only get audited by the customers till then.

+What I’ve observed that asset build up and scale up phase in Pharma takes a lot more time. Eg:- Laurus took full two years to utilize the built up gross block which was lying idle. Neuland still hasn’t been able to increase Utilisation of Unit 3 inspite of it being commercialised.

Compare this to Agro, Syngene management itself mentioned Agro is much more industrial. PI keeps setting up new plants, Astec, BR, Srf and Navin too! Lead time to capacity utilisation is much lesser.

Just my learnings ![]()

Disc:- not invested in personal PF. Family members do hold it.

27 Likes

From FY17 Ar which talks about construction of the Mangalore unit starting in mid of FY18

Here:-

Conc:- Maybe it’s not a J curve story. With Cro growing in mid teens and Manufacturing verticals being added on the top. What needs to be pondered upon, is whether the growth will accelerate to early 20s or mid 20s. Given the quality of the business (high margins+Cash conversion). Only in this scenario one might make reasonable returns.

18 Likes

Here are my thoughts.

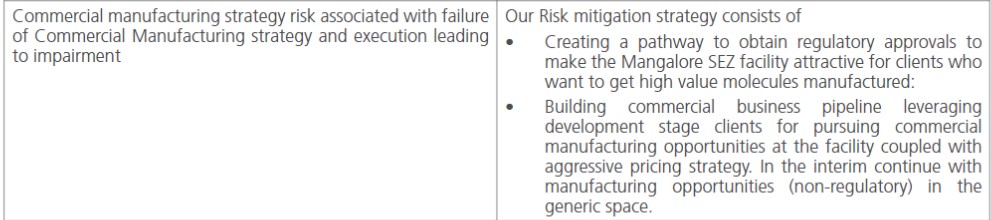

- Syngene management made it clear multiple times that the margin profiles in manufacturing is fundamentally different from their other line of business and it also brings in raw material availability/pricing/supply chain and several other factors into the game.

- They also pointed out that the manufacturing of the non-novel molecules is not something they see as strategic. However, they are open to utilize the capacity if there is an opportunity until they scale up novel molecules. There is little evidence to suggest as of now that they are changing their strategy now (may be they are, we will need to wait and watch)

- Managment view Mangalore facility is one of the levers they have but not the only one lever (again a quote made by their CEO). Relatively speaking, they also gave a rather aggressive guidance if we compare the typical commentary they used to give earlier

- Personally, I prefer a professionally run organization (say as compared to Suven). If Suven is 100% sure about the revenue trajectory, why invest in a manufacturing plant with generics in focus. Probably this business comes with lot of uncertainties and a small piece of generics might make the clock tick.

Disc: Invested in both Syngene and Suven.

19 Likes

Now ,thats a sizable deal, takes Syngene at next level - both capabilities and scale. Well done!!

Invested

22 Likes

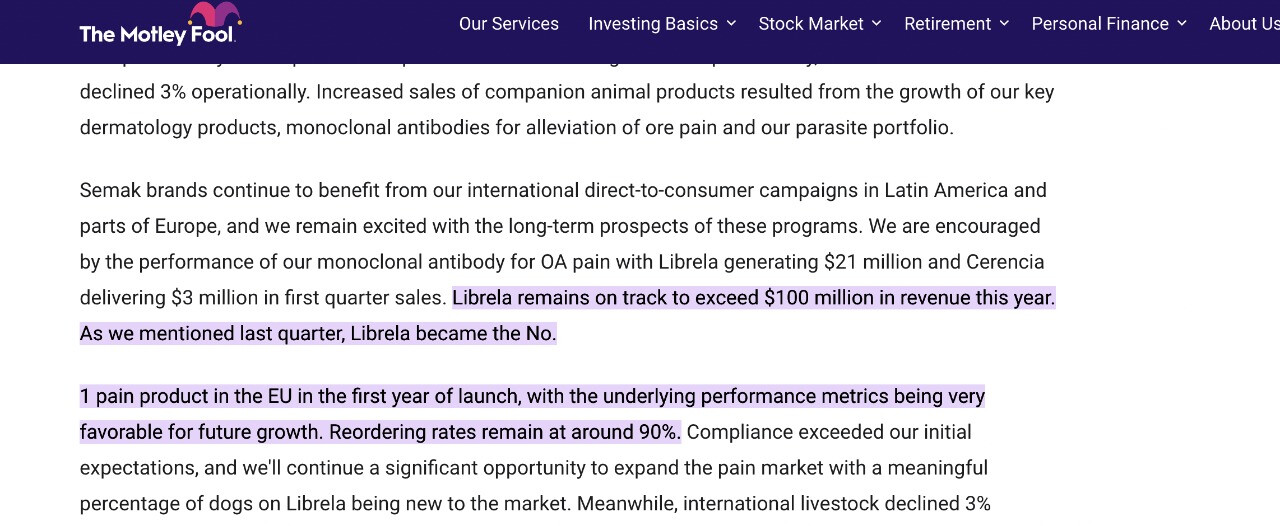

Just to give more perspective on the opportunity size-

Source-Zoetis (ZTS) Q1 2022 Earnings Call Transcript

23 Likes

CRAMS is at same point where Indian IT was in 90’s !!

4 Likes

CRAMS will not take that longer to mature, like IT has taken several decades. Market is quickly responding the trasformation.

1 Like

I think this is a flawed comparison. The scalability of CRAMS is nowhere close to scalability of I.T. There was a time in the late 1990s when people used to joke that Infosys had a board outside their office which said “Caution: Trespassers will be recruited” ! ![]()

Even the current I.T. boom is something similar. In I.T., you can recruit someone, give him a laptop, run him through a six-month course on coding and put him on the job. You can’t do this in CRAMS. There are several challenges, such as skill sets, physical infrastructure, regulation etc. Surely CRAMS will grow, but in slow motion (compared to I.T.).

38 Likes

Most important of them all is- uncertainty related to which molecule will be a blockbuster and which one won’t be. At the end a lot to do with how lucky you get.

Eg:- Pi’s plenty of growth in export is driven by Pyroxasulfone which is known by the name of Axinfeev and is a blockbuster molecule (research reports+export data)+ Agchem is a lot more industrial

In pharma, one has to keep increasing the funnel of molecules on which the co is working. Who knows which one will be epic. It comparisons are flawed due to this uncertainty of success. As gestation period is even higher than agchem

33 Likes

8 Likes

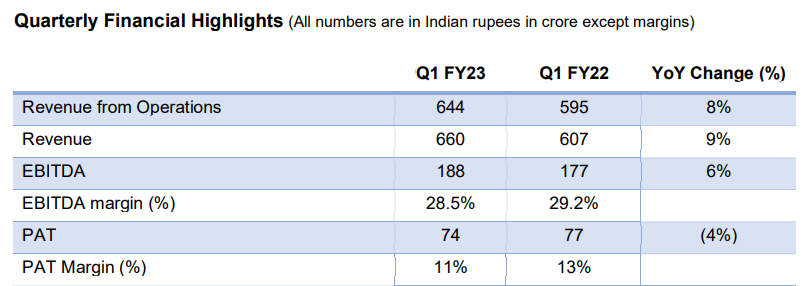

Syngene 1st Qtr results Press release

-

Reports revenue from operations up 8% in the first quarter .

-

Company reported quarterly revenue from operations up 8% Y-O-Y to Rs. 644 Cr; profit after tax for the quarter declined by 4% year-on-year to Rs 74 Cr.

The first quarter results were against a strong quarter last year due to sales of COVID

treatment, Remdesivir. -

Excluding the impact of Remdesivir, the underlying revenue from operations growth in the quarter was around 30% year-on-year.

-

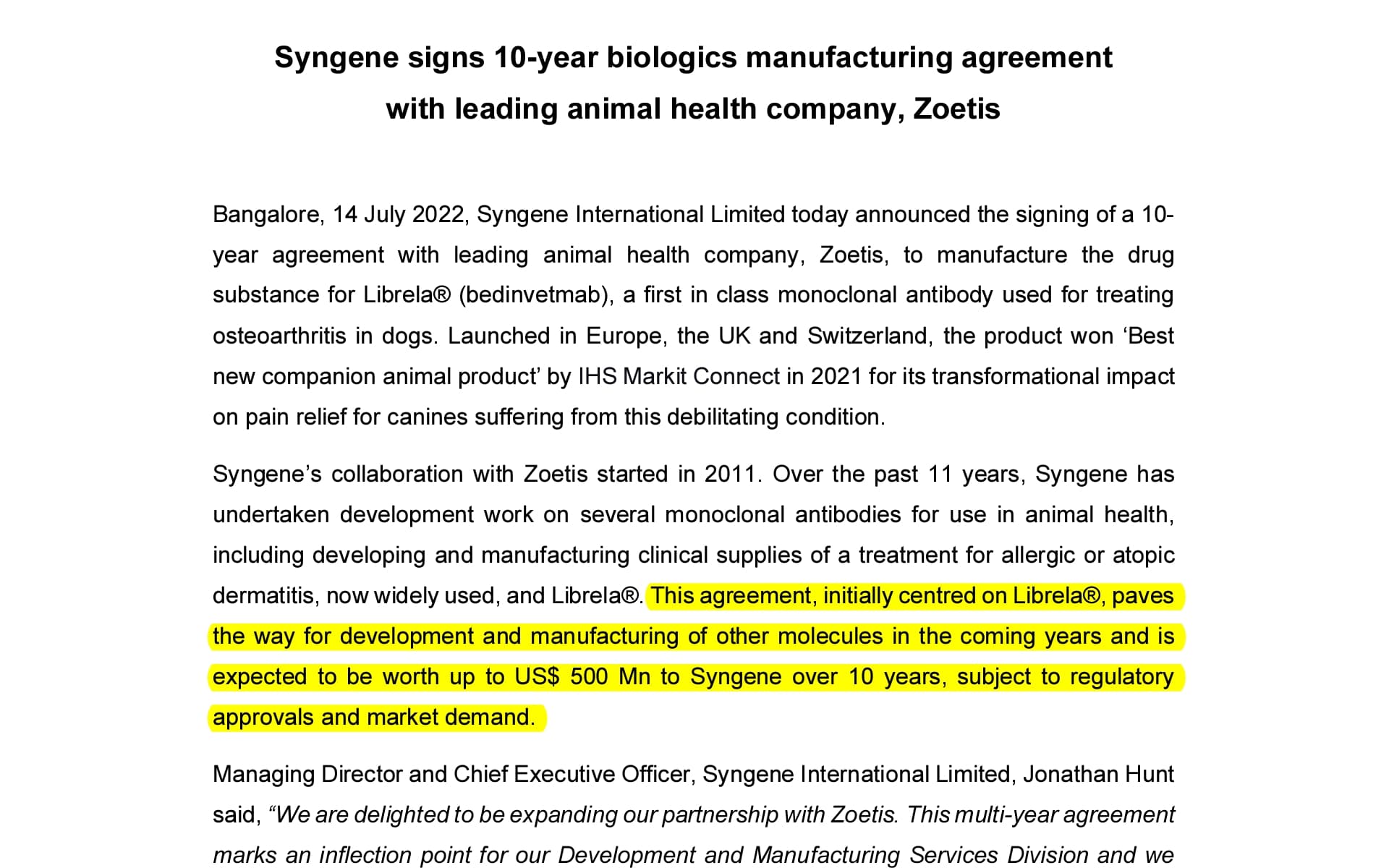

Jonathan Hunt, MD and CEO said, "A recent highlight was the signing of a 10- year agreement with Zoetis. The new agreement initially focuses on the commercial manufacturing of Librela®, a first-of-its-kind injectable monoclonal antibody used for the alleviation of pain associated with osteoarthritis in dogs. This is a major strategic step for our biologics business and gives us a pathway towards FDA and EMA regulatory approvals anticipated later this year.

-

These first quarter results were in line with our expectations and reflect strong underlying

performance across all our business divisions. The contribution from the Development and

Manufacturing Services divisions drove the growth momentum against a low base in the

previous year. The Dedicated Centers and Discovery Services divisions delivered

continued growth.

The decline in profit in the quarter compared to the same period last year was as expected

given the strong sales of Remdesivir last year when India was in the midst of the second

wave of the pandemic. No sales of Remdesivir were recorded in the first quarter this year -

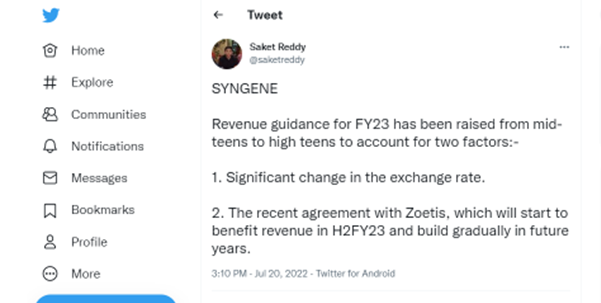

Revenue Guidance for the year has been raised from mid-teens to high teens to account

for two factors: a significant change in the Re/US dollar exchange rate which helps the

top line as most of our client contracts are dollar denominated and the recent agreement

with Zoetis, which will start to benefit revenue in H2FY23 and build gradually in future years.

Business updates

-

I qtr Rev reflects strong underlying performance across all its business divisions. The Dedicated Centres and Discovery Services divisions continued to grow supported by a healthy demand environment.

-

The Development and Manufacturing Services divisions delivered strong growth in the quarter.

-

The Company signed a long-term agreement with Zoetis for the commercial manufacturing

of the drug substance for Librela®, a first-of-its-kind injectable monoclonal antibody to

alleviate pain associated with osteoarthritis in dogs. The agreement, initially centred on

Librela®, paves the way for the development and manufacturing of other molecules in the

coming years and is expected to be worth up to US$ 500 Mn over 10 years, subject to

regulatory approvals and market demand. -

The multi-year agreement marks an inflection point for the Development and Manufacturing Services divisions.

Infra Investment: The Company continued to invest in infrastructure: a kilo lab was established for polymer and speciality materials in the Development Services division. The facility will shorten the

development timelines for clients who look for customizable and flexible systems to expedite formulation and process development services. -

As part of the phase 3 expansion in Hyderabad, a lab was commissioned in the newly constructed Innopolis building with over 150 scientists and analysts dedicated to PROTACs, a targeted protein degradation technology that offers therapeutic interventions not achievable with existing drug discovery approaches. PROTAC is part of Syngene’s novel drug discovery strategy

for clients involved in treatment for cancer.

13 Likes

Niraj Shah ended the interview with same question ![]()

6 Likes

2 Likes

I was comparing the staff cost of Syngene with Suven Pharma. Found that Syngene’s staff cost was 28-30% of their revenue, whereas Suven’s was only 8%. What could be the reason for this difference?

2 Likes

Suven is primarily into manufacturing where as Syngene does contract research as well. Both are not comparable companies.

6 Likes

Surprised to see just two questioners in the Syngene concall ! The call getting over in hardly 25 minutes. What gives?

3 Likes

Q1> From the investor presentation of syngene, which facility are they talking about?

In Manufacturing Services, the Company successfully completed the US Food and

Drug Administration (US FDA), European Medicines Agency (EMA) and Medicines and

Healthcare products Regulatory Agency (MHRA) regulatory audits for its biologics

manufacturing facility

Q2> Can someone point me where I can get the brief description of all their facilites and what they do there?

2 Likes

Time to Study Syngene then. A little improvement in Asset Turnover, boom Pat will shoot.

4 Likes