Commenting on the results, Jonathan Hunt, Managing Director and Chief Executive Officer, Syngene International Limited, said, “Syngene’s performance across all divisions has been positive through the year, and we expect a busy fourth quarter. As a result, we have raised our revenue growth guidance for the full year to high teens

Q3 press release

Q3FY22 Result Update

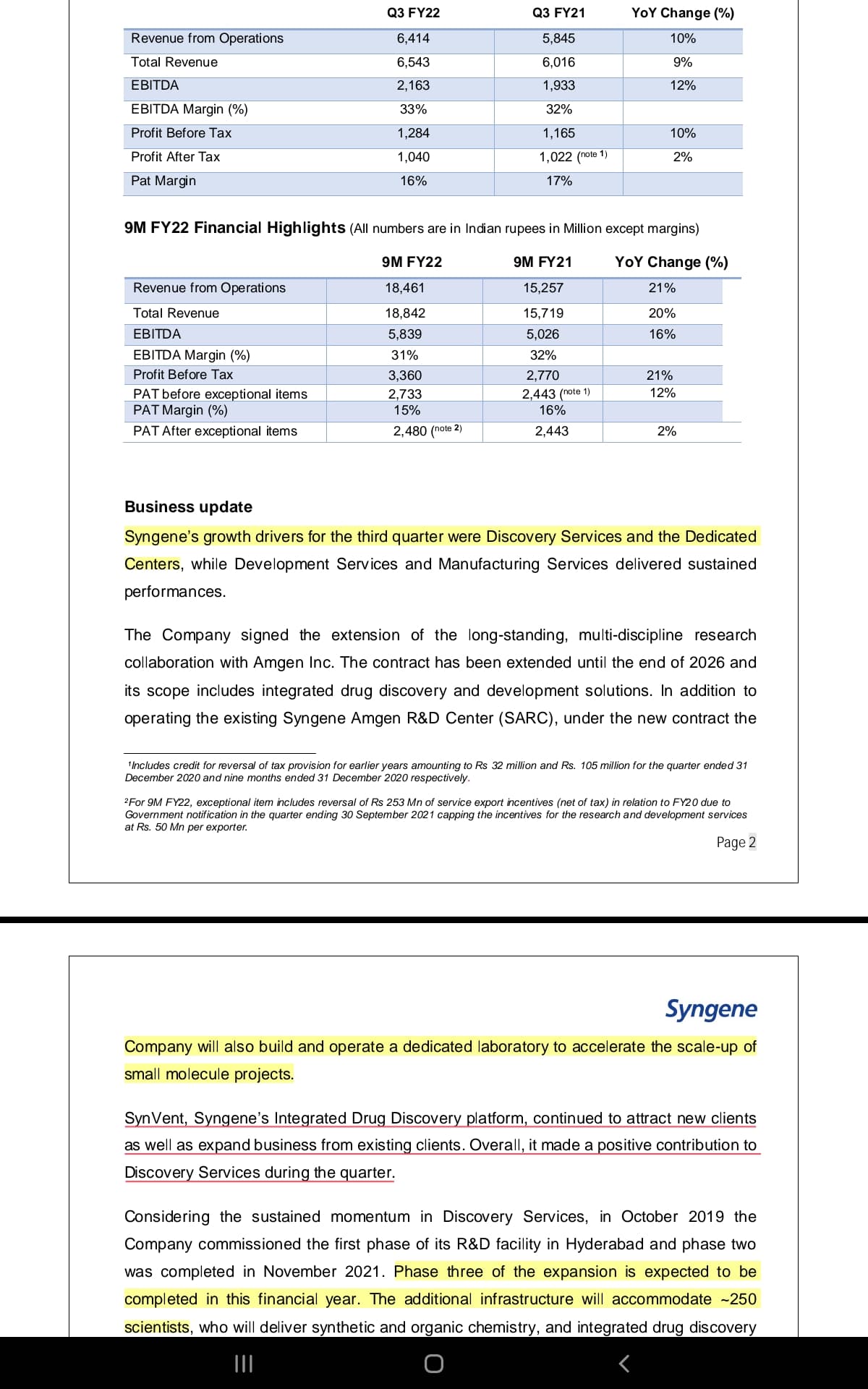

For the 9 months to December 31 2021, the Company delivered growth of 21% in revenue from operations to Rs.18,461 Mn, and profit after tax, before exceptional items, was Rs 2,733

Mn, an increase of 12% compared to the same period in the previous year.

Q4FY22 comment - Based on the Company’s performance to date and the anticipated project deliveries in the fourth quarter, the Company updated the full-year revenue growth guidance to high teens, from the mid-teen guidance shared at the beginning of the financial year.

Source - Q3FY22 Press Release - https://www.bseindia.com/xml-data/corpfiling/AttachLive/55728de9-ac0d-4dce-9c90-7a81cd4a4b05.pdf

Syngene Q3FY22 Investor Presentation - https://www.bseindia.com/xml-data/corpfiling/AttachLive/7372f471-3200-4ec5-8940-e67d5a448552.pdf

Q3FYY22 Result - https://www.bseindia.com/xml-data/corpfiling/AttachLive/500c2d4f-48a9-452d-854a-2177fb9aa239.pdf

Thanks for the summary.

This is what the management had said in their concall dated 23rd Jan 2020, a good 2 years back

“The construction of our commercial API manufacturing plant at Mangalore is on track and is scheduled to be operational as planned by the end of this financial year (by March 2020). As Jonathan has pointed out many times in the past, this project once commissioned will go through a process of qualification and validation”

And this is what was said on 13th May 2020

“The construction activities in our API manufacturing facility in Mangalore have been completed and we have successfully executed the first batch from this plant. As is required of all such facilities before commencing full scale operations, we are now in the process of completing all the qualifications and validation activities and I think that will take us through much of this financial year to complete those”

We are right now at least 2 years away for the Mangalore facility to contribute to the overall topline.

Any further update on this from management or any other sources? Have they lost Herbalife or they just dropped the name from presentations?

Not sure …but seems like they lost Herbalife as a client. This was there in almost all the quarterly presentations from past three years. This information is missing in q3 2022 presentation , so assuming , they would have lost them. But seems not so big thing , Herbalife is only billed for 9 Scientists and 3200 sft space…

Agreed very small number of scientists deployed in herbalife, but i think if they are talking about addition of new client they should also talk about losing a client?

Just a newbie Investor, always Learning

This came out about 15 days ago, but I read about it today.

CRISIL has placed its ‘CRISIL AA+’ rating on

the long-term bank facilities of the Company on ‘Watch with Developing Implications’ following the rating

action on the long term debt facilities of the holding Company, Biocon Ltd. The rating on the short-term bank facilities has been reaffirmed at ‘CRISIL A1+’. B

More information in the announcements.

What does this indicate about the company?

Watch out for biocon too.Biocon’s debt is a concern for sure for Syngene too.

Syngene has fallen many times due to bad results of Biocon even though Syngene did well itself.

Good story with Syngene. But not a risk free bet right now.

Syngene Press release on Q4 FY22 results.

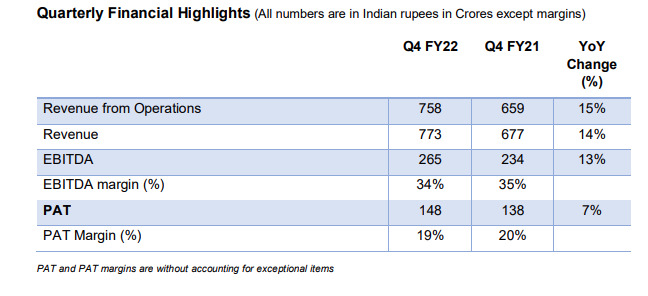

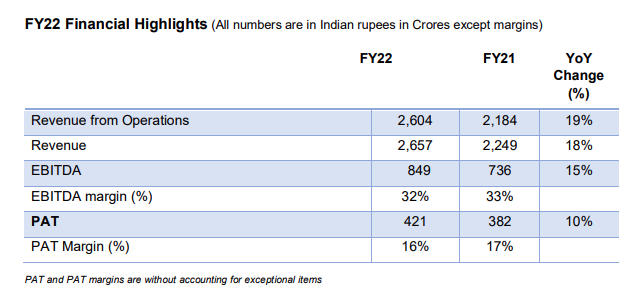

Syngene reports full year revenue from operations up 19% to Rs. 2604 Cr

Revenue from operations up 15% to Rs. 758 Cr in fourth quarte.

Profit After Tax for the quarter, before accounting for exceptional items, was

up 7% year-on-year to Rs. 148 Cr. Profit After Tax for the full year was up 10% to Rs. 421 Cr.

Expansion Plans:Phase three of the expansion plan at the Hyderabad research facility was completed during the quarter. The Company commissioned the first phase of the facility in February 2020 and phase two was completed in November 2021. With the completion of phase three, the facility now accommodates approximately 600 scientists and further expansion is planned in the year ahead.

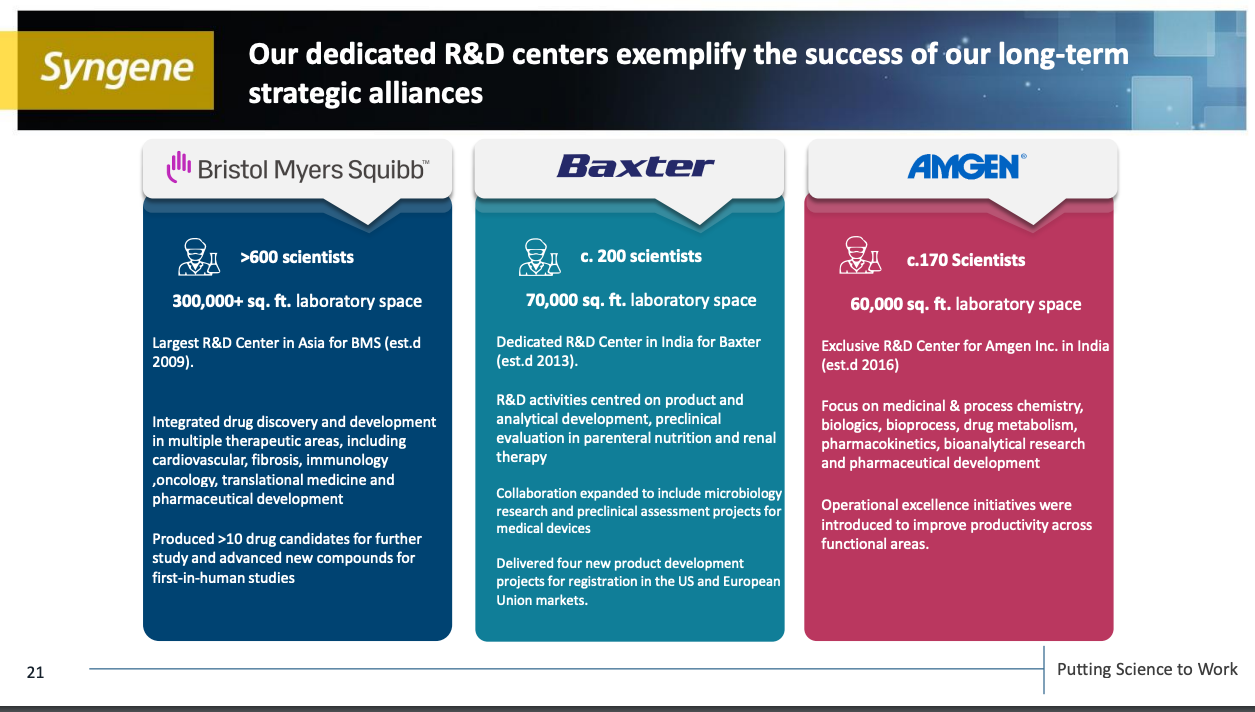

Collaboration with AMGEN: The Company signed an extension of the long-standing, multi-discipline research collaboration with Amgen Inc. to the end of 2026. In addition to operating the existing Syngene Amgen R&D Center, under the new contract the Company will also build and operate a dedicated laboratory to accelerate the scale-up of small molecule projects.

FY23 guidance

Overall revenue from operations for FY23 is expected to grow in the mid-teens. In light of

the positive demand environment for CRO and CDMO services, the Company expects to

step up investments in new scientific capabilities, IT/ digitisation and commercial activities.

This step up in investment, along with resumption of travel and other business activities

post-pandemic in an inflationary environment, is likely to put pressure on margins during

the course of the year. In aggregate, the Company expects to deliver an EBITDA margin

around 30%.

b373bcb6-1928-464c-b2f1-02b94241af4b.pdf (bseindia.com)

Investor Presentation

72c96fbb-fc92-4502-9b39-64235e10c871.pdf (bseindia.com)

Does anyone know why Syngene’s business has seasonality and that Q4 is always the strongest quarter?

Our Q4 correspond to Q1 of regulated market and in Q1 new capital allocation and probably new orders start

May be the reason for seasonality

May be, but I haven’t seen or heard of this in other companies. There must be company specific reason.

Q4FY22 Concall Notes

- Growth was driven by solid delivery across all divisions. Development Services had a particularly strong quarter as it caught up on projects postponed due to supply chain and other Covid-related disruption, in addition to planned work. Syngene’s Integrated Drug Discovery platform, made a positive contribution to Discovery Services during the year as the number of IDD projects increased by 40% compared to the previous year.

- Phase three of the expansion plan at the Hyderabad research facility was completed.

- FY23 Guidance:-

- Revenues expected to grow at least in the mid-teens.

- Expect to deliver an EBITDA margin around 30%.

- Expects the effective tax rate to increase by 200 to 300 basis points in FY23, creating some dilution in the PAT margin. Have MAT Credits available.

- Extended and expanded research collaboration with Amgen. Syngene will also build and operate a dedicated laboratory to accelerate the scale-up of small molecule projects.

- Development and Manufacturing businesses included expanding the biopharma manufacturing capacity by commissioning a cGMP microbial facility and expanding of the mammalian cell manufacturing facility.

- In small molecule development services, the oligonucleotide and highly potent API capabilities were both extended and plans are on track for the Mangalore manufacturing plant to achieve a major regulatory approval thus opening it up to a broader scope of projects.

- Worked with clients on diagnostics, treatments and vaccines related to the coronavirus. The Company also manufactured remdesivir under a voluntary licence from Gilead. This manufacturing will continue for as long as the pandemic persists.

- Deliberately chose to carry higher raw material in FY22. Expect to carry higher inventory in FY23 as well.

- There is a good wave of demand building and Syngene wants to catch up with it.

- Added 100 clients during FY22.

- Seeing good demand in Biologics.

- Investments during FY22 was $80 Million. Capitalized around ~510Cr worth assets.

- Expect better operating leverage from FY24 led by biologics.

- Bulk of CAPEX dedicated to biologics manufacturing and allied activities in FY23.

- Manufacturing business to become visible starting FY23 and pick up momentum FY24.

- Can see YoY decline in revenues in Q1FY23. Growth in 9MFY23 would be higher.

- Have increased investments in Sales and Marketing.

- RM costs to be stable from FY22 Levels.

- Want to spend ~50% of total capex on research with atleast 1x asset turns in 18-24 months, 30% is going to biologics and rest spread across other segments.

- Manufacturing GMP materials going to clinical supplies. Also supplying Monoclonal Antibodies.

- Saw a step up in small molecule development space in Q4.

- Current bio reactor capacity on biologics space is sufficient to cater to rise in demand

Credit: Saket Reddy

Even strides (stelis) said they have capacities ready. We have to wait and watch what kind of strengths (technical ) these two have "right to win "

Predictions are playing now.

https://twitter.com/Ankush__Agrawal/status/1541674637868027905?t=2IF3r_rFhylwdqJz_s5cng&s=19