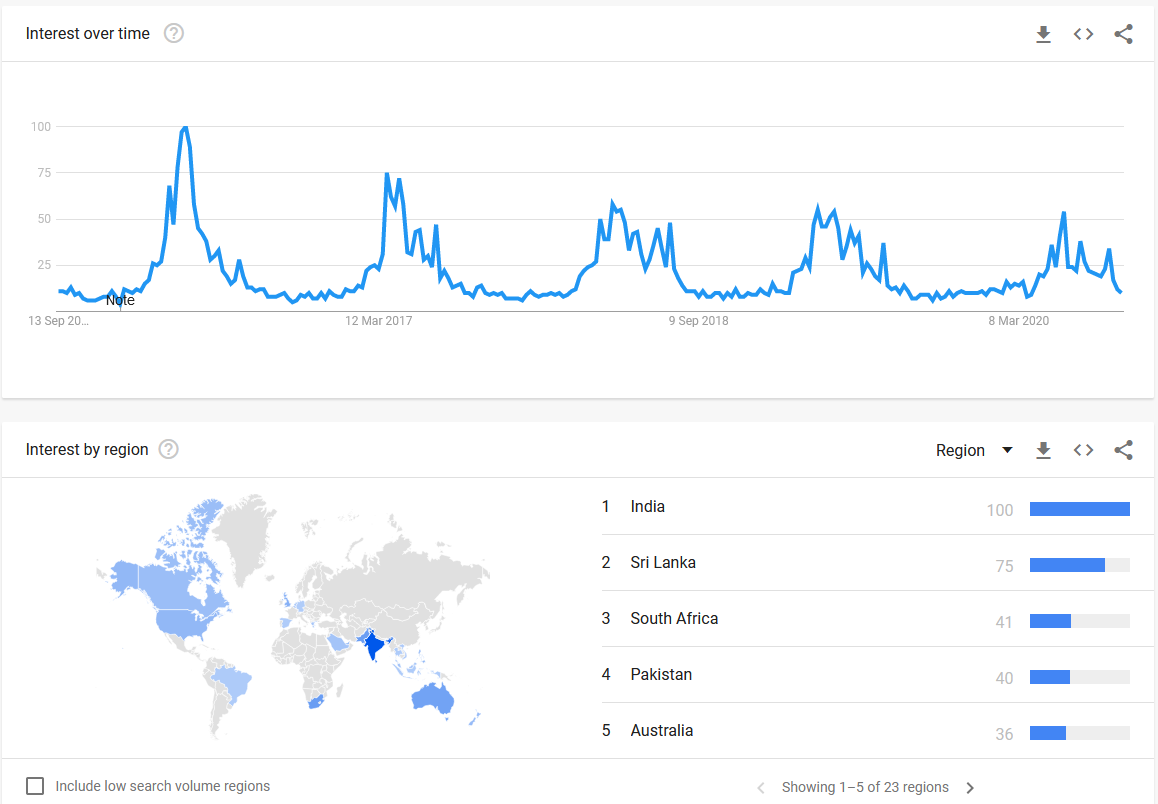

The search for Air Coolers is highest in India over the last 5 years. However, you can see Australia at number (5) which I believe is good news for Symphony. UAE, UK and US are all in 6 - 10 positions. Achal Bakeri told in one of his interviews that China is the 2nd largest Air Cooler Market in the world. You won’t see it here probably because I searched for the term “Air cooler”

In India, Hyderabad, Secundrabad, Vizag and in Australia - Sydney and Melbourne seem to search for Air Coolers the most.

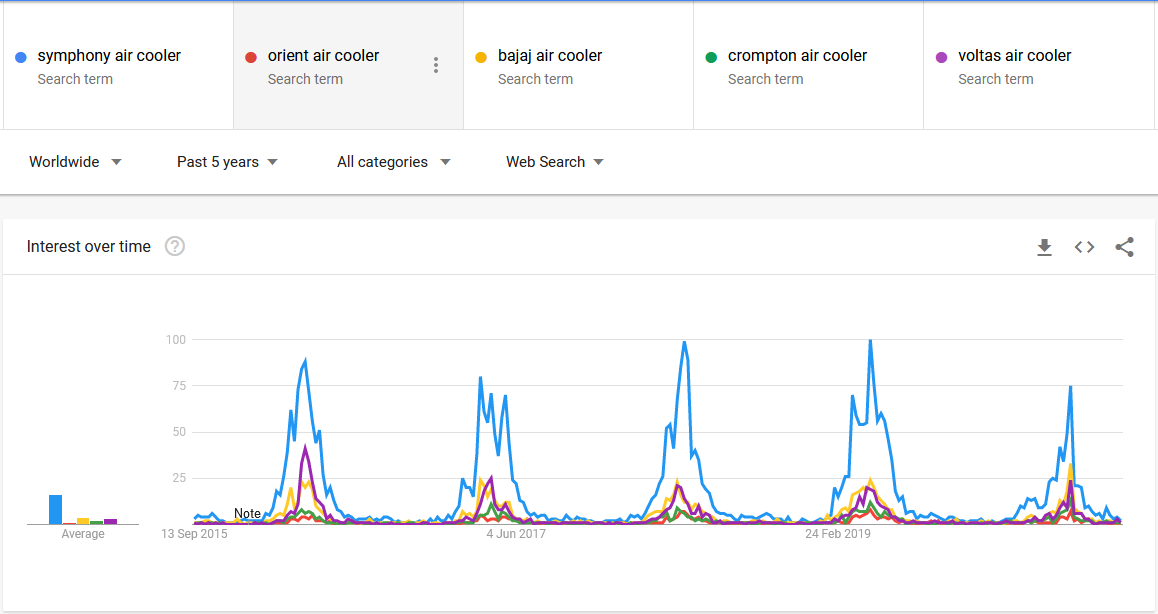

I compared the top brands in India - Symphony, Voltas, Bajaj, Orient, Crompton. Here are the search trends over 5 years. Clearly Symphony is still the Market leader. Interestingly in 2020, the search strength of Symphony has come down while for Bajaj has gone up. Does this translate in the results? It’s some to watch for.

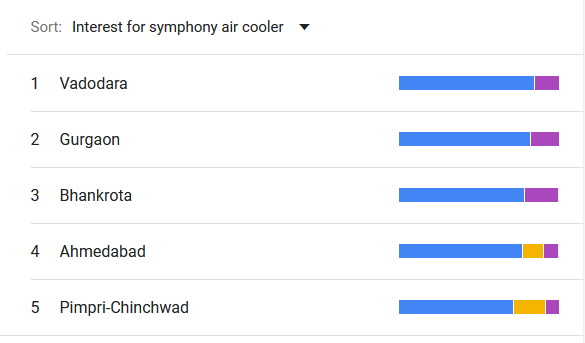

Top 5 cities where Symphony is searched the most. In Vadodara and Gurgaon, Symphony has a search strength of 85%

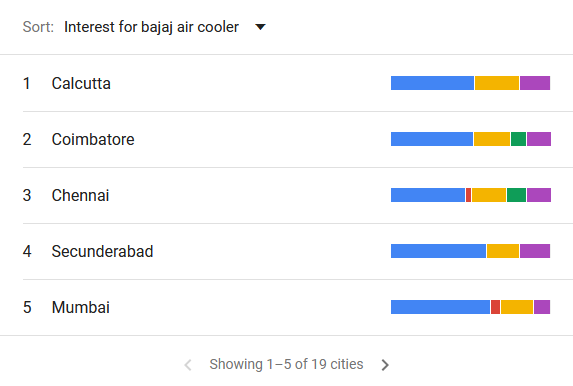

Bajaj Electricals has the second highest search share. Here is the list of cities sorted with Bajaj. For e.g in Kolkata, Bajaj has a search strength of 28% v/s Symphony’s 53%

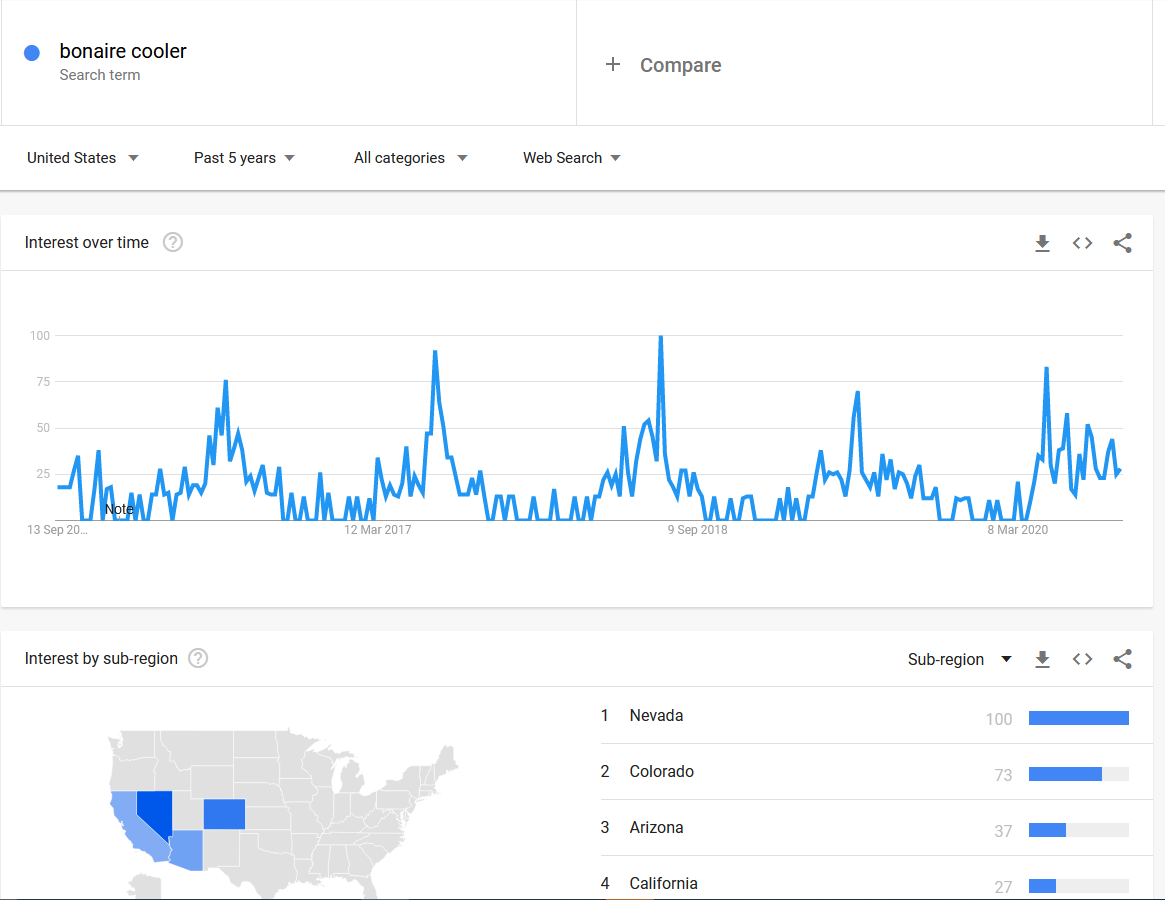

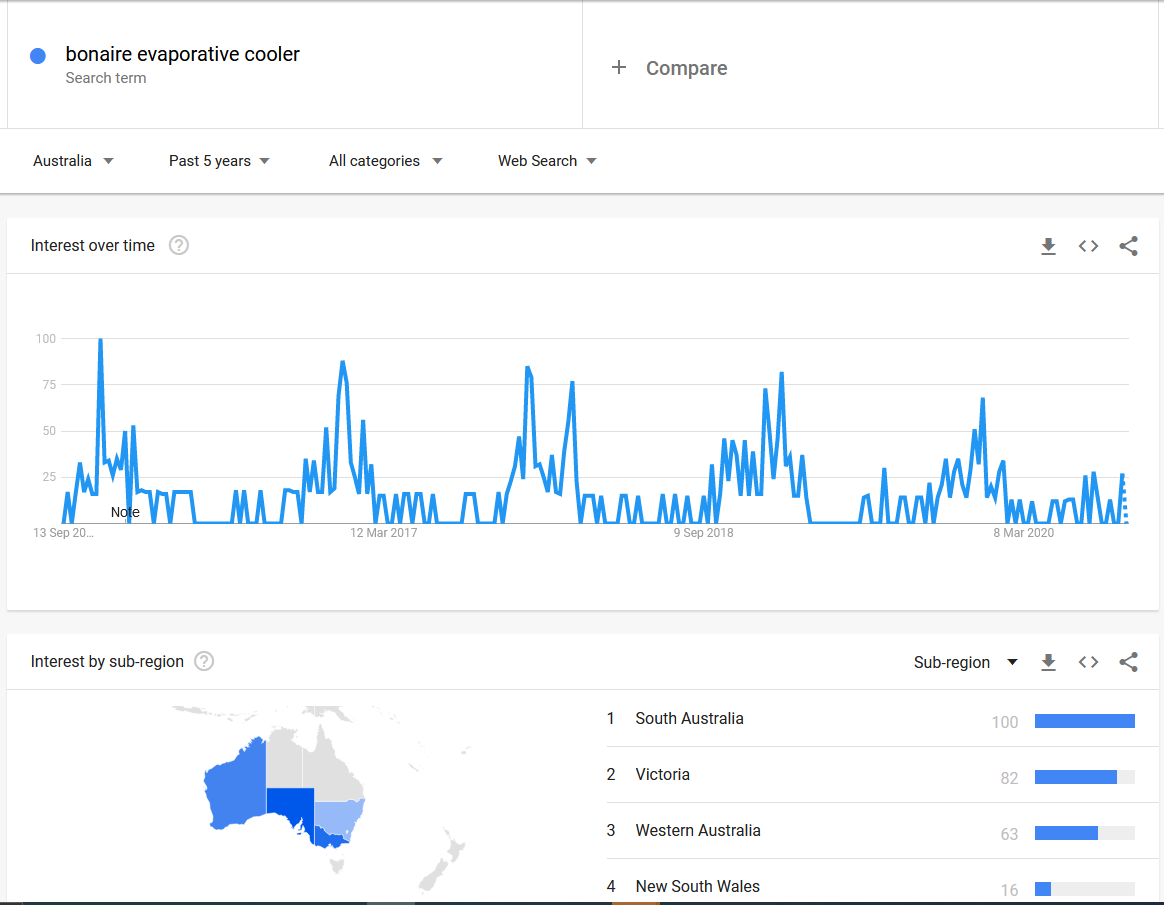

Coming to their CT acquisition, I searched for Bonaire and Celair coolers.

On Industrial Coolers, the search trends are relatively lumpy. Gujarat obviously has the highest number of searches in India. While globally, we have Pakistan, Australia, UK and US in the list

Overall, it seems there is some sort of a market for air coolers in dry regions. In India, clearly there are just 3 major players in the organized market with Symphony miles ahead of Bajaj and Voltas. How long can they hold onto the lead is anybody’s guess. Can someone explain why air coolers are not popular outside India? Is it expensive to maintain? Is it just not worth the hassle?

I see the following negatives in Air coolers when compared to ACs:

1.Product quality is poor among all brands

2.Filling up water on a daily basis involves human effort whereas AC dont need any such effort.

3.Water is a scarce resource in most parts of the world

4.Aircoolers occupy physical floor space inside a house whereas ACs occupy only wall space.

5.Difficulty in using- from filling up water, to moving the air coolers to a proper place within a room,no remote control support -> Whereas ACs dont have such drawbacks

Will air cooler industry survive say 15-20 yrs down the line?

With rising income levels, ACs are far easy to install and use compared to coolers…When the lower middle class migrates to upper middle class, demand for coolers will go down

The disadvantages as mentioned above with air cooler are logical…

But there are a couple disadvantages with conventional AC. You keep the doors and windows closed. You keep releasing Carbon dioxide in side the room after consuming Oxygen… There is no fresh air coming to your room and the stale air keeps circulating inside room.

Further , if more than one person is sleeping or sitting in a room , there are every chance of Virus infection spreading from one person to another ( Covid19 is only one type , but there are 100’s of virus which spreads human- human).

Air cooler scores better since you need not close doors and windows and so you get fresh air . And Rural poor which currently consists of 60% of indian population can nnot afford an AC due to initial cost and thereafter electricity bills. The same thing is true with many other underdeveloped and developing countries.

Also with Air-cooler, you save the planet earth from Global warming by reducing consumption of electricity which is produced by burning fossil fuels like coal, Diesel, Gas…( Which produce heavy carbon dioxide)

So, both need to go side by side…

However the disadvantages of AC as discussed above can be overcome with HVAC ( Heating, Ventillation Air conditioning) system where fresh air is inducted intermittently after filtration.

This technology is currently available though cost is higher and many offices are already using HVAC.

While symphony has struggled over past 2 years for various reasons( mild summer, subsidiary performance, Corona impact) - thus derating of stock where it is today, hardly any participation in pull back rally either.

Seems some interesting events are lined up which may help them get the past glory back, if that materializes, they are poised for a good performance over coming quarters

There are some very aggressive call outs in Annual report with some hard numbers- for e.g. page 33

“” We believe we are

at the inflection

point from where

US$ 6 million of

US revenues ( Home depot driven)

derived by Climate

Technologies could

become a

US$ 30 million

business in less

than five years.""

“”

At Symphony, we

see ourselves at

the bottom-end of

a multi-year

J-curve in this

sector for a

number of

reasons""

That will be quite a feat to achieve and a smart mgmt like Symohony will not put it in black and white unless there is pipeline visibility.

Last 2 qtrs they have been media shy on interviews and for right reasons, there are multiple interviews lined up in next week as well as investor calls, all of this right before peak summer season, expect a good pick up in distributor orders for upcoming summer and Symhony gaining market share with unorganized players suffering as aftermath of covid, as well as air cooler experimental organized competetion focusing on core space.

They have been quite vocal about Industry and commercial range to be next driver of growth in addition to retail, its overdue to show in performance, expect some concrete updates here. Some good traction articulated in Annual report as well in regions on some very large brands using these solutions( Walmart, home depot, India - RK marble, Chokhi Dhani etc)

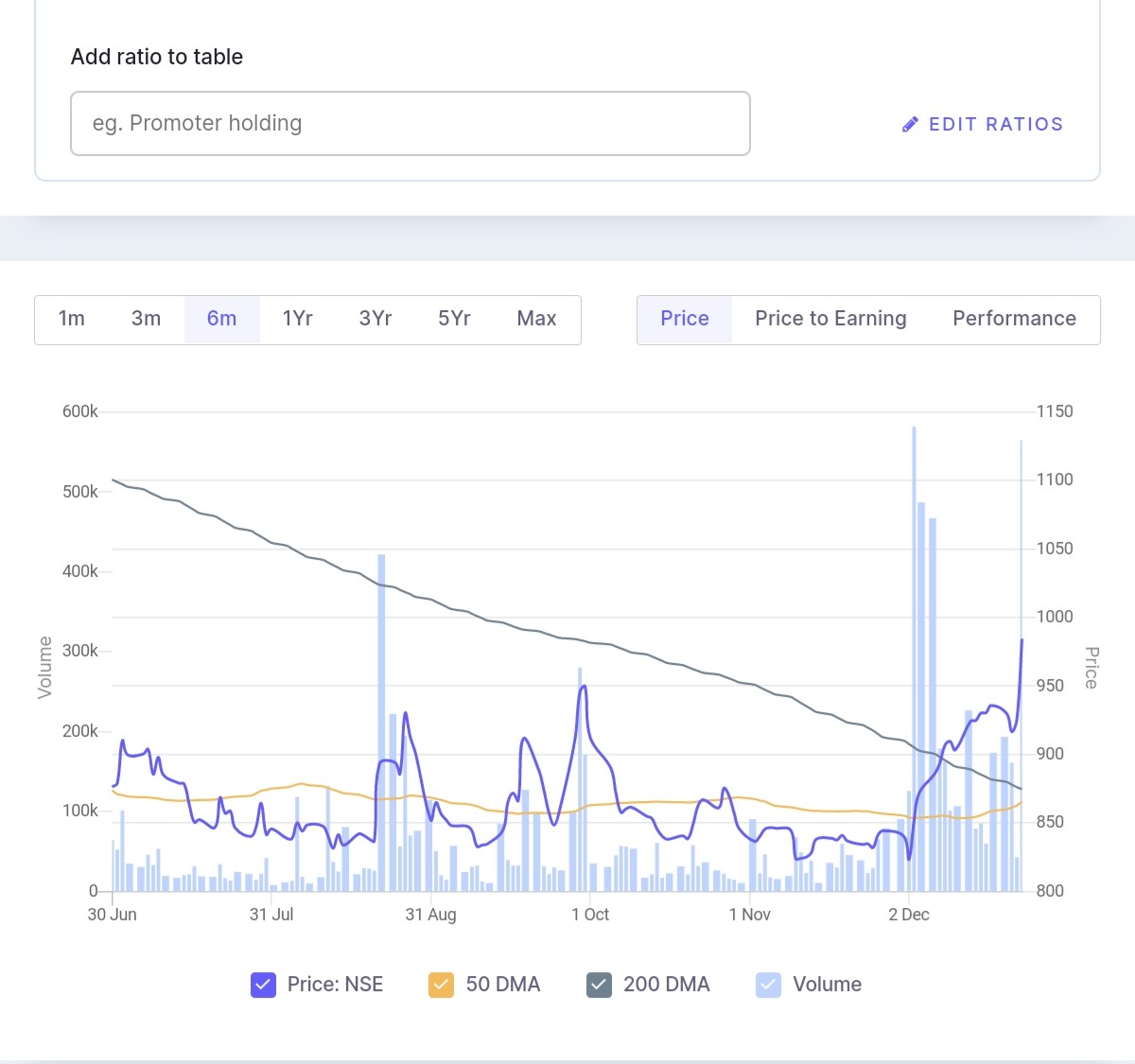

Technicals telling a price volume action in last few weeks with heavy volumes and taking out of 50 and 200 MA

Given that they have clearly articulated in Annual report on efficiency iniyiatives across each geographies ( market/ solution/ tech know how/ production base ) - though this has taken longer but they have been transparent and fast learners, some of cost initiatives are bound to improve bottomline especially in Climate Technologies ( e.g assembling vs production, outsourcing of call center and digital marketing to India) etc will deliver quick results.

Likely beneficiary of WFH trend as well with strong brand and reach

All in all a bet on quality management and early signs of green shots, reasonable valuations for a strong balance sheet with sizable cash reserves and past track record.

A glimpse into what Symphony is trying to break into, potential is to create another symphony itself- just by playing climate products right in USA alone…air cooler market in USA is going to be $2.2B by 2025( could be earlier given ESG push and govt policies support), current market size is $1.5B in 2019 - with Bonaire from climate technologies being a successful product via Home depot and now on Amazon too ( see product reviews here https://www.homedepot.com/p/Bonaire-Durango-4-500-CFM-3-Speed-Window-Evaporative-Cooler-6280030/204679889 ),

$5M sales from USA currently is nothing to what Symphony can achieve- even a conservative 5% market share is a $100M potential- creating a New Symphony itself. With all blocks in place ( low cost mfg in India and China, product quality acceptance for Bonaire range, Symphony way of asset light model giving cost advantages etc)…lot is to unfold in coming years

Below are some of triggers and market dynamics playing out per report summary ( its a paid report but below is summary)

The North America Evaporative Cooling Market was valued at USD 1.50 billion in 2019 and is expected to reach USD 2.20 billion by 2025, at a CAGR of 3.71% over the forecast period 2020 - 2025. The North American region has been witnessing an increasing number of initiatives for sustainable energy management. Therefore, traditional air conditioning is not a feasible option. This factor is driving the popularity of evaporative cooling, which is fast becoming the most efficient option, for cooling large areas or open spaces. Evaporative cooling enables firms to gain cooling benefits without adverse effects on the environment. It has become imperative for firms to adopt sustainable practices for their production and HVAC operations, to mitigate risks of environmental pollution.

Various government standards have been implemented in the region, specifically, in the United States, for the efficient use of energy across commercial and industrial sectors, with evaporative cooling technique. Therefore, the Natural Resources Canada is considering increasing the minimum energy performance standards (MEPS) for evaporative-cooled products, to align with the MEPS in the United States, for those classes of products. As evaporative cooling makes use of a natural process, namely the reduction of air temperature by evaporating water on it, they are the preferred alternative over the traditional cooling technologies.

Evaporative coolers offer several benefits to end users, including energy savings, cost effectiveness, low maintenance, and operational requirements, besides being multifunctional (can be used in an open environment, for cooling, air purification, and ventilation). Thus, owing to favorable regulations for sustainable energy across the region, advancements in technologies and their benefits compared to traditional cooling techniques, are significantly driving the market studied.

The other major driver for the US segment is the adoption of evaporative coolers in data centers. The demand for data centers is growing at a brisk pace in the country, with the rapid adoption of Big Data, digital content, and e-commerce. Keeping these facilities constantly functional is mandatory for multinational companies operating in this space. In addition to reliability, the industry is now seeking energy-efficient solutions that have the potential to lower the operational costs and reduce carbon emissions from data center operations. In 2015, the data centers in the United States consumed more than 110 million Kwh of electricity, equivalent to the output of 500 MW coal-fired power plants.

Was wondering why Symphony annual report was titled world at 27 C, probably below is one explanation

“”“A normal data center usually requires around 0.5 to 50MW of cooling capacity, and due to recent changes in ASHRAE guidelines, the permissible operating temperature has been raised to 27°C”"

Here are my notes from the Q3FY21 concall and the last interview (link).

FY21 revenues will face a major de-growth

Launched 30 new products in last 12 months

Due to raw material price increase, cost of models have increased by 2-6% of sales price

Increasing prices in only models where there is no competitor products

Current year gross profit margins will be maintained close to 50%

Witnessed very good channel collections (better than last year), especially from the rural and semi-urban places

Expecting a turnaround quarter for Climate Technologies in March 2021 quarter

IMPCO margins impacted due to bad debt (~7.4 cr.) that happened because of bankruptcy of a large retail chain in Mexico. Climate Tech margins impacted because of local procurement of raw material due to supply chain disruption

Industrial cooler sales in India is still not substantial, COVID disruption upset the growth trend

Already supplying air coolers from India to Australia

Think that the industrial and commercial air cooler potential market size should be greater than the residential air cooler market.

Organized retail sales (including large format sales + e-commerce) ~ 15% of India sales

Short term performance ( next two quarters) looks deliverable with sound performance given poor base in last yr and low expectations from mkt as of now given last 2 years performance - risk reward favorable as any revival will give good returns given company credentials and business model

India vs Global is around 40:60 in revenue split

India they sound confident for market share gains, maintain gross margins despite cost rise

demand scenarios for India mkt good as per their trade channel, intact they believe its not pent up demand case, consumers sentiment is strong, highest collection in Dec

india market share gains thesis - Unorganized sector - supply chain issues in most fy20, smaller player shutting down, consolidation benefits to symphony, other organized player can’t produce much due to supply chain issues of parts - symphony has ready low cost inventory due to year around manufacturing

Global biz - major part is Climate - confident about Climate tech turnaround in Q4( long pending) -

symphony Australia orders from india are booked already, couldn’t be shipped in Dec qtr, will show in Q4 - these shipments add to Symphony India topline and retained margins

supply chain reorg- climate technologies will get full products in cooler from symphony India( already happening). Heaters components will be from symphony india - this will help climate delivering better margins and cost advantages to compete better- local sourcing setup at competitive cost in place in India( earlier china)

Industrial segment is insignificant as of now.

Invested - with a lesson that overseas acquisition are not quick turnaround for Indian players( factor buffers in mgmt claims), no matter how great company and management is - there is limited they can deliver in bad times( hence entry price is imp for quality as well) - all in all things are finally looking up again - unless we get a poor summer

Climate has delivered on topline, will catch up 9n bottomline

homedepot 25Cr/Qtr additional biz generated- sustainable- US biz has contributed 90 cr in FY21 topline, expect this to double next year- and this will be at higher margins

eCom 100% plus growth YoY

There is no reason to believe that they will not exceed last year PAT of 180 cr - mgmt seemed confident and still cautious.

In my view result and management commentary is very positive. Highest ever Revenue and PAT. Good growth in US and Australia business. I don’t understand the reason for today’s fall. I know one day movement doesn’t matter but just after a day of spectacular results ,it should not have fallen this way. I would have understood the fall if Results were priced in but that is not the case here. Am I missing anything here?

Very good demand witnessed in India until April; 70-75% of Indian market is still unorganized and symphony has broadly maintained their 50% (by value) market share among organized companies; Symphony’s estimate for Indian air cooler is ~80 lakh/year and ~4000 cr./year

Symphony makes 10% excess EBITDA margins compared to Indian peers who make 13-15% at EBITDA level largely because of the premium pricing commanded by the brand

Inventory lying with symphony and within the channel is similar to normal levels

Spent additional 8cr. in quarter on advertisement in expectation of a good summer

Have launched 30+ models over the last 2-years

Gross margin for FY21 has come down to 45% vs 47% in FY20 (sharp increase in freight cost, raw materials). Couldn’t pass on all of the price increase and will do it gradually to take margins back to 50% for standalone India business

Not willing to share numbers related to domestic industrial segment, e-commerce vertical and modern channel sales

Rest of world business contribution > 50% of overall revenues because of very sharp de-growth in India (-32%; 431 cr.) and slight growth in ROW business (4% growth; 469 cr.); Witnessed highest ever quarterly consolidates sales surpassing June 2019 quarter

Acquisition of Climate Technology was done by loan which is being served from accruals of Climate Tech and its current interest rate is 3.6% (in Australian dollars). Repayment of this loan will require more than 3 years

March has been a turnaround quarter for Australian subsidiary Climate Technology and expect it to perform according to expectations at the time of acquisition; Sold 21cr. worth of air coolers in US (to home depot) sourced from India and overall ~25cr. during March quarter and this should be a great opportunity; A large amount of incremental orders for Climate Technology will be sourced out of India; Total sales to US has been $13mn (~95 cr.) during the entire year

Any idea about industrial air coolers market in more developed countries than India? Just to extrapolate what can happen in next 10 years…In interviews they are promoting very big way about what they can achieve in industrial air coolers.

Important Announcement

We are pleased to inform you that Board of Directors, at its meeting held on June 19, 2021,

based on recommendation of nomination and remuneration committee, has consented and

proposed that Mr. Amit Kumar (DIN : 01946117) be appointed as an Executive Director and

Group CEO of the Company for a period of five years with effect from August 2, 2021. Symphony.pdf (283.0 KB)

Domestic demand was very robust until mid-April (demand was much higher than supply). Market share has been maintained or may have improved

Gross margins were maintained at 48% and operating margins were lower due to ad expenditures. Very confident of going back to normal margins (domestic gross margins of 50%) because of new product launches where they do not face any competition and have pricing power

D2C: Launched e-commerce platform with a few exclusive products such as cooling fans

A lot of commercial air coolers have been developed with the support of GSK China

Overall channel inventory is lower than June 2020

FY22 sales should be in-line or slightly better than FY20 (unless there are unforeseen covid waves)

India

o To take care of unsold channel inventory, undertook a stock compensation plan where a discount was applied to the entire unsold inventory

o Launched a range of products specifically catered to the needs of rural and semi-urban customers (called Bharat)

o Five oldest models accounted for 16% revenues and the ten youngest models (launched pre-FY21) accounted for 23% of revenues

o Ad spends: 22 cr. (vs 39 cr. in FY20)

o Maintained 50% market share of organized market

o Launched 4 new models (vs 21 in FY20)

o 25000+ touchpoints and caters to 18000 pincodes (19000 total pincodes)

o Net promoter score of 81

Australia

o Higher revenues were on the back of increased heater offtake

o Provides access to the US market through Home Depot and provides seasonal complementarity as their summers corresponds with India’s winters

o Large number of products will now be supplied from India

o Extended presence in refrigerated air-conditioning market with Bonaire brand

Mexico

o Generated ~178 crore revenues in last twelve years and the aggregate profit has more than paid for the acquisition price

o Large number of products will now be supplied from India

o Passed on 10% price escalation to customers

China

o Helped moderate components costs, strengthen competitiveness of Indian operations

Established Brazilian operations (Symphony Climatizadores Ltda) which will import range of Industrial and portable coolers from Symphony India and from GSK China and distributes in the local market.

Average decrease in remuneration of employees other than Managerial Personnel is -6.45% and average decrease in remuneration of Managerial Personnel is -30.93%. The criteria for increase in remuneration of employees other than Managerial Personnel is based on an internal performance evaluation carried out by the Management annually, which is further linked to the overall performance of the Company

Symphony is an interesting case as an out of favor stock at current levels of ~900 odd. Changes in perception can lead to big swings on the level of valuations assigned. Symphony is a perfect case for this if we look at the 2009-2016 era of strong domestic revenue/volume growth and the peak multiples being assigned then. The general consensus was very low HH penetration & Symphony’s dominance + strong volume growth demonstrated (FY09-FY16 superb run) should ensure a long runway of profitable growth, hence the heavy multiples which got assigned. Shift to the next 4-5 years, where it’s fair to say domestic volumes have been very lumpy, somewhat flat, specific reasons have hurt for some year’s growth (back to back bad monsoons in earlier years, then lockdowns in 2020 & 2021 right in the critical months of sales, very seasonal product).

1 general thought today is given the alternative of AC(Industry ACs volume growth has been much better than air coolers for last few years), its rising penetration, the runway for coolers is shorter & its actual potential market is lower.

Given the lumpiness of last few years’ volumes, it’s been a challenge to rightly figure out the volume growth potential. And repeated weak pnl nos + flat share prices do slowly shift underlying expectations towards a bearish one. Management have remained steadfast in their view that domestic still offers a decent runway. In their latest presentations, they estimated HHs penetration at 28% North, East 4%, West 12%, South 5%.

Can be a case where expectations go from overly optimistic to overly pessimistic when it comes to thinking on growth.

Domestic volume growth - This is the key factor at play for double digit earnings growth (overseas has inched up, but still domestic residential will dominate SOTP). While overseas may now have become 35-40% of overall sales, their profitability share is much lower. For sizable earnings growth vs implied quoted PEs, one needs the domestic piece to show growth.

I think both the bull & bear cases have a point when it comes to the growth conundrum. 1 being the AC vs air cooler debate. The good news for the bulls is base matters, and after years of subpar growth & hits from poor summers & ‘summer’ lockdowns in last 2 years, I would incline to the argument of reasonable volume growth possibility over the next few years. In this regards, current valuations are interesting.

1 negative on Symphony I find is ratings/reviews are average on e-commerce, infact new peers like Crompton are better. Though of course no other organized company (barring say Bajaj) provides the wide range of SKUs symphony provides.

Focus on scalability – Climate acq, and recent nos in exports to USA from India & Australia. Credit to the management here for their desire to be a strong globally competent player, onus on maintaining a good sense of technological trends in this space (spate of acqs in the last decade, sound capital allocation, bought assets frugally, successful turnarounds on older acqs), keep looking for growth opportunities outside of India. From interviews/concalls, they have indicated the global market of air coolers is ~2$bn, USA is 2100cr, now they have exported around ~100cr in FY21 - imply ~5%Mx in US.

From a domestic turnover of ~400-700cr over last 5 years, they bought a sizeable entity in Climate(~275cr sales) and worked towards achieving 100cr of export sales in US ~10% of total sales by FY21.

“No comparable company to symphony which operates in many markets. All local players whether it is US or Australia. even we don’t know size of market. Fragmented. US business fairly small, but growing rapidly, lot of potential due to strong relationships with large box retailers.”

Industrial – They were the category creators for air coolers in India, and are trying a similar playbook for industrial air coolers in India.

“Industrial AC market in India is ~10000cr, value of industrial air cooling market is undefined, symphony only branded player in this segment”

“90% of American firms named cool air as the single biggest factor determining their productivity.”

“Cooling raised productivity by a quarter. On factory floors it cut absenteeism and stoppages.”

FY14 installations 100, FY21 3400

“Most factories in India don’t view cooling as a necessity unlike china. Need to educate. Almost nothing exists in india while almost every factory in china is cooled.”

Lets wait for nos here. Recent signs point to increasing traction, given the co took the step to actually advertise for its industrial air coolers, still better to wait for nos to figure out some rough estimates.

Unlike ACs, refri, washing machines which are dominated largely by organized cos, air coolers have a huge ~75% unorganized piece. Tier 2,3 towns + rural areas, one can find cheaper local alternatives vs Symphony. So far the organized space has not been able to really capture share from the unorganized(~75% 5 years back & today from management comments), the price-value equation may not be very superior to prompt a sizeable shift so far, but I’m guessing over time certainly branded cos should capture a greater share as incomes go up & the relative cost of purchase for a consumer decreases. Note how other large consumer durable cos like Voltas, Crompton etc too have gotten into air coolers over the past few years. & they see growth potential.

From a 2018 Edel report: “Moreover, of all the consumer durable sectors, air coolers have one of the highest growth potential due to higher proportion of the unorganised segment.

However, in the past 12-18 months, at least 10 new brands have entered the fray comprising established players like Havells, Voltas, Orient, Wox, Bluestar, Maharaja Whiteline, among others. The lure of a large unorganised market and profitability therein enjoyed by Symphony have led to established players making a beeline for the market.”

Overall thesis is simple:

Possibility of better than priced in growth.

Cheaper valuation multiples today vs its quoted history. ~25x FY23 PE (can differ really based on what you bake, domestic volume nos key).

Whether growth will be flat or low single digit or high single digit or even double digit for its domestic residential piece for the next 3-4 years. If we get a high single digit or higher domestic volume growth for the next few years, then there is upside. I am more inclined to the possibility we get better than expected growth.

Earnings growth resumption + some PE expansion (perception change, cyclical not structural) can aid upside.