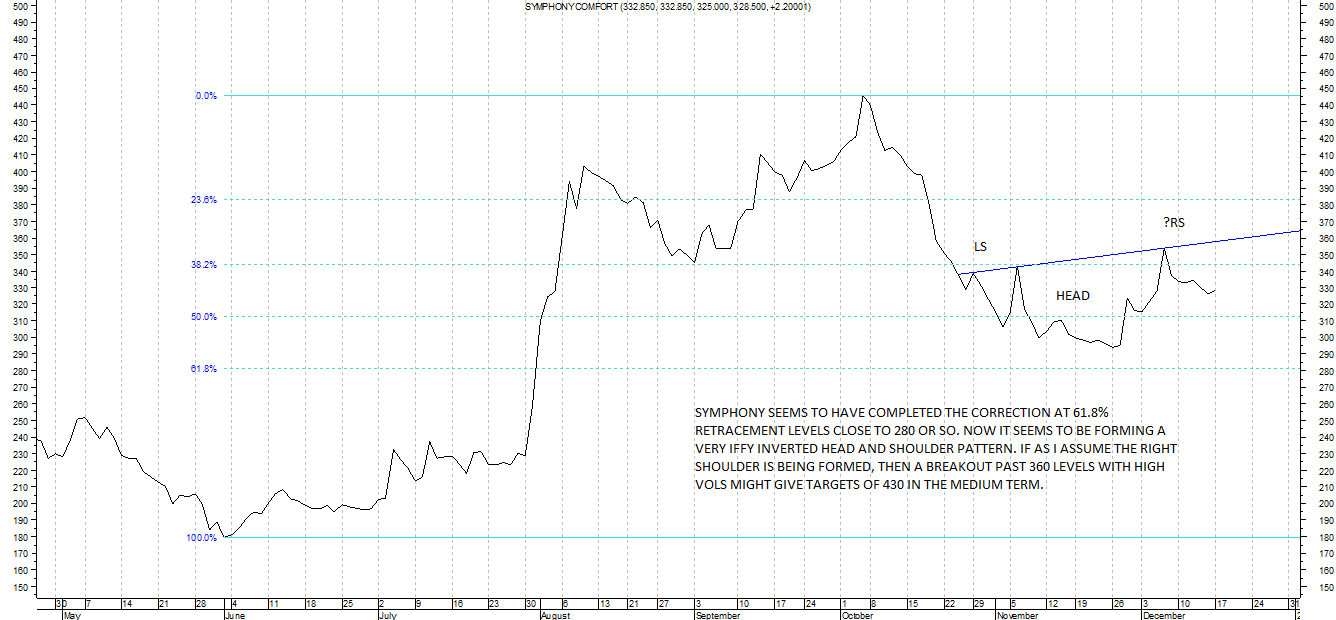

Concall details for symphony.

Some key highlights:

Keynote - This time more emphasis on qualitative overall macro than the quantitative aspects

Overall externalopportunity

Population view

In India there are250 million house holds

)- 83 mn not having even fans. (1/3rd )(33%)

)- 164 mn having access to fans and other sources to cool (65%)

)- out of these 9.4 mn having AC - (3.8% having air conditioner)

)- 5% of population having air cooler in that.

)- hugeopportunityfor symphony for many years.

)- addressing marketopportunityof 95%.

)- still 67% households of market potential to upgrade to air cooler.

Climate view of the cooler market

household in the regions having dry/hot and moderate climate.

o dry& hot - 132 mn (54%)

o moderate - 11 mn (5%)

o 143 mn target

Export

o tied up with top notch distributors in 60 countries

o non-Mexico exports (ROW) - 39%(volume wise) and 57% (value wise)

o Mexico impco having huge inventory and no further exports till the inventory comes down (expected to come down significantly by Sep)

o Exports for impco will start after that. So FY14 we can see further exports to impco.

Industrial cooling

)- tied up with consultants, appointed 32 dealers

)- For 9 months - installed IC in 55 sites.

)- major clients include marico, one of group company of hero honda, tractors India, akshardam, swami narayana, baba ashram, isckon etc.

)- continue focus on asset light, cash and carry

)- 40 sites in progress.

General

o For quarter avg improved from 5029 to 6062 realization.

o Took two price increases.

o Confident of good volume growth.

o Launched 6 new upgrades.

o Competition subdued.

o Sylvan pte increase in holdings for better fiscal management and tax handlings.

o Consolidated reporting(of subsidiary) only in the year end and not quarter to quarter.

As of April 28, domestic sales value have surpassed what has been achieved for full year FY12. Volumes also increased close to full year fy12. This is a great news since for FY 12

For FY12 the volumes on domestic -357,813 units.

For 9 months -303,371 units

So 54000 already sold till April !!!

Company bullish on volume growth and expect sales to pick up in the coming months. Sales to dealers will happen throughout the quarter based on demand…

The concall is also available in researchbytes.com