In that case you need to see Prof Sanjay Bakshis lecture on Anti Fragile businesses. He has discussed that business of Symphony is not Anti Fragile and lot many other players have entered Air Cooler space. (Presentation available on India investing conclave)

The stock went up 30% and is back down to 1100-1200 levels. Can anyone discuss the reason?

Is it due to the new cooling policy of the government or because investor are exiting the stock to book profits?

In the latest interview Mr. Nrupesh Shah calls out the estd. market size for many of the overseas regions they operate in. Collating the information below from his latest interview and my notes earlier. This completes the puzzle to a certain degree on the opportunity size they are working with.

-

India residential cooler market = ~ Rs. 3500 - 4000 crores (Overall market growing at 12% y-o-y. Organized market growing at 18% yo-y) (source: https://www.youtube.com/watch?v=LqrybOSi1t0 )

-

India industrial / centralized cooler market = ~ Rs. 4000+ crores (picked from Symphony’s corp presentation)

-

Exports from India (focused on 15 - 17 markets) = Markets nor opportunity size called out. This is also being looked to drive sales in the medium term. (https://youtu.be/iLT5I-r2Pnk)

-

Aus + US Market (through CT) = ~ 3000 crores (https://youtu.be/iLT5I-r2Pnk)

-

**China Market (through GSK)= ~3500 crores (local market) + ~1500 crores (export market size opportunity from China) (https://youtu.be/iLT5I-r2Pnk)

-

**IMPCO Mexico = ~400 crores (https://youtu.be/iLT5I-r2Pnk)

-

**Brazil subsidary = Good potential market. Estd. opportunity size not disclosed. Company just about starting out here. (https://youtu.be/iLT5I-r2Pnk)

Symphony’s consolidated sales last year were Rs.844 crores and they are sitting on an opportunity size of 12,000+ crores at the least of a growing cooler market worldwide.

Disc: I continue to remain invested here and see the business as a good one to hold at least for the next 5 years (been an investor here since Jan 2014. Symphony is a top 5 holding for me).

2 Likes

Any thoughts on why Symphony will be able to capture greater share of these markets? What are its competitive advantages?

Not sure if these are competitive advantages or not, though here is why I believe they are capable of growing:

-

The company is focused on one thing - that is selling coolers. Their goal as a company is simple. Make one product and sell it all over the world. I reckon this makes them a focused player in what they do.

-

Innovation in the coolers they come out with. The chances of Symphony coming out with an improved or a new category within the cooler segment is quite high. This gives them somewhat of an edge over competitors (albeit a minor one). Industrial cooling opportunity is an off shoot of this innovative streak of the company.

-

Trust they’ve built with the customers over the years they’ve been selling coolers. I reckon, the brand name ‘Symphony’ stands for something in the cooling industry.

-

The management team. Mr. Bakeri is leading the company in an exemplary way. With many years still to go under his stewardship, I think Symphony can continue to scale greater heights.

-

Leadership position in countries like India, Aus and Mexico. Also, the opportunity to be leaders in other countries, esp. China considering it is a fragmented market (as per mgmt commentary).

-

Their unparalleled distribution in their main market of India.

-

Export opportunity that they can tap into over the medium term. They are yet to meaningfully start looking at this.

All of this helps me have the conviction I have in Symphony.

2 Likes

Another point to note is that that market size is increasing with the recent heat waves in Europe. But this will bring in even more competition. So only the fittest will do well.

1 Like

I was surprised to see that nobody mentioned this article here. It’s been a while since this happened, and I posted it on the “Great articles to read on the web” thread then, but I’m posting it here for the obvious relevance to the topic.

I completely agree with Sir Branson. This is also one of the reasons I was always reluctant to invest in A/C companies. The current technology we have for A/C is due for an overhaul. Somewhere down the line, when the massive usage of A/C hits the world (Asia more specifically), we will see considerable damage to the environment.

What’s worse is the fact that the chlorofluorocarbons and hydro-chlorofluorocarbons, the greenhouse gases released by the usage of A/C, eventually lead to increase in temperature. This will in turn increase the demand for more A/C. And so on. Indeed, this is a positive feedback loop. While that may sound good, in this case it’s clearly bad.

And all this is before we even consider the electricity / power usage problem linked to massive A/C usage.

Unless there are already advances in green cooling systems (I don’t think there are), Sir Branson’s challenge makes a lot of sense for many reasons.

1 Like

Symphony don’t make A/Cs. All their sales are from coolers.

Aren’t coolers supposed to be green products? Symphony certainly claim so. And I think what they claim makes sense. Coolers work on simple tech.

In the light of this, aren’t they better than AC’s as they don’t release CFCs?

And also as they are not impacting the environment, it makes their technology more sustainable from an environment pov.

Also I reckon, for something new to come up and disrupt things at scale will require a decent amount of time too.

https://www.symphonylimited.com/coolopedia-resources-aircoolers-and-airconditioners.aspx

1 Like

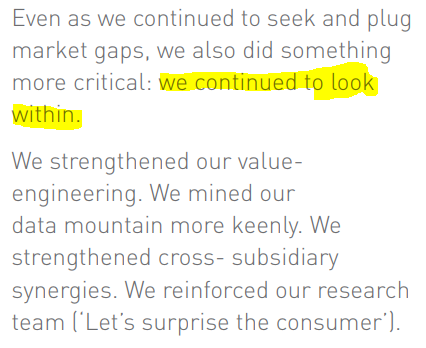

Also, this was pointed out to me in a WhatsApp group, that Symphony’s AR was weird read. So, I went ahead and took a peek myself. Some golden nuggets from Symphony’s 2018-19 AR:

Eye of the Storm

The AR is titled ‘Eye of the Storm’ for some reason. But again, there is one whole page dedicated for just this:

Umm… okay?

But wait… there’s more

Is it just me or is the metaphor nowhere close to what they’re trying to convey? Also, what is the need for the metaphor anyway? Why not just lay out the info as it is?

Questions and Answers

This is followed by some very generic questions and equally generic answers about the industry:

Cooling will be a lifestyle statement? Really?

The Pareto Principle

This could be just me, but that reads like a text you send someone in WhatsApp.

We worked closely with our larger dealers. Remember the Pareto Principle?

Nietzsche inspires an Air Cooling company

We can certainly expect more quotes from “The Birth of Tragedy” in the future ARs, I suppose.

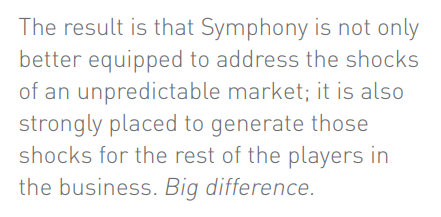

Surprise the Shareholders!

Excuse my french, but that sounds like a steaming hot pile of nothing. Actually if you read through, you will realize that there’s no additional lines backing their “value engineering” or “data mountain”. So much for the hype!

Punch Dialogues

Please tell me you see the resemblance to a Bollywood Punch Dialogue.

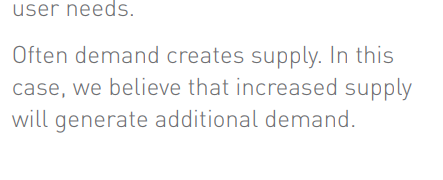

Economics Redefined

I think Adam Smith just rolled around in his grave.

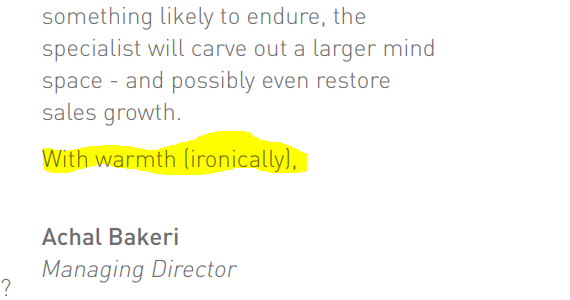

Ironically…

I’m sure that terrible pun deserved a couple of smileys too.

Pages 6-17 in the AR are full of this weird, philosophical dialogue and chest-thumping. Do give it a read. I couldn’t bring myself to read through the AR after this.

8 Likes

When I went shopping for coolers in a Tier-3 town in TN for my grandparents couple of months back, of the 4 shops I looked at, none of them stocked Symphony coolers. This was strange as the last cooler I bought from the same town was a Symphony and everyone had them then (back in 2014 or so).

Apparently they are too expensive for the townsfolk and no one buys them, so they have stopped stocking them. Only ones available and moving well were Crompton and Voltas. I ended up buying a Crompton which was just as good as the old Symphony it replaced at the same 2014 prices. The AR sounds very delusional and I think the days of mindless margin expansion are over as the competition is offering a lot of value in comparison.

12 Likes

With R32 being available in India, ozone layer is now safe. Better and safer refrigerants will be discovered and may replace R32 sooner or later. However the basic principles of AC may be retained for many use cases as we have seen that other alternatives are less efficient. Some use cases may benefit from Peltier model but not all. Similarly we saw that a body wearable (AC) can help better heat exchange between our body and environment and it can be a good option for someone who is outdoor. However it may not replace an AC.

Every business has potential to be disrupted. So we may have to watch out anyway. However this industry seems less likely to be disrupted in the short term to medium term although the refrigerant used may be upgraded from time to time.

1 Like

Same type of incidence happened with me though in T4 town when buying for Mother in law, shopkeeper had symphony coolers but told me they are very costly when I enquired and ended up buying local brand which was 40% cheaper( on my In laws insistence)

1 Like

This was the same conclusion I drew when analyzing Navin Fluorine who still haven’t bothered to get into R-32 or R-410a which could end up being a big risk for them.

2 Likes

![]()

6 Likes

the company and the video are both highly priced.

COVID-19 lock down hit hard on air cooler and AC companies.Normally, March, April & May are their main months of business of the full year. Due to lock down they are not able to sell the products and are starring at cost to due piling of lot of inventories at factory level /distributor level and dealer level !

Also, govt has banned E-com companies to deliver non-essential products during lock down period. Hence, they lost full year!!

1 Like

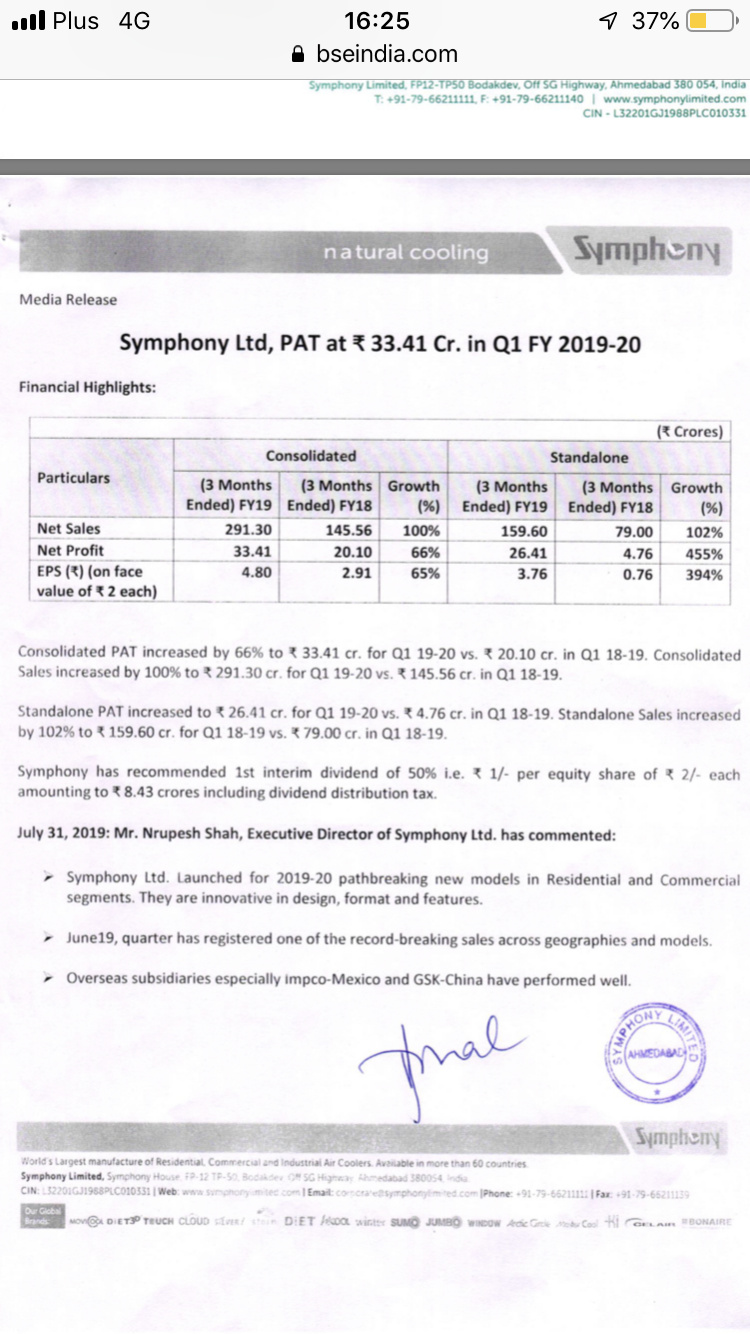

Good performance

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=144f500d-7ae9-4c49-baed-f05061af08ac

Symphony Ltd, PAT up by 84% to ₹ 186 Cr. up from ₹ 101 Cr. in FY 2019-20 despite COVID-19 impact in Q4

Consolidated EPS at 26

Domestic biz going very well till Q4 - numbers speak, May biz has been good, expect channel inventory to clear if summer lasts with intensity till June end.

New launches has been received well in commercial spaces, Expect Covid issues to be blessings in disguise for coolers.

Int biz holding okay( china been impaired) , key is they plan to use Australia/US and Mexico subsidiaries to act more like front for mfg in India. Feel int biz need to yet deliver on fin performance improvements.

Optimism in overall commentary. Like promoters and asset light rigor. Very high/ negative RoCE, debt free and valuations at good level from long term avg as well.

Invested and added in last 30 days.

2 Likes

Covid Impact will be visible in Q1FY21 , also China subsidiary is a Q mark with recent china-India sentiments , how that business in China will pan out is a Q mark but i have faith in the mgmt capability …lets see how it will pan out in future.

Disc : Not invested but tracking it for future investments.

SYMPHONY_COVID-19_Impact --Press release 16th July.pdf (3.4 MB)