Swiggy is a leading online food delivery platform in India, founded in 2014 by Sriharsha Majety, Nandan Reddy, and Rahul Jaimini. The platform connects users with a wide variety of restaurants, allowing them to order food and have it delivered to their doorstep. Swiggy operates in multiple cities across India and has expanded its services to include grocery delivery (through Swiggy Instamart), pickup and drop services (Swiggy Genie), and even Swiggy HealthHub for healthy food options.

Swiggy has revolutionized the food delivery landscape by offering fast delivery, an extensive selection of restaurants, and features like live order tracking. Over the years, it has attracted substantial investments, cementing its position as a major player in the Indian food-tech sector.

The app is known for its user-friendly interface, offering seamless browsing of restaurant menus, placing orders, and making payments. Swiggy also offers various deals, discounts, and membership plans, such as Swiggy One, which provides users with benefits like free deliveries.

Swiggy founders have played it smart before their IPO:

Co-founders ‘Sriharsha Majety’ and ‘Nandan Reddy’ have sold shares of their company from July to September 2024 through secondary transactions. While Majety offloaded a stake worth Rs 196 crore ($23 million), Reddy sold shares amounting to Rs 101 crore ($12 million) as per the DRHP. Isn’t that a bad signal?

NO, it’s all well planned!

As per Swiggy’s ESOP Plans of 2021 and 2024 disclosed in DRHP, both the co-founders have been issued ESOPs of total ~5.5 Crore equity shares in the company which at current secondary market value stands at over a whopping Rs 2,200 Crores!

In India, ESOPs are taxed twice - firstly when esops are getting exercised, the difference between the exercise price and the fair market value is taxable as part of your salary, and then at the time of sale of those ESOPs converted shares on the capital gain, if any.

The first level of taxing can be treacherous for most founders as you have to pay the tax as per your income tax bracket (~30%) in a given year even if you didn’t have any major cash inflow, as all you have in hand is ESOPs with ongoing vesting period.

This is exactly the reason why Policybazaar’s founders Yashish Dahiya and Alok Bansal had to sell their own shares in open market in 2022 and 2024 in order to generate enough liquidity to pay tax on the ESOPs worth thousands of crores which their company has issued to them.

So Swiggy founders have done the right thing by generating decent liquidity before hand so that they aren’t forced to sell their own holding post IPO and face any backlash.

Smart move!

More on ESOPs at Finding Outperformers! (pc: Business Insider)

Real issue with Swiggy’s IPO is actually the existing set of investors who might be desperate for 6 month lockin to get over!

Lets take the example of Zomato:

The ownership structure amongst Top 10 shareholders of Zomato didn’t change for 1 year as pre-IPO investors weren’t allowed to sell as per the regulatory lockin (tenure has been now reduced to 6 months). But the moment regulatory restriction got over, in span of next 24 months, 7 of top 10 shareholders completely exited as they continued to reduce their stake month after month.

In fact as per our calculations, Zomato has witnessed PE/VC funds selling of roughly 50% of its total equity capital in open market in the last 2 years, constantly adding to the free float. The names include Softbank, D1 Capital, Tiger Global, Sequoia, Tencent, Uber and many more!

Importantly, the day when the lock in had got over for Zomato’s pre-IPO investors, shares worth Rs 1,000+ crore were up for sale immediately and investment bankers were building a book for block deals at price as low as Rs 44/share which was significantly below IPO price of Rs 76/share.

Well, I am not saying Swiggy will have similar fate as a lot will also depend on the global macros post lockin gets over, but one must remember that global PE/VC investors are no way similar to promoters who continue holding in a big way - These funds have obligations to their own set of LPs and sooner or later with will have to exit from the stock - adding to the free float in a big way within short to medium term.

Read more on how Zomato’s shareholding pattern has evolved over years on: findingoutperformers [dot] com; Pic source: ET

Recently Dominos got opened at walking distance to my house (tier 3 city), and its 5th or 6th outlet in my city. Apart from that local franchises have mushroomed (south indian, north indian, cafes) at every nook and corner of residential areas (and I am not talking about street food pull carts). Even my next-to-next Neighbour has started selling home baked cakes.

My point is why would anyone pay 20% more with delivery fee when they can just step out and buy a meal. For that extra 20% I can buy ice-cream and chocolates after my meal or some snacks.

Gone are the days when there was one good restaurants 10-15km away and only few people know about them. Nowadays every second person has learned to cook good food watching youtube. Even housewives are selling cakes and other stuff from home. Every 2nd engineer, lawyer and doctor has opened chai, momos, kullad pizza, etc shops. And there’s huge motivation in them of making it big, even more than swiggy and zomato.

Everything can be found using google maps. I don’t believe in food delivery story, I never invested in zomato, so swiggy doesn’t interest me either.

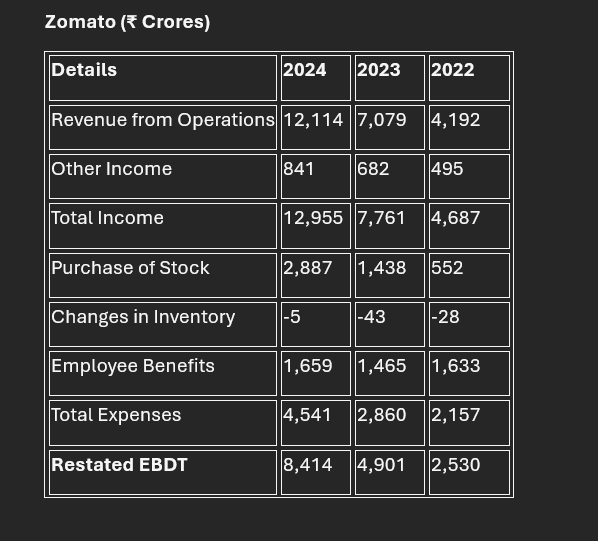

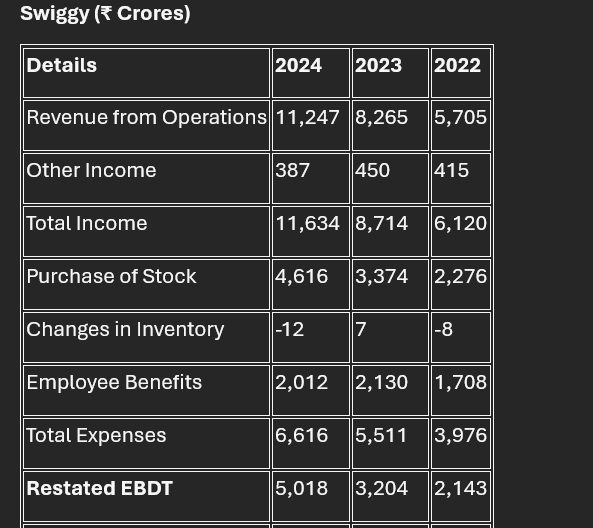

I recently reviewed a couple of Michael Mauboussin’s recent papers discussing the valuation of new-age businesses. He highlights that traditional accounting practices expense intangible assets rather than capitalizing them. Since intangible assets form the backbone of new-age businesses, unlike the tangible assets of traditional businesses, it is essential to rethink how these intangibles are accounted for.

Michael explains that intangibles, often expensed under Selling, General, and Administrative (SG&A) expenses, primarily include customer acquisition costs. These investments provide benefits over several years, not just within the financial year they are incurred. Therefore, traditional GAAP/IFRS standards fail to accurately reflect the financial health and performance of new-age companies. Financial statements, under these standards, are limited to presenting a true and fair view of accounting transactions rather than the overall business’s operational reality.

To address this, financial statements for new-age companies need to be restated to accurately depict their business activities. This analysis attempts to restate and evaluate the financials of Zomato and Swiggy compared to Hindustan Unilever Limited (HUL), a leading traditional FMCG company in India.

For simplicity, expenses such as advertising, promotion, delivery charges, and other similar costs in the Profit & Loss (P&L) statement are capitalized instead of being fully expensed in the same year. Interest costs related to these capitalized expenses are also included. While employee costs could also be capitalized, to remain conservative and avoid inflating the bottom line, they have been expensed as per the original statements.

Below is the restated P&L for Zomato and Swiggy over the last three years:

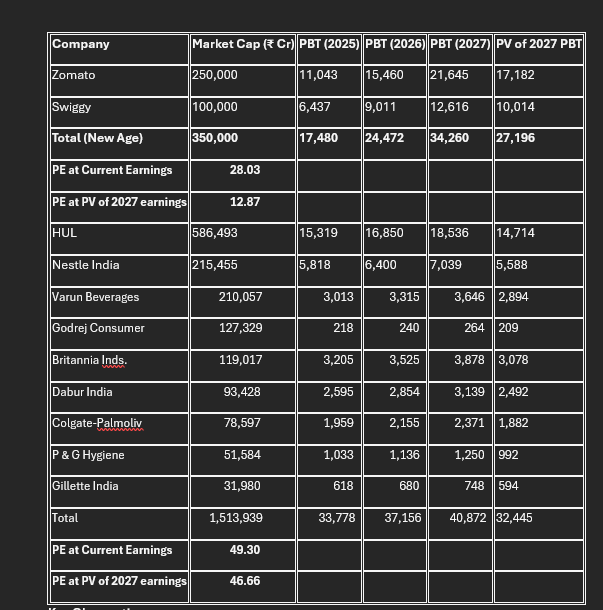

To analyse further, the restated profits for Zomato and Swiggy were projected for the next three years (assuming a 40% annual growth rate). Their performance was then compared with major FMCG companies in India, assuming a conservative 10% growth rate for the latter.

Traditional FMCG companies trade at high Price-to-Earnings (PE) ratios of around 50x even when future earnings are discounted to present value.

In comparison, Zomato and Swiggy appear undervalued, with far superior growth prospects. A 40% growth rate for new-age businesses is likely conservative.

Conclusion

Traditional valuation models under GAAP/IFRS inadequately reflect the true profitability and potential of new-age businesses. As shown, Zomato and Swiggy, when restated, showcase strong financial performance and significant growth potential.

Opportunity hiding in plain sight!!

I would hold Swiggy for long term and would love to buy on dips and the major reason is the flats t in bangalore and other metros that are construted, are outside the city; hence, Swiggy is lifeline for many and i believe since land is limited, this trend will continue

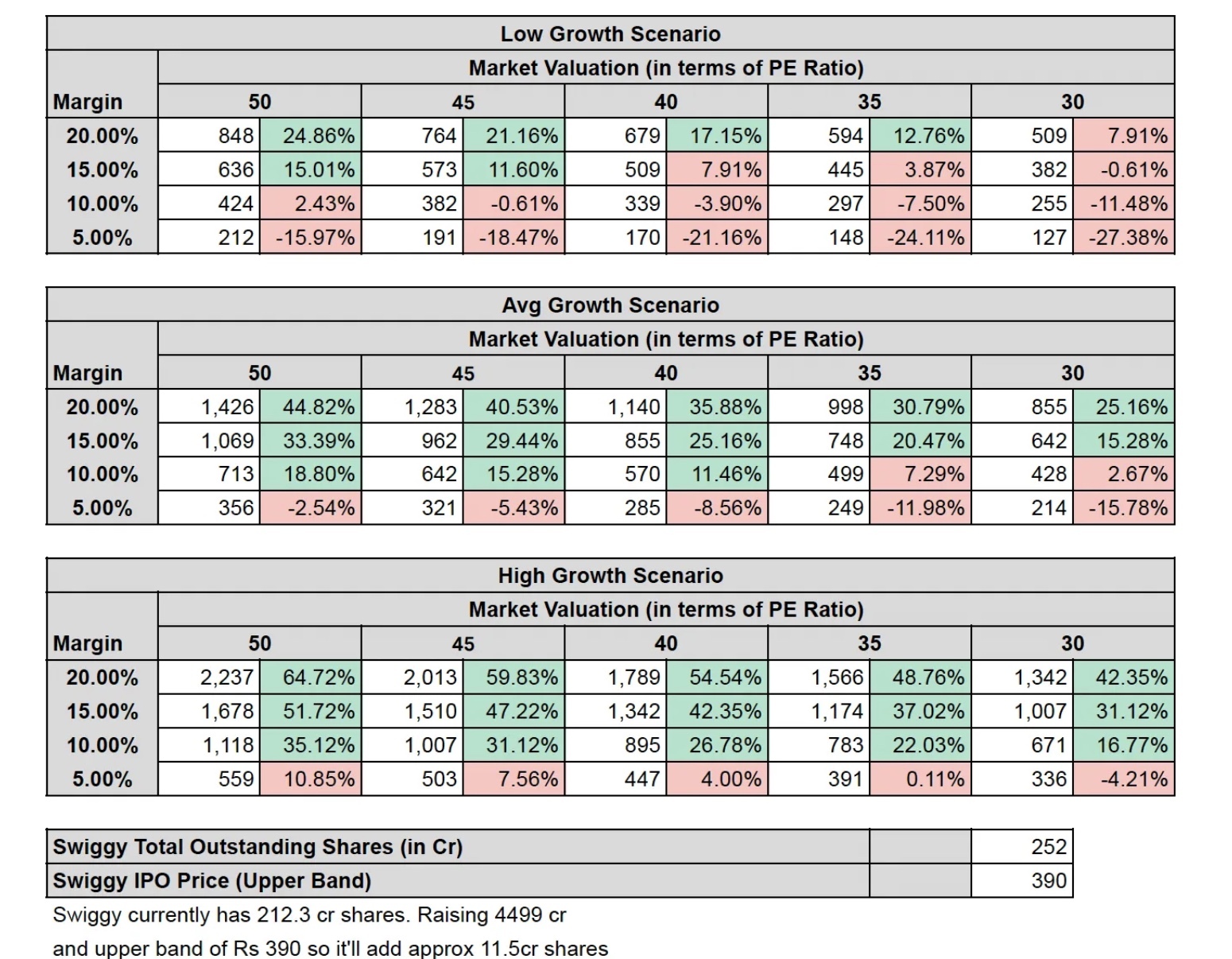

@Vivek_Kalavadiya Regarding your valuation, I think the revenue targets are just too conservative. It seems like you are projecting 15-16% annual revenue growth. The last QoQ revenue growth of Swiggy was 30%.

Here are mine where I assume the conservative case to be 20%!

Additionally, on the other hand I think a 25% margin is just too optimistic! I’d run a sensitivity analysis with multiple valuations with margins ranging from 5-25%.

You also have a gradual shifting of margins but I feel most likely Swiggy will do slightly negative margins for 3-4 years more before switching to efficiency mode where you will very quickly see the margins settle around whatever is possible due to unit economics. (Currently, Zomato is able to get 16% gross margins in food delivery and it remains to be seen what quick commerce settles at).

Here are mine (I haven’t run a DCF, not a huge fan of it) for pricing multiples

I agree with you that tech companies should have certain costs capitalized. However, the question is which costs.

I actually think employee costs should be (at least partially) capitalized as they mostly build the software whose benefit is realized over several years.

I see no reason why a transactional cost such as delivery charges should be capitalized. With advertising it is a little tricky but I would lean towards expenses rather than capitalizing as Zomato/Swiggy aren’t very stick - people frequently shift between the apps.

Also, I am not sure how you are calculating interest expense related to these capitalized costs? Can you elaborate. I would amortize them over a certain period instead (e.g. 3 years for software development costs)

Actually if you see in any normal business any project cost includes every expense that happens till the plant is put to use is capitalised.

Now these companies do not have any plant as such to establish but their project can be customer acquisition hence all expenses happening directly or indirectly towards customer acquisition should be capitalised.

The only assumption I can make is capitalise everything till the business gets publicly listed. Post that just like any normal business has gestation period post capex, we can treat these businesses as well in the same way.

My approach is more back of the envelope and does not include nuances to just get a fair idea about valuations of such businesses.