Swiggy is a promoter less company. They have mentioned that in their RHP.

1 Like

Got around to looking at the Q3 results of both Zomato and Swiggy and wrote down my thoughts below

tl;dr - I’m pretty bearish on both, set some really, really low price alerts for them. I doubt they’ll ever be activated ![]()

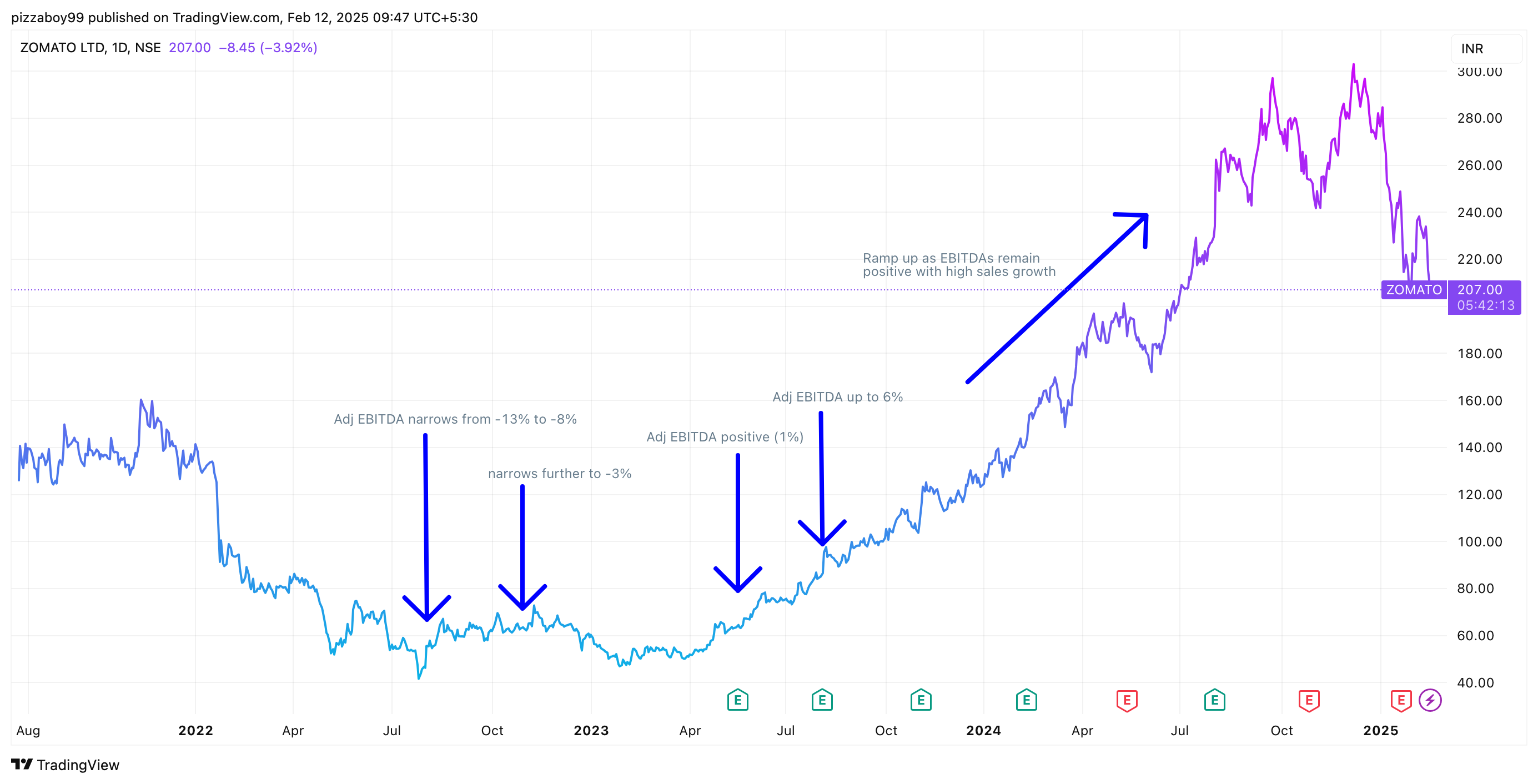

Overview of Financials

Annual Financials

Looking at the history of annual revenues and EBITDA margins, the first impression is to be very impressed with Zomato. Starting from a lower revenue base in FY22, they are now far ahead of Swiggy while at the same time managing to reduce their EBITDA margins from -44.15% to 3.92%

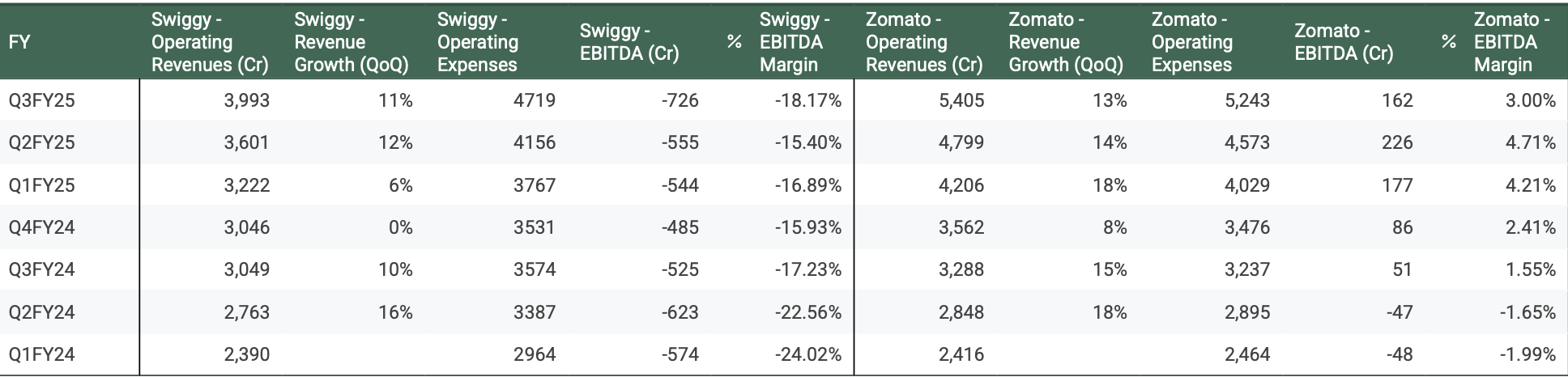

Quarterly Financials

EBITDA margins of both Swiggy and Zomato widened after narrowing for six subsequent quarters. The very obvious inference is the toll of quick commerce wars which both Zomato and Swiggy have 100% committed to.

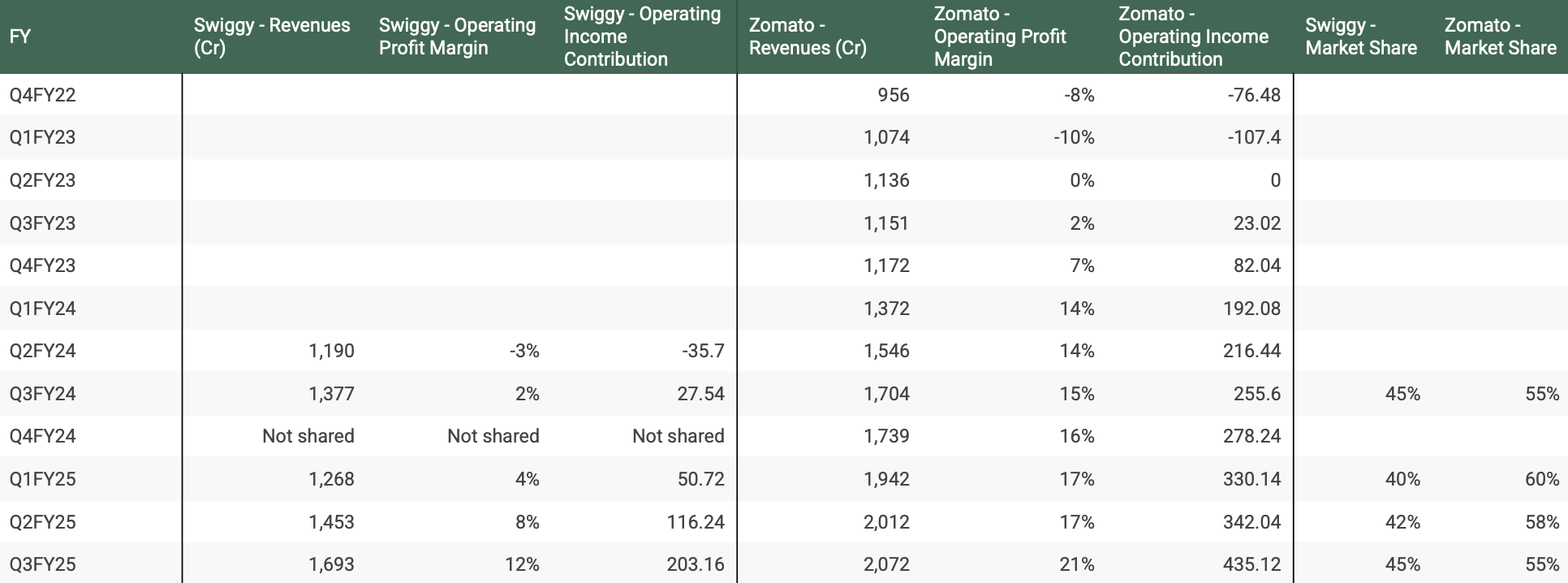

Segment Financials - Food Delivery

Zomato and Swiggy continue to enjoy the benefits of the duopoly they hold over food delivery.

While Zomato has a bigger operating revenue and income in the food delivery segment, in a rare positive for Swiggy - they appear to be clawing back marketshare and catching up with Zomato with their marketshare going from 40% to 45% since the start of the FY25.

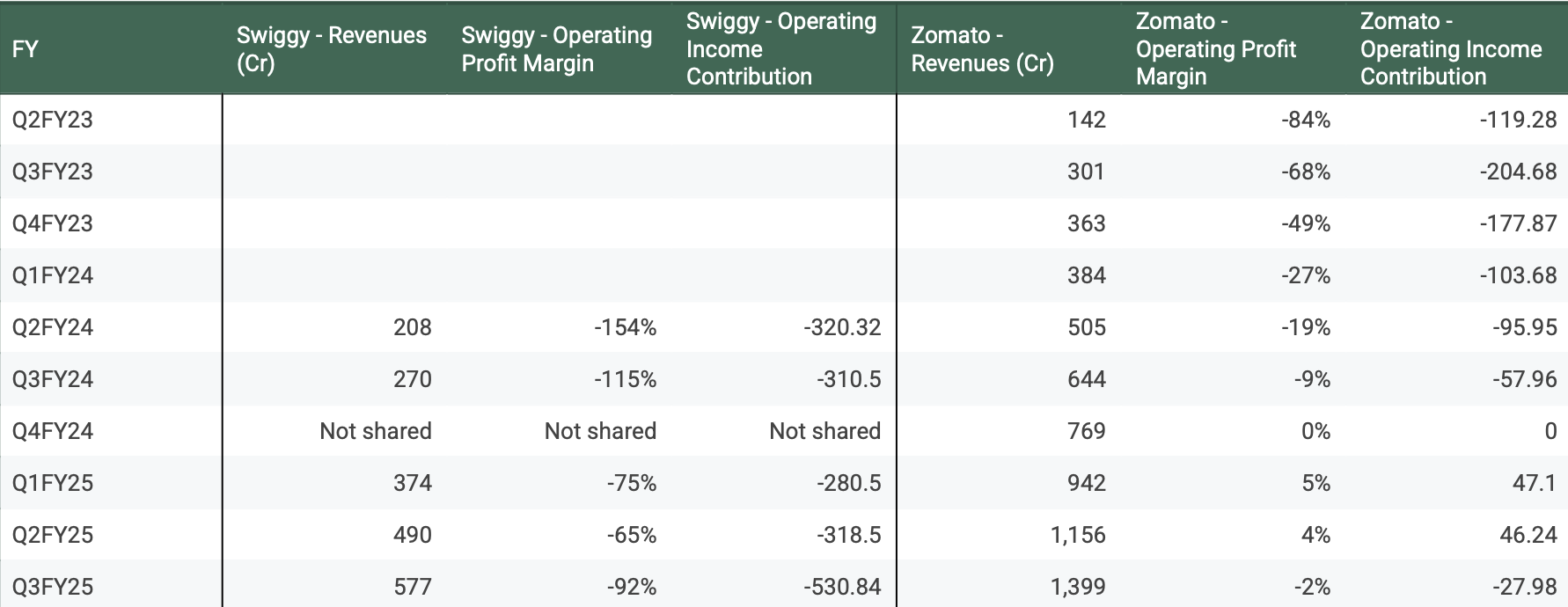

Segment Financials - Quick Commerce

All the income and then some appears to go straight to firepower for the quick commerce wars.

While there are many players in the QC wars, Zomato at least appears to be leaving behind Swiggy in the dusk with operating revenues 2.5x times Swiggy and seeing operating losses contract while Swiggy’s QC operating losses appears to expanding.

Things really do not look rosy at all for Swiggy in the QC wars.

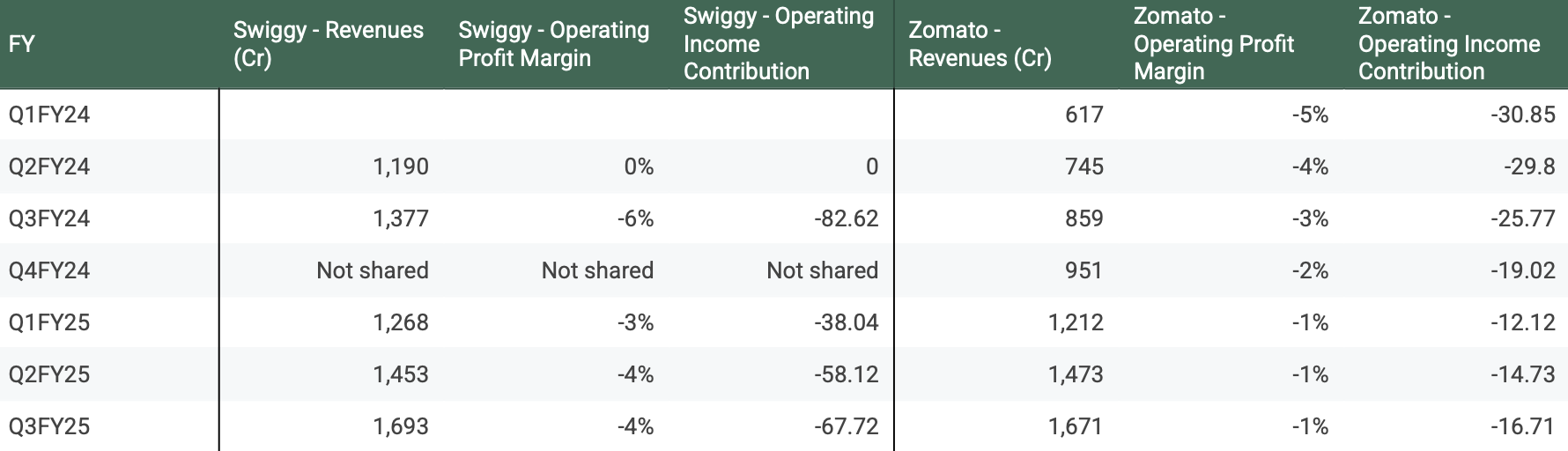

Segment Financials - B2B

Literally nobody is talking about Swiggy and Zomato’s B2B segments while their other segments (dining out, events etc) which barely pull any revenue get a disproportionate amount of the attention .

While Zomato’s B2B revenues quickly caught up with Swiggy, they now appear to be growing in lockstep - albeit with Zomato having slightly better operating profit margin.

Rough seas ahead for Swiggy?

I think there is a good chance that Swiggy follows a similar path to Zomato - falling stock price until they demonstrate breakeven EBITDA margins, after which they would be massively rewarded by the market.

However, Zomato did this in times of peace - they did not have a QC war going on. Will Swiggy be able to contract their losses with wartime spending?

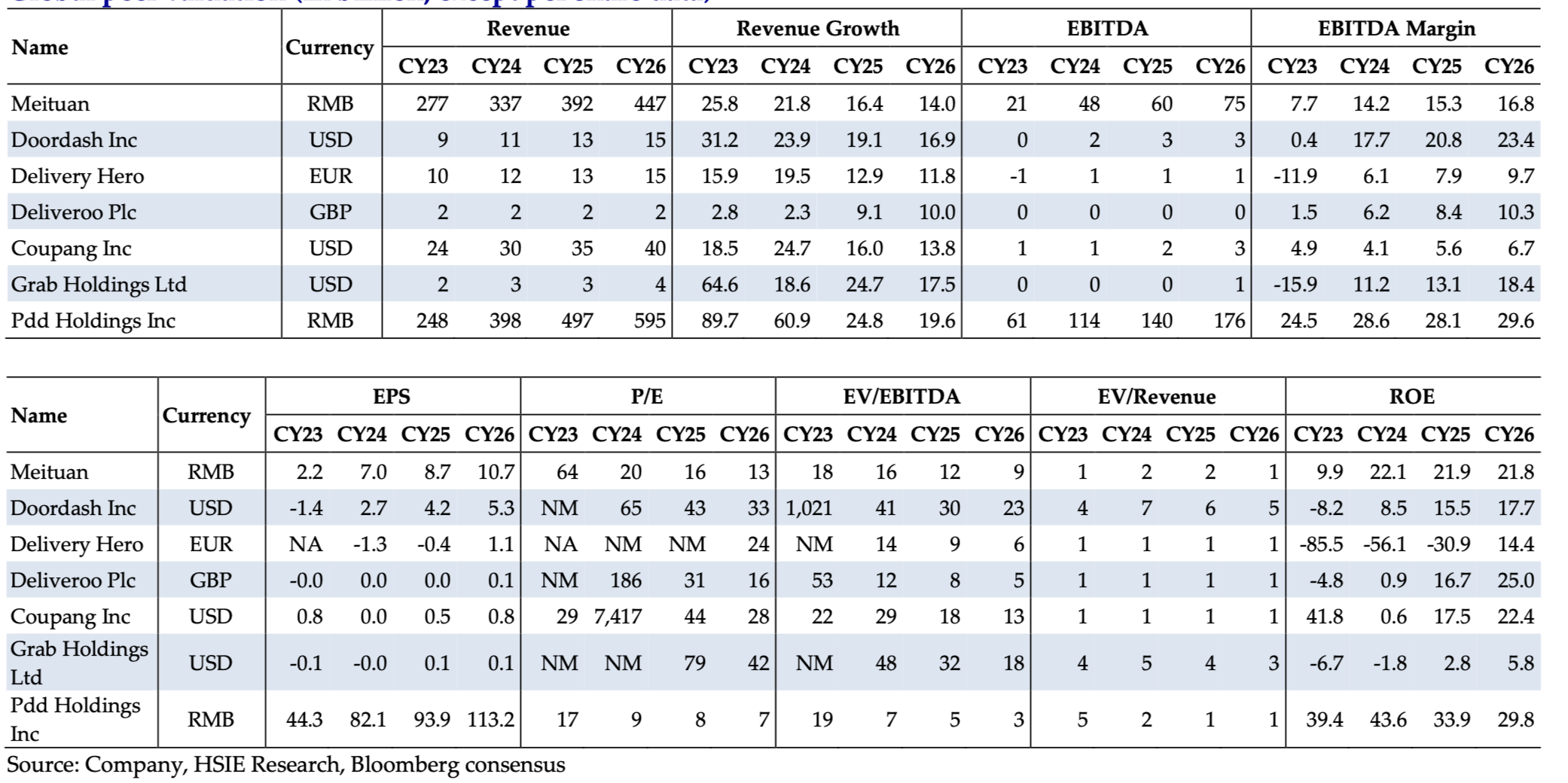

Valuations

To be honest, I must confess a lot of uncertainty regarding valuations of Zomato and Swiggy. I don’t think there market also has a clue either ![]()

If you look at the above chart, you can bucket the types of businesses

Where EV is equal to CY24 sales

There are three businesses in this category

- Delivery Hero - Not profitable in CY24

- Deliveroo - Subpar revenue growth in CY23 and CY24 (2.8% and 2.3%)

- Coupang - Went from profitable in CY23 to breakeven in CY24

Where EV is 2x CY24 sales

- Meituan - Entering mature business phase, revenues and EPS growth projected to be <20% over next two CYs. Market probably switching over to valuing it by P/E.

- PDD Holdings - Not sure why this is included in the list as it mainly an ecommerce giant.

Where EV is 5-7x CY24 sales

Now we are approaching where Zomato and Swiggy are valued at ![]()

- Doordash (7x revenues) - Became profitable in CY24 while growing revenues 22%

- Grab Holdings (5x revenues) - Became breakeven in CY24 while growing revenues 18.6%

Zomato is currently at around ~11.5 EV/Revenue. To me this suggests it is overvalued as it has not demonstrated anything that sets it apart from Doordash. EBITDA of Doordash is around 18% while Zomato’s EBITDA for last 9M FY25 is around 4% while having much lower revenues and revenue potential.

Swiggy also feels overvalued at around ~5.5 EV/Revenue considering that it should be put in the not profitable cohort of Deliveroo/Delivery Hero/Coupang who are trading at 1x EV/revenues.

Caveat - Of course, none of these companies are directly comparable. Meituan operates a significant travel ecommerce platform. Doordash does not have a network of dark stores fulfilling its grocery orders, Grab has a significant ride sharing businesses etc. Also operating in different markets which brings about different unit economics

I am staying well clear of these for now but set price alerts for massive corrections.

- Zomato - CY24 revenues for Zomato is ~18000 Cr. At a 7x EV/Revenue multiple, Zomato’s EV should be 1,26,000 Cr. This would be a 40% fall from current prices giving it a fair value of Rs 130

- Swiggy - CY24 revenues for Swiggy is ~14000 Cr. At a (generous) 2x EV/Revenue multiple, Swiggy’s EV should be ~28000 Cr. This would be a 64% fall from current prices giving it a fair value of Rs 126

Disc: Not invested in Swiggy or Zomato. Valuations are not buy/sell advice or price targets

9 Likes

I thought I will share something I have noticed when I had ordered Pepsodent Gumcare toothpaste on Zepto/Instamart platform for 140gram paste. What I have noticed is the the tube seems lot more watery and feels diluted compared to the ones you get them in kirana stores which is lot more hardy. Mind you its a same size/priced paste. Does it mean, the FMCG companies make products specifically for quick commerce companies versus regular distributer channels/kirana stores? if they do that, is it even legal?

I am almost certain that they don’t make products that way. Something must have happened to the substance of itself or due to some external factors like heat. Toothpastes have long shelf life. Must be a one-off.

Despite using the same products like FMCG and services like banking, QC; experiences can be very different.

Have a position in Swiggy.

1 Like

Nothing in particular. The whole concept looks promising. Evolving businesses, some aspects of which might have surpassed and surprised even the owners’ expectations. Long story. Decadal, even if the journey is turbulent. I also have a position in Zomato, Swiggy is complimentary.

I build positions, so unless there is an irrecoverable damage to the business, price does not fall beyond a point, and as market knows more than me in assigning valuation, I stick with the business side to the extent possible. And as overvaluation reflects in price, either through consolidation or profit booking, and if the situation is latter, I also book profit, I cannot afford to not book. I buy again. I cannot recall a big name (from investing standpoint) who does this, maybe there isn’t one.

Even excluding the technological advancements, I believe, the whole participation landscape is changing with numerous participant groups with different objectives. So sometimes, a rise if not capitalized, may never be seen again, and I cannot miss that.

I know this is not what you expected, but this is the truth.

5 Likes

Swiggy is good. At half the valuation on Zomato, we can expect 5% ebitda margins in fd which will bring stable profits from fd in coming qtrs. Another interesting point in recent concall was that swiggy said expansion of stores in qc was over and they can grow gov by 100% based on existing stores only. This will reduce losses in qc significantly in coming qtrs and will lead to good operating leverage.

Discl:- Invested in both swiggy and zomato.

3 Likes

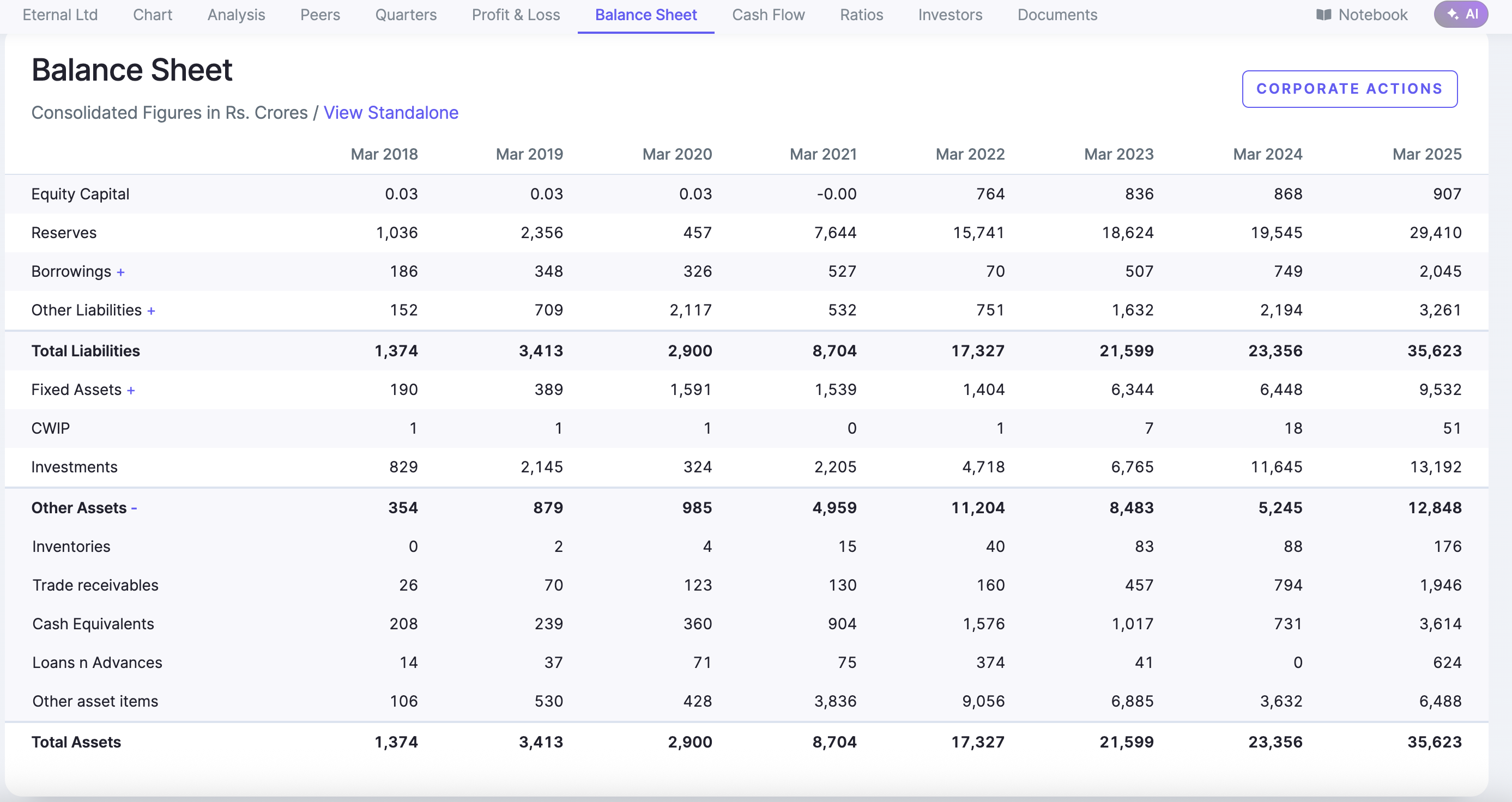

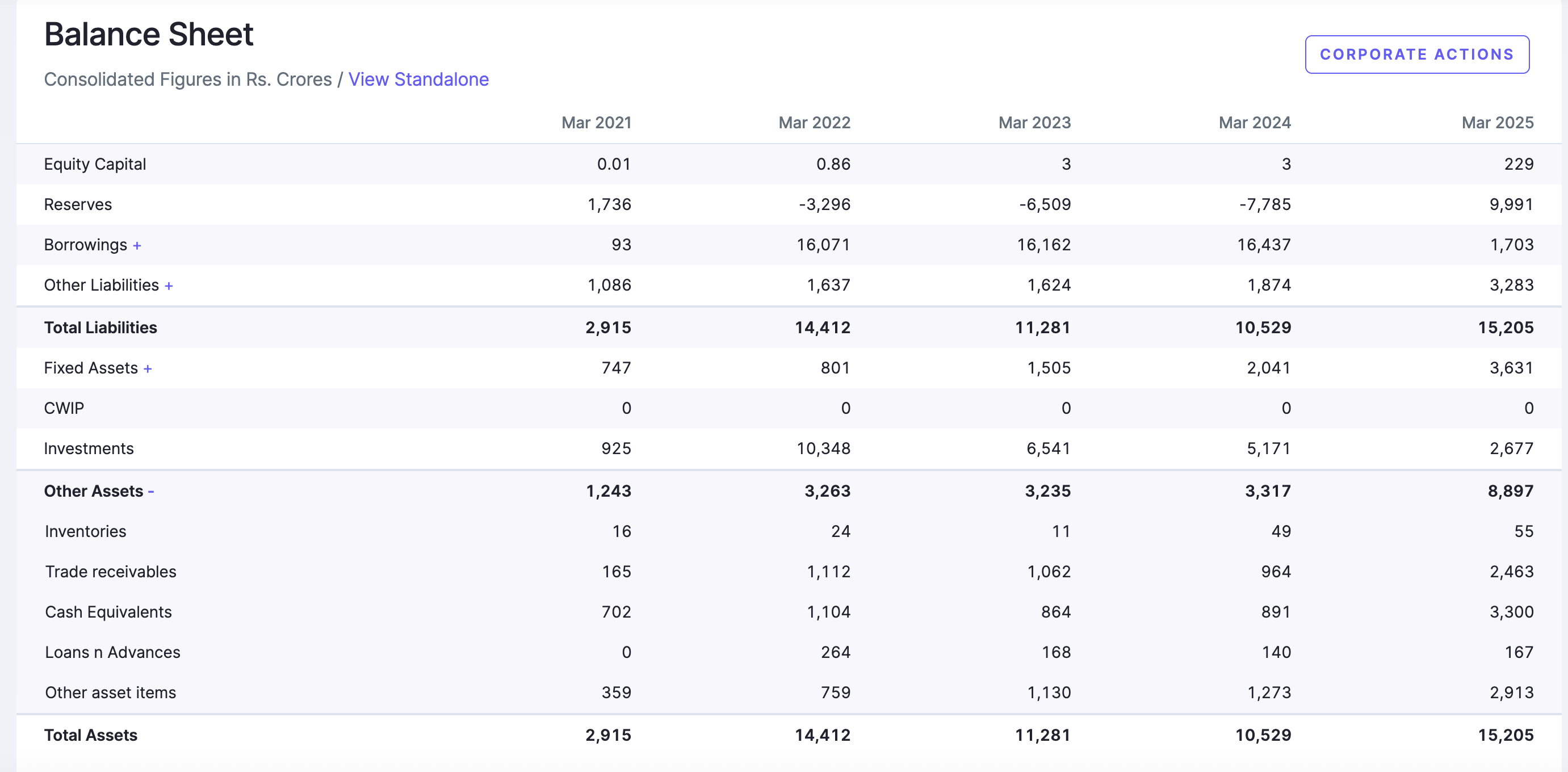

not great at determining balance sheets but from the looks of it. combining reserves and cash equivalents, they would have net around 13000cr. if the current burn rate of 1000+cr per qtr doesn’t come down they could be in bad situation. I guess that’s why a potential selling of rapido stake is talk of town.

I feel the story of discount of zomato premium won’t play that well, here is balance sheet of zomato sure they had qip and treasury income etc, but it’s quite clear zomato has too much juice to be dried up same doesn’t show with swiggy

Disc: not invested, new to understanding sheets could be wrong as well

2 Likes