Swiggy’s Q4 FY25 disclosures provide a rich case study in strategic ambition colliding with operational reality. In the previous communication, management laid out clear focus areas from breakeven timelines to performance metrics. Below is a forensic comparison between those stated priorities and the numbers now on the table.

- Performance vs. Guidance

Guided Focus:

- Instamart and Corporate Adj. EBITDA breakeven

- Food delivery growth within 18-22% YoY

- Movement in take rates and EBITDA margin targets

What Happened:

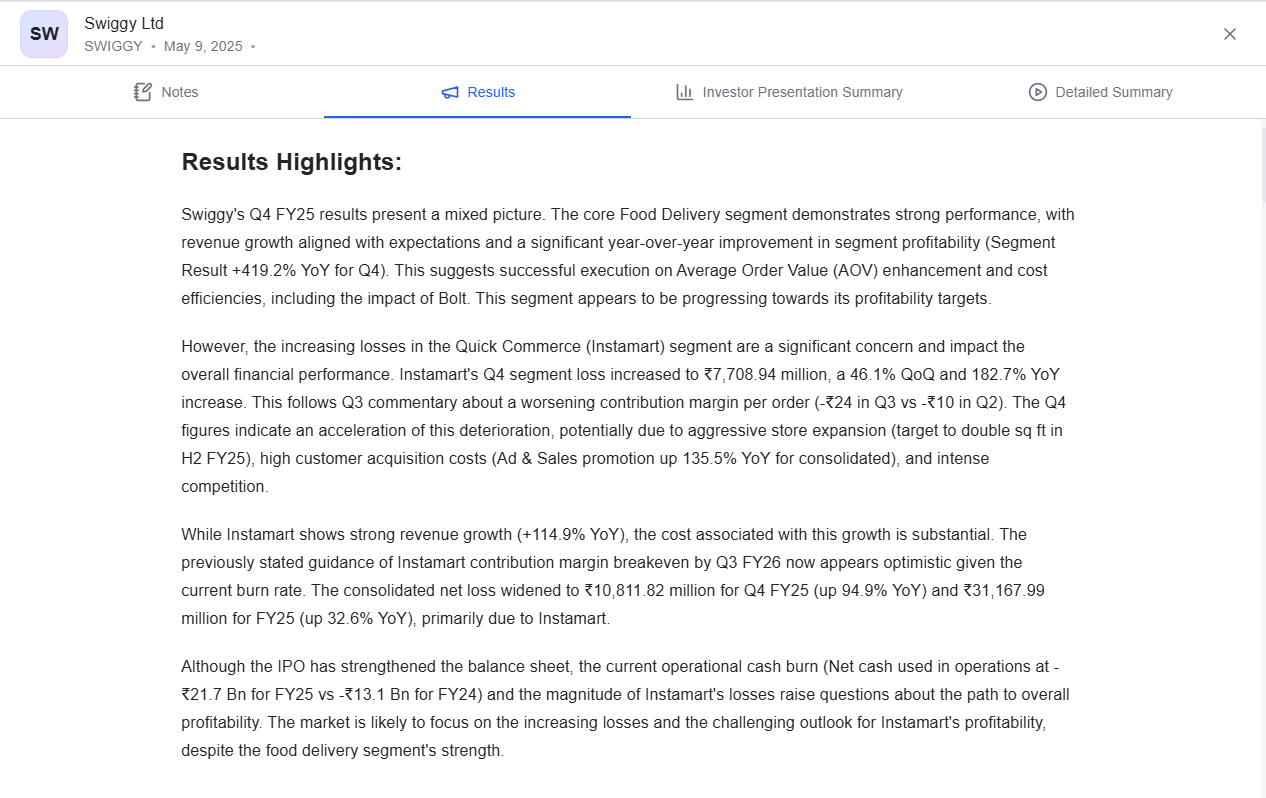

Food delivery delivered strongly, with 18.9% YoY growth, exactly within the guided range. Segment profitability grew 14.4% QoQ, and 419.2% YoY, with leverage from higher AOVs, stable fixed costs, and Bolt’s scaling. This supports the case for a sustainable path toward the 5% adjusted EBITDA target in this segment.

But the story is very different for Instamart. Revenue may have grown 19.5% QoQ and 114.9% YoY, but losses exploded to ₹7,708.94 million in Q4, up 46.1% QoQ and 182.7% YoY. The contribution margin deteriorated to -₹24/order, from -₹10 in Q3. This puts a massive question mark on the OND quarter (Q3 FY26) CM breakeven target, which now appears more aspirational than data-backed.

Reflection:

The dual-track performance here highlights a structural divergence: food delivery is maturing into a profitable business, while Instamart is increasingly a cash furnace. The original guidance was based on unit economic stabilization in Instamart, the reverse is playing out. Continuing to present breakeven timelines without addressing this deterioration risks not just execution credibility but governance integrity. Investors should start modeling downside cases for Instamart’s breakeven being deferred well beyond FY26.

2. Updates on Strategic Initiatives

2. Updates on Strategic Initiatives

Guided Focus:

- Bolt contribution (>10%)

- Standalone app, MTU/order growth

- Non-food, megapod expansion, and ESG goals

What Happened:

Bolt’s influence was indirectly confirmed it helped raise AOV and efficiency, likely playing a role in food delivery margin uplift. Its >10% order share from Q3 appears to be sustained. Instamart expansion targets were also met (100 cities, doubling of sq ft by Mar’25).

However, there was no visibility on the standalone app, user growth specifics, or non-food SKU ramp-up. Nor was there any update on megastores or ESG-linked milestones (EV fleet, packaging improvements, etc.).

Reflection:

While scale-based metrics like footprint and order share are being reported, impact-based metrics are missing. Are the new Instamart customers higher frequency? Is retention improving? What are the unit costs for megastore logistics or dark store ops? In the absence of these disclosures, the initiative updates feel one-dimensional. This is a red flag because top-line expansion without clarity on quality or economics of that growth can conceal operational inefficiencies until it’s too late.

3. Follow-up on Risks & Challenges

Guided Focus:

- Competitive intensity in Q-commerce

- CAC pressure, promotional expenses

- Working capital trends, tax litigation

What Happened:

Competitive pressure is clearly visible in the 135.5% YoY spike in ad & promotional spends. Instamart is in early-stage ramp-up, with zero evidence of improving unit metrics. Working capital stress is acute trade receivables surged 155.5% YoY to ₹24.6B, indicating longer credit cycles, likely from FMCG brands being targeted for co-funded growth.

No meaningful update on litigation but the balance sheet commentary confirms that operating cash burn widened due to trade receivables and Instamart losses.

Reflection:

This is perhaps the most concerning dimension of the quarter. We now have hard data confirming that Swiggy’s customer acquisition strategy is front-loaded and balance sheet-intensive, while monetization remains back-ended and speculative. This is not just about CAC or competition anymore it’s about the sustainability of working capital under stress. If receivables aren’t brought under control, Swiggy may find itself in a position where it needs more capital much sooner than expected, despite IPO proceeds.

4. Progress on Key Metrics

Guided Focus:

- CM per order for Instamart

- Delivery cost trends, Bolt retention

- Platform-level efficiency gains

What Happened:

The CM per order trend for Instamart sharply worsened to -₹24, negating earlier stabilization seen in Q2/Q3. On the other hand, food delivery showed a clear improvement: profit grew from ₹1,927M to ₹2,204M. Delivery efficiencies and AOV improvements helped with Bolt likely playing a role again.

Still, Bolt’s metrics (retention, order value lift, CAC) weren’t disclosed directly. Instamart remains grossly margin-negative.

Reflection:

The CM deterioration, despite growth in GMV and city footprint, highlights a foundational issue, scale in Instamart is not translating into operating leverage. This could imply pricing power weakness, discount-led growth, or unviable last-mile economics. Unless we see a flattening of this curve over the next 1-2 quarters, every new city may actually be increasing the burn, not distributing it.

5. Potential Shifts in Narrative

Guided Focus:

- Is the company prioritizing profitability over growth?

- Reaffirmation or rethinking of breakeven timelines

- Change in tone around market competition or expansion pacing

What Happened:

Despite the clear deterioration in Instamart economics and an overall ₹10.8B net loss in Q4 (up 95% YoY), there was no strategic pivot or soft guidance reset. Management continues to reference the Q3 FY26 breakeven for Instamart and maintains aggressive expansion cadence.

This feels disconnected from the burn profile. IPO cash helped strengthen liquidity, but net operating cash outflow for FY25 stood at ₹21.7B, which is significant.

Reflection:

This lack of narrative shift is perhaps the loudest signal in the entire result. In high-burn businesses, the willingness to adapt or lack thereof becomes a predictor of survival. What we’re witnessing here is a classic case of strategic inertia: the business is committing to a course even as evidence accumulates against it. Unless Swiggy recalibrates and communicates a tighter execution framework including a slowdown in Instamart expansion or better CAC control ,they risk not just missing profitability targets, but credibility altogether.

Closing Thoughts:

Swiggy’s Q4 FY25 is a mixed bag , not in the way of some wins and some misses, but in the sense of one business line performing and another actively undoing the gains.

- Food delivery is turning the corner: improving profitability, stable fixed costs, AOV gains, and likely positive unit economics.

- Instamart is turning into a structural liability: aggressive expansion, deepening losses, worsening CM, and working capital stress.

The company has the data. Investors now await signs of acknowledgment and action. Without that, the next few quarters may bring not progress, but a pivot forced by market reaction rather than strategic foresight