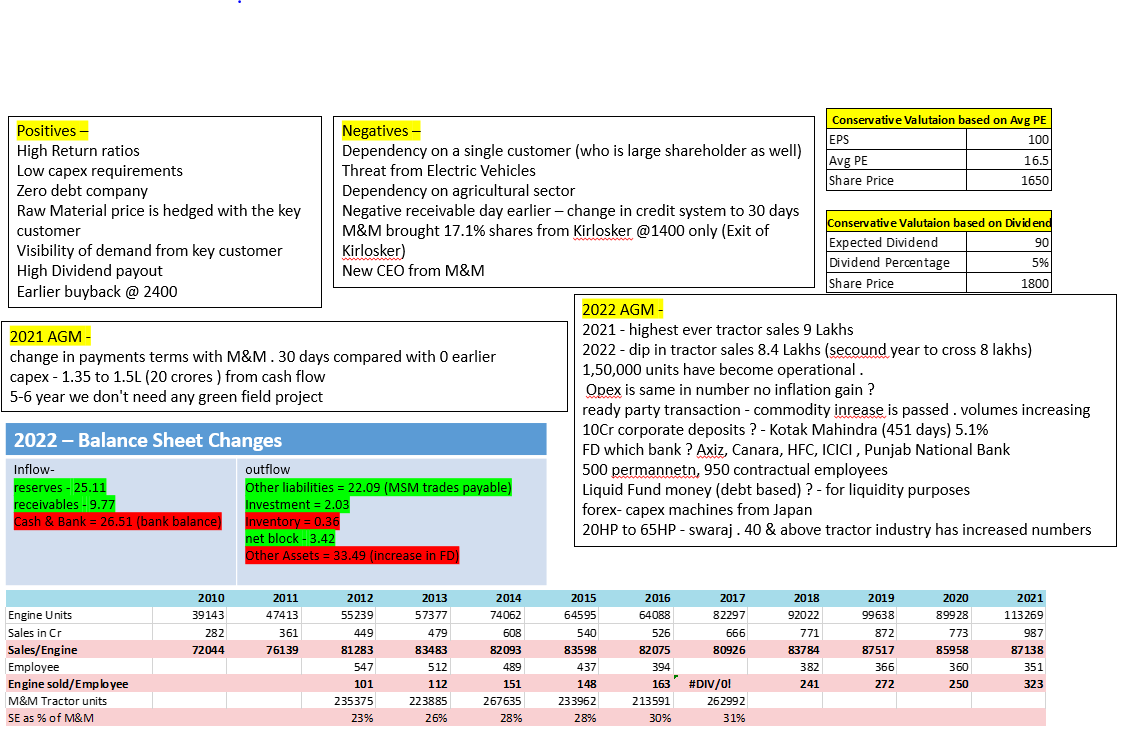

Swaraj Engine would now become M&M group subsidiary with Mahindra buying Kirloskar Group holding as per BSE announcement.

I have been happy investor with Swaraj Engine for almost decade now. However, after this announcement, I found other opportunities like Azko Noble/Cochin Shipyard and Heidelberg as good dividend yield investment along with growth in dividend over longer terms and hence moved from Swaraj Engine (except for token position) today.

The company has been wornderful learning experience and also excellent clean company on corporate governance on my portfiolio. While it has not gain much in share price over decade, the dividend growth has been excellent to make for that.

Positives:

Shift in Control in the company would provide better visibility of future growth for the company. Previously, the company was controlled by two diverse management group, which would may have different view about future path of the company. That may have kept company on path of brownfield expansion in capacity at appropriate time and distribute exceess cashflow to the shareholders by dividend/buyback. With Mahindra group now in control, the long term future prospect would depend what additional products/path Mahindra group add to this company business. Tractor engine is likely to be cash cow business but would offer limited growth. The new products are essential for the company to maintain the terminal value in my view.

Negatives:

The deal at Rs 1400 per share between two promoter group which know inside out about operation of the company as compared yesterday close of ~ Rs 1,700/- was not seen positively by me. While there would have issue about exiting from the company for Kirloskar group, nearly 17% discount to market price was very steep in my limited understanding. Also, there was jump of 10-12% post announcement which I am not able to understand. Hence, I exited from the company.

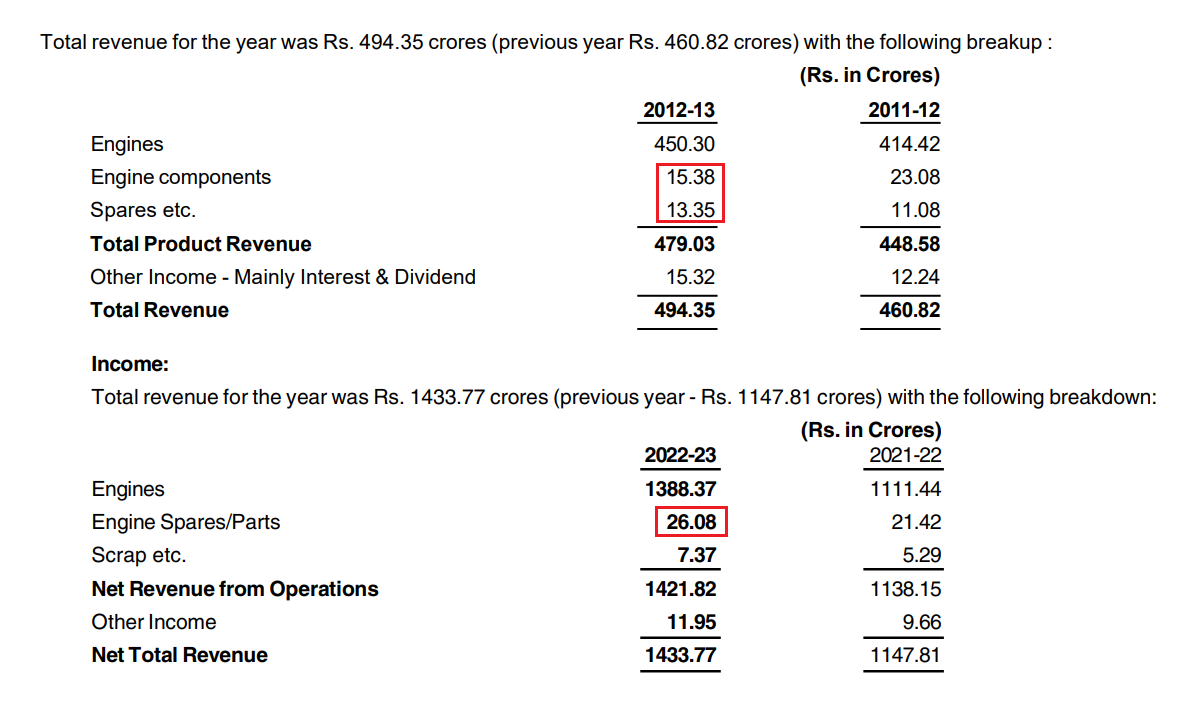

In past Mahindra group has been only customer of the company. While economies of scale was achieved by Swaraj by supplying tractors, It was making major profit from spare part and other small business which was attributing to higher profitability margin. Over period, non-tractor business decline to insignificance, hence despite growth in volume, Swaraj Profitability decline its past level.

Also, in last 2 years, Mahindra changed arrangement of trade and started buying at 1 month credit period. Generally, nothing negative but change in trade terms would result in lower free cash flow from shareholders and also raise concern about future dealing with the only customer which is also controlling shareholder. Till now, there was another independent stakeholder which would have protected interest of minority shareholder, but now the dealing with Related parties would be between the Parent and subsidiary. Having said that, both Mahindra and Swaraj Engine management and corporate governance are kind of gold standard in Indian listed spacce, still this concern need to be addressed properly.

Last, Tractor engine business, while it is good cashflow generator for medium term, the company need new porducts/segment to sustain its working for long term.

Considering all factors mentioned above and also other opportunities available in current market, I decided to exit (except for token holding) from the company. Swaraj has special contribution in my investment jounery and I would alway greateful to this wonderful company for same. I wish we have many Swaraj Like companies in listed space and (also in my portfolio  ).

).

Thank you Swaraj Egnine and all the best for future.

Disclosure : My view may be negatively biased due to my selling decision. Not a SEBI registered advisor. Not suggesting any investment action. The purpose of the post is to keep reasons for my investment decision for my future evaluation.