I like Swaraj engine and holding for last 5 year with addition during May/June 2014. Very good business model with management and real cash generating compounder. I never expect Swaraj to grow by 50-75% during one year. However, very comforable with the kind of dividend and growth it has shown.

During FY12, it declared Rs 13 Dividend (With March 2012 share price Rs 407, giving almost ~3% dividend yield).

FY 13, dividend declared Rs 33 (March 2013 share price Rs 395, giving dividend yield of ~8%)

FY14, dividend declared Rs 35 (March 2014 share price Rs 691 giving dividend yield of ~5%)

FY15 dividend declared Rs 33 (March 2015 share price Rs 802 giving dividend yield of ~4%)

FY16 dividend declared Rs 33 (March 2016 share price Rs 857 giving dividend yield of ~3.5%)

FY17 dividend declared Rs 43 (March 2017 share price Rs 1484 giving dividend yield of ~3%)

On share bought on March 2012, Rs 407, total dividedn received by investor is Rs 190, so almost 50% of value received back as dividend ! Further, on acquisition price, the company is paying almost 10% dividend yield, which is much better than current interest on fixed income.

Risk:

- M&M hold ~40% stake with major customer. the company has consistently gain business from M&M, howerver operating margin remain stable despite increased scale. However, same has been case with other auto ancillairy business. Further, Kirloskar as being second largest holder would also ensure fair transfer price to protect minority shareholder rights.

- Swaraj would continue to face cyclicality due to tractor demand, but historitcally company has managed that volatility very well.

Positive:

- High ROCE and Capital intensive business model

The company expended capacity in December 2016 quarter with 15,000 unit and capex of around Rs20 Cr giving brownfiled expansion cost of Rs 13,333 per engine. Average EBIT per engine 12,960 giving almost 100% ROCE. (During FY10 to FY17, average Sales realisation per engine is Rs 80,331 while EBIT is around Rs 11,760 per engine. The company reported capex of Rs 55 Cr during FY14 for adding 33,000 units; (18,000 per engine); Further Rs 38 Cr during FY15 for adding 30,000 engine capacity (Rs 12,700 per engine capex). After revival in demand and expected good growth, it again incurred capex of Rs 20 Cr for 15,000 unit addition (Rs 13,300 per engine capex).

As per my understanding, the company has increased capacity from 42,000 in March 31 2012 to 120,000 in March 2017.

So almost 3 times increase in capacity with no increase in debt and constant increse in dividend. What more we can expect form the company? While at a particular stage, the company would not be able to increase capacity by brown filed, and may need to undertake greenfield project. I expect Greefield capex cost would be signficantly high as compared with current capex cost. However, with 82,297 engine sales and 120,000 installed capacity, I feel even no further scope for capacity expansion in current plant, I still feel it would be able to work with current capacity at least for 12-18 months.

-

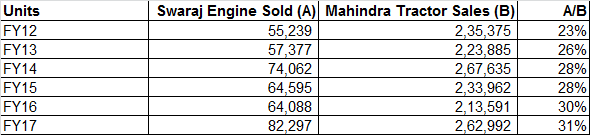

Increasing share in Mahindra Tractor procurement

Find enclosed incresing share of Swaraj engine in Mahindra Tractor sales over the period

-

Efficient operating performance

Despite increase sales (no data about of production of engine avaiable now, so assumed production equal to sale), average production of engine increase signficantly

This is just one parameter I could collect from annual report over the period. However, give very good unstanding about efficient resource utilisation.

BSE link for dividend declared:

Discl: Swaraj is among Top 5 holding of mine and my view may be biased. Investor are requested to do their own due diligence before investing.