He seems to have given conflicting & confusing replies. One can listen to the call at approx. 10 mins / 30 mins / 65 mins and draw one’s own conclusions.

Decent set of numbers by Suven Pharma. Some headline numbers:

- Operating revenue of Rs. 1320 Crs. for FY’22 against 1009 Crs. for FY’21. Solid 30%+ topline Growth.

- EBIDT of Rs. 768 Crs. against 455 Crs for last year. - 68% jump.

- EBIDTA margin of 51% against 44% for FY’21 and 47% for FY’20. May moderate going ahead (guidance range of 40% - 45%), still industry leading numbers.

- Personally, one of the most important take away from the concall is the commentary around 50%+ growth for Specialty Chem CDMO business. Interestingly, this growth is not majorly attributed to the 3rd molecule which was launched recently. Based on management commentary, my conclusion is that the growth is driven by molecule #2 which went off-patent and they had major setback in FY18. Now innovator has come-up with combination formulations thereby increasing volume offtake this financial. Repeat order possible with a buffer of 12-18 months.

Some Notes from concall dated May 9th’2022:

Casper Pharma Acquisition:

- Acquisition completed in last week of April’22 for a consideration of $20.5M.

- 2 ANDAs already filed under and waiting USFDA visit to commercialize. Other 15 products to be filed within fiscal year. This pipeline is for Rising Pharma.

- Conflict of interest with innovators due to this: Full transparency and support from CDMO innovator clients. In some cases, seeing they extending hand for support, where needed.

- Market front ending - Suven dont have capability. Will depend of various marketing partners (Rising can play a critical role here).

Guidance:

- Revenue growth guidance in range of 10% - 15% with possibility of upside. Will depend on project mix and pipeline moving from L2 to L3 or commercialization. (this is on higher growth base this FY)

- EBIDTA Margin in range of 40% - 45% for FY’23. Current FY was more of any outlier due to favorable mix, may or may not repeat. Realistic to stabilize around ~45%.

- Formulation margins - Both Casper and own in the range of ~25%.

Pipeline:

- CDMO: Phase 1 - 77 | Phase 2 - 37 | Phase 3 - 5 | Commercialized - 5

(good build up in phase 3 compared to historical range of 2-3 molecules) - CDMO SpeChem - 3rd one got commercialized in this FY. 4th molecule commercialization expected sometime if CY23. Will be a 40 Crs. - 50 Crs opportunity.

- Rising Formulation - 2 Para 4 submitted. 15 in pipeline for FY’23.

- Suvens own legacy Formulation - 17 Fillings out of which 9 approved and 8 commercialized. Few are not turning out to be very remunerative. Another 7 - 8 filling expected in FY from Suven’s FDF facility in Pashamylaram

- Focus is not to chase blockbuster or crowded drugs. Small/niche molecules with limited competition. (sub $10M types)

Forward Integration:

- In few cases, innovator were interested in Suven moving up value chain however COVID has delayed the things.

- May take couple of more years before any material progress in this direction.

Disc: Invested

Thanks,

Tarun

22 Likes

2 Likes

Somehow I am not very convinced of the Casper Acquisition from strategic perspective. The 15+ ANDA molecules that they are filing in FY 23 from Casper are “Me too” Generic products where Suven does not have a right to win (along with their potential distribution/sales partner). Also for the short term this acquisition will be margin dilutive and will need management focus.

I really hope that they can quickly turn this formulation facility for CDMO/CMO work on formulation side, when it can become an asset. In the meanwhile they should not lose their focus on the current API CDMO/CMO business.

Regards,

NIkhil

Disc: Invested

7 Likes

Capital allocation decisions are to be assessed against alternative options available at that point in time. Every large company has multiple products, product lines, customer segments, geographical regions and so on. Not all of them yield the same margins. If an existing high margin product line becomes a rigid benchmark for future capital allocation, businesses will struggle to grow.

Suven is debt free and sitting on surplus cash. Capital needs of CDMO business have been provided for (capex announced earlier), all from internal accruals. Thus, the Casper acquisition does not starve CDMO of money.

Casper is located in a SEZ and has long-term customer contract to buy all its production. These are valuable intangibles not visible on the balance sheet. Once it clears FDA inspection, Mr. Jasti says it can generate revenues of Rs.300 crore per annum with a potential to be scaled even more. Mr. Jasti has said he is paying only for asset value (Rs.155 crore), not for business value. He understands that the business value is much higher, even with ‘me too’ products. The acquisition also helps to de-risk the business from excessive dependency on CDMO. In FY21, top 2 customers constituted 45% of Suven’s revenue.

An opportunity came his way and he seized it. Most businessmen in his place would have done the same thing. Casper is thus a step forward.

18 Likes

I have no issues with the valuation paid for the asset - 150 Cr for a reasonable facility ready for inspection is quite fair. However the logic of buying the facility is what I am not convinced about. What may be possible reason to buy the facility?

- Diversification for growth as a reason? - I think Suven is still very- very small from a CDMO/CMO perspective from API/ Speciality Chemical perspective with revenues of < $150 mn/year. There should be ample opportunity in this space looking at what Divis has done/doing as well as what Laurus is doing.There are also significantly larger Chinese companies in this space who have big business…

-

Diversification for risk management/concentration as a reason - I would believe that US is extremely competitive market for the formulations. All the large companies are witnessing significant price erosion and not making desirable margins despite vertical integration is a case in point. How will Suven with most API coming from outside for regular products and having a partner in US to share margins will get enough margin/compete is something which beats me.

My view is that even if they wanted to diversify, this does not seem to the best business , that too with “Me too” products. While they may have buyback arrangement, what margins will this business deliver is anybody’s guess. - Surplus Cash management - I dont think this would be the reason but if it is, they could have increased dividend and paid off the excess.

Just to clarify, My objection is not towards diversification - However If they would have setup something which is more differentiated it would have been better.

I am still not saying that this formulation mfg is a bad step. However there is a likelihood that they may face margin pressures on this. Therefore earlier they move to something more differentiated (either on portfolio or customer) it may be better for them.

The investment thesis of investing in Suven, who is an emerging CRAMS player will get changed for me, if they keep on investing in the US generic formulation business for whatever reason.

Regards,

Nikhil

9 Likes

Excellent concall transcript to understand CDMO business.

3 Likes

Pfizer has stopped Paxlovid trials for less vulnerable COVID patients as data showed no significant benefit. Relevant links here and here.

This may temper down the total market size calculations as well as the sustainability of Paxlovid sales. Since Suven is an intermediate supplier for Paxlovid, we should also not bake-in a lot of Paxlovid intermediate sales into Suven’s revenue.

As a side note, this probably explains the sharp falls in Suven (and Laurus) over the last couple of days.

7 Likes

Tks. Paxlovid was a one off. any update on other molecules going to commercialization stage n the pipeline in pharma n chemical?

1 Like

Any idea how much were the Paxlovid revenues for Suven?

Mr.jasti clearly said in concall that paxlovid is oneoff.any way this is pandemic drugs so more suppliers for this. In recent concall he also said that very small revenue from this paxlovid otherwise there is much more from products mix

2 Likes

Some take aways from AR 2021-22 (link)

Financial and Numbers:

- Standalone Revenue from operations stood at Rs. 1,320.22 crore in FY22 against Rs.1,009.71 crore in FY21 - a growth of 30.75%. This growth was primarily owing to the growth in CDMO and specialty chemicals divisions which reported a better than budgeted performance.

- Our top-line grew by 47% on a higher base. Our EBITDA margin scaled the 50% mark despite the inflationary pressure that prevailed during the year. Our Net Profit increased by 80%.

- operating margin improved from 47.22% in FY21 to 51.04% in FY22.

- The overall debt burden dropped from Rs. 141.23 crore as on March 31, 2021, to Rs. 95.57 crore as on March 31, 2022;

- Debt-equity ratio improved from 11.4% to 3.3% over the same period.

- The Company invested Rs. 65.42 crore in the business as part of its ongoing planned capital expenditure.

- The Company spent Rs. 620.08 lakhs on its social and environmental commitments in 2021-22 to make the business sustainably profitable.

Rising divesture and Casper acquisition

- We had invested US$35 million in Rising Pharma in 2019. In FY22, Rising Pharma was acquired by HIG, we sold our entire stake to the acquirer for which we received US$41.55 million in cash and a 7% stake in Rising Aggregator (a holding Company created by HIG to manage Rising Pharma and other acquisitions that would happen in future).

- In a nutshell, an investment of US$35 million has given the Company US$41.55million in cash, a 7% stake in Rising Aggregators and 100% stake in Casper Pharma, which promises to bolster our formulation vertical significantly

[important to call out… Technically above statement is incorrect/misleading, not that they have got $41M + 100% stake in Casper. Casper was acquired from the proceeds of $41M ]

- We used US$ 20.50 million to acquire Casper Pharma, which has a large manufacturing unit in Hyderabad dedicated to the manufacture of solid and liquid oral pharmaceuticals for USA and regulated markets and ready for USFDA inspection.

- Casper Pharma is into manufacturing solid and liquid oral pharmaceuticals for USA and regulated market. They have a new manufacturing facility (approximate capacity of 1.20 billion doses) located in GMR SEZ (outside Hyderabad airport). They have filed 2 ANDAs which have triggered a US FDA audit which is likely to happen anytime soon. Besides, they have 15 ANDAs which they plan to file in FY23. When these get approved by the regulated authority, it will strengthen our position in the formulation space.

- Casper has agreement with Rising Pharma for next 7 years

Segment wise business updates:

Formulations (Suven standalone without Casper):

- We filed17 ANDAs of which 9 have received approvals and 8 were launched. In FY22, we witnessed healthy traction for four of the launched products which boosted revenue from the formulations vertical. ,

- we are planning to maintain a steady pace of ANDA filings over the next 3-4 years. We plan to file about 6-8 ANDA’s in FY23 which should hopefully start generating returns 18-24 months thereafter.

- In the last 3 years, our revenue has moved up steadily from H6.50 crores to H45.69 crores.

- Armed with intellectual capital and capability matrix, we realise that we can partner with any global player anywhere across the pharma value chain. Hence, we moved from working on intermediates to developing formulation.

we have put in place three out of the four wheels in our formulation vehicle.

- Wheel 1: Our existing formulation’s piece under Suven Pharma.

- Wheel 2: Our stake in Rising Aggregator. The value of our stake in Rising is expected to rise over the coming years as HIG is focused on new acquisitions to more than double the enterprise value of Rising Aggregators in future.

- Wheel 3: Our acquisition of Casper Pharma and their contract with Rising Pharma should generate interesting returns.

- Wheel 4: We plan to manufacture KSM and API for formulation for some of our clients.

CDMO Business:

- The CDMO business registered a healthy double-digit growth in FY22 driven by the success of molecules in clinical trials with conversion to next stage and good volumes for some commercial CDMO projects.

- We had a good number of projects in the Phase 2 and 3 categories which resulted in higher volumes and hence better billing.

- In the Commercial CDMO piece, supplies were robust, and the combination of these factors helped in elevating the performance of the CDMO vertical.

- we became preferred vendor to four global players which will enhance the new business opportunities and expansion of our offerings into forward integration of the product development.

Specialty Chemical:

- The volume picked up because this molecule came out of patents in some countries during the year under review. But our partner developed a robust life cycle management which generated good volumes.

[ must be referring to molecule #2 that they had] - Also, there was a commercialization of 3rd molecule during the year which also helped the growth.

- One molecule for which developed the intermediate made it through to the commercial launch stage. While this is something to cheer about, it does not immediately translate into business volumes for us. Repeat volumes for the intermediate supplied by us could accrue in the next 12-18 months after successful launch of the product.

- The Company is also working on the development of a fourth intermediate which holds the possibility of seeing the light of day in the next 18-24 months.

Capex:

- The capex is mainly a replacement capex. We will invest H200 crores for the replacement of a block at Suryapet which is more than 35 years old. This plan should be completed by March 2023.

- We have allocated another H200 crore for relocating our R&D centre.

- The last piece in our capex plan is the additional block at Pashamylaram for which we will invest H200 crore. We plan to undertake this project in 2023-24.

Outlook and Misc:

With the slowdown in pharma business globally we hope to sustain business growth in the current year. While the speciality chemicals and formulations verticals would remain stable at best, we expect the CDMO piece to drive moderate business growth.

- We are expanding our services model, which should create immense value for our customers and the Company. This strategic direction is an outcome of our multiple and intense interactions with the global innovator community, most of whom are also our clients. They want us to extend the runway of our services. They wish that we walk the extra mile. For this, we have contoured two prospective service options. One, forward integration service,where we extend our services to develop and manufacture products further ahead in the value chain - from say, one intermediate (currently) to more intermediates and KSM (Key Starting Material) and APIs and Formulations. Two, life cycle management service, where we contour the prospects of working with the innovator on a product that will genericise in future. We will develop and manufacture everything (intermediate to formulation) for the innovator

Disc:

Invested

26 Likes

Here comes the good news, FDA inspection with zero observations for Casper (link):

We are glad to have completed the audit successfully with Zero observations and at the end

of the inspection no form 483 was issued by USFDA which signifies compliance and

conformance to applicable cGMP regulations says Venkat Jasti, Managing Director of Suven

Pharmaceuticals Limited.

Possible implication is that those 2 filings can move further into commercialization this year while rest of dossier pipeline for 15 filings keep moving as per plan.

9 Likes

It says three product applications so looks like they have filed one more ANDA by now. We will know in the upcoming concall.

3 Likes

Casper pharma facility inspection completed.

Thanks to @T11 for detwiled AR notes.

Suven of future is likely going to look very different from past.

- Higher formulations sales, with assured supplies from Casper this becomes a straight add on with visibility, ramp up may take some time.

- With forward and backward integration - directionally seems very customer(s) specific approach but does make them one stop shop with KSM to API to formulations. It may be based on assurance of customers ( similar construct as Casper supplies)

- High margins and mderate growth to relatively higher growth ( relatively) and realtively lower margins butbztill likely industry leading( mix changes) - again this is assumption and markets like growth. Until Mr Jatsi or Numbers says it - its logical speculation.

- Replacement capex nearly behind them - this is a sort of hangover which didnt translate into equivalent growth capex - at least perception.

If we were to observe Mr Jatsi, he comes across as science passion( suven life a case in point) with strong delivery capability - though doesnt like/ can’t do much about uncertainties in small biotech segment demand pattern, which is out of his control.

Give him longer running programs, offtake assurance for clients which requires strong delivery/science capabilities - he will likely get this done. In earlier avtaar Suven had dependency on small size innovators, which leads lower visibility hence conservative guidance.

Going forward Casper scaling + client assurance backed Fwd and Bwd integrated programs( unclear at molecules focus at this point, but some hints on client lens apprach per AR)+ post covid era stability for small biotech demand normalizing + Spec chem molecules, all of it seems a logical multi engine growth + diversification in a way, hopefully a stronger growth setup construct.

Invested

10 Likes

A good article on Paxlovid. Suven has very old n special relationship with Pfizer.

2 Likes

Links to Q1’22 results and investor presentations

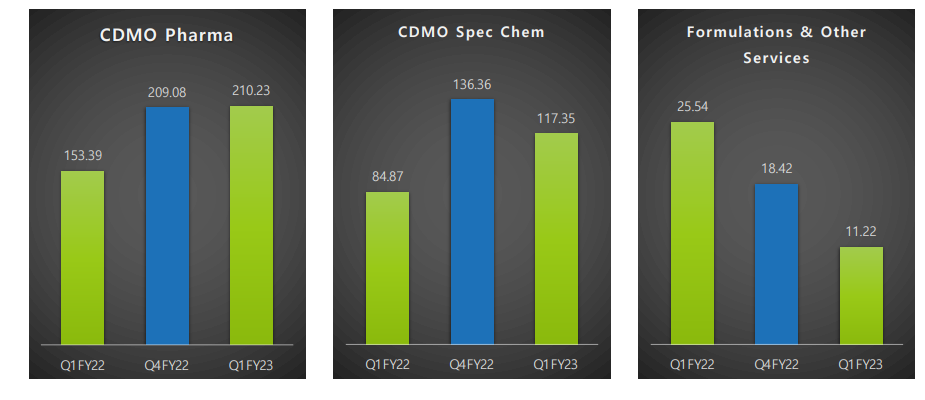

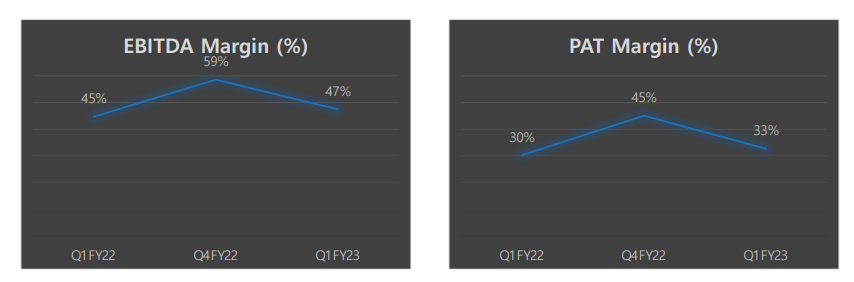

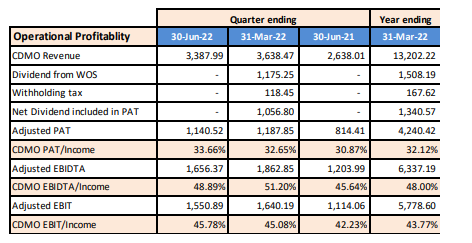

YoY over 30% revenue growth in CDMO (QoQ-stable)

Some degree of margin compression QoQ, but YoY, there is slight improvement.

CDMO margins are largely consistent

Senior boarders such as @Vivek_6954 , @spatel, @T11 , @Chandragupta, @ayushmit can please help get more narrative around the numbers

5 Likes

For any CDMO (Innovator CDMO is where Suven plays it’s game) the biggest asset is their scientists. How this can be tracked ? In the IT world attrition rate parameter plays a major role in valuations, here we are talking about scientists . How they hire these scientists ? What is their background ? ( depth of the knowledge they are bringing into the organization - number of patents filed etc… )

In the latest Gland call, management mentioned about challenges in retaining people.

4 Likes

Why suddenly announcement for dividend?

They already done 5 Rs for FY 21-22

1 Like