Q4 FY22 revenues were upwards of Rs.300 crore for the third quarter running, with both Pharma & Spec Chem CDMO businesses growing handsomely. Operating profits remained healthy at more than Rs.150 crore, a big jump over Q4 FY21 though lower than Q3 this year. Gross margins remained intact at 69 %. Operating margins were down to 43% from 47 in Q3, but it is still a big jump from 36% in the Q4 of FY21. Manpower cost has increased substantially though, and I am surprised no one asked about it in the concall (or did I miss it?). Debtors have gone up substantially but the management said they would get normalised, there could be some bunching effect towards the year end.

In the Pharma CRAMS business, 5 molecules are now commercial. The 5th was launched in Q4 itself, so can be expected to be ramped up in coming quarters. CDMO pipeline now has 5 more molecules in Phase III, 35 in Phase II and 77 in Phase I.

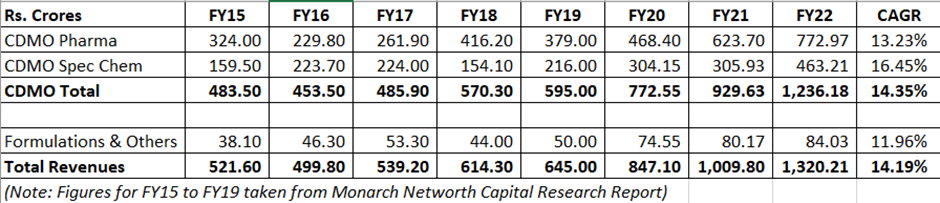

The Speciality Chemicals has 3 products in commercial and 1 under development. Outlook on this business is flat for the current year.

On Formulations business, 5 to 7 more ANDAs will be filed during the current year.

Overall, Mr. Jasti gave a ‘conservative’ guidance of 10-15% growth with EBIDTA margins of 40%+.

On the Casper Pharma acquisition, the deal has been sealed and Suven has got control of the facility in April. Casper has filed for 2 ANDAs and is waiting for the USFDA inspection. 15 more ANDAs are planned to be filed within the current fiscal year i.e. FY23. Mr. Jasti said EBIDTA margins on Casper will be identical to the current formulation business margins, which is 25%. Casper molecules are normal generic molecules chosen by Rising Pharma.

Overall, the results seem to be in line with past with no major negatives. I am not sure why the markets have reacted negatively. Perhaps the worry is that with the growth of formulations under Casper, the overall margins will be diluted, robbing Suven of its high margin USP.

But CDMO itself is a Rs.1000+ crore business and growing in double digits. For Casper starting from zero and existing formulation business also too small, it will be a long time before formulations begin to dilute company margins. Mr. Jasti has said he expects Casper to generate Rs.300 crores p.a. revenues from Year 3 onwards. Meanwhile one or two hits in CDMO can raise the CDMO share and nullify possible dilutions. At an investment of Rs.155 crore, Casper only adds to the growth and should be considered value accretive in absolute sense.

Please point out if I have missed anything.

(Disc: Invested)