Sources share that the Promoters are evaluating options to sell Suven Pharma and have hired an investment bank to advise on majority stake sale in the company.

.

“Sale of Suven Pharma is to raise funds for drug development in Suven Life Sciences which have so far been funded by the promoters through dividend earned from Suven Pharma,” a source added.

4 Likes

1 Like

Did similar things happen during sequent’s , solara’s as well ?

Suven received Establishment Inspection Report (EIR) from USFDA (Pre-approval) with zero observations.

Snap from its BSE filing today.

3 Likes

What caught attention in the press release (link) was mention that out of three applications, one is NDA (novel drug) approval:

Pre-Approval Inspections covering of three applications: NDA 016084, ANDA 217020, &

ANDA 217030.

Reading through the HSS ciruclar (available in public domain) carefully, this is an amendment to own existing NDA for 100 MG and 300 MG tablet for which approval was received prior to 1982 and listed as RLD drug. Over time, ALLOPURINOL has gathered competition with 25+ ANDA approval.

Mylan has NDA for Injectable route since 1996, however did not caught much competitor (except Gland and Hikma). My conjecture, Rx tablet are preferred by payers since facility cost may be involved with administrating injection through nurses/professionals.

Also, looked at the Orange book and was surprised (in mixed ways), all the filings under Casper are NDA only with RLD ‘Yes’. Most of them are bit legacy though (approved prior to 1982) with moderate competition only.

Thanks,

Tarun

9 Likes

Any idea why Suven Pharma is grinding down inspite of good qtrly results?

Promoter has sold off his banjara hill property & has given hefty interim dividend recently . He is now nearly 71. how Is 2nd gen,daughters mostly US citizen , ? are they interested in running the business ?

can the co be sold off & price is being brought down?

2 Likes

I think Casper buys out trademarks for very old drugs. For the case of allopurinol, this website shows how trademark has changed hands over years.

8 Likes

BSE clarification from company today first time probably saying

Yes we are exploring possibility

Thanks

4 Likes

They are exploring.… ![]() ; if the moneycontrol news taken into account…and the sale is significant, expect an open offer as well. Market sensed it quickly, and have runup in last few days… seems 400 is the short term support.

; if the moneycontrol news taken into account…and the sale is significant, expect an open offer as well. Market sensed it quickly, and have runup in last few days… seems 400 is the short term support.

4 Likes

Promoter in final round to offload half of their stake.

2 Likes

Further progress on the stake sale; Valuation wise does not appear to be very attractive for retail investor given the price paid by Advent is close to current valuation. Am I missing something.

3 Likes

In near term nothing much may happen but it might lead to more aggression with a new owner coming in

11 Likes

3 Likes

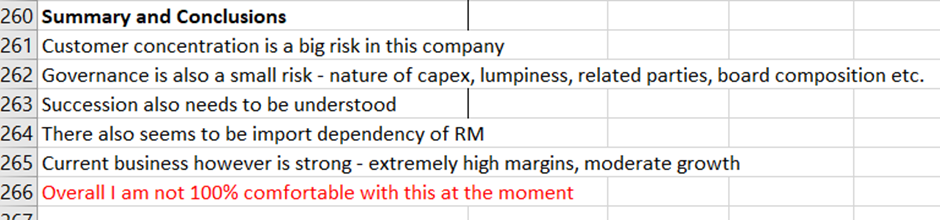

I was going through my old notes on Suven Pharma and came across the following lines:

“Overall, I am not 100% comfortable with this at the moment” is written in red. This is how analysis of FY21 Annual Report ended, so these comments must be dated around July – August 2021. I couldn’t pinpoint what exactly caused me discomfort – may be a Rs.600 crore capex of which only Rs.150 crore would go for increasing productive capacity, may be the alternating of a good quarter with a bad one almost as a set pattern, may be limited level of disclosures in the AR – may be all of this or something else - but something seemed missing. I did nothing about this – held on to my stock and continued to monitor.

In the Annual Report of FY22, I noticed details about Top Customers were missing. I wrote two emails to the company asking for this information but received no reply. Later in the concall post Q1 FY23 results, someone asked about this but the management did not reply. Rollback of any disclosure is a clear negative, if not a red flag.

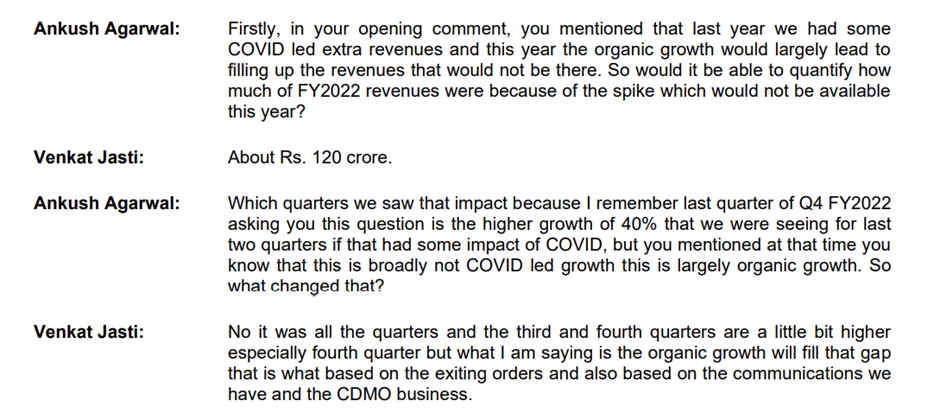

The Q1 FY23 results themselves had been disappointing, and the management blamed the same on Covid inflated revenues in the previous period. Below conversation is from the Q1 FY23 concall:

Last year, Rs.120 crore were covid revenues, mainly in the 3rd and the 4th quarter. But in the concall after the 3rd and the 4th quarter last year, management clearly denied any one off and stated that the growth was all organic. Below conversation is from the Q4 FY22 concall:

Transcript of the Q3 FY22 concall is not available but here are some quotes from the audio:

“things are moving well”

“run rate will be closer to the same thing as of quarter three”

“for the next 6 months things look good”

“things are better now”

“On the CRAMS side, the traction is much better for the next two quarters”

And after this, the revenues fell sequentially from Rs.392 crores to Rs.339 crores in the next two quarters. Quite surprising since the management always maintained they have visibility for 2 quarters.

In the interim, Suven had bought Casper, a deal which was looked upon unfavorably by the markets. But I was okay with the same (see comments here). The market saw a dilution of margins in the Casper deal, I thought it reduced the business risk.

By this time, the stock had also begun to underperform severely, indicating the market knew something which I didn’t, adding to my discomfort. I decided to exit the stock and did so in a phased manner. In any case, I had entered the stock soon after the demerger and a 3X return in less than 3 years was not a bad bargain.

In the TV interview after the current deal was announced, Mr. Jasti said the primary reason for selling out was a lack of successor (click here). However, there was no mention of this in the analyst call post the deal announcement, where the management repeated the ‘platform + value creation + global reach of Advent etc.’ ad nauseum as justification for the deal. But it is inconceivable that a promoter will completely sell out a growing company with top class margins for these benefits. It is like a husband telling his beautiful wife to elope with someone else so that she will be happier !

The lack of succession from within the family sounds a more credible reason for Mr. Jasti’s sell out. But still it is difficult to understand why he could not appoint a professional CEO and move to the background, like so many other Indian promoters have done – if Suven was as good a business as the market has generally believed it to be. The lack of successor point also brings to question the Rs.3 crore plus per annum (in dollars) paid out to Mr. Jasti’s daughter from the company’s books. One would have thought she was being groomed to take over the business. Her husband – also a healthcare professional - is also on Suven’s board. But evidently, the couple is either unwilling or incompetent to carry forward the business.

On the whole, Mr. Jasti’s sell out of Suven justifies the discomfort I carried with the business. With Advent merging Cohance with it, which itself is a company formed last month by merging three other companies, a deeper understanding of Suven Pharma as a standalone business will most probably never happen.

(Disc.: No positions)

41 Likes

During November 2020, Advent Int, a global private equity investor had acquired 74% stake in RA Chem Pharma Ltd (which earlier was held by Micro Labs Ltd).

Further, Advent envisages to build a merchant API platform and, in the process, has acquired a 100% stake in another two companies by the names, ZCL ( August, 2022) and Avra Laboratories Private Limited ( September, 2022).

The combined Total Operating Income of these three entities is about ₹1,300 crore. The three entities at the combined level derived around 80% of revenue from exports and ~70% belongs to the API segment. Substantial share of CDMO (30%+) in business with growth faster (35%+ CAGR) than other segments

-

RA Chem Pharma Limited (RACPL): Initially incorporated in 1996, RA Chem Pharma Limited (RACPL), is engaged in manufacturing of Active Pharmaceutical Ingredients (API), Formulations and Clinical research activity at its four manufacturing facilities. The company has a strong pipeline with 114 approved DMFs and 63 approved ANDAs. As of June, 2021, the company has 19 DMFs and 20 ANDAs pending for approvals.

-

ZCL Chemicals Limited (formerly Zandu Chemicals Ltd) is one of the well-known pharmaceutical companies in India engaged in manufacturing and exports of advanced drug intermediates and Active Pharma Ingredients (APIs). Established in 1991, it is headquartered in Mumbai and has a state-of-the-art successfully inspected and audited USFDA, EDQM, KFDA, WHO GMP, and COFEPRIS, Japanese MOH accredited facility with a capacity of 227,000 litres (60,000 gallons) along with strong R&D capabilities.

-

AVRA: Established in the year 1995, Avra is among the first in India to focus on providing high-end contract research and manufacturing of advanced intermediates and APIs covering oncology and other therapeutic areas. Avra was founded by AV Rama Rao, who is a highly experienced scientist by profession. It has several active process patents and is the only company in the world to develop and successfully commercialise a synthetic process for Irinotecan

Revenue Growth:

The total Operating Income at the combined level has witnessed a growth of about 23% from ₹1,060 crore during FY21 to ₹1,309 crore during FY22. Even between FY2020-21 growth was ~22% (from 866 Crs. For FY20)

The growth is driven by an increase in the sales volumes of existing products in new markets. The two-top selling products – ALPHA-Ph-2-piperidine acetic acid and Mebeverine (cumulatively account for 16% of FY22 sales) – increased by more than 50% as compared with FY21 owing to increased demand. (soure of growth, sustainable??)

Margins:

The profitability margins of the company marked by PBILDT margin were 26.68% in FY20 to 21.84% in FY21 and 27.22% for FY22. The PBILDT margins moderated during FY21 due to incurring of considerable onetime professional charges of Rs.26.98 crore

Profit after-tax (PAT) margin of the company has gone up from 16.59% during FY21 to 16.76% during FY22.

28% EBIDTA, growth of 28% between FY20-22.

Revenue Mix by Geo/Segments:

On a combined basis, the domestic sales of the three companies are only around 20% in FY22. The majority of the sales, ie, 80% are derived from exports. The company at the combined level derived over 50% of its TOI from regulated markets, with Europe contributing about 27% and the US contributing about 20%.

- RACPL: major revenue derived from exports (70.65% during FY21 against 70.75% during FY20). The company exports its products across the regulated pharmaceutical markets of Europe (18.09%), Asia Pacific (8.43%), Middle East (12.73%) and Latin America (11.10%).

- ZCL: 88% revenue from regulated markets. 42% revenue from Innovators. 30% are patented products.

Therapeutical Mix:

The company at the combined level has over 100 products, top 10 products contribute about 45% to the TOI. Furthermore, in terms of the therapeutic segment, the company derives about 47% of its TOI from therapies such as anti-depressant (17%), anti-spasmodic (10%), attention deficit hyperactivity disorder (ADHD; 8%), anti-psychotic (6%), and anti-epileptic (5%).

Leadership (top 3 position) in 8 key molecules driven by deep cost position due to backward integration/ Amongst top 3 players globally in most of our key molecules including Betahistine, Drotaverine, Entacapone, Fluvoxamine, Lamotrigine, Mebeverine, Midazolam and Quetiapine amongst others

- RACPL: RACPL has a presence across 42 therapeutic segments and majorly caters to niche therapeutic segments viz. Anti Spasmodic, Anti-Depressant, Veterinary products; besides Anti- fungal and Obesity.

- The top 5 therapeutic segments contribute to 56% of the revenue during FY21 as against 49% during FY20. For FY 21, the revenue contribution of Anti Spasmodic stood at 16%, Anti Depressants stood at 15% , Anti epileptic stood at 10%.

- RACPL has a diversified product portfolio with top 10 products contributing to 67% of the revenue during FY21 as against 39% during FY20.

- Further, RACPL has a diversified client base comprising some of the reputed players in the industry viz. Selectchemie, Helm De, Welding, Intas Pharmaceuticals; Aurobindo Pharma among others.

Infra:

-

RACPL has four units i.e. two API unit and two formulation units (located at Nacharam and Jadcherla Hyderabad). Further the company has Bio Analytical and Bio Availability studies unit located at Balanagar, Hyderabad and one API R&D unit in Kukatpally, Hyderabad.

-

ZCL has an API and R&D facility at Ankleshwar, Gujarat, and these facilities are successfully inspected and audited by regulatory authorities such as the USFDA, EDQM, KFDA, WHO GMP, and COFEPRIS, a Japanese MOH accredited facility.

-

Avra has two API and two R&D facilities and its manufacturing facilities are located in Hyderabad (USFDA and WHO GMP-approved) and Vizag. These facilities are duly approved by various regulatory authorities.

Working Capital:

The working capital cycle of Cohance, although improved, still remains elongated and stood at 148 days during FY22 (FY21: 152 days).

The average inventory days increased from 107 days during FY21 to 114 days during FY22. The high closing inventory is on account of orders which materialised in Q12023. Furthermore, the company has to maintain an inventory of semi-finished goods and finished goods to meet the expected demand as part of its growing business, resulting in a stretched working capital cycle for the company.

- For standalone RACPL: Average Inventory days improved from 98 days during FY20 to 92 days during FY21. Further, Average collection period stood high at 115 days during FY21 (115 days during FY20).

Capex:

RACPL has completed capex of Rs.70 crore during FY21 without any cost or time overruns. This capex was funded through term loan of Rs.44 crore and balance Rs.26 crore from internal accruals. Further, during FY22 the company was scheduled to incur additional capex of Rs.70 crore which will be funded through term loan of Rs.8 crore and balance through internal accruals. The proposed capex pertains to capacity expansion at API and FDF units and towards regular maintenance and upgradation at other unit.

Likewise, Avra was scheduled to increase production capacity by ~50% (100 KG/day to 158 KG/day with a capex of ~15 Crs,

Overall, at Cohance Level, >2x expansion potential on invested capex - Fully invested in capex with current capacity at 7 plants - enough to support 2x current scale

Gearing:

During the year, the company at the combined level, has reduced its long term debt from ₹95.19 crore to ₹77.34 crore. Contrastingly, the short-term debt has increased from ₹89.14 crore to ₹149.39 crore to fund working capital requirements.

at the combined level, the total cash and liquid funds are about ₹270.72 crore as on March 31, 2022, which provides an additional cushion.

The net cash flow from operations with an improved scale of operations is expected to remain at about ₹300-350 crore going forward

I think more clarity will emerge once the consolidated (Suven + Cohance) pro-forma financials are released and internal re-alignment of portfolio (between CRAMS, API, Formulations). However, on the face of it, looks like this will be broadly ~ 60% CDMO/CRAMS/Research and 40% API/Formulations entity at consolidated level.

From growth perspective, will have enough head room considering the recently concluded capex by RACPL and Avra (50% addition from current capacity). For Cohance side, even in past two years the growth rate has been ~22%ish. Cohance website is indicating about 2X capacity headroom (ex of Suven for now). Even on Suven side, they have earmarked ~600 Crs (mostly internal accruals) over 3 years towards bolstering R&D infra.

As with most PE investments, Advent will have an accelerated growth road map. Within India and Globally, they are well invested and networked in pharma domain to drive cross sell and synergies. ( In the recent Suven call someone hinted about Advent aspiration for making the Cohanc platform a $1B entity)

Another interesting possibility/conjecture could be related to Bharat Serum and Vacines Ltd. Advent had picked majority stake in Biopharma player BSV in 2019 for ~$250M - 257M. Bharat Serum is a niche player in Gynecologic and assistive productive segment with revenue of ~900 Crs in FY20. Further, BSV have strengthened market position with recent acquisition of TTK health’s reproductive business segment. So far, BSV/TTK health are not part of the Cohance platform however, interestingly have significant management/Board overlap across Cohance and BSV+TTK. Will be too early to conclude one way or other since consolidation may depend on product/tech synergy and Advents exit horizon for BSV. However, even at separate stand alone entity basis, may have overlapping business opportunities.

From Product portfolio perspective, what caught attention is the mention of “Amongst India’s leading manufacturer of high purity electronic chemicals”. My understanding is that these are product offering by Avra Synthesis which is different entity (from same promoters) then merged entity Avra labs.

[Worth evaluating further,what is the key product/tech differentiation between Avra Labs and Avra synthesis]

Even otherwise, Avra has some interesting product relationships (with innovators for blockbuster drugs):

- Ticagrelor ( Brilinta) - The drug is produced by AstraZeneca. Avra provides complete GMP manufacturing of Ticagrelo

- Lenalidomide (Revlimid) - Avra provides complete GMP manufacturing of Lenalidomide API for Form-A, Form-B and Form-I and has an Open Part DMF available.

- Carfilzomib - Anti Cancer Drug

- Eltrombopag (Promacta) - It is being manufactured and marketed by Novartis under the trade name Promacta in the US and is marketed as Revolade in the EU. Avra provides complete GMP manufacturing of Eltrombopag Olamine API.

Likewise, ZCL has impressive profile - 43% revenue from Innovators, 30% from Patented products. Also, noticed that they have API for one of the successful commercial product Jardiance (Dapagliflozin) and multiple combination doses around same under development stage.

On flip side, Suven had an envied margin profile to the north of 40%. Current Cohance EBIDTA are around 28%. Merged entity will have a drop in margins. Also, working capital is really elongated at ~150 Days for API side of the business. Finally, modality of merger, valuation of entities, extent of dilution and overall consolidation deal structure are big monitorable for now.

Thanks,

Tarun

Disc: Invested, No recent transaction, tracking the development.

32 Likes

Fabulous analysis.

The product profile of each of these entities looks quite attractive.

Having worked closely with ZCL, I can say they are a very balanced organization and have good long term relationships with their customers. For some of the products, they are the only supplier.

They too like Avra are getting into Electronic chemicals. Again very high value high margin products. Infact, they have already reached a scale of doing multiple pilot campaigns for the electronic chemicals.

My ex-company was a supplier ( Indian subsidiary) as well as their customer ( US subsidiary). Last 3 years have seen accelerated revenue growth from them.

14 Likes

And the results are out, big jump in revenue and profits QoQ ! https://www.bseindia.com/xml-data/corpfiling/AttachLive/c750c20f-3250-4b45-ba0d-1b77a8c4dc85.pdf

1 Like

US FDA accepts supplemental New Drug Application for Jardiance® for children 10 years and older with type 2 diabetes

Innovator has expanded the market by proving drug effectivness for 10+ Years childrens.

Tarun

4 Likes

Cohance has published recent investor presentation (link). Very detailed as compared to last one with expanded view and additional details on each of the business verticals:

[Note: This is proforma consolidated numbers and summary for RA Chem, ZCL and Avra Labs. Suven numbers are not consolidated till now under presentations.]

Key readings:

- Revenue growth of 21% CAGR between FY19- FY21. Consol. revenue FY’22 of 12802 INR Mn.

- EBIDTA margin 28% for FY’22. margin growth CAGR of 32% between FY’19 - FY’22.

- Business Mix - 65% API, 30% CDMO and rest 5%. Good growth and higher contribution from CDMO.

- Concentration - Top 5 customer 20% revenue, Top 5 products 32% of revenue

CDMO:

- CDMO across pharma and speciality chem. Relationship are mostly 6+ years old with innovators.

- 36% growth between FY20 - 22.

- Cohance supplies intermediates of several NCE’s involved in ongoing clinical trials with large potential including:

- Lung cancer drug in Ph III;

- Anti-thrombotic drug starting Ph III;

- Active discussions for various other supplies

API

- Portfolio of Nascent high-potential products (9 molecules) with near term potential of 3 billion.

- 24% CAGR growth between FY’20 - FY’22.

- Pipeline products (12 molecules) - Mid term potential of 10 bn.

- Semi regulated market focused fillings: 15 China, 10 Brazil.

Overall capability and Capex:

- Capacity expansion from 850 kL at acquisition to 1,330 kL in FY23 & 1,500+ kL by FY24.

- CWIP of ~50 Crs for FY’23.

- Capex of ~ 6 % - 7% of revenue.

- Cash and liquid investment - 412 Crs.

Overall, Advent has steared the Cohance ship quite well for last 2.5 year. 1.8x revenue over the last 3 years at 20%+ CAGR. Have added 40+ customers since acquisition. Discussions underway with 10+ global innovator pharmacos for opportunities in lifecycle management of genericized molecules. Pipeline of new products with mid-term sales potential of INR 10 Bn in an addressable mkt of ~INR 100 Bn

They are looking at Cohance as a platform for all things Pharma/API/CDMO under Advent. Should auger well for Suven post full integration.

Disc: Invested

Thanks,

Tarun

13 Likes