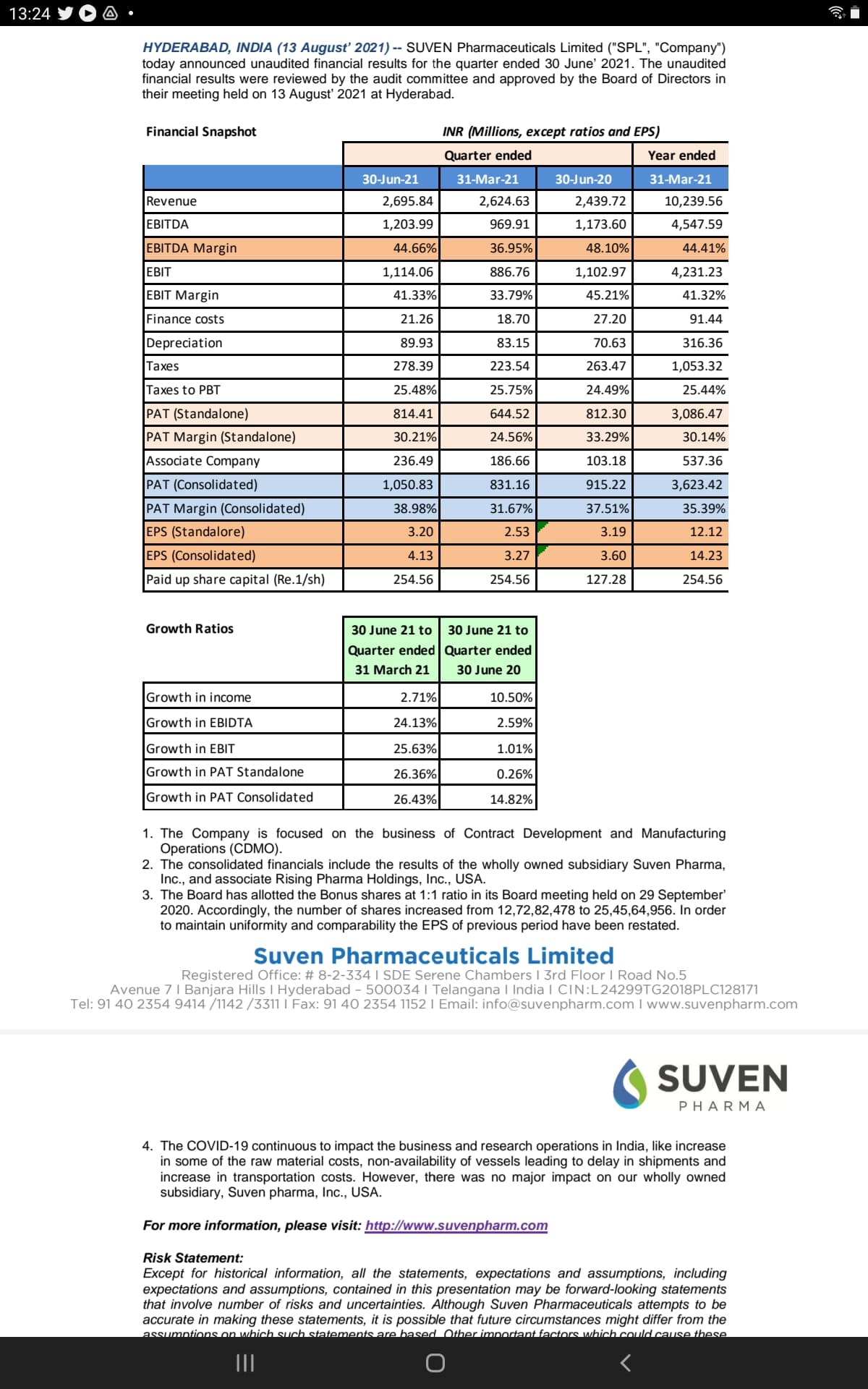

Quarterly results are out. BSE receipt time 13.18 hours

At first glance, year on year figures are good but Q on Q can be a discussion point

2 Likes

Suven Pharma Investors Presentation

Just wondering. Why does the company sell intermediates and formulations but not API? Or does it? I did not see it mentioned anywhere. Would be glad if someone could clarify? Maybe because they are trying to do entire life cycle of pharma they will do now, but why not earlier?

1 Like

Suven Pharma’s Venkat Jasti On Mfg Of Molnupiravir & 2-DG MoU:

FYI,

The company manufactures formulation but do not market and sell it. It partners with Rising Pharma Holdings for that purpose.

And it is into intermediates (Key starting materials) in order to backward integrate for their CRAMS portfolio. They indeed have the capabilities to enter into API space, but APIs (especially generic APIs) are high volume low margin plays and will dilute their margin profile unless they do things like what Divi’s does. And that requires entire different focus.

5 Likes

A bit dated initiating coverage report by Monarch Capital (21st Dec, '20)

2 Likes

Must watch video.

Detailed presentation on why we should keep on holding Suven as substantial portion of our portfolio.

In case anyone has more info on the subject, pl do share

CVOCA INVEST-O-NOMICS - Fundamental Analysis Research by Harini Dedhia - YouTube

Disc, : Invested recently

8 Likes

Some of the key points from Suven Pharma FY2020-21 Annual Report:

Business Overview:

-

Suven has established its core competency in cyanation and heterocyclic chemistry, including pyrimidines, quinolones, thiazoles, and imidazoles, in addition to demonstrating our proficiency in Carbohydrate and Chiral chemistry including tetrahydrofurans, amino acids and sulfoxides from gram to multi-ton scale.

-

Our focus NCE-based CDMO A full-fledged biopharmaceutical solutions provider for global pharmaceutical companies

→ Present across the entire CDMO value chain – intermediates & APIs

→ Working with innovator companies in developed markets having stringent regulations

→ Long term commercial supply with the launch of product by global sponsors

→ Repeat business owing to long standing relationships with MNC companies

- I can say with pride that Suven Pharma would be the only Indian pharmaceutical company to report, on a consistent basis (for the last five years) and EBITDA margin in excess of 40%.

CDMO:

- This is flagship business vertical of the Company contributing more than 62% of its topline. The business comprises of clinical and commercial CDMO projects.

- While there was no addition to the Commercial molecule portfolio, marginal increase in volumes resulted in some revenue growth from this segment.

- It was a good performance. Revenue from this vertical increased by more than 30% which, under the prevailing circumstances, was very satisfying.

Specialty Chemical:

- But what was heartening is that we initiated commercial supplies of a third molecule towards the close of the financial year. This, I expect should add some volumes in the current year.

- Also, there is one additional molecule which is in the development stage currently; it could become commercial in 2023 maybe. So things are moving in the positive direction.

Formulation:

- The formulation vertical did very well. We widened our product basket with 5 new commercial launches

- We increased our commercial formulations basket in FY21 and have a pipeline of 6 ANDAs that are pending approval. I expect these filings to receive the stamp of approval in the current year.

- Additionally, we hope to file another 6 ANDAs during FY22, enhancing our growth levers.

- Going forward, we expect to deliver 10-15% growth on the expanded topline.

- Having said that, I must add caution, that this is a very small vertical currently, by design. For we have cherry picked very small volume, niche products which are bereft of competition owing to the brand market size (US$2- 5 million per product). Despite sustained addition to the product basket, the overall size of the formulation piece, will remain relatively small when compared to other verticals.

Current Concluded Capex (320 Crs.):

- We were implementing a Rs. 320 crore capex plan which had three parts to it 1) the multi-purpose facility at JNPC Vizag, 2) an OEL4 capacity at Pashmylaram and 3) a new formulation facility (adjacent to the existing one). This capex plan was completed in FY21.

- In our business, we need to invest proactively, maybe 12-18 months before an opportunity materialises into reality. For example, our Vizag facility is being used for specialty chemical intermediates. We have started the commercial batches for a third molecule and are hopeful of a fourth about 18-24 months from now. The formulations unit will also be sufficiently occupied in the next 18-24 months if our plans over the coming months see the light of day

Future CapEx: (600 Crs.)

- We are not investing for returns, we are investing for our sustainability.

- The plan: It is a three-pronged investment 1) relocating our R&D center due to zoning regulations, which will take two to three years 2) replacing the 30 year old blocks (one at a time) and with upgradation and some balancing equipment at our Suryapet facility, and 3) adding a new block meeting FDA and other regulatory requirements in Pashamylaram.

- This is not just modernising, but it will be a block-by-block overhaul and upgradation. In doing so, we will introduce sophisticated equipment and absorb cuttingedge technology which will enhance productivity and improve resource utilisation. If this investment is not done now, Suven Pharma, over the next few years, will not be able to meet customers, regulatory and technological requirements

- Our relocation initiative will significantly upgrade our R&D facility in terms of capability and technology, such as high potency capability, continuous chemistry, etc. This, I am confident, will enhance our competence to undertake a wider spectrum of research projects and sustain our 40%-plus EBITDA margin that positions us out of the pharma clutter.

Business Model specific:

The Management has, through its Annual Reports, consistently explained to shareholders that the common parameters by which they apprise the performance of other companies do not apply to it. Suven needs to be evaluated on its strengths and its strategies that promise to make its business sustainable. The success of the Company is reflected in important realties 1) it has consistently delivered on its commitment 2) its profitability is among the highest in India Inc. 3) it has created wealth for shareholders through its performance which not many pharmaceutical companies can boast of.

Growth Guidance:

- We hope to grow by about 10- 15% in FY22. This is subject to the race between the virus and the vaccine panning out across the globe. We hope to sustain our profitability as we go forward. In doing so, we will be able to generate healthy returns for our shareholders.

- Suven has lived upto its commitments. In FY21, the Company has communicated a 10-15%topline growth. It delivered a 20% topline growth. Going forward, the Company appears confident of sustaining this growth. This optimism is based on certain formulations in the pharmaceutical and agrochemical spaces which were commercialised in FY21 (which are expected to gain traction in the current year) and some molecules which will get commercialised in FY22 (which will add to its revenue basket). Moreover, the research projects, the bread and butter for the business, continues to gain traction as the Company continued to deliver on its commitment.

Thanks,

Tarun

Disc: Invested

29 Likes

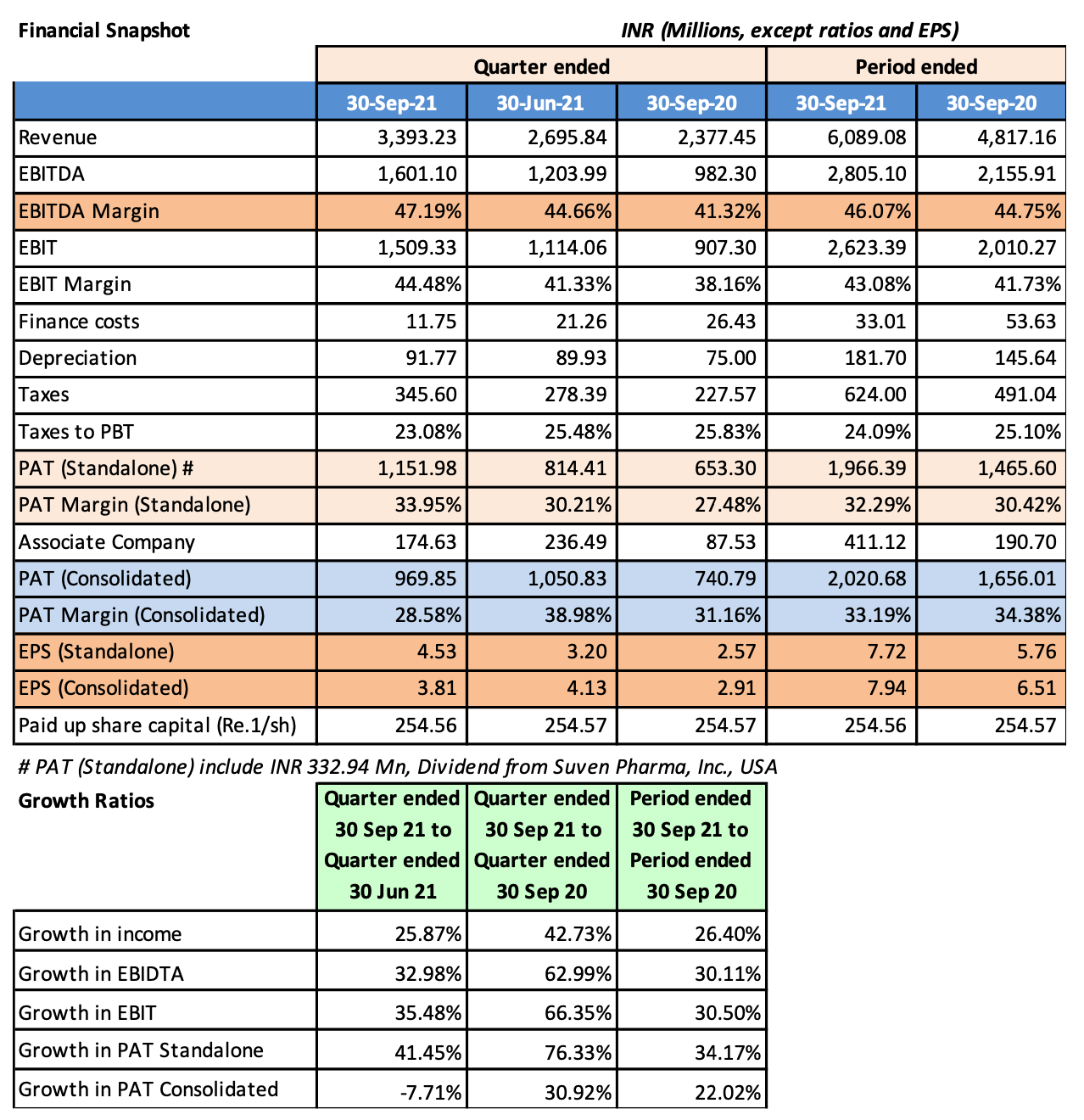

- Margins are back at regular levels of 45% EBDITA

- Cherry on cake is Associate profit numbers - 24Cr Q1 FY22 vs , 19 cr Q4 21, 10 Cr Q1 21, 53 Cr FY 21

For FY 22 , Top line may grow mid teen to high teens , bottomline could grow meaningfully higher proportion - aided by Associate/ Rizen performance as visible in quarterly performance - concall could provide more details

Invested

9 Likes

Decent performance despite margin pressure…

About the stock: Suven Pharma is a CDMO that supports global life sciences

industry & fine chemical majors in their NCE development endeavours. Its services

include custom synthesis, process R&D, scale-up & contract manufacturing.

Business comprises three segments – CDMO (development projects and

commercial supplies), specialty chemicals and contract technical service

CDMO vertical contributes more than 62% of its topline. Owing to its CDMO

competence, it has developed & supplies intermediates for two specialty

chemical products (agrochemical) to large global conglomerates

Q1FY22 Results: Suven reported strong Q1FY22 results.

Sales were up 10.7% YoY to | 263.8 crore

EBITDA in Q1FY22 was at | 114.6 crore, up 2.3% YoY with margins at 43.4%

Consequent adjusted PAT was at | 105.1 crore (up 14.8% YoY)

What should investors do? Suven’s share price has grown by ~1.6x over the past

five years (from ~| 316 in July 2020 to ~| 506 levels in July 2021).

We retain our BUY rating on this stock

Target Price and Valuation: We value Suven at | 650 with 32x P/E on FY23E EPS

Key triggers for future price performance:

The company has announced a | 600 crore investment – in upgradation of

facilities, absorbing new technology & moving its R&D – executable over a

two to three-year horizon, benefits of which may be visible in the long run

Formulations have registered healthy growth due to increased commercial

basket & have a pipeline of six ANDAs in FY22, enhancing growth levers

Focus on research by global innovators has intensified post Covid & augurs

well for pharma CRAMS operations, which remain a key growth driver

Alternate Stock Idea: Apart from Suven, in our healthcare coverage we like Divis.

Divi’s is engaged in manufacturing generic APIs and intermediates, custom

synthesis of active ingredients and advanced intermediates for pharma

MNCs

BUY with a target price of | 4916

Key Financials

(| Crore) FY20 FY21 CAGR

(FY20-21) FY22E FY23E 2 year CAGR

(FY21-23E)

Revenues 833.8 1009.7 21.1 1118.0 1284.6 12.8

EBITDA 384.8 442.4 15.0 485.7 587.7 15.3

EBITDA margins (%) 46.1 43.8 43.4 45.8

Net Profit 317.0 362.3 14.3 426.0 516.7 19.4

EPS (|) 12.5 14.2 16.7 20.3

PE (x) 43.7 38.2 32.5 26.8

EV to EBITDA (x) 36.4 31.2 28.4 23.3

RoE (%) 37.5 30.7 26.9 24.9

RoCE (%) 35.6 31.2 26.8 26.5

Particulars

Particular Amount

Market Capitalisation | 13847 crore

Debt (FY21) | 141 crore

Cash (FY21) | 10 crore

EV | 13979 crore

52 week H/L (|) 590/292

Equity capital | 25.5 crore

Face value | 1

Shareholding pattern

(in %) Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Promoter 60.0 60.0 60.0 60.0 60.0

Others 40.0 40.0 40.0 40.0 40.0

Price Chart

Recent Event & Key risks

Embarking on a | 600 crore

investment, largest since inception

Key Risk: (i) Lumpy nature of

business (ii) B2B model with heavy

reliance on management guidance

Research Analyst

Siddhant Khandekar

siddhant.khandekar@icicisecurities.com

Mitesh Shah

mitesh.sha@icicisecurities.com

2 Likes

Suvenpharma With 5 molecules in phase-3 & moving from intermediates to API (30-40% margin in API) big chances of re-rating here

2 Likes

Suven trades at 13 times sales and has a 600 cr maintenance capex coming up. Not cheap by any stretch, and returns on incremental capital over the next year or so will be low IMO. Not expecting any upward re-rating. Rather a time correction is likely.

7 Likes

CNBC interview

SuvenPharma is in focus today as its input costs have surged in the past month due to the China power outage. @_soniashenoy & @SurabhiUpadhyay speak to CMD Venkat Jasti who says that margin could be impacted by 5-7% due to high input costs. @ekta_batra https://twitter.com/CNBCTV18News/status/1446313668774285320/video/1

3 Likes

Promoter is usually conservative and has been since last 2 Qtrs on demand side and now supply side as well.

If Suven core CRAMS biz is considered a many small projects for many small biotechs, here margins are usually not a challenge as Suven has some pricing power, key is demand pick up which should be coming back given lots of these projects would.be reviving again as Covid takes a back seat.

At best it could impact current quarter margins as he called out by few%.

A silver line possibly is that Logistics costs are dropping nicely as per some tweets, Suven has more impact from shipping as breadth of projects are more. This should cushion to some extent. Didnt see that being called out in interview.

Suprises me sometime that Promoter themselves gives interview responses with myopic views, while channels ask questions that are of short term nature but its up to management to give both prespectives( short andnlong term). Some managements are good at that some are not. Mr.Jatsi is a no nonsense and to the point kinda person.

Anyways these are temp hiccups and any meaningful correction could be good opportunity to add, CRAMS long term theme seems intact.

Invested

6 Likes

Results look quite good at standalone basis, 47% EBITDA margins. However, margin pressure is visible at the consolidated level. CFO declined in H1 due to increased inventory and trade receivables.

4 Likes

From AR 21

What are the estimates for FY22?

We hope to grow by about 10-15% in FY22. This is subject to the race between the virus and the

vaccine panning out across the globe. We hope to sustain our profitability as we go forward. In doing so, we will be able to generate healthy returns for our

shareholders.

Add this with press releases notes caution notes

Management has been warning on margin front, though not much visible in Q2 numbers. Also H1 gives the desired rev guidance even if H2 was to be flat.(1000 cr was FY21 rev, upper end of guidance put it at 1150 cr for FY 22, they have done H1 22 at 565 cr rev, H2 22 they need 600 cr to meet guidance and H2 21 was 560 cr - so 8% type growth will take them to guidance). Also note Q3 21 was exceptional on margins at 50%, unlikely to beat that in Q3 22, so even at low single digit rev growth on YoY, EBIDTA could take a meaningful beating.

Would be interesting to see commentary in concall for H2 - whether they revise guidance for FY22 or better part was delivered in H1 and lumpiness to play out in H2 with flattish performance, given conservatism history of mgmt.

Learning- CRAMS/CDMO- better to base thesis on YoY to be on safe side to factor lumpiness, extrapolation of Qtrs tend to lead to trouble.

Invested from lower levels

7 Likes

2 Likes