Sorry, I couldnt find any mention of QIP in the con call ? Was it a speculation or were there any mention of QIP in concall ?

From concall, I felt that they may be funding capex from internal accruals or reserves/debts. Capex of such a magnitude may delay, free cash flow generation for some time. If so it may have a slight negativity in the near term, till they can come with better quarters vindicating their claims.

Also as per the management, they have not clearly defined how to use the 600 crore capex, Being a conservative management, expected them to have a pre-defined plan for capex first (Like machinery/process/accreditions which they were planning and a clear timeline) . Can you give your views on this ?

@Worldlywiseinvestors has summarized things very well but I still see enough speculation on certain aspects. What I understood:

Capex: As some people have noted the 600 cr. capex is for sort of a renovation of the company’s buildings and facilities. I guess the management did state explicitly that this would take care of the next 20-30 years. However,since technologies and customer requirements keep changing this may not hold true. The capex will be done over 36 months. So an average of 200cr./year which is well within the realm of Suven’s internal accruals. The management also said they will maintain the same kind of financial prudence as they have done in the past. Importantly,after a fair gap Mr. Jasti sounded quiet upbeat on future prospects for his company and the sector in which they operate. The renovation should help in a big way for attracting new clients.

Sale of company: As Mr. Jasti noted that whenever he tries to reach out for funding for Suven Life Sciences,media speculations around the sale of Suven Pharma restart.It’s pretty clear to me that Suven Pharma is not on the block and whatever attempts are being made to raise funds is for SLS.It makes sense too since SLS is a cash hungry business while Suven Pharma is a cash cow.On the other hand,some people might interpret this renovation as a means of attracting potential buyers.Again I don’t see what’s so negative if a promoter wants to sell his stake and get a good sum for it.What matters is the new investor or set of investors and what valuation the deal is agreed upon.All this is still in the realm of speculation but I don’t see it as any overhang on the company.At worst it will be a short-term disruption.

I had been personally building in a 1000cr. kind of FCF generation from Suven over the next 3 years.That goes for a toss now but if this capex will bring in higher growth rates then I welcome it.Mr. Jasti and his team have been prudent capital allocators and there is little to doubt that it won’t be the same this time.

As Suven derives majority of it Revenues (Almost 80%) from Europe. Does the increase in Covid cases in Europe affect Suven in near term. I believe the forecasts for H2FY21 is based on the orders already in pipeline and even if there are intermittent lockdowns in Europe its effect maybe visible from FY22 onwards.

This might be a dumb question, but wanted to check, Since Suven only manufactures Intermediates, do they need any USFDA approvals? Do their manufacturing facilities have any USFDA certifications? As far as I understand it, companies need to file DMF for APIs and ANDA for FDF and for those filings, the USFDA approvals (for [facility, API/FCF] pair) is required, but not sure about intermediates (which are N-1 and N-2 for the API).

If the deal goes through and the controlling stake is bought by any of these PE firm, this may have a potential to evolve into a Sequent like situation where the MNC ownership has worked very well for the minority shareholders till now.

CRAMS and intermediates are both very profitable segments and are expected to keep enjoying industry tailwinds in near future.

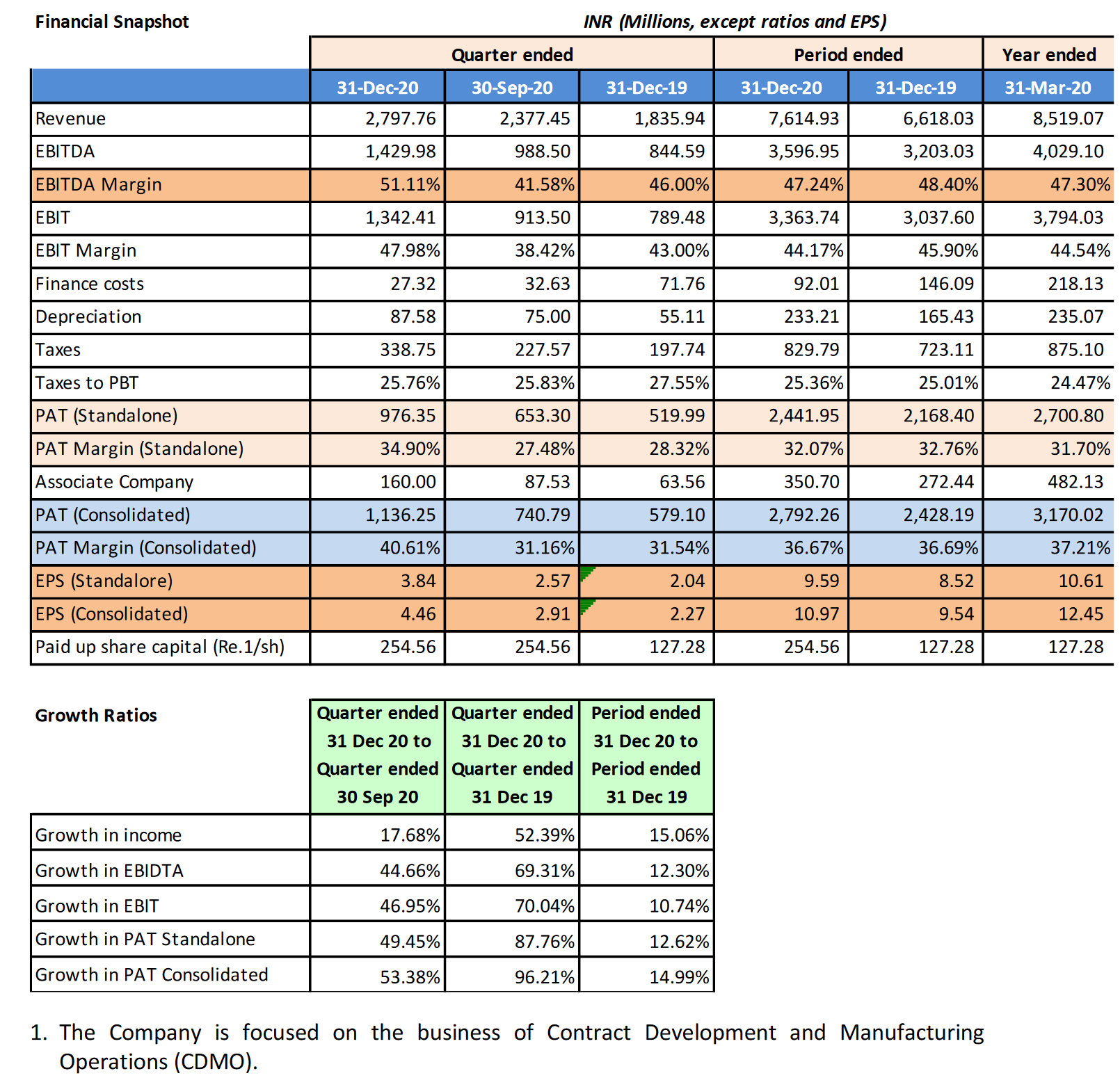

Excellent results post the fiasco in Q2.Mr. Jasti had maintained that Suven will be able to close the year with 15-20% kind of bottomline growth,they now seem well on track.I feel more than anything this increases the management’s credibility and should help in sustained re-rating.Barring quarter to quarter volatility Suven remains a very good,structural story.

As per this call still suven can grow 15 to 20 % top line and eventually bottom line …compounding still left for some more yrs… can we assume like that

Does anyone here know or understand the below things about Suven pharma?:

Who are those big global “innovator” pharma companies (Suven’s customers) that Suven does CDMO for ?

The names of top customers should be mentioned rather than hidden by the company in order to attract more such customers and build investor faith. I dont understand why they hide.

Its ok to not mention what molecule are you doing CDMO for but atleast the name of the customer should be known

Are CRAMS business revenues predictable from year to year ?

Can one assume secular growth ? Or is there a degrowth scenario also possible?

Why are CRAMS revenues volatile from quarter to quarter?

How come margins are higher than any other listed player catering to the same space? People say CDMO for NCE before commercial production starts.

Won’t these margins erode as almost everyone rushes to enter pharma CDMO ?

One could do capex, hire their workforce and do CDMO work for these innovator companies. So, where’s the moat ?

I could’nt see the mgmt. (Mr Jasti) having a clear multi-year vision or growth strategy in place. Does anyone know what it is?

Summarizing some of the key points from Annual Report 2020 (Link)

Business Direction:

You must be wondering what drove us to create an independent entity. The answer lies in the questions you had been posing before us: Why are you restricting yourself to a small part of the entire value chain? Why aren’t you expanding your activity? What stops you from leveraging your deep chemistry skills in synergic verticals? And, so on. In response to all your queries, here I present your very own company, which is focused on expanding its horizon, vertically and laterally, with the objective of emerging as a full-fledged pharmaceutical solutions provider.

From a medium-term perspective, by when we will hopefully see our strategy in motion, our business profitability should be evenly balanced between our three verticals – CDMO-Pharma, CDMONon-Pharma and formulations – making Suven a full-fledged pharmaceutical solutions provider.

CDMO:

Suven supplies intermediates for four molecules addressing rheumatoid arthritis, diabetes, depression and women’s health for clients based in the US and EU.

In a few years from now, CDMO will not be the same. We are manufacturing only intermediates today, and we would be doing much more tomorrow.

We are steadily building the infrastructure and capabilities to reach that level. Suven Pharma will not just be about CDMO. It will be a lot more. Even in CRAMS, which was until now restricted to intermediates, will now straddle the pharmaceutical value chain. We will also expand our customer profile from innovators to virtual companies and local markets for multinationals.*

In base CDMO, we secured new projects and gave supplies for one late-stage development project. We saw good growth in commercial supplies and volumes. We delivered ahead of schedule because our customer’s campaign had ended. But there is a caution here. Revenue from commercial supplies will remain uneven. This is because once a customer buys one batch of material, the next order comes usually after 12-18 months, depending on how the customer campaign had ended

Specialty Chemicals:

It was a stellar performance by the specialty chemicals segment. But this was not entirely unexpected. We are supplying intermediates to two commercial molecules, one of which was launched by our customer towards the close of 2018-19. Hence, we expected additional volumes for the intermediates of this new product. And it happened

The first molecule was a bit of a surprise, though. A year back, the supply of the intermediate for this molecule dipped because the molecule came out of the patent umbrella in certain geographies. Our customer was agile and regained the patent applying the combination technique. This brought in additional intermediate supplies for Suven in 2019-20.

We are developing two molecules which we expect to commercialise in 2020-21. These molecules have the potential to generate an annual revenue of about $7 million (H50 crore) each at optimum volumes. But the scale-up to this level will take time. It will depend on the traction which our clients’ products attract globally

Formulation:

We had one formulation as on March 31, 2020 for which we were supplying commercial volumes. We have started commercial supplies for two more products, and we hope to supply commercial quantities for a third by the end of FY21, taking our commercial formulations tally to four by the end of 2020-21.

We have profit-sharing agreements with our marketing partners which are marginally revenue-growing but significantly return-accreting.

We have carefully chosen to be in products that have recently gone off-patent. Hence, there will be no conflict of interest with our existing CDMO clients.

Raising Pharma:

Rising Pharma Holdings, Inc., our associate, may also assist us in enlarging our formulation venture. Rising is a development and distribution company in the formulations space. It has many ANDAs in development every year with its partners. Some of those may fit into our capability matrix. For those products, we will have the first right of refusal^. I look forward to projects coming out of Rising. The additional advantage with Rising is its strong forte in distribution.

(^ My comment- though the first right to refusal was denied by Ventak during the last concall)

Suven and Rising. For one, we can and hopefully will, help them develop their ANDA pipeline. Out of the 11 ANDAs filed, two are those of Rising’s. We will also utilise their expertise in distribution of our formulations. One commercialised product is being distributed by them. We would continue to explore and work on other mutually beneficial opportunities.

Rising Pharma has reported a profit in CY2019. We will get a share of profits only when the Company declares a dividend. Rising Pharma is a growing company which has just turned around. It will need funds to build stability in the marketplace. In keeping with this reality, we can expect a dividend only after a year or two.

CapEx:

To cater to these opportunities, we drew up a Rs. 320-crore capex plan which includes creating a multi-vertical capacity. Out of this, Rs. 210 crore was pumped into the business up to 2019-20, while the rest will be invested this year. Our OEL facility – a highly sophisticated and automated unit which operates in a closed atmosphere – began operations during the year under review, while our other facilities such as specialty chemicals and formulations will go on stream this year.

At Suven, we have to take tough strategic calls. This capacity creation is one such call which is based on interactions with customers and the future requirements. The intrinsic value from our investment will come when we are able to secure projects appropriate for our capacities. Till then, we have the flexibility to utilise it for other products.

Misc:

In terms of team expansion, the next generation of the founder Mr. Jasti have stepped in to learn the business ropes. His daughter, who has been with the Company for 8 years, is efficiently managing the affairs of Suven Pharmaceuticals, US. An engineering graduate and an MBA, she has been the customer interface for the last 4-5 years handling customer negotiations.

Revenues from one of the customers of the Company’s in Europe was Rs. 30,966 lakhs representing approximately 37.89% of the Company’s total revenue, for the period ended 31st March 2020 and Rs. 15196 lakhs representing approximately 41% of the Company’s total revenue, for the period ended 31 March 2019.

Thanks @T11 for summary.

Concerns:

I checked the leadership of Rising pharma on its website. Researched the guy Vimal Kavuru listed as its CEO. He started multiple unrelated businesses registered in both India and US. I dont see any “strength” as such of this Rising pharma and am doubtful of why this deal was done by Suven. Dont see any distribution “forte” there.

Regarding CDMO pharma, non pharma & specialty chem business: Suven never talks anything specific. Which customers? What chemicals? What advantage they have over alternate suppliers? Whats the revenue visibility if there are contracts with customers (as in the current outstanding Order book?)