Very useful discussion guys, thank you. @bhambani @sahil_vi @ankush12495

One question: Any idea who Suven’s largest customer is? Contributes almost 40% of the revenues.

Very useful discussion guys, thank you. @bhambani @sahil_vi @ankush12495

One question: Any idea who Suven’s largest customer is? Contributes almost 40% of the revenues.

Suven’s biggest customer… no clarity on that at the moment.

Only clue is that with 78.6% revenue coming Europe, the customer has to be a European Pharma entity

The revenue from biggest customer has come down slightly to 37.89% in FY20, a small comfort, if at all. The customer concentration risk is definitely very high, and not knowing / being able to track the dependency’s financial well being does cause some discomfort. Hopefully, its a big pharma name, with very small odds of going bust ![]()

Given the quantum of revenue from this single large customer, its very difficult to see this being diversified in the next 2 years. But I do hope that they have plans to address this in next couple of years beyond that.

However, having said that, at the same time, a huge comforting factor is that CDMO is a very sticky business, where the customer once he has established the relationship and comfort with you, will keep giving you long term business, as long as you are able to deliver on quality and time. The stickiness is not only due to business relationship alone, but is also largely due to the technical reasons / capabilities that the CDMO partner has developed relating to the particular molecule, during its discovery phase.

And being one of the 2 or 3 trusted suppliers to their customers for a given molecule, effectively there is no cut-throat competition as well, so it does not put pressure on margins too.

Purely in terms of customer names, I have rarely seen Suven documents displaying any names, most probably due to strict confidentiality clauses around the development process. So, as a shareholder, it does make me uneasy not knowing the identity of largest customer, but I would respect that. There was one slide though, which I have from a document of 2018, with some names on it.

This is from the pre-demerger days, but its very likely that the entity contributing 37% of revenue figures on this slide.

For those who may not like it, apologies upfront for a long and technical jargon intensive post.

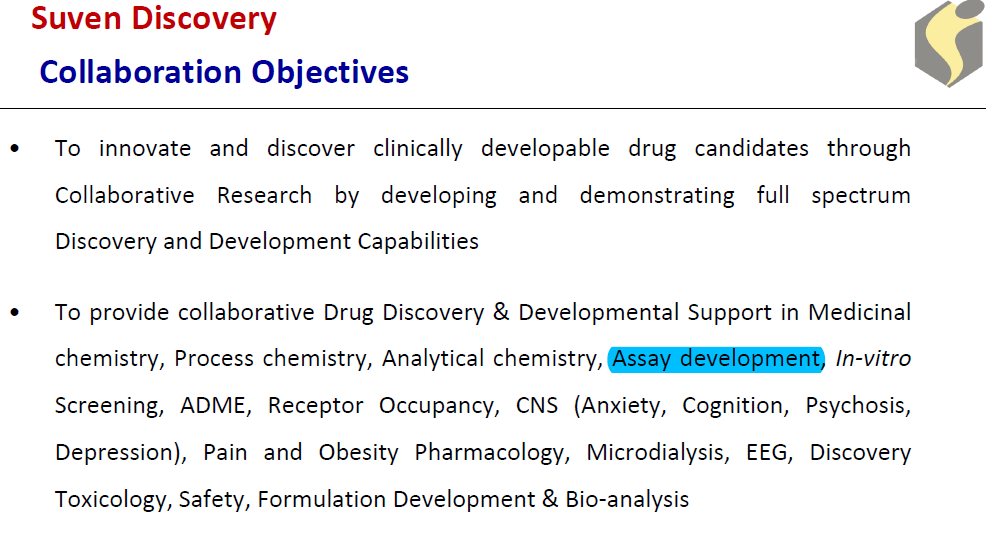

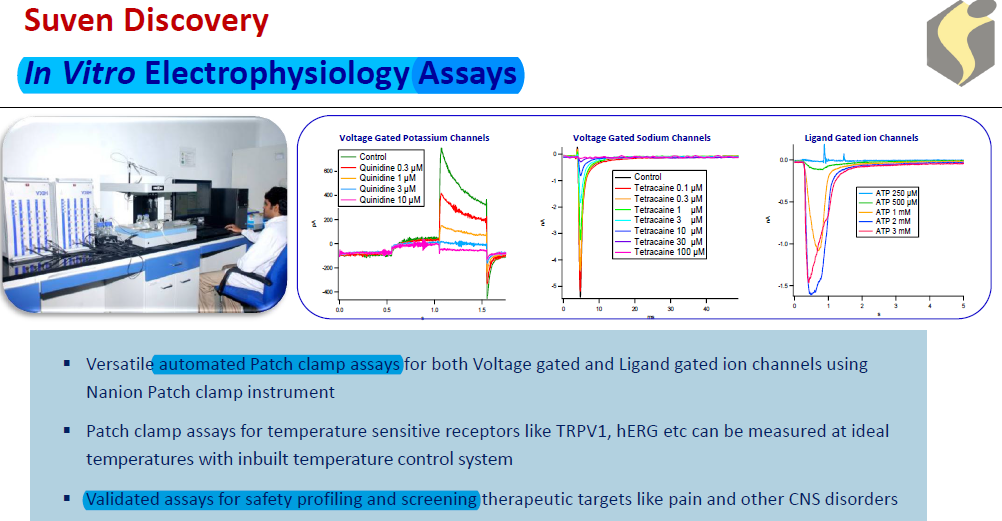

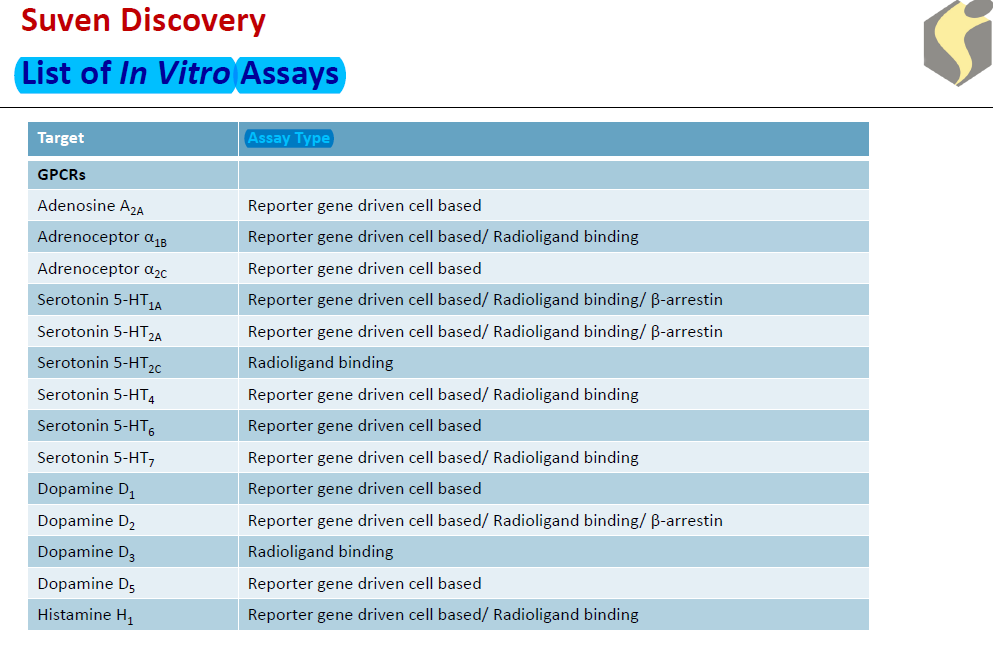

Thought it would be a long haul before we get to decode the profitability puzzle in Suven, glad to see some starting point after a burst of effort today. It seems to be the strength of Suven expertise on drug-discovery side of things, the CRO, which is certainly giving them that edge in value add. Digging deeper into Suven’s core activities, looks like they have developed in-depth expertise in services which are very specific to the drug development phase. Most of the terminology sounds alien, but they have stated following capabilities

Here is a short glimpse of what some of this means in layman terms

“Assays are investigative procedures that qualitatively assess a compound or examine a compound’s effects on identified molecular, cellular, or biochemical targets. The first steps in drug development are the identification and validation of potential drug targets involved in human disease. These targets are typically either a cellular structure or specific protein. Targets include:

- Receptors

- Enzymes

- Hormones and factors

- Nuclear receptors

- DNA

- Ion channels

In the following stage of drug development, biological assays and compound screening assays are created. These assays are used to identify compounds that have a desired activity at the drug target. These compounds are referred to as “hit” molecules. During the initial phase of hit compound identification, termed high throughput screening (HTS), a compound library that contains many potential hit molecules is tested to identify any compounds with the desired activity towards the target. Further assays are required to retest the hit molecule’s activity at the target. Finally, cell-based assays are used to examine a drug’s toxicity, safety profile, and efficacy. Every drug that is developed undergoes a unique series of assays that are specifically designed and organized for the drug target and compound in question. This process is termed assay development.

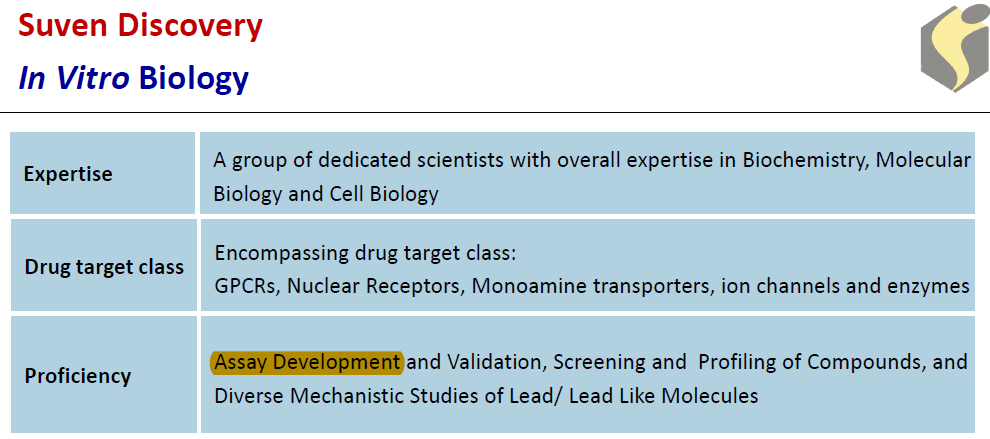

Now, let’s look at what Suven offers under “Assay Development”.

There have over 70 such in-vitro assays available with Suven.

Its lot of technical data, a lot of which was totally alien to me till today, but after reading a lot on the subject, it seems that these assays are processes to study and understand the impact of the drug molecule on the target cells / receptors (request boarders with domain knowledge to validate this, and kindly correct if any of this is wrong). To me this process then seems super critical in the development phase of the molecule. Suven clearly has deep expertise on this.

And please remember, that this is JUST 1 of the several dozens of other such critical processes that Suven seems to be offering.

So, just how critical is this kind of capability? Here’s another excerpt from an independent site

“Important factors in assay development

Developing top-notch assays is pivotal to drug discovery and development. The better the developed assays, the fewer potential problems in subsequent stages of the research and development process. Proper assay development requires carefully considering multiple factors, including relevance, reproducibility, quality, interference and cost.”

Just to triangulate the data, I also checked with independent sources whether Suven offers some of these stated services.

Now, I realise that a lot of these services would have moved to Suven Life after the demerger. But as Mr Jasti mentioned in last 2 con calls, both the firms will continue doing work for each other, on pre-agreed terms, so Suven Pharma would certainly have continued easy access to such high-quality capabilities in future, and that will continue to greatly differentiate its offerings from other CDMOs, and would allow Suven Pharma CRAMs operations to continue enjoying high margins and profitability.

Finally, just rounding off the discussion with some data on Neuland. Though I track Neuland in some detail, its not at the same depth as I track Suven. Also, I have looked at PI, Syngene and Divis very, very superficially. Whatever little I have read on Neuland, it seems more focussed on API in CRAMs. While they do work on early stage development molecules, it appears that they offer a more limited set of capabilities. Here is a snapshot of their offerings, taken from the same 3rd party website

As we can see from this, Neuland’s skills are more focused on Chemistry / Synthesis / Process research/ Manufacturing side of the development cycle, whereas with Suven, they are not only experts in these areas, they also have developed deep expertise on the drug discovery / biology / clinical trial phase of development cycle. And their expertise in both areas, is what allows them to command such premium with customers.

Don’t know their largest customer name but what I know is that it is a chemicals company and not a pharma customer.

I recently presented in our VP Carolina meet, on Suven Pharma. attached is the presentation. Suven_VPCarolina_meet_Sept2020.pdf (1.9 MB)

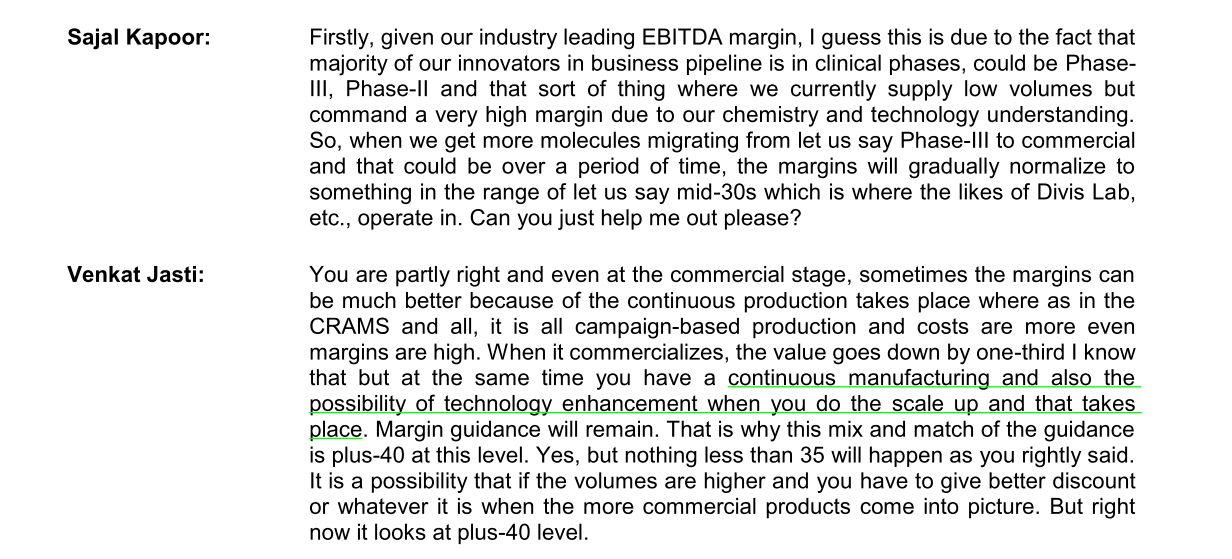

The reason for high margin was mentioned in Q4FY20 Conference Call as pointed out by @SwarnashishC on Twitter.

Thanks, just to add some context, I’d asked @SwarnashishC this question on twitter (His tweet was in response to my question). Forgot to add this info on the thread. Thanks for adding it, Sujay.

It looks like the margins have peaked out and it would be reasonable to expect them to come down a bit as more molecules move from clinical phases to commercial phases. However, the revenue stream would become more stickier so the expected variation in revenues would come down. It would be interesting to see where the margins settle at in a steady state scenario where a larger proportion of revenue comes from commercial side. My guess is it would be similar to Divi’s.

Sorry for a long post and excuse me if it’s repetitive at points:

Suven, as you guys will note, until today they are specialized in making Intermediates for Base commercial CRAMS, and specialty chemicals. Only recently they are getting into formulations.

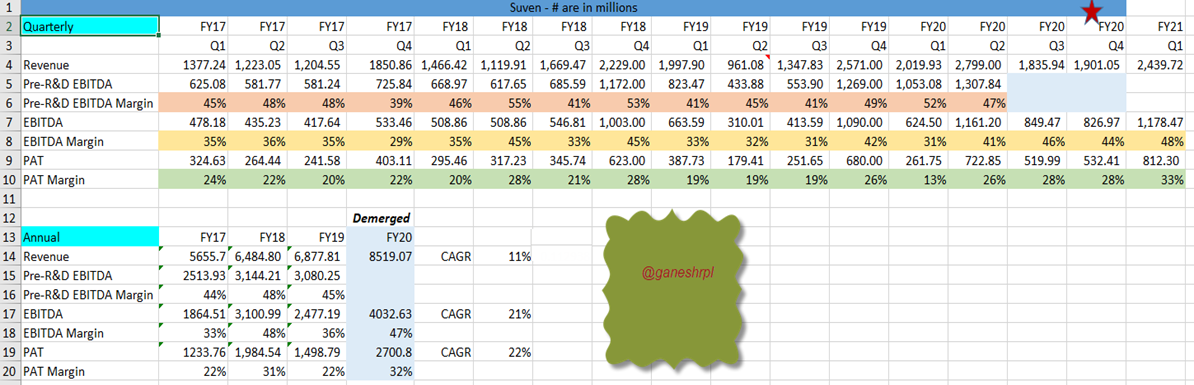

Consider the snapshot of their margins, which have been consistently above 40%+ as the mgmt has always talked about. Reproduced for quick reference here (from the data I collected for the presentation in our VP meet)These are the margins for the last 21+ quarters, manually compiled from their quarterly presentations.

To @bhambani’s point although they produce for 4 different therapeutic areas they are therapeutic agnostic. They specialize in CNS space (among the handful few in India) but they cater to other areas too.

Their margins in my opinion can be due to the area of CDMO which they cater too, which is in the NCE space, where the volumes can range from very small ( on the lower end of the clinical phase) to large (if they go commercial). I believe the mgmt. agrees to contracts/deals/partnership provided they are able to meet an internal benchmark, of say, a minimum of 40+ margins. (Mgmt. Strategy, which is margin accretive)

Layer on top of this if you consider that since they do batch productions and not continuous productions like how the other players in the industry might manufacture, say, for supporting day in and day out-manufacturing of a particular API/formulation. Even for commercial if you see mgmt commentary on this topic, a client might ask for a molecule say for the Diabetes molecule, Suven manufactures them probably in 3 months and then the client does not come back for more until anywhere between 12-18months depending on the velocity of sale of the end product. so they already have the infrastructure ready, knowledge (chemistry skills) handy and the scientist and the talent too … so they can leverage this and thus add a lot to the EBITDA and PAT levels incrementally.

But we do have to take a look at this in a broader sense - as they might be a quarter here or there and can be lumpy based on the product mix… in one quarter they might have base and specchem to manufacture and in other specchem and commercial, etc…For eg., if I remember correctly if you look at the above image in Q2FY19, the revenues where low- in Q1 they had all the raw materials and thus they could just build and ship the product well before in the previous quarter-ended (Q1FY19) and thus Q2FY19 might have optically looked bad… so if we zoom out and see the yearly progression, they have consistently clocked 45%~ EBITDA margins ( note- Pre R&D EBITDA is to be used for monitoring margins in the CDMO biz before Demerger, as they used to expense all the R&D effort for the new molecule discovery like 502, 3010 etc, whereas after demerger, we can directly look at EBITDA for monitoring margins as the R&D is baked into the cost of doing operations )

also to @bhambani’s additional point - its not a standard plant/system with incremental volumes in which they can do cost optimization to increase the EBITDA margins incrementally.

Another noteworthy strategy in this space is, they build infra either based on industry trends (like the OEL Level 4 they have been building in Pashamylaram plant) (or) customer-specific requirements. only if they have the infra, they can go ask for better projects. Imagine if they have a scenario where they want a project but it needs OEL - so starting to build after the requirement comes in, getting it approved by the regulators, and then starting to work in that plant - is lost opportunity cost… but by building it ahead of time and being ready to bid/ask for projects - is an additional advantage where they can demand better margins. (they have the luxury of cash to invest in these type of CAPEX & being prepared)

These are a few points that come to my mind about why they continue to command premium margins.

Media reports surface saying promoters planning to sell stake.

Venkat Jalsi is obsessed with the Life Sciences business. Connecting the dots backwards, the demerger and then sale of the CRAMS business seems to have been his plan all along to fund the research business

I don’t trust speculative reporting of CNBC. They has been doing same thing to Granules from last many months but there is no such development so far. If Suven management need funds they could get lot of money from their US associate and distribute proceeds as dividend or buyback. But they are partnering with the associate for formulations which is the long term vision of the company. Why would they enter into formulation if selling the business is their motive.

Disclosure: Holding since long.

I guess its too early to say if this is true or not. But I just hope is this not correct. Mr Jasti has such passion for his businesses (both Life Sciences and Pharma), and it would be very surprising if he was to sell out at this stage.

However, If the report is correct, then it raises very interesting questions. Mr Jasti is already about 70 years, is the decision age / retirement related? (personally, I doubt that).

The other possibility (as mentioned in the article) is that the promoters plan to use that money to fund the Life Sciences business, which is fast running out of cash. With failure of SUVN-502, monetisation is definitely delayed, and they will need funding beyond the 12 months of funds that they currently have. SUVN-G3031 is still under trials and with Covid, the schedule is likely pushed further out. The options before them were to either bring in a a strategic investor to fund the continuing R&D or to take Suven Neurosciences to IPO in US. Or now, they are possibly exploring a third option - investing their own funds through a stake sale in Suven Pharma.

It goes against conventional wisdom, to sell stake in a company which is a proven cash-cow, growing at a good pace, has established enviable reputation in its field of work and enjoys best-in-industry margins. On the other hand, its a well-known fact that Life Sciences business is a zero or hero business, and the odds of failure are very high.

So, despite all this, if this plan is real, that only means one thing - Mr Jasti has unshakeable faith in his molecule pipeline in Life Science business. Stretching the logic, do they already think they have a winner on their hands? If they have, the pay-off in that case will be quite huge. Or is it just the passion for drug discovery that is driving Mr Jasti’s decision once again? Time will tell.

I must add, that all this is just pure speculation till the time it is confirmed or denied by the management. I just hope that this is not true, and the management continues to run both the businesses.

True, but we have a precedent from software. A few years ago, Arun Jain of Polaris demerged Products business of Polaris (lumpy, unpredictable, high risk – high return) and then sold off the Services business (repetitive, predictable, cash cow), staying with Products (now called Intellect Design Arena). So, one never knows.

Since Suven management has not denied the reports, it is possible there is some truth in it. In a similar case a day earlier, media reported Tata Group was in talks to buy stake in Indiamart. But Indiamart was quick to come out with a detailed rebuttal. Mr. Jasti has chosen to remain silent.

That is the nature of such endeavours.In the same vein,if companies are not ready to throw crores and crores of cash flows,we will never have a cure for AIDS,neither a cure for cancer and so on.So I don’t think it shows “unshakable faith”.In fact,faith has very little role to play here.You need chemistry skills,some luck and a large dataset to prove that your molecule works.If it works,then sky is the limit.If it doesn’t then too bad but someone needs to try! This theory of selling out the cash cow to fund the ambitious drug discovery unit sounds like a good one.However,there is a lot we don’t know.For me these three things will be of utmost importance:

→ Price/valuation at which the deal is finalized.

→ In what capacity will Mr. Jasti continue or will he completely leave the company

→ Who buys the company and what plans they have.CDMO/CRAMS is a business where trust is of utmost importance.

Given that all this is still speculation,I don’t think there is much to offset the long term trajectory of Suven’s business.While I would love Mr. Jasti to be the captain of the ship,the business is very high quality and should continue to do well,except for a short term disruption.

Disc.: Invested. Views are very biased.

fade3893-8256-4e47-bdb4-ec6217b01acb.pdf (2.7 MB)

Today q2 result is announced earnings are down

Suven Pharma Concall Updates Q2FY21

I attended it live, there could be a mistake or two

Comparison of our business should be done yearly and not quarterly as we have said before (Due to lumpiness)

Growth guidance of 15-20% remains intact, expecting H2FY21 to be much stronger.

Product mix has also led to a decline in margins also environment-related costs have gone up.

Categorically denied the rumours of selling the business, stated that such news was there 9 months ago and 1 year ago as well. No plans to sell.

All About additional capex of 600 crores

New money is not being used for R&D anymore, some of our blocks are more than 30 years old, spending money for Tech Upgradation,and replacing old blocks (Building by building).

Process hasn’t been finalized, will update in coming months. Entire activity will be completed in next 36 months. Capex also is being done for qualitative purpose to upgrade ourselves as we see next 5 years to be positive.

To survive in this business you have to upgrade. 20-25% of the capex would be for additional capacity.

On capex of 320 crores, expecting fully utilization and impact to be seen in next 24 months (Hopefully).

On Pharma(Project) Pipeline

1 product is in phase 3 and 1 more has moved into phase 3, for which we will be supplying in next 6 months.

This quarter Formulation sales were at 10.18 crores, out of which 2 crores was royalty. 11 fillings have been done, out of which 5 are approved. 3 are commercial and expecting to launch 2 more before the end of this year.

Suven is also entering the contract manufacturing of API’s and Formulations for CDMO customers (Generic Api and Generic Formulation). Participating in life cycle management of its customers products. This will be a new line of the business.

Profit share from Rising will accrue, when Rising pays a dividend. First 6 months they reported PAT of 19 crores, and in last year in H1 they reported a PAT of 20 crores and 48 crores for full year.

On Spechem: we will be launching 1 product this year and another one in next year.

Dislosure and my views: Capex of 600 crores, 2 ways to look at this. First way, is that this is actually required to upgrade itself technologically or capability wise in order to get new customers, and some of it should be looked as replacement/maintainence capex since some blocks are 30 years old.

The second way, it can be negative for the shareholders in the near term, as this CAPEX could be unsubstantiated and the cash flows which were to come to the shareholders would get delayed. Could also be a red flag as CWIP/Gross block would remain elevated just after the completion of 320 crores of CAPEX.

Let’s see what view the market takes. Invested and this is not a recommendation to buy or sell.

Business is 30 years old and Mr. Jasti is preparing the company for the next 30 years. A very satisfying concall, I would say.

What is current P/E of suven pharma

1…On screener,consolidated pe@26

Standlone pe @31

2…On trendlyne,both pe are same@15.9 with mcap 3997 instead of 7996cr

3 …moneycontrol is not showing pe of suven

Thanks for adding your notes, worldlywiseinvestors. As always, very useful. If I understand correctly, going over your notes as well as the concall: TIKR Terminal, this seems like a specially capital intensive business. The ROIC, on screener of 51% while being accurate looking backwards, is probably not the sustainable ROIC in a steady state, due to the need to large frequent Tech upgradation CapExs. It would be really great if we could pick the management’s brains about what the average life of these plants and equipments are. They say some of these are 30 year old plants, why didn’t they do any capex in the last 30 years, then ? Did the business dynamics change in the last 1-2 years which forces them to do 300cr capex in last 1-2 years and 600cr capex in next 2-3 years ? In fact one of the analysts asked him a similar question on the useful life of the equipment, he told about the building (20-30 yrs), which is more obvious and makes sense, but not the equipments and machines which are the more frequently occuring expense, most likely.

Would like to hear your (and anyone else’s thoughts).

My thoughts on the capex are that if it is going to be a regularly occuring capex, then one has to evaluate the business with that factor in mind. If it’s a one-off kind of a capex, then it might provide us a good buying opportunity into an excellent business.

Disc: have a small tracking position in the business right now, trying to understand it better.

Would consider this to be a one off capex, rather than recurring. Important to distinguish between the 320 crore capex and this one. 320 crore capex could be classified as growth capex, whereas this one could be to maintain the overall competitiveness of the business or in terms of technological upgradation.

Listneing between the lines in concall:

Renenwed focus on Crams business as increasingly cash flow will be allocated in this segment, no burden of R&D in Suven Life.

Qip might be done to invest in capex and moreover another interesting thing was the confidence that was indicated in terms of projects moving to Phase 3 and I think another project is going to be commercialized next year.

Remain invetsed and managing risk through allocation, asset turns are usually 1x in pharma Cdmo and close to 2-2.5x in agchem Cdmo. On the other lines, not expecting Roic to sustain at 40-50% levels, as they are also getting into contract manufacturing of generic APIs and formulations. A ballpark figure of 25-30% Roic would also end up creating value for the stakeholders