Product concentration risk and client concentration risk a part and parcel of Cdmo/crams. Syngene too used to get 70% of their revenues from top 10 customers a few years back. Divis too gets 50% revenue from top 5 products, as Suven scales or the pipeline progresses which no one knows when. Expect this aspect to improve, but cannot be sure of it. As lumpiness and concentration is built in to the business model

4 Likes

Agreed, which is why I think the valuations will catch up with Syngene and Divis only there is clarity on the progress of the pipeline. But then the risk reward seems reasonably favourable and so I have initiated a tracking position.

In this thread we are talking about Suven Life or Suven Pharma?

Sorry it was not my intent to offend. I was getting confused hence I asked. Anyway please forgive me.

just check the recent management interview, another molecule might commercialize in FY22. They might have some clarity, capex in OEL facility also gives some indications

1 Like

In markets one has to understand that secularity of growth always results for higher P/E compared to lumpy growth.

If one looks at players like Divis, Syngene and PI, all these companies have achieved a good scale and all have some sort of secularity. Divis has generic API business, Syngene has CRO business and PI has long term contracts.

A good example is Aarti Industries, even though it is a chemical company, but due to the fact that it has long term contracts of 5-7 years, the growth has been secular compare to other chemical companies and the long term price action reflects the same here.

In case of SUVEN and other smaller players, as these guys show some form of secularity, even they will get higher multiples. In case of SUVEN, the new segment of ANDA can offer much needed secularity in the long run. Management has already guided that ANDA’s will be 1/3rd of the business in next 2 years.

13 Likes

Suven Pharma Board meeting and Bonus issue consideration on August 17th

1 Like

How is issuing bonus shares use of cash? which accounting book has taught this?

6 Likes

Coming to the other part of the question about opportunities, they have nearly doubled the gross block. And Capex benefits to be seen from FY22 onwards  (bonus question already answered by @vivekbothra)

(bonus question already answered by @vivekbothra)

Disclaimer: invested and biased.

2 Likes

I have lost track here but is this thread for Suven pharma or Suven life or both?

Considering these are two very different businesses I think it’s best to have a disclaimer on top and we can start a new thread on Suven life sciences

Suven Pharma reports flat Q1 results. Profit almost flat while revenue sees a rise of nearly 21% on a yearly basis. Board approves issue of 1:1 Bonus.

1 Like

1 Like

1 Like

Q1FY21 is comparable to Q1FY20. What management said was that FY19 had only 6 months of business activities in PnL, so FY20 is not comparable with FY19.

1 Like

Thanks for clearing that. Deleting my post to avoid spreading wrong info above

Edit: won’t waste this post. Did anyone attend the concall? Looking for the transcript but can’t find it. I believe it’s already completed?

Bottom line guidance of 20+ this FY.

Top line 10-15% this FY

May see better traction from Q3 for new projects as currently it’s lean period for Innovators and they focusing on OPEX

Disc : Invested

Details below

3 Likes

A few comments and observations from the FY2020 Annual Report, whatever struck me as noticeable, in no particular order:

(Note: Figures for FY19 in the P & L are for the period 6 November 2018 to 31 March 2019. Hence figures for Cash Flow Statement and P&L Account of FY2020 are not comparable to the previous year.)

- Gross Block at the beginning of the year was Rs.344 crore and addition during the year is Rs.109 crore, mainly Factory Buildings & Plant & Machinery. In addition, Capital WIP at the end of the year is Rs.102 crore. This is part of Rs.320 crore capex, of which Rs.210 crore has been spent and the rest will be spent this year.

Report says they are building facilities in anticipation of business; they do not have the customers yet for them. The facility will commence operation this year.

-

Intangible Assets are negligible, less than Rs.4 crore.

-

Rs.307.39 crore has been invested in Rising Pharma Inc. giving Suven a 25% stake. Rising is a Development and Distribution company. This investment is made through WOS Suven Pharma Inc., USA. Suven got Rs.48.21 crore as share of Profit from Rising Pharma.

In the concall, the management has said that this investment should be seen purely as financial investment and not a group or subsidiary company.

-

A total of 11 ANDAs were filed in the year and 3 approvals received. Of the 11, 3 are their own, 6 are with their customer and 2 are New Animal Drug Applications with customers.

-

Supply of commercial volumes to 1 formulation was on at the start of the year. During the year, they have started 2 more and intend to start 1 more by the end of FY21. Thus, total formulations for which commercial supplies would be on by 31-Mar-2021 would be 4. In addition, they are aiming to commercialise 2-3 more products in FY22. The two molecules have a potential of Rs.50 crore revenue each. Company has profit sharing agreements with marketing partners and when the products are sold, they get a share of the profit.

Business from commercial supplies are uneven, since once an order is delivered, the next order will come only after 12-18 months. The existing batch needs to be distributed and sold to the end consumers first.

-

There is no API manufacture today but the report says they can manufacture if the customers want them to do.

-

Net Debt has increased over the year. Rs.133.25 crore is owed to Suven Life Sciences @ 8 % interest.

-

There is an “Advance for CSR Expenses” current asset for Rs.2.10 crore. Not seen any such item before anywhere else before.

-

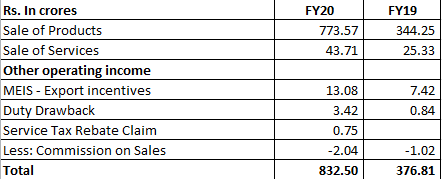

Revenue break-up is as follows, but as explained earlier, the previous year’s figures are for part of the year; hence the numbers are not comparable:

-

Rs.2.74 crore was paid as interest on income tax. It looks like there was a delay in payment of income tax.

-

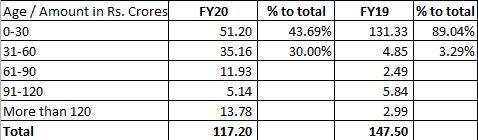

Aging of Receivables is given in the Balance Sheet

Though overall debtors have come down, the quality has deteriorated. Not sure if this is a temporary phenomenon due to Covid related issues or something else. Elsewhere, the report says Debtors Turnover Ratio improved “due to changes in the contracts with the customers”.

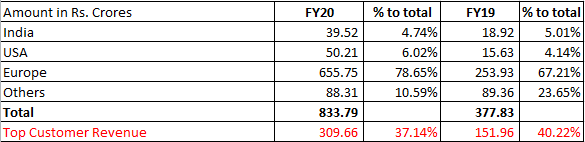

- Geographical break up of revenues is as follows: (Once again, note that the YoY figures are not comparable)

Europe is the primary contributor contributing 79 % of the revenues to the P&L, and not U.S. There is significant customer concentration risk to the revenues with nearly 40% coming from a single customer. I think this constitutes a big risk. (Any idea who this customer is?)

-

A new Contingent Liability of Rs.6.07 crore has cropped up under the head “Restoration Fee and Delay Condonation Fee” for APIIC-JN Pharmacity, Parawada. Not clear what this is.

-

Business Segment wise break up of revenues is as follows:

Same caveat as before applies; previous year’s figures are not comparable YoY.

-

Remuneration of Mr. Jasti is Rs.6.08 crore which includes a profit linked commission of Rs.2.11 crore. Other Directors do not get commission but only fees. CFO gets Rs.34 lacs and CS gets Rs.25 lacs. Overall KMP remuneration is low and well within limits.

-

Total number of employees is 942 and average increase in salary for the year was 10%. There are ESOPs.

-

Total R & D expenditure was Rs.14.13 crore which is 2% of the turnover. Entire expenditure is Revenue expenditure and capital expenditure is nil.

-

One of the Independent Director Mr. DG Prasad is also an Independent Director in Natco Pharma, a company in the same industry (though not a direct competitor). Generally this is avoided.

Summary and Conclusion:

Overall, no major negatives found. The report strikes a fine balance between optimism and caution. Company says with the current business in hand, they will be able to deliver a 10-15% growth in topline and 20% growth in bottom line during the year. But there will be an issue in getting new projects, since not much is happening at the moment in the space (I think this is with reference to Covid disruption as the reason). One major risk factor is customer concentration.

(Disclosure: Invested)

23 Likes

This thread is very informative and I was able to understand a lot about Suven Pharma and how it evolved from the erstwhile Suven Life Sciences. Suven’s Gross and Operating Margins are through the roof, so I wanted to understand how it compares against competitors. Here is a comparison of Margins for Suven, Neuland (similar sized Pharma CRAMS player with much lower % of revenue coming from CRAMS), Divi’s (Largest Pharma CDMO), Syngene (Biosimilars CRAMS player), And PI Industries (Large Agro CRAMS). The comparison is as follows:

All numbers are for Q1-FY21.

| Attribute / Company | Suven Pharma | Neuland | Syngene | PI Industries | Divi’s |

|---|---|---|---|---|---|

| Revenue (cr) | 238 | 205 | 2011 | 3366 | 5394 |

| Cost of Goods Sold | 95 | 125 | 623 | 1895 | 2245 |

| Gross Margin % | 60.08403361 | 39.02439024 | 69.02038787 | 43.70172311 | 58.37968113 |

| Selling and Admin expenses | 17 | 35 | 600 | 373 | 631 |

| SAE % | 7.142857143 | 17.07317073 | 29.83590254 | 11.08140226 | 11.69818317 |

| Depreciation & Amortization | 7 | 9 | 219 | 136 | 186 |

| D&A % | 2.941176471 | 4.390243902 | 10.89010443 | 4.04040404 | 3.448275862 |

| Other Operating Expenses | 11 | 12 | 185 | 380 | 691 |

| OOE % | 4.621848739 | 5.853658537 | 9.199403282 | 11.28936423 | 12.81053022 |

| Operating Profit Margin % | 45.37815126 | 11.70731707 | 19.09497762 | 17.29055258 | 30.42269188 |

| Asset Turnover Ratio | 0.81 | 0.79 | 0.68 | 1.07 | 0.73 |

A few inferences for Suven vis-a-vis the competitors:

- Suven’s Gross Margins are one of the highest. The only company having higher gross margins is Syngene. I think of gross margins in some sense as the value addition by the Company. The fact that the company took RM worth cost of goods sold and converted it into something valuable worth revenue demonstrates the value added. Do we understand why Suven’s gross margins are so high? This is especially surprising because if i understand correctly, a large portion of their CRAMS comes from intermediates manufacturing. They do not even make APIs (or FDF) and yet are able to churn out these high gross margins.

- Not only are Suven’s Gross Margins high, their Operating Profit Margins are the highest among the peers. The effectively means that the expenditure they have incurred in adding all that value is the lowest. Look at their Selling and Administrative Expenses. They are 7% of revenue compared to Syngene at 29%. This is huge. How is Suven able to operate such high. value addition systems with such low expenditure towards Employee costs (I believe this is the largest part of SAE).

- Depreciation and Amortization charge to P&L and Other operating expenses are also the lowest among all competitors. This means that use up the lowest % of their fixed assets every year for making the sales that they do.

- Suven’s Asset Turnover Ratio is the highest among all pharma peers.

While I am looking to deep dive more into Suven, it would be great if anyone who already understands the company well could help me understand the answers to these things better.

Thanks,

Sahil

16 Likes

One thing you need to understand is that CRAMS and CDMO are very vaguely used terms. Specially, in current market wherein CRAMS/CDMO has become a fancy word.

Every company has different business models.

The reason for Suven having the highest margins is the fact that their entire CDMO operations is for NCEs and that too in the CNS space, which gives them better margin.

Syngene on the other hand is currently a 90% services business, they largely work on cost plus basis.

Divis and PI Industries have CDMO operations wherein they partner with an innovator post the clinical stages, they are basically commercial manufacturing partners and do not manufacture for the molecule’s development stages. They are the 2nd supplier and 1st supplier is the original CRAMS company like SUVEN. (Note: PI is primarily agro-chem so the discussion will apply loosely)

One needs to understand that as a molecule progresses the volumes increases but the margins reduces a little. Margins are highest during the clinical trials supplies.

Also keep in mind that a lot of companies will say they do CRAMS/CDMO, but they are basically into generic contract manufacturing, which is plain vanilla manufacturing and does not command very high margins.

So do not invest just on the CRAMS/CDMO name, see and understand what kind of business model are they following in the CRAMS/CDMO.

(Note: this is what my understanding has been based on reading about all these companies. Open to any contradicting thoughts.)

21 Likes

Thanks, completely agreed. It was not long ago that investors thought of CRAMS as being a worse business model:

I do realize that they are primarily into NCE and that boosts the gross margins. What perplexes me is how they manage to spend so little on Employees side (or any other costs). One would assume that the employee salaries would be somewhat proportional to the value-added by the company.

Thanks for the warning. That wasn’t the intention at all. The intention was always to better understand the business.

Thanks so much for adding your thoughts, appreciate it a lot. ![]()

2 Likes

The reason for Suven having the highest margins is the fact that their entire CDMO operations is for NCEs and that too in the CNS space, which gives them better margin.

This is partially correct. Its true that their CDMO operations are focused on NCE, it is NOT limited to CNS space. For example, all four of their commercial CRAMS molecules are in four different therapeutic areas Rheumatoid Arthritis, Diabetes, Depression and Women’s health. So they do work across therapies.

@sahil_vi you’ve brought out a fantastic perspective with this analysis, and it would be interesting to fit the pieces of this puzzle, if we can decipher it cleanly. As @ankush12495 said, I too think the high gross margins have got to do with the fact that Suven delivers a very unique flavor of CDMO on the NCE side, which I think is quiet rare so far, at least in India.

I think there are a mix of factors which contribute to their amazing margins. From whatever I have deciphered of the company’s area of work, sharing some pointers consisting part data points and part my perspective. Please note, this is at best a conjecture and not based on solid data points

-

In FY19, about 45% of their revenue came from what they call as Base CRAMS i.e. work of all molecules in the pre-clinical and clinical stages of development. That’s almost half of their FY19 revenue from NCE based molecules.

-

I am not an expert on pharma / CDMO, but having studies Suven closely for a few years now, they do take on lot of projects. In FY19, they had 116 projects, with 30 new projects acquired in that fiscal alone. So a lot of volume of work in done in NCE space. My guess is that, in these projects, they have to be doing a lot of work which is NOT just plain manufacturing, but there has to be lot of work that is expertise based. Work such as custom synthesis, process research etc. which I assume requires specific skills / knowledge / expertise to deliver. Such kind of work is not simply an outcome of a standard plant / machine / system, which could be replicated and delivered by just any other CDMO, Hence it commands higher margins, even compared to high-margin, high quality contract manufacturing in pharma. Its a bit like software products, everyone has same hardware, same programming languages, same tools etc, yet different software products using same tools have vastly different levels of complexity, and hence varying price / value attached to it. Kind of people based IP.

-

For decades now, Suven in its erstwhile form had also been pursuing its own drug discovery program. For this, they must have certainly developed capabilities on NCE research side. Post-demerger, while delivering their services in Suven Pharma CRAMs side, they must be in a good position to leverage this expertise to deliver superior value-add to the customer projects, hence that could also be contributing to superior margins. In other words, regular CDMO companies, without the similar knowledge / capabilities that Suven has on CRO side, may not be able to add as high a value, as Suven can. Hence it is able to command the margin premium higher than any of its peers.

Will continue to look for data / information to answer this more convincingly.

14 Likes