Folks,

This post is specifically about the emerged Life sciences arm of Suven. There is a separate forum for Suven Pharma which is CRAMS business that is not described here.

So here is my piece on what is possibly the only truly publically listed drug discovery company in India. The Indian Pharma market as you may know is generally considered to be composed of

- Branded generics - Some of the biggies do offer a branded version of the originator molecule that has lost patent

- Generics - This is common paracetamol kind of stuff where there are dime a dozen mnf

- Biologics/Biosimilars- Very similar to generics except that this is not a true copy of the originator. The Generics copy the chemical entity while Biosimilars make similar monoclonal antibodies or cells.

- API/ Formulation manufactures

Largely the pharma space is concentrated by companies in the Generic molecule space. Largely the money to be made in the Pharma world is the development of NME(New molecular entities) that get 20-year commercial patent protection leading to a monopoly (think Pfizer, Roche, Novartis, etc)

Stages of clinical trials

- Computer model

- Pre-clinical studies

- Phase-1: Safety, tolerability

- Phase-2: Safety, tolerability + efficacy

- Phase-3: All the rest but in a bigger trial population

Typically it takes 8-12 years to bring an NME to the market meaning that the product only has the remaining 12-8 years to make money before it loses exclusivity and generics come in. The same applies for Suven

Coming over to our company Suven Life sciences - This company was carved out of the recent demerger at Suven with a pinpoint focus on discovering and bringing to clinical trials innovative molecules in the Central nervous system (CNS) space such as Alzheimer’s, Cognitive disorders, Depression.

The Business model

Revenue: This is currently a cash-burning machine. The revenue model revolves around the successful development of the molecules across the stages of the clinical trials. As the company is quite a small size and can’t commercialize on its own they will make money from

- Out-licensing the molecule

- Partnering with the bigger company in Phase-3 and revenue share if successful

Risk- Clinical trials have two outcomes - If it is successful, you make a lot of money. If not, then all R&D costs are basically sunk costs and zero revenue

This is what happened to SUVN-502 which recently failed to meet end-outcome in Alzheimer’s in Phase-2 POC trial. But apparently they are now testing it in dementia

Other assets and stages of development

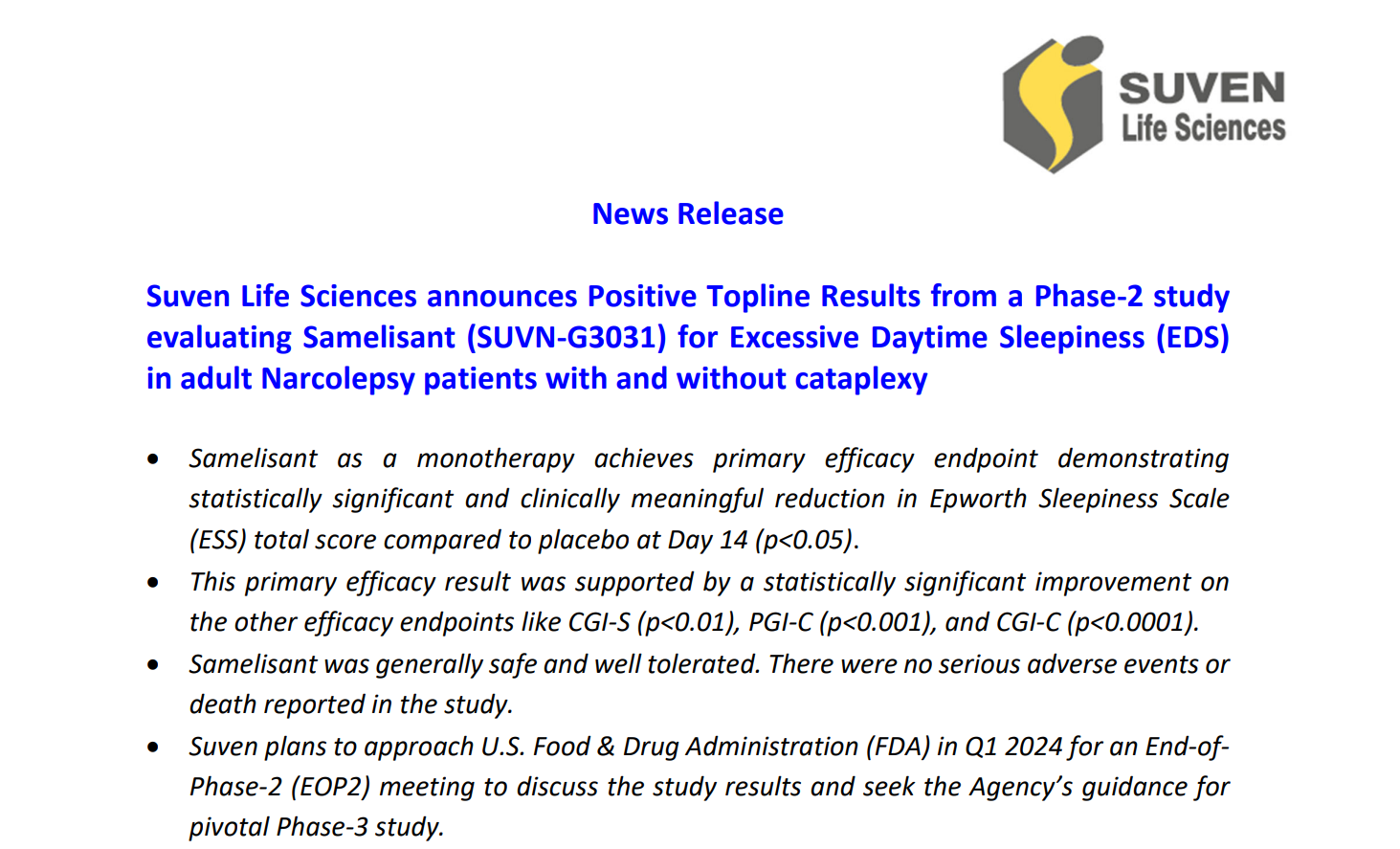

- SUVN-G3031: Narcolepsy, Phase 2 POC

- SUVN-911: Depressive disorders, Ready for Phase 2

- SUVN- D4010: Depression, Dementia, Planning for Phase 2

The success depends on how the company can get a product into Phase 3 and beyond because then it will get the attention of major players in the disease areas.

Current revenue sources

a) 136 crores loan from Suven Pharma- Enough to last them for the next 15 months

b) Contract technical services - minor

Costs - As I said, the costs of a drug discovery company are largely R&D numbers which are around 44 crores in FY20. As per the latest estimate, they are burning cash at the rate of 10-12 crores per month. A major point to note is that they get a tax deduction benefit, under Section 35(2AB) of Income-tax, of 150% of the R&D expenses. Therefore if they were able to successfully monetize the assets, they will get an additional benefit of a tax deduction on costs.

Risks or Unknowns

- COVID has delayed trials and this company cannot afford delays considering the tight budget they are on

- It’s a 0 or 1 company. If the assets fail to meet end-points in Clinical trials, it is game over for them.

- Currently, they can manage 12-15 months but they can’t produce a good result what happens then? They may possibly dilute equity further by raising more money either in the US or India.

- The main guy in this company is Dr. NVS Ramakrishna who heads drug discovery. He led Zydus previously and is an oncologist. I don’t have any further information but he is the guy to know about

Financials

- I am not going to talk about the P&L for two reasons

a) This got demerged from Suven and therefore nothing is comparable YoY

b) Its a cash-burning machine. They do not have sustainable revenue sources right now because its a drug discovery.

I advise against trying to value this a generic Indian Pharma company. The payoffs are not linear and either they can score a big win or go bankrupt.

Questions (Need to ask the management)

- How is management dividing the span of attention between Life sciences and Pharma business

- Impact of COVID in patient enrollment

- What is the validity of the current patents of molecules in Phase 2? Remember that they have a fixed 20 year period

- The consolidated R&D spend was 121 crores while standalone was 43 crore so I’m trying to figure out the numbers here

- About 100 crores worth of land given to Suven Pharma is in the name of Suven Life sciences. This can be a hidden asset

- Why is the board composition made up majorly of finance people and not scientists/drug discovery folks?

IMHO this is a pretty interesting company to track as it is the only one in its space. it has a niche but that comes with its own set of risks which includes bankruptcy.

Comments/suggestions/questions are welcome

Cheers

Uzi

Discl - Going to take a tracking position.