Suryoday small finance bank (SSFB) was incorporated in 2009 as a Micro finance organization and then got converted into Small finance bank (SFB) in 2017.

Business:

The small finance bank is in the business of banking as an SFB and the services they offer include loans for Affordable Housing, Commercial Vehicle, Microfinance Loan to Inclusive customers, and liability products.

Primary differences between SFBs when compared to scheduled commercial banks (SCB) are:

- SFBs should extend 75% of their loans to priority sector (Small borrowers, unorganised workers, MSMEs). Whereas for the SCBs, there is no such limit.

- SFBs have to open 25% of their branches in rural areas, in the initial 3 years. Whereas SCBs do not have to abide to this.

Understanding the Asset (loan) business of Suryoday:

Sarvoday has been classifying their Asset business in to these categories (Primarily):

- Inclusive finance (Microfinance lending)

- a. Joint liability Group loan (JLG): These are MFI loans extended to a group of 4 to 10 individuals (mostly to a group of women), without any collateral. The interest rates charged are higher, above 20%+. The higher interest rates are possible here because of the smaller tenure of the loan, which is less than a year in most cases.

- b. Vikas loans: These are unsecured loans extended to individuals who have matured from Joint liability Group category, and have good repayment record for more than one and a half years. Here, the cash flow of the family members is also evaluated. The ticket size is between 60000 Rs to 2 lakh Rs.

- Non-Inclusive finance (Retail lending)

- a. Commercial Vehicles: Bank provides loans for small and medium size commercial vehicles, new or used. On the back of small-ticket overdraft lending facilities, particularly to small and retail transporters, they hope to digitally onboard a potentially-sizeable customer base.

- The average ticket size of these commercial vehicle loans was 15.9 Lakhs, with an average tenor of 40 months. The average yield for FY22 was 12.7%.

- b. Affordable Housing Finance: The Bank offers housing loans to self-employed and salaried customers. Loans are provided for home building, home remodelling, home extension, and home buying.

- The average ticket size of loan was 12 Lakhs and the average term was of 198 months during FY22.

- c. Secured Business Loans: These loans are extended to Individuals with proper documents and a good credit history, and are provided on basis of their cash flow.

- Financial Intermediary Group: The Bank provides term loans to financial intermediaries i.e., NBFCs, MFIs and HFCs that further lend to retail customers in the form of housing finance, loans against property, supply chain finance, evolved. These loans are typically provided to entities that are predominately rated BBB (-) and above from a recognised credit rating agency.

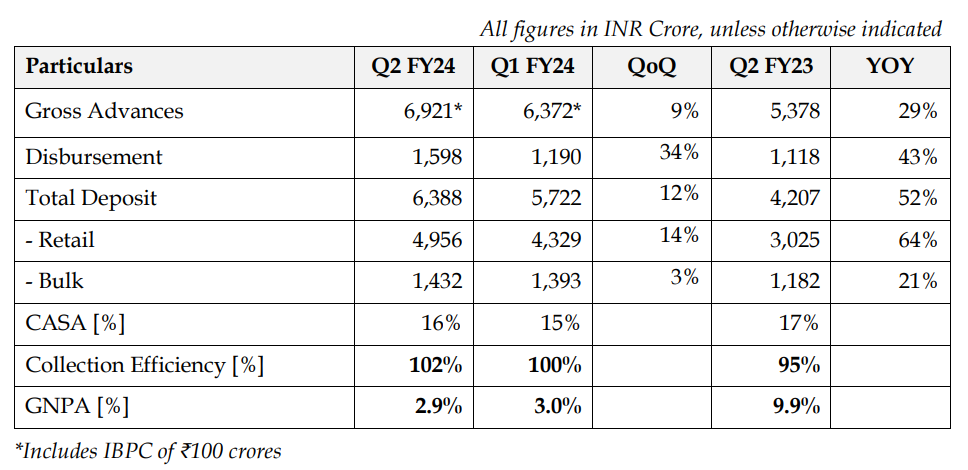

Asset breakdown as on Q4 FY 23 end:

Total Gross advances: 6114 crore Rs.

Inclusive finance 3734

Housing loan 642

Secured business loans 405

Commercial Vehicals 391

Financial Intermediary 688

Total 6114

Liability side:

Suroday does not have higher capex branches like other banks or SFBs. Their liability model is to have much smaller office space for their branches and lesser staff. Rather, their focus is on offering higher rates for deposits to customers to attract them. You may see that they offer a relatively higher rates for the fixed deposits.

They also offer deposit generation using digital mode, and higher deposit rates should do good on this front.

Guidance:

In FY24, Management is guiding for 30% advances growth, and NIM of 10%, GNPA / NNPA <0.5%, ROA of 2.2% and ROE of 15%

Where are they planning to increase their lending going forward:

SSFB has guided for 30% advances growth for FY24.

- Their retail book, which is secured would grow at faster rate of about 35% to 40%.

- Unsecured book will grow at about 30%. In the FY24 they would increase the Vikas loans at faster pace then the JLG.

-

Vikas loans are sort of insured products. Because they are insured under CGFMU (Credit Guarantee Fund for Micro Units). Under CGFMU, SSFB would be paying certain fixed percentage per loan, and in return up to 20% of credit losses would be covered by state govt agency and CGFMU fund. I do not have exact details of the coverage with me.

-

For FY24, overall outflow expected due to CGFMU fees is 1% of the insured book which will substantially reduce any abnormal event risk such as Covid for the insured portfolio.

NPA position: ( I am writing this based on my understanding of their concall transcript )

On the book of 6114 cr, they have GNPA of 191.4 cr (3.1%) and NNPA of 93 cr (1.5%). However, it is notable that the GNPA figure of 191.4 cr includes ECLGS loans of ₹63.6 Crores wherein ‘nil’ provision is to be made following IRAC guidelines and will be recovered through a Guarantee mechanism as per ECLGS circular.

If we exclude the ECLGS loans, then GNPA and NNPA will reduce to 2.09% and 0.49% respectively as on March 31st , 2023. So the actual Uncovered GNPA is ₹35.5 Crores however, as per the management, they are confident that the recovery during Q1 would negate the provision requirement of this 35.3 cr .

Please note that they would continue doing standard assets provision though, because they want to build a good 5% standard assets provisions in future years, so that it would help them in case of any unforeseen events like COVID or demonetization. and hence they are guiding for 2% provisions for FY24.

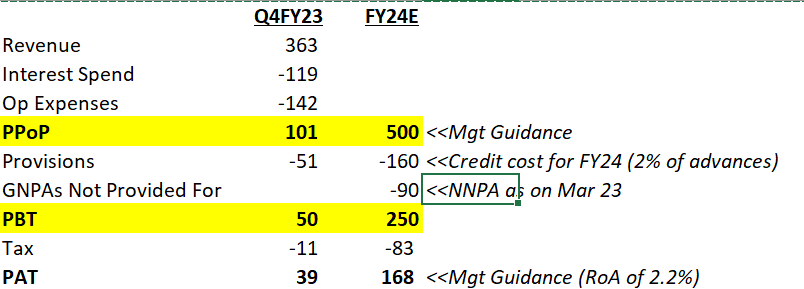

Profit estimate for FY24:

Note: this estimate is opinion only and I need fellow members from here to correct me if some figures I am taking may not be correct.

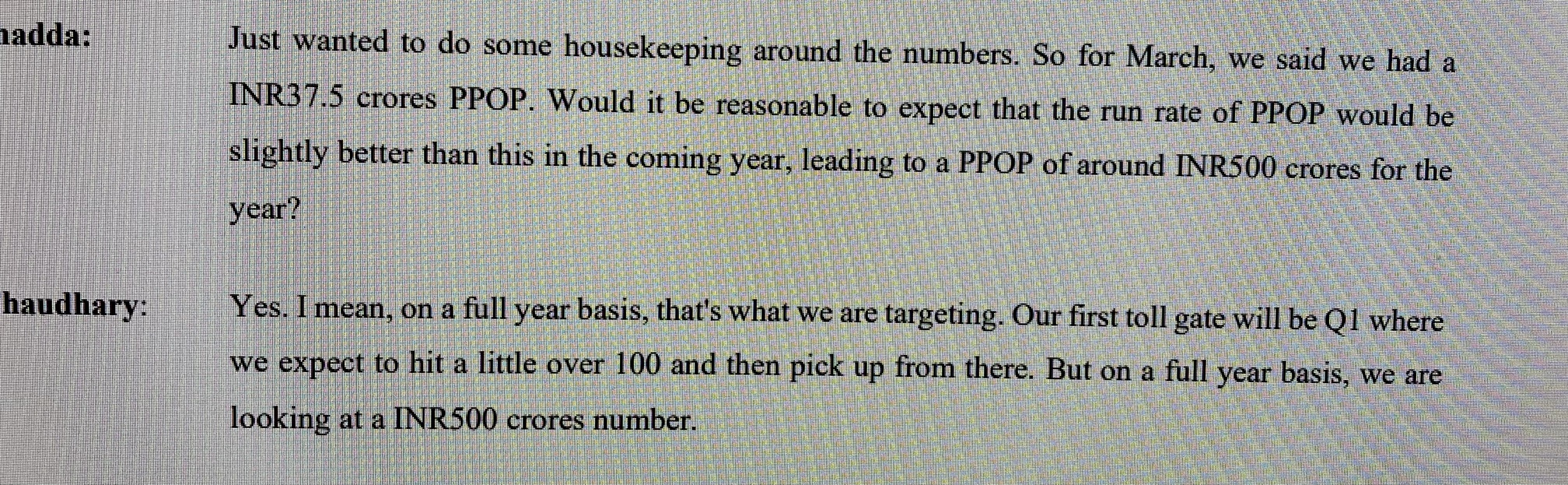

Management is guiding for 500 cr of pre-provision operating profit for FY24 end.

At 2% credit cost guidance for a book of say 8000 cr (average gross book for FY24, I assumed considering guidance of 30%) , the provision figure would be 160 crs. So 500 cr – 160 cr =340 cr of profit before tax.

At 25% rate of tax, then Net profit would be 340 * .75 = 255 cr.

At this net profit figure and given that market cap of Suryoday as on today is 1350 cr, its trading at FY24 forward PE of 1350/255 = 5.3 PE. (I want other members to opine if this calculation holds merit?)

Other SFBS are trading at higher PEs. Suryoday should not be compared on like to like basis with them because other SFBs may have larger secured book and they (some +MFIs) have proven faster recovery from COVID NPAs. However, for an SFB (Suryoday) which possibly could grow its profit at 30%+ (if management guidance turns out to be true), and available at below book value, with all NPAs out or provided for(as per management presentation of last quarter), markets should assign a higher PE . Let’s opine on this in the comments below.

High NPAs were generated due to covid lockdowns

I believe that COVID was a once in a 100 year kind of event for MFI and unsecured business category institutions. (Or am I wrong? Do comment)

a. During lockdowns, business activities were shut/disturbed for more than one year (COVID one and two).

b. And this applied to the whole country.

c. Government had extended moratorium too (this would incentivises a few, much weaker section of unsecured small borrowers to not pay, many would also confuse this with loan waiver, etc.)

d. Small borrowers like people falling in yellow collar and labour section had relocated back to their hometowns and villages, many of them never returned to the same place again. such events dis-incentivised them to payback.

So the level of NPAs seen by finance institutions due to covid were much higher than other events like flood, lockdown, elections etc…

Risks: Financial institutional can get more bad loan problems due to events like covid lockdowns, demonetisation, other economic shocks and company specific Defaults.

Disclosure: I am invested in Suryoday SFB from 100 Rs level and have a good portion of portfolio invested in it. I may have a biased view because I am invested in this company. Do verify personally about my opinions and figures mentioned above before counting on them.

Important Disclosure: I am not a registered sebi analyst. Nor do I have expertise in stock research. Do not consider this writeup as a stock recommendation. My aim in relation to writing this post is only to share my thought process regarding this company (and the stock) with the members in this forum and take their opinion about what do they think about this company through discussions in the comments below.