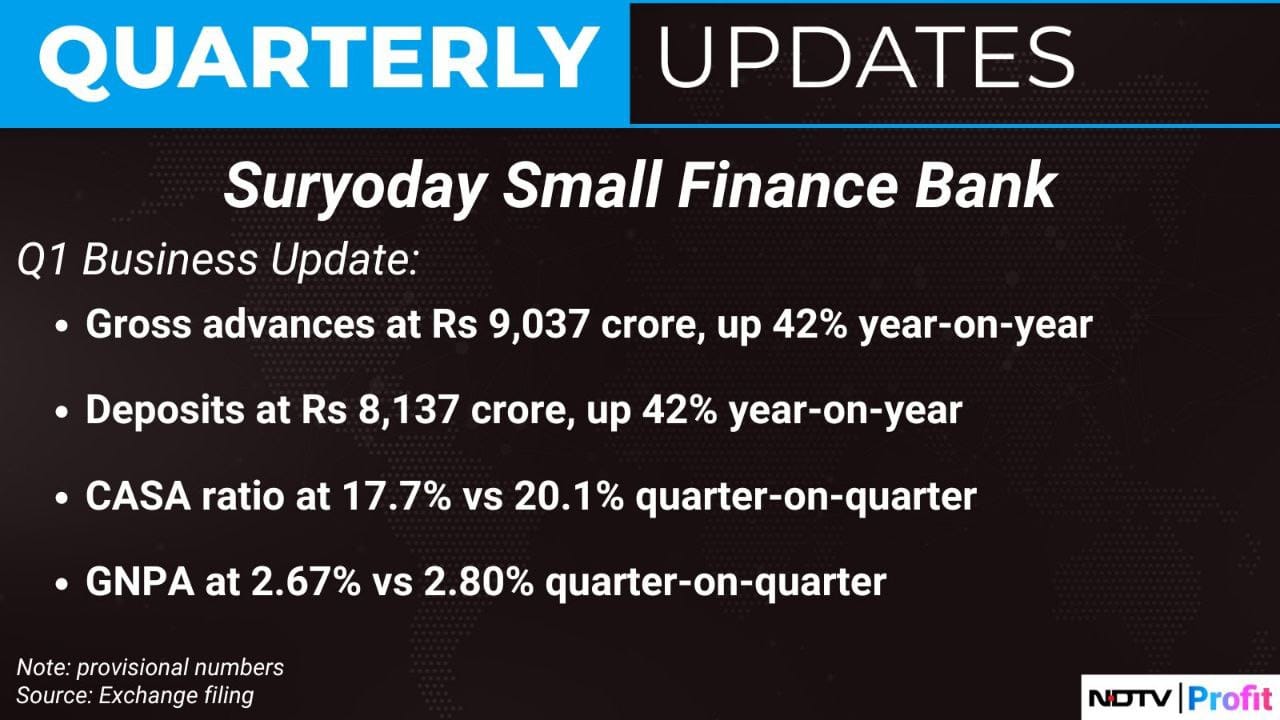

The bank has reported advances of Rs 8,650 crore for the quarter ended March FY24 (including inter bank participatory certificates (IBPC) of Rs 400 crore), growing 14 percent over the previous quarter and 41 percent over the year-ago period. Disbursements at Rs 2,340 crore increased by 31 percent QoQ and 39 percent YoY, while deposits grew by 20 percent QoQ and 50 percent YoY to Rs 7,775 crore for the quarter. The CASA ratio has improved by 1.6 percent QoQ and 3 percent YoY to 20.1 percent in Q4 FY24. The disbursements in FY24 of over Rs 6,900 crore increased by 36 percent compared to FY23 on continued momentum in Vikas Loan as well as retail assets disbursements.

1 Like

SURYODAY_09052024190035_SSFB_Intimation_in_relation_to_press_release_sd.pdf (452.1 KB)

Excellent results posted by SSFB for Q4

2 Likes

while Q4 result is excellent. Company seems to be firing with all cylinder, but Pledged percentage 22.4 % , DII reducing stake is concerning.

3 Likes

Ujjivan in its analyst day warned of sytem wise stress. Suryoday for long is guiding for 2% credit cost as new normal. Looks like next one year will be time correction for all MFI stocks till market adjust to their new credit cost. Their Yields already factor in high credit cost and Suryoday in particular has CGFMU cover too [credit insurance cover] so it should be well protected for credit cost beyond 3%. x.com

3 Likes

Ujjivan small finance bank reported 1.7% credit cost

Great growth YoY, however, disbursement is down 26% QoQ.

Any views why this could be the reason or should wait for management commentary?

First quarter is generally slow for financial institutions, that may be the reason.

1 Like

The RBI has superseded Aviom India Housing Finance’s Board due to governance issues and payment defaults, initiating bankruptcy proceedings. Shri Ram Kumar, ex-Chief General Manager of Punjab National Bank, has been appointed Administrator.

Aviom owes Suryoday Small Finance Bank Rs. 11.66 Crore

Worrying ?

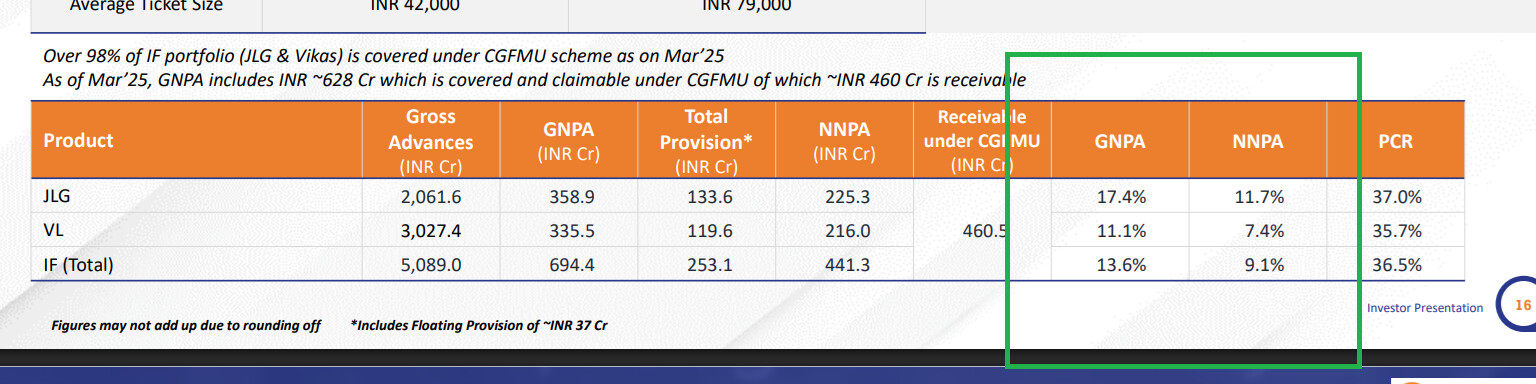

One of terrible asset quality reported compared to any listed company’s MFI book. But management is very much focus on growth and not at all concerned about their state of affairs

Most of the microfinance loan book is insured and net npa would be less than 1% after factoring it in.

They are the only sfb that I know of who had the foresight of buying insurance to manage black swan risks in the mfi portfolio.

3 Likes

Having insurance is a protection. Whether they have insurance or not does not take away the fact that you have to underwrite properly and make sure book has best asset quality. Off course this is sector level issue and not restricted to this bank, but why here the MFI slippage is more than 10% and look at the GNPA of the MFI segment. If you do comparative analysis you will find that this is one of the bad returns

This insurance covers only 72-73% of the NPA account, it does not cover interest segment and it does not settle claim immediately (I think only after a year bank can claim this amount) and until bank receive that money, bank is forgoing the interest income for that period also. Bank did a good thing on insurance part but failed miserably in maintaining the discipline when it comes to asset quality

11 Likes