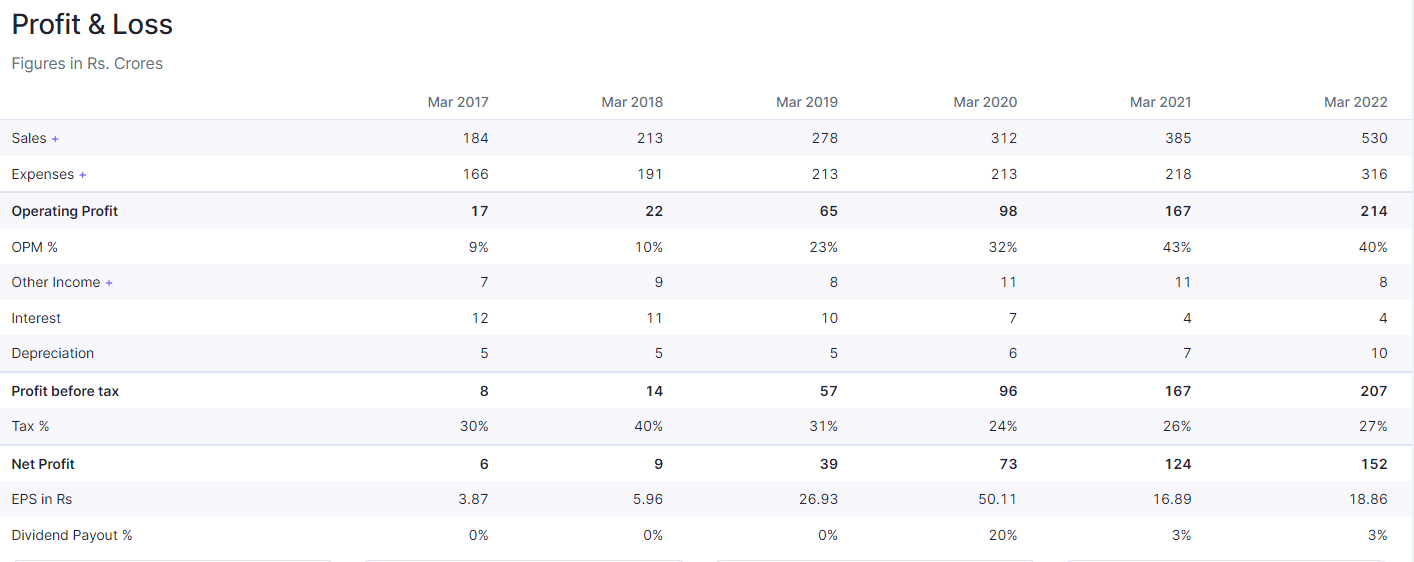

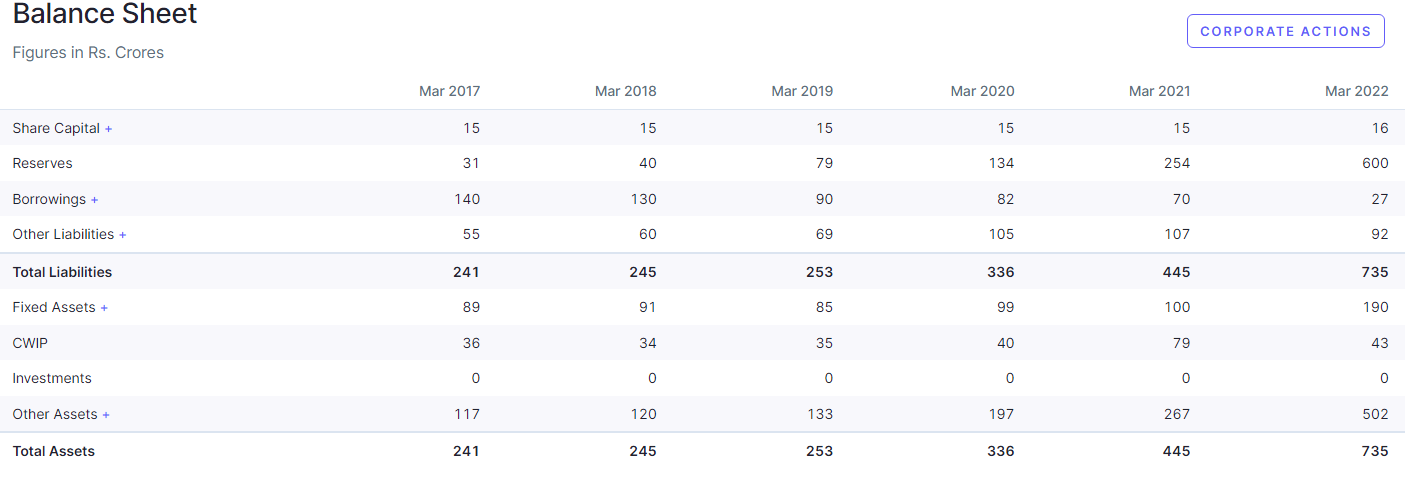

Above profit and loss statement show OPM margin jump from 10% (2018) to 23% (2019 and onwards), if we check balance sheet fixed asset, there is no increment during or one year before (capitalization amount) these periods. so chances of backward integration during this period is less.

Below is screen image is from annual report of 2018-19, shows same product (as shown in current year) as major export product.

May be this jump in margin is due to price fluctuation (could be temporarily), sustainability of margin is the question

There could be various reasons for margin improvement. To understand what they are, one will have to listen to the pre-IPO analyst concall, someone must have surely asked this question. Whatever their reply, a more practical reason is that in unlisted companies, managements have an incentive to understate profits (to save tax) and in listed companies, managements have an incentive to overstate them (to boost share price). You will find this pattern in dozens of companies – the performance dramatically improves in the IPO year or just before IPO compared to distant past. Pre-IPO Vs. Post-IPO is not a like to like comparison, I don’t try to dig too deep into it but look at them going ahead. But your point is logically valid.

Supriya’s business model is based on being the most cost-effective, quality producer of a few select non-commodity APIs, as opposed to diversification into many APIs. Cost-effectiveness comes from backward integration. The competitive advantage is reflected in its large market share in India among its top exports.

May be this jump in margin is due to price fluctuation (could be temporarily), sustainability of margin is the question

In the previous concalls, the management said that the jump in margin is due to increased contribution from the regulated markets, in which the company gets higher margin. Naturally, when there is higher margin, the product prices would be higher. That is, the product prices (of exports from India, in which Supriya has a large share) would have shown an increasing trend in the last few years. From whatever I have heard from the management, the margins are likely to sustain.

However, given the current valuation of the company, it seems that the market has decided that the margins and revenue are likely to reduce. Supriya’s strategy of concentrating on a few products provides it strong competitive advantage but the market does not seem to like the product concentration risk. This stock seems to be a rare case of a wide disparity between the management projection of the financials and the market’s belief.

Results look good on a YoY basis. QoQ is not to be seen given that the management has said in the past there is a seasonality in their business, with Q2 and Q4 having higher sales. Anyone knows what causes this seasonality?

Anti-histamines is the therapy which is a major contributor to their sales is what causes this seasonality! China is the key market for anti-histamines. Q2 and Q4 are strong qtrs for this therapy and Q1 and q3 are relatively weaker!

Also, good results YoY by the company with strong Gross margins of 65%. QoQ comparison would be wrong here.

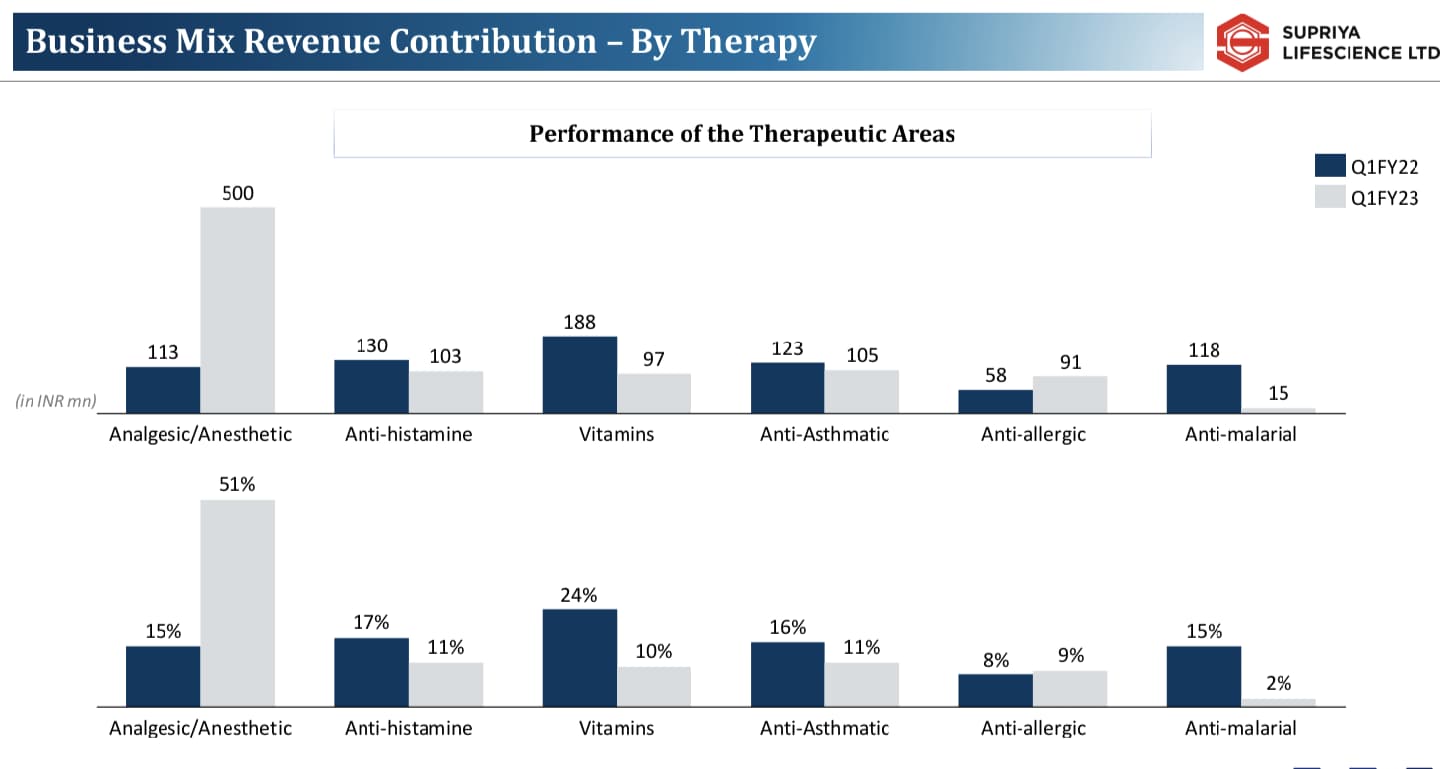

It is interesting to note only Analgesic/Anesthetic therapeutic have grown 5x YOY and other therapeutics have declined. Not sure if growth in Anesthetic will be sustainable and will other therapeutics recover in next quarter or not

Listening to this call, some quick questions/comments:-

The mgmt alludes to sustainability of current margins on progression of the api basket (larger portion) to regulated markets. There seems only 4 or 5 of the 38 catering to regulated markets

The mgmt refers to some portion of money raised for inorganic growth - seems a bit surprising

The contracts with Supriya are still quarterly (why no long term?) despite 30 yrs in the business. This might allow price revisions. Given the high inflationary trends across the world, downward revisions is possible. How is it for other API players?

Opportunity size is still not known. However, Supriya’s market share for top 3 APIs is known with Divis competing in one of them.

Any price comparisons with low cost API producers? Perhaps, China could be the lowest cost - seen this in agrochemical space

Pursuant to Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, this is to inform you that Dr. Shireesh Ambhaikar, Chief Executive Officer and a Key Managerial Personnel of the company, has resigned from the position due to his personal reasons and requested, inter alia, for acceptance of his resignation and relieving him by September 30, 2022 and which has been accepted by the Board in its meeting held today i.e. September 27, 2022.

However, Dr. Shireesh Ambhaikar has agreed to extend his services on a retainership basis for a period of 2 (two) years effective October 1, 2022 where he will be designated as Technical Head for certain projects of Supriya Lifescience Limited to ensure their timely execution, knowledge transfer and smooth transition to his successor, who will be joining the company on October 3, 2022.

The Board has in its meeting held today i.e. September 27, 2022 approved the appointment of Mr. Rajeev Kumar Jain as Chief Executive Officer and Key Managerial Personnel of the Company, who will be joining on October 3, 2022 to take Supriya on the next phase of its growth journey.

The Board would like to take this opportunity to express its gratitude to Dr. Shireesh Ambhaikar for his contribution to the Company during his tenure of office and look forward for his continued support and guidance in his new role.

What I fail to understand is that there are many API companies like Divis whose valuation are sky high but Supriya is getting hammered everyday. Is there any technical sector information which is discounting the share price? Any thoughts gentlemen?

Company is not giving consistent growth- management has highlighted that they will have Q2 and Q4 will be best quarters each year. As company has recently done the IPO and there is no visibility in the past quarterly results.

Also, the Operating margin fluctuates a lot each quarter depending on the product concentration for that quarter. This will also need to be seen in next few quarters.

I believe these are few concerns investors may be having.

Even though the seasonality involve in the business the yoy sales is growing and and the current Q1 & Q3 sales will be higher than previous Q1 & Q3 sales. I think the promotors are also strong. Still there must be some reasons not known to us.

Compared to same quarter in the last year for dec, march and june. they had a growth above 30% as management said in interview. when u compared results with previous quarter only u could see fluctuation in the earnings. I feel that comparison is not correct because as per management interview they said they are manufacturing various items on seasonal basis. will get exact picture post Q2 results.

Dis: Invested and will double the investments post Q2 results if results increase by 25%.

Invested at 285 range based on following conviction…

Last 3 quarters based on the available information company growth is above 25% including PAT.

Highly profitable business PAT is above 25%

3.Increased their market share in regulated market to 53% in 2022 from 34% in 2018. That is the another reason for increase in EBIT margin over the years.

Management expects that business and profit will increase CAGR of 25%.

Their total capex investments at the end of 2026 seems 450 crore( including current). Normally asset turnover of the company is 3 times. if that is the case expected turnover in 2026 will be 1350 and PAT margin of 25% will result Earnings of 330 Crore. Current Market cap is 2300. if the above expectations are met then P/E at current market value in 2026 will be 6 times. Normally pharma sector P/E is around 25 to 30 times. That gives enough margin of safety for me to hold this share for long period. But watching results and updates from company from quarter to quarter is very important.

Current P/E of Supriya is 13 and industry average 25… seems recent IPO hit at 270 range and share went to 600 and profit has booked by few so now trading at 280 range

Seems management is very honest and next generation is well knowledgeable and efficient.

What interested me more in their annual report they have provided 2 pages for employees comment. Never come across such pages in annual reports.

specially the following comment of an employee

" “Satishji invited employees with

their spouses – from the office

boy to the senior management at

the wedding of his daughters – at

Radisson’s in Alibaug and Leela in

Jaipur. All employees stayed at the

same hotel as the Waghs!”

and one more

“When the Managing Director heard

I had employed a baby-sitter, he

added the baby-sitter’s cost to my

salary, ensuring that my daughter

would be looked after while I

was at work. This company treats

employees as family!”

you could see many more in page 52 and 53 of AR 2022

They have obtained all most all the major certification from USFDA, EUGMP, EDQM, SFDA

NMPA, ANVISA, KFDA, PMDA, TGA, Taiwan

FDA, COFEPRIS, Health

Canada, CDSCO

For me it is a value buy for long term perspective when the market at 13 p/e and a growth buy when management is putting plan for 25% growth in sales and PAT for next 5 years. Very rare to see value and growth combination of a share when market is at all time high.

Understand the risk of high concentration on business in 3 to 4 products and few customers of supriya. However, reading their annual report, going for various management interviews, analysis report, company website, of course VP discussion given me a confidence to allocate 10% of my capital to Supriya lifescience and will watch their next few quarters to see whether management is capable to deliver the result then will double my investment if supriya available at this valuation.