Background

Sundaram Finance (SFL) belongs to the wellknown TVS Group. Incorporated in 1954 it is a leading player in retail finance with presence across multiple facets of the financials industry,including Vehicle Finance, Home Finance, Mutual Fund, General Insurance, and financial service distribution .The company operates through 586 branches . As of 31 March the total standalone assets undermanagement stood at approx 30,000 crs . It has investments in Royal Sundaram General Insurance, Sundaram Asset Management, Sundaram BNP Paribas Home Finance

The Company networth has grown at CAGR of 18% over the 5 year period… The last quarter results showed a increase of 10% over QonQ. This is after taking into account the effect of demonitisation. They had also not taken the benefit given by RBI for NPA Classification on account of demonization. Infact the management is very conservative they follow a provision policy of 3 months against RBI current guidelines for classifying NPA of 4 months . They are also very low keyed and you won’t find any significant management interviews.They have been concentrating in expanding the business.

Key Announcement

They have now announced a demerger of Non Financial investments that had in Sundaram Finance. They have shareholding in Wheels India, Axles India, IMPAL, Sundaram Clayton etc. The scheme envisages issuing shares to all SFL Shareholders on a ratio of 1:1 and provide an opportunity for all shareholders in value creation in this portfolio. The current market value of this investments is around Rs 3,000 Crs . The companys share of Net Profit from this investment was Rs 142 Crs Last year. Attached link to the PPT which give the demerger scheme announced by the Company. You can refer to the March 16 balancesheet which gives the shareholding of SFL in various automotive companies. The ppt also gives the details of investment holdings by SFL in various business

http://t.in.com/46tD

Basis for Investment

The Company belongs to a reputable TVS Group and Proven management. There has been no negative news about the company or the Group.

The current market price is Rs 1520. The current 9 mnths standalone EPS is Rs 32, so the annualized EPS works out to be Rs 44 approx Based on the CMP the PE works out to be 30 without considering this demerger been initiated by the Company. Radha Kishen Daman-Dmart owner- Damani Estates & Finance also holding 10.30 lacs shares in the Company(Refer annual Report March 16). This is a unique opportunity where we get to invest in both the NBFC(including Insurance, Mutual Fund AMC) and their cream automotive business as majority of the companies in which they have shareholding are leader in their segment. Their insurance business is also doing quite well and a potential candidate for merger which will also be a potential trigger for valuation. The company has initiated a process for rewarding the shareholders and creating the valuation after a long time and I believe this process would continue.

Discl : Am currently invested approx 4% of my portfolio

Hi …Thanks for starting new trend.

Iam very much excited to know that Mr Damini is holding 10% stake in this wonderful company.

However, here is my take… earning growth for last three years 2014,15 nd 2016 was 7.4%, 1.7% and 2.6% .For 17 it might be the around same level…With these earnings growth and PE of 32 seems to be little upside… and little chances of higher side.

.

Mr Damani owns approx 1% stake current valued at Rs 150 Crs. You are valuing the business based on standalone PE, you are not taking into valuation the investments the company is holding into, 75% stake in Royal Sundaram, investments in AMC and other business. The actual value of those investment along with the proposed demerger is significant. Further as far as the performance is concerned, agreed that theyPAT has not been growing at a substantial pace, but there last quarter performance which was way better than what lot other NBFC had reported, I think they are getting their mojo back, however you can wait for one more quarter if you feel this is one off. Further If you value all the investments held at marketvalue it would be quoting at a bookvalue of less than 2, compared to other NBFCs who are quoting at a book value of around 4 and have been raising capital aggressively. I believe this should be steady compounder and with a conservative management there is no significant risk at the cmp.

Hello,

I developed a recent interests in demerger after reading chapter 3 of the book-you can be a stock market genius. this stock has already gone 7 times in last one year. in view of that, you still believe the demerger will unlock value? a recent exp I have is of PTL and artemis demerger which took 1 year since identification to develop. Appreciate your thoughts on this.

Regards,

“this stock has already gone 7 times in last one year” which stock Sundaram Finance…??

Yes sundarsm finance only

Your info on price rise appears to be wrong.The stock appreciated only 25% Y-O-Y. Very slow and steady stock. The stock has gone up from 1230 (17.3.2016) to 1593 with a low of 1085. .

My take is one should wait for demerged entity listing and buy if it trades below intrinsic value. Calculation of intrinsic value is a pending task. However, rough calculation shows that SOTP value comes in the range of Rs 77-100. So, this being a holding company I will give 50% discount. So IV comes now 37-50. Hence, worth a buy if trades after spinoff at Rs. 10-20.

Thoughts / questions welcome.

Yes. I misread it apologies.

I also took another look at the pdf and realised its cross holding in other TVs companies and Jvs is too intertwined and kind of a lock it one needs to exist or gain from a subsidiary or JV doing too well…

comments welcomed.

Aren’t there enough holding companies at huge discounts?? How is the demerged entity different from Bengal & Assam, rajapalayam mills ltd and etc?

Am i missing something here?

disc: invested mainly as an opportunistic demerger situation kind of bet. basic theme was that there seemed to be low downside post the announcement of de merger at around 1380-90.

Nice Find Dada…Tgts looks achiveable.

Would look forward to thoughts on how price of 2400-2500 is achievable. The company is great but looks fully priced.

Hitesh sir… could you pls help us to understand that how buying SFL before demerger is better bet? in comparison to buying demerged entity after demerger. are you saying that we will get demerged entity free as there will not be any meaningful correction of SFL price post demerger and hence value of SFIL is nothing but pure profit for an existing holder?

atul,

I had my eye on sundaram finance since a long time having tracked it before too. Demerger just came about as a surprise for me. I liked the move by the management because post this demerger there is likely to be higher focus towards the finance business and whatever accrues out of demerger is likely to be icing on the cake.

Sundaram finance main business is CV and passenger vehicle finance, home loan, asset management and the loan book growth was not great since past few quarters and hence the stock price also went no where. But if economy revives as expected then the company would be in a sweet spot. Insurance business would have an optional value.

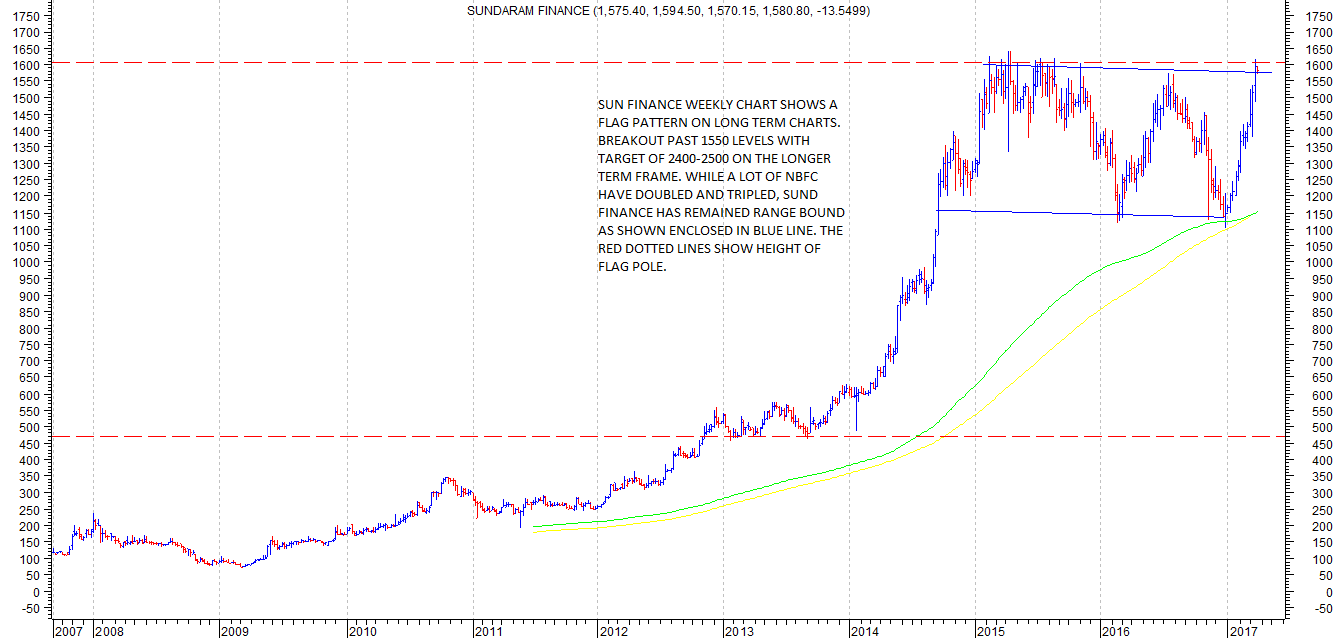

Companies like sundaram finance are super stocks kind of companies which dont undergo too much correction in terms of value but have time correction for long periods of time. The consolidation in SF seems like time correction which was long overdue post the stupendous run from 500 odd levels in Sep 2013 to 1600 in April 2015. Lets see how the possible breakout pans out in terms of stock price. For me levels of sub 1400 were a kind of situation where downside was limited and any positives out of demerger could provide decent upsides.

Hi Hitesh/Atul:

At a PE of approx 36 (based on 24 March closing price of SFL of Rs 1,567/-) coupled with the fact that there has been a 13% price rise in the stock post announcement of de-merger on 17 Feb 2017 (when it was Rs 1,384/-); I would hesitate to venture into the SFL stock right now.

Real value lies in the listed shares of Sundaram Clayton, Wheels India and IMPAL being transferred to SFIL; because:

-Market Value of these holdings are much higher than the book value due to the P/B ratios of these entities ( P/B of Sundaram Clayton is > 11 times vs of SFL at 4.7X);

- ROE & ROCE of the first two of the three have been showing an improving trend over past 4-5 years data seen);

- Possible Operational inefficiencies of the de-merged entities when managed separately under SFIL umbrella.

Based on 14 March 17 Market value of the de-merged entities, De-merged entity MV works out to Rs 2,655 crores (book value of 919 crores). If SFIL issued capital will be 15.11 crore shares of Rs 5/- each (per SFL letter to NSE dated 17 Feb 17), then the market value & book value works out to Rs 175/- and Rs 60/- respectively. At a 50% discount due to holding company structure, the fair value would range between Rs 87/- and Rs 30/-.

Comments invited with numbers to back.

SOme more reading on demerger gains potential. Best wishes

Disclosure. learning more on this- have added ptl and sundaram fasteners…

Hi,

THere is no update on the demerger for sometime. Infact even the name of company has been changed.

Do you have a read on this? Please share your thoughts.

An old but useful link of sundaram clayton demerger-http://neerajmarathe.blogspot.in/2012/06/sundaram-clayton-demerger-not-so-sundar.html

Looks not a clear work on demerger then, now there is no communication on this demerger…

.

any news?