Sundaram clayton is demerging it’s non automotive business and will give 1 share of Sundaram investments limited of 48 for 2 Sundaram clayton limited share.The stock is available at a PE of 10 .The company’s 87 % shares are with promoter and mutual funds.At cmp 160 we will get a dividend yield of around 5 % + 24 Rs gain on each share due to SIL. With aluminium prices cooling off and good demand for aluminium cast dies as auto sector will recover we can expect good results.It qualifies for a good short term pick

[ Comment too short ]

This announcement was made long ago and the exit option of Rs.48 was announced on 19-Jan. Seehttp://www.bseindia.com/xml-data/corpfiling/AttachHis/Sundaram_Clayton_Ltd_190112.pdf Link: http://www.bseindia.com/xml-data/corpfiling/AttachHis/Sundaram_Clayton_Ltd_190112.pdf

Has there been any new development after that?

Dear Ajit Sorry for late reply .Kindly read the footnote of the quarterly results of march quarter. I think they will take decision on 18 may.

Regards

Hi,

This is first time I am trying to understand demerger / merger kind of situation and trying to understand. Can someone publish the findings if (s)he has done the research.

Regards,

ved

I also feel Sundram Clayton looks good to add even at 170 . De-merger when approved by High Court and reduction of number of Equity shares( Half Qty ) of Sundram Clayton .

As`such company is doing good and with reduction in number of floating stock in market one can expect decent gains. Joint Venture with BMW for motor cycles also can be a good trigger. Company holds 40/45 % stake in TVS Motors.

Manher Desai

I’m trying to understand how the CV cycle (if it turns) would have an impact on this company. Since the company manufactures aluminium diecast for commercial vehicles, shouldn’t it be a direct beneficiary IF global growth picks up?

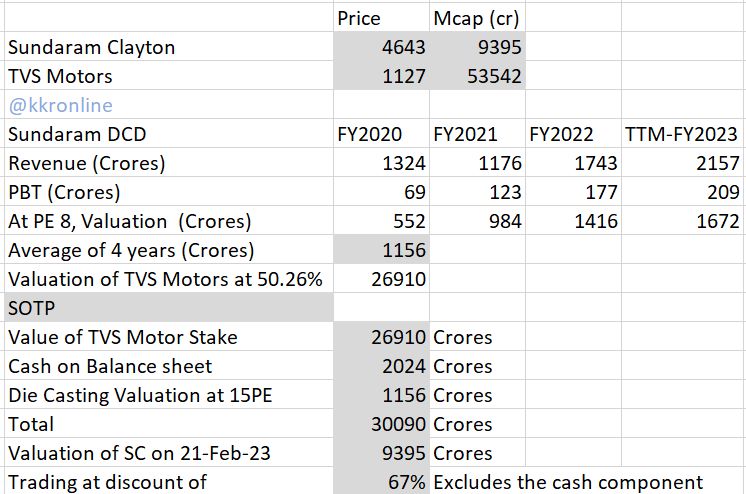

Besides, the company is the holding company of TVS Motors and holds 27,26,82,786 shares in the company. As on today, the market value of the stake would be ~Rs 19,469 Cr, and the market cap of Sundaram Clayton is Rs 10,033Cr. And not to forget, Sundaram Clayton itself has a strong business on a standalone basis with an annual turnover of Rs 1,400 Cr and generating a healthy ROE of >15% (on a standalone basis, according to screener.in).

Wonder how much value is there in this company going forward?

Disc: invested

Whats the reason for such a high pe ratio of sundaram clayton ?

Anyone can share views on this company? High debt and tremendous price drops in the stock? Can’t figure out what’s the plan ahead…

1 Like

Special Situation Alert:

- Company announces demerger and bonus issue of NCRPS bearing 9 % p.a.

- Rs. 1160/- worth to be received in the form of NCRPS which is equivalent of cash.

2 Likes

I have tried to summarize the opportunity with what can go wrong with the investment. Let me know your feedback.

4 Likes

Die casting business would be valued much higher, you have taken 1000 cr sales whereas the current rate is around 1600 crores and the amount of capex they have done over last 3-4 years, then can easily hit 2000 cr topline

1 Like

It was mentioned too in the credit rating report that their US subsidiary is also expanding which will increase sales to around 1500-2000 cr range for die casting business. But I created a base case scenario where the company remains stable as it has been in the past.

The bear & bull case scenario is highly subjective. Hence I added link to excel sheet & described the calculations so anyone can modify according to their views.

1 Like

Sundaram Clayton (CMP: 3600 )going for corporate restructuring.

Issue of Non-Convertible Redeemable Preference Shares NCPRS : 116 of FV10 for every 1 sundaram clayton share. Coupon rate is 9%. Redemption by Feb 2024 or 12 months from issuance

TVS holding limited and VS investments limited are parent company of Sundaram clayton. which will be merged with Sundaram clayton as part of process

Then Sundaram clayton DCD is demerged which will be given the operating business of aluminum die casting

Sundaram clayton will become the holding company of all investments

Bonus Shares: 1160 +9% given

If you take conservative 15PE, then Sundaram Clayton DCD would be valued as 1300 crore; (Whereas other sundaram auto ancillary were valued more)That means Rs 650 per share

Is the resultant holding company worth Rs 1750 per share or 4500cr mcap? It would be holding TVS motors, Sundaram auto components,TVS housing, TVS housing finance …etc. The holding company discount would be steep like Hero, Britannia, Sundaram. So think twice on this unknown scenario.

The calculation was done last month. Price is more or less same only. There is nothing left as special situation alpha.

However, the reverse merger possibility with TVS motor can bring lot of value into the visibility. Have no holding as on date.

1 Like

Is anyone still tracking this company.

Is the demerger over, and shareholders received the shares of demerged entity.

If not, if someone invests now, will he get the shares of demerged entity.

The demerger is already over, the new shares are also credited in CDSL/ NSDL demat accounts and waiting for trading approval.

The current company is just the holding company of TVS motors. check the historical valuations and holdco discounts for entry.

The company data shows sales and profits. So if the demerger is over, the sales will remain on its book even post demerger.

So besides being a holding company will it also have some business of its own.

Is my understanding correct