Not necessary to have some business of its own, it can show the dividends, sales of subsidiaries as w.r.t it’s holding… I guess. there are these two kinds 1) just act as hold co examples maharastra scooters, bajaj Holdings, Ujjivan Financials the other examples likes of Kama Holdings, Hercular Hoists etc.

The listing date has come… from today the aluminum casting division is going public.

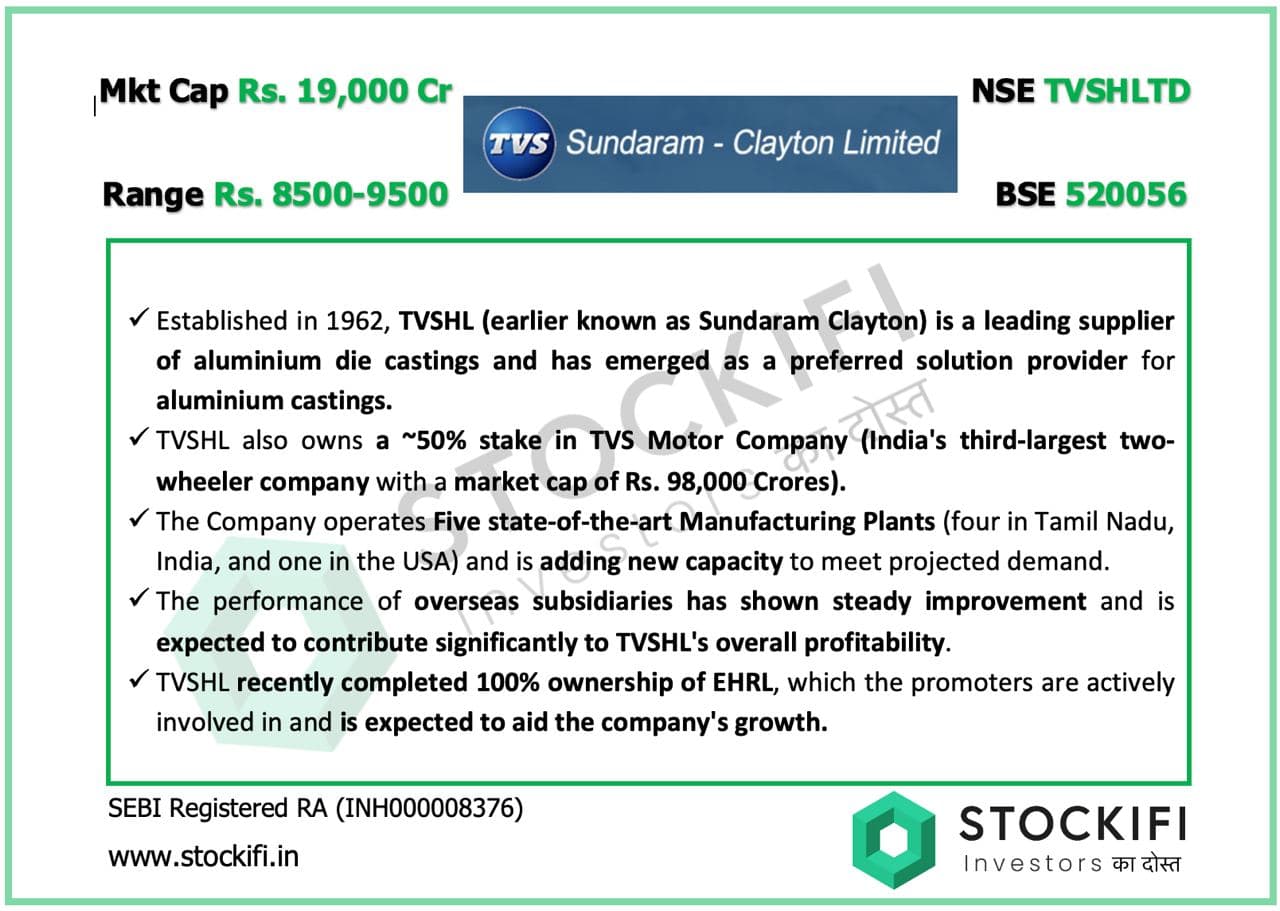

SUNCLAY.pdf (1.5 MB)

Can anyone tell me what’s happening in this counter?

It’s present in my investment portfolio… I’ve checked after many months and found now I’m having shares of both the companies

Tvs holding & sundaram clayton

Initially I’d brought only sundaram clayton, under demerger what’s the ratio?

Was it 1:1?

yes the demerger ratio is 1:1, TVS holdings holds TVS motor company shares, Sundaram clayton does aluminum casting business.

1 Like

Hi Kandukuri,

I recently came across a report (publicly available) stating that TVS Holdings is a leading supplier of aluminum die castings. My understanding was that TVS Holdings had transitioned into a core investment company (CIC) and no longer directly manufactures auto parts.

Could you please clarify whether TVS Holdings is still involved in die casting or the auto parts business?

Considering TVS Motors market cap 99241cr - 50.26% value of holding is 49.8k cr. Currently trading at 57% which can only be a trigger for TVS holdings to rerate?

No, TVS Holdings is not involved in die casting. The aluminium auto parts business was demerged and listed separately as Sundaram Clayton.

I don’t know about the competition in auto components. Sundaram Clayton is still a high debt and low margin business.

You read it’s annual report for further details.

The recent rally in TVS Holdings is more related to new NBFC venture rather than TVS motors stake. I believe TVS Holdings currently reached the max possible discount. In general when the discount between holding company and the actual company comes close to 52-57%, you should exit, If you follow the previous cycles ( based on reading from report). However due to recent announcements ( venture into NBFC, Real estate) and uptrend in Auto sector,I continue to Hold, if you have bought previously. However, New entry is not an value buy from now as it’s like predicting the future without any results.

2 Likes

Thank you for the prompt reply. Your detailed insight about the company is helpful.

Hi Kandukuri,

Your comments above have been super helpful, so firstly, thank you so much for educating all of us.

I have 2 questions:

- How do I value TVS holding business other than its stake in TVS motors?

Context: today the market cap of TVS motor is ~115k. TVS holding has ~50% stake and then factoring in 50% discount due to holding structure of TVS holding, the market cap that TVS holdings gets due to TVS motors is ~25k, which is where TVS holding is exactly at today. So I want to see how much fuel do we still have in TVS holding?

- What is your perspective on Sundaram Clayton valuation?

Context: I feel it is suppressed because its profit have been taking a huge hit due to non operation of USA factories and fixed cost from them. However this may improve on some years. Also, I think the huge Chennai land they have in the prime area, is worth a lot which they may sell some day. Whatever I am saying here is not with a lot of confidence, so looking for guidance from you as well. Thank you!

1 Like

Hi.

Sorry for the delay in response.

Q1) I do wonder, how much of optimism is already built in TVS holdings CMP, because of latest SEBI special trading session for holding companies, the current auto sector bull run and the future potential of NBFC status. I would say my entry was in the hope of NCPCRS and the compression of Holding company discount.

I have tried the company with less than 2% of my portfolio size. Even though it more than doubled, It didn’t reach a position to cut my holding. Further I’m not ready to add more at CMP. As per my thesis I should have already exited. But I haven’t done that, I’m hoping to exit at the end of Auto sector bull run (don’t know exactly, may be using some technical analysis).

Q2) I have not studied well about the Sundaram Clayton, initially I thought it was the only company doing aluminium die castings, but later found that they have the competition and their major focus on Comercial Vehicles ( CV), I have exited in the initial sessions of trading and not following currently.

Hope this helps.

2 Likes