Sumitomo to acquire Barrix Agry Sciences Private Limited.

Barrix Agro Sciences Pvt Ltd. is into R&D innovation, manufacturing and marketing of IPM (Integrated Pest management) & IPNM (Integrated Plant Nutrition Management) products with special focus on pheromones with dispersion technologies, that are used to monitor and

trap agricultural pests.

Size and Turnover of the Target: ₹380 million for FY 2022-23 as per the management certified financial statements

Sumitomo Japan is looking India as their global manufacturing base. Bio Rationals is the new focus area of Sumitomo Japan.

Further, Sumitomo Japan is in talks with Sumitomo Chemicals India for many molecules at least 5-6 molecules further, which are Top Class molecules, not the old molecules and they are thinking to get them produced in India.

These are all the new technology, new molecules, & very very bright futuristic growth molecules. (new generation)

refer Q4FY23 Concall Transcript…

El Nino, Chinese dumping and channel destocking especially in the international markets badly impacted the Q2 FY24 performance, according to the management. But I will take this with a pinch of salt. For Sumitomo, 75 % of the revenues are from India and things were not all that bad in the domestic market. Dhanuka Agritech whose business is largely domestic reported revenue growth of 14 % (which means volume growth should be even higher). Even Rallis reported marginal volume growth. Sumitomo on the other hand reported 3 % de-growth in domestic volumes. Meanwhile, there seems no sign of company utilizing the huge cash pile it is sitting on, as there is neither any large capex nor big bang acquisition on the cards. No plans to returns cash to the shareholders either, at least there was no mention of that. Everything seems to be move very slowly in this company. Perhaps that is the Japanese style of working.

Anyway, some highlights from the concall:

-

Revenues were down 20 % YoY for the quarter overall.

-

Exports dropped almost 50 % in the first half, about 25 - 30 % in volumes and 25 - 30 % in price. Exports were contributing 19 % of revenues in H1 FY23 and now down to 11 % in H1 FY24. LATAM demand has been hit.

-

Domestic business showed 15 % total fall of which 3 % is volume and 12 % is price drop.

-

Company was able to consume all the high-cost inventory that it was carrying as of 31 March 2023 by the month of July

-

Two projects for 5 new products: The first project at Bhavnagar facility has commenced production for a global proprietary product. The second project at Tarapur facility involving multiple EHD products has started commercial production recently. Both these projects are expected to generate some revenue in FY24 but major ramp up only in FY25

-

In domestic business, we launched three herbicides, one insecticide and two fungicides in the first half of this financial year

-

One analyst said in the last 3 - 4 years, we have launched 25 to 30 products but they have not scaled up

-

Glyphosate volume increased 5 % during the year but prices dropped 23 %. Domestically in Glyphosate, there are hardly 2, 3 major players. Exports happen in H2 but they are not very big. The ban proposal will die its own death, most likely.

-

Animal Nutrition business volume increased 31 % in H1 current year

-

One analyst noted that the Environment Health business (EHD) has not grown much last one or two years. Management blamed it on destocking by clients like Godrej, J & J etc. and said things will improve in the coming months.

-

Barrix acquisition - one analyst noted that while the technology is not that new, the acceptance in the Indian market is also not that much. So it will have to be sold globally only. Management said in India this is approximately INR 400 crores to INR 500 crores market today, which is spread across several unorganized players and there is no single large player who is having a very good national level presence, having very good technology.

-

Normalized capex for the business is around 15 % of EBIDTA. Project specific capex if any will be over and above this.

-

One plant which manufactures Quinalphos and Tebuconazole was non-operative from the month of April to almost August end.

-

One example of destocking - We sell a huge quantity of Profenophos to Syngenta for global market. And what we were told that there is a full stop, to not increasing even 1 kilo of inventory till 31st December (Just a thought - what if Kumiai does this to PI)

-

One analyst said based on recent commentary or guidance downgrade by a couple of the global agrochemical majors, it appears that at least even in the near term the situation does not seem to be abating.

-

Cash in hand is Rs.1400 crores but no big bang acquisitions. May go for smaller niche companies rather.

-

Dahej land is very big and the capex will be around Rs.300 crores - spread across 2 - 3 years

-

Promalin - launched in March this year. Lot of hopes on it. It should transform how the apple farming happens in India.

-

The normal industry average growth in a normal year historically is somewhere between 8% to 10%

(Disc.: Holding)

valuations across the agro chem space seem to attractively priced currently - just for context if we see the results from Bayer , Basf , GAVL etc : Risk to Reward seems favourable for Sumitomo Chem : one pertinent point ref Glyphosate hearing on 7th dec 23 company management believes that regulatory restrictions are unlikely

Any impact post this?

It’s just a temporary postponement and should not have any impact in my opinion

Yeah market had already priced it in, so no movements today. I guess, it will only be revenue growth which will move it further considering the current high PE it is in

Amid widespread distress in the agrochemical sector, the Sumitomo share has shot up and settled at a level above where it had crashed to when the glyphosate controversy first erupted more than 18 months ago. Q4 results were good, margins were among the highest in recent years, sales growth returned after 4 quarters of decline and operating profits were sharply higher by 74 % YoY after 5 quarters of degrowth. Cash flows were very strong and dividend payout has jumped due to a special dividend declared in February this year. More importantly, the concall revealed even bigger surprises which seem to have excited the market.

Some highlights from the Q4 FY24 concall:

-

Q4 & full year FY24 performance: The decline in domestic revenue during the year was caused by mix of both price and volume reductions. Pricing decline of 25 % to 30 % was seen in FY '24 across. The decline was mainly in generic molecules, decline in specialty was only around 2 % or so, but here volumes have degrown by around 8 to 9 %. The decline in prices of key active ingredients has now stalled to a large extent. The company did not pass on that entire cost benefit in the market. It launched 6 new products - 3 herbicides, 1 insecticide and 2 fungicides in FY '24.

-

Two projects with around Rs.120 crore capex initiated in 2021: Both these projects have started commercial level production. In the first project, 40 to 60 % commercialization was achieved last year and it will be ramped up to 100 % this year. In the second project, some revenues will come in the current year and ramped up in the next year.

-

Bhavnagar plant: Current year, 100 % of the production capacity Is expected to be exported out

-

Tarapur plant: New plant is ready for commercial production. It is only for exports to affiliate companies. Those molecules are not sold to any other third party.

-

Dahej plant: The application for environment clearance has already been submitted. It will have at least 2 brand-new products from SCC Japan. However, it will have a gestation period of at least 18 to 24 months after the EC is received, before supplies for the next set of molecules start. But the product which will be picked up will have a very long strong competitive situation for at least next 10 years plus, either in terms of patent protection or in terms of SCIL’s leadership in those products all over the world. They will not be commodity products.

-

Barrix: The acquisition helps in expanding the product segments in environmentally friendly technologies. Barrix was acquired on 15th December 23. In terms of the sales, about INR 10 crores to INR 12 crores has been consolidated in the books for this 100-day period.

-

Parent’s commitment: The management said the parent company in its various presentations and investor interactions has emphasized the importance of India as a market and as a manufacturing footprint indicating future growth potential for India and SCIL. India is a priority for them. The top management of SCC want India to be a big manufacturing hub in times to come. (My observation is that parent’s commitment to Indian subsidiary is the most important driver of valuation in case of MNCs, and this must have sounded like music to analyst’s ears)

-

Electronic Chemicals: The management said the parent company is quite strong in electronic chemicals. Some of these technologies used in the display devices such as chemicals used in LCD, LED, QLED - Sumitomo has been one of the leading companies in the world. In addition to that, some of the products that go into semiconductor for the 5G mobile tower and mobile stations, in those applications also Sumitomo has a very strong presence globally. In India also, there is this whole ecosystem gradually being set up. We are now seeing a bit of scope of doing this. We have just got the preliminary inquiry from Japan, they have asked certain very high-level questions. What will be the final decision or outcome of it, we are unable to say. But for sure, it is starting now. And it (i.e. the foray into electronic chemicals) will be through Sumitomo Chemicals India Ltd only and not through any other company. (This again is very good news, and though actual action is still several years away, is more than enough to excite the investor community in the current environment).

-

FY 25 and beyond: The management said they are concentrating on increasing the volumes of their products first. The purchasing in Q4 for the coming quarters has been at a very good level, very good pricing. So the current margins will remain at least for another few quarters. As of today, they feel that pricing is quite stable and they don’t see any risk of reducing the prices in coming months. Because of the (good) rain forecast, the domestic market will revive very quickly. As it revives, SCIL will revive further. International business revival may take some more time. But there is stability in order positions. About 8 % to 10 % contribution may come from new products. There will be at least 3 new product launches in FY25. These are 9(3) proprietary products, which will be coming into the market in the next few weeks targeting the Kharif season. And there are 1 or 2 more products, that depends on the regulatory approvals. Overall, they are looking at 12 to 15 % volume growth in the domestic market.

To conclude, those who held on to the stock amidst the more than a year-long distress seems to have been vindicated.

(Disc.: Invested)

Few observations while deep-diving in this company ![]()

a) Parent compnay has discovered only one new molecule in last 30 years in agrochemicals space , rest of the products are 30-40 years old .

b) During last 3 years, company’s domestic business of speciality products is going down as far as volumes are concerned (most of these products are old discoveries), hence it seems that they have either reached their maximum potential or competitors are gaining market share from these or the company does not have capability to grow these further.

The top-line for these specilaity products grew after Covid in lines of price-revisions across across agrochemicals industry. But the concern area is volume-decline (loss of market -share).

Even the new launches of speciality products have not compensated the losses of old speciality portfolio.

c) After acquisition, the company is focusing more on generic business and is very much dependent on export (orders from parent company).

d) Other observation one can draw from parent company’s latest results is that agrochemicals is one of the business for the company among many other varied businesses. So it is not a pure-play agrochemical compnay. From same report, one can conclude that the parent company is struggling very badly - losses as well as high debt/equity ratio (1.3). And it seems that the parent company is desperately selling some businesses to improve debt-equity ratio.

In nutshell, the company is more of a generic-play (cyclical ) in India and export-play (for the parent company).

Thanks for these valuable inputs!

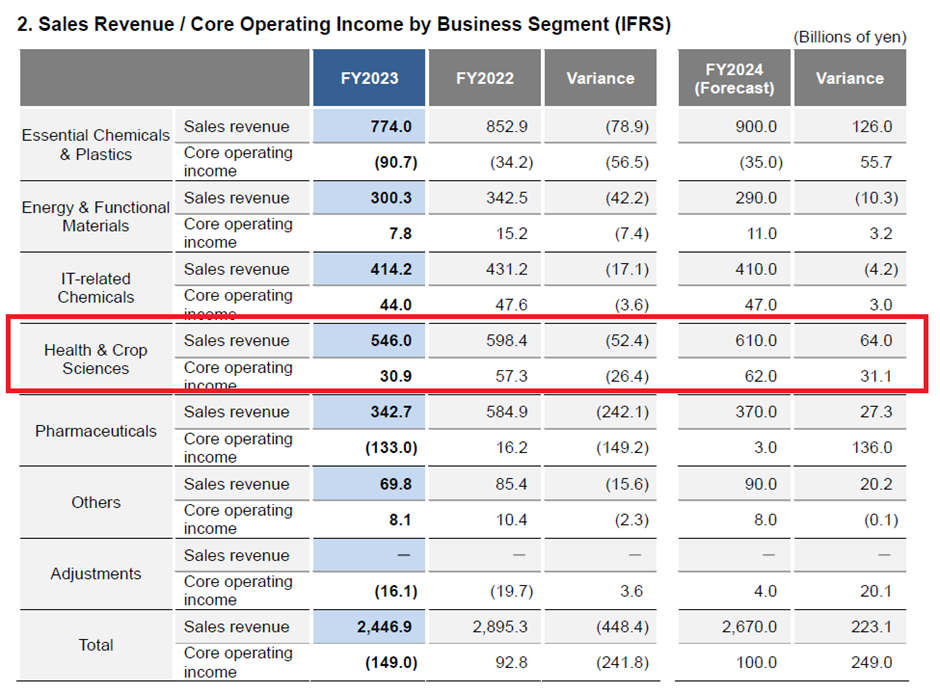

Being diversified is not a negative by itself so long as the parent is committed to the product line in question, several large Japanese / Korean companies are diversified (or Reliance, in India). As far as I can see the parent’s Crop Protection business is doing well and made a profit of 30.9 billion Yen in a difficult year when many others in the sector have reported losses.

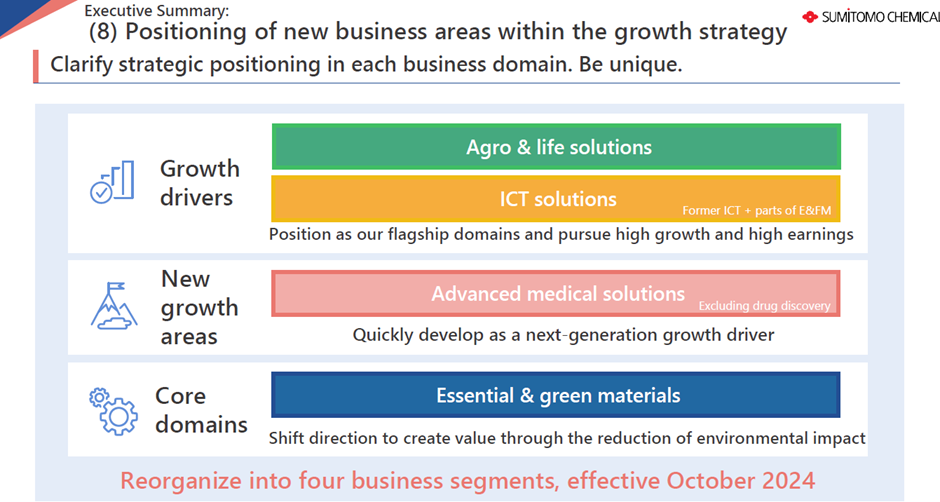

The parent’s losses came from other verticals like Chemicals & Plastics, and Pharma. I look at this as a positive for SCIL, since it improves the relative importance of Crop Protection within the parent’s portfolio. In fact, the guidance for 2024 is to double the profits of Crop Protection to 62 billion Yen, as the above table shows. In their presentation, the parent refers to Agrosolutions and ICT as “growth drivers” and “flagship domains” (see below).

I think the last three years have witnessed large scale distortion across the entire chemical / pharma / agrochemical space, first due to a huge spurt in prices amid covid lockdowns and supply chain shortages, and then the dramatic fall last year once the Chinese supplies resumed. All numbers for the last 3 years must be viewed with this caveat. Many companies with significant international exposures have made losses (take UPL, for example) and Sumitomo parent is not an exception. They were in profit in FY22, and guidance for FY24 is also for a profit.

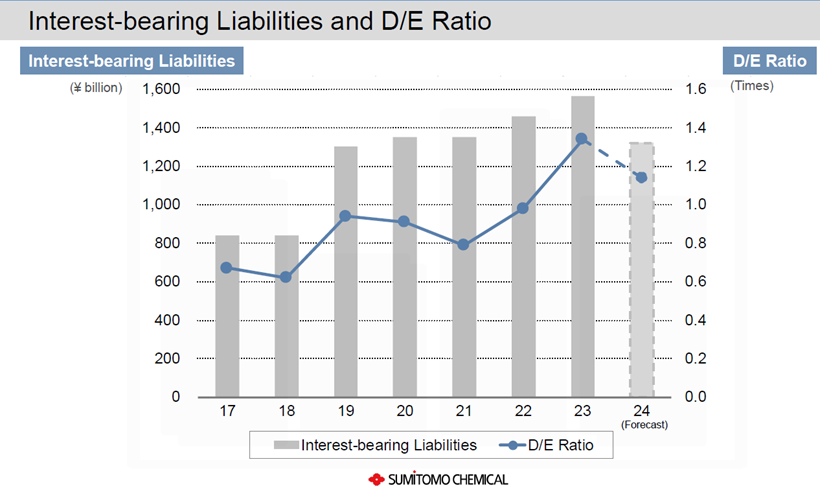

The Debt / Equity ratio of 1.4 – not very high by itself – should also be viewed in this context. It was much lower prior to this crisis and is expected to go down as situation normalizes. See the chart below.

Still if they sell off other businesses to reduce debt, that again is a good thing as it just increases the importance of agrochemicals for them. And when the management says they would like to make India a manufacturing hub – as it seems from the recent pronouncements – that would override these temporary (hopefully!) issues and make SCIL more valuable for everyone in the long run, I think.

As regards new product discoveries and volume data, the company does seem to have an extensive R&D as is apparent from their public website / ARs etc. But I am not able to locate the precise data points you mentioned, can you please share the source of your information so I can investigate this aspect further. Thanks in advance!

Any data in isolation is a dangerous data. Compare it to the last year as well as various forecasts given over last year, you would undertand the point.

We consider all generic businesses in same manner . They’re (all generic bsuinesses )like tiny boats in the ocean, when the water is calm and wind is in your direction, all boats seem to be doing great. Real boats and boatmen are tested in stormy times. This company and UPL has really done really bad during bad times .

In these kind of industries, you don’t trust boats as they are too tiny in the ocean. In high tide ,they can rise to any level, But when the tide dies down, they don’t know where to go.That’s why forecasts also go wrong. No one in a tiny boat can forecast what would happen in the next high wave of the ocean.

Look at the track record , their previous guidance and actual results.

They gave 3 forecasts last year, and failed to meet any of the forecast. Even the forecast given in February was not acheived in March.

That shows the disconnect between the management and the ground. And it also indicates that all forward looking statements from this company should taken with pinch of salt or bowl of salt in casr of Japanese parent.

Diversification is not all an issue. But how you manage different verticals ,that is the issue.

These are motherhood ,generic statements.

These kind of presentations are made by proffessionals, when companies don’t have clear plans, they start using acronyms .

Check what they are selling. If you sell what you bought just 2-3 years back or you built 2-3 years, back-that tells a lot about the management vision.Check the history of Nufarm-Sumitomo deal and how much they lost over the duration of 10 years, your would understand the quality of top management of the parent company.

Take the names of AIs of specialitty chemicals of the company from any distributor in your area and check the history on Google, you would get to know.( it is simple work )

When one is biased , every debt:equity ratio may look good.Increasing debt in increasing interest rate-scenarios is never considered good.

Overall , we’re not saying that company is bad. We’re just saying that the comapny is in generic and cyclical products , and should be valued accordingly.

But markets don’t work like that.

There are many other factors that makes the basis of price. In this case, despite being a generic & cyclical company ,the price may remain high due to a MNC tag and its major shares lying with mutual funds.

![4005_2024-06-20_06-35-52_00ab0|690x474]

Monthly Chart

This is what Japan market thinks about the parent company. Price is moving towards Covid lows (Feb 2020) whereas overall Japan market has gone up by approximately 250% over the Covid lows (Nikkei 225- 16000 to 39000).

Otherwise also , we Indians have a habit of paying high price for foreign goods irrespective of quality ( true in stock market also) ![]()

Blockquote

a) Parent compnay has discovered only one new molecule in last 30 years in agrochemicals space , rest of the products are 30-40 years old .

@StageInvesting - you mentioned this above. May I know where you found this statistic? From one of their reports, it appears in crop protection chemicals alone they have over 2300 patents and they have launched new molecules every year. They have also collaborated on R&D with Bayer and Valent on different products. I am not clear why you say they have discovered only one new molecule in the last 30 years. That seems incorrect - happy to be corrected if you can share the source.

Name 5 new molecules- discovries done by them in last 30 years !

Getting patents is not a sign of new discoveries …it can be combinationations of AIs, formulation method,methd of application etc etc

Ok, that’s what I was asking you actually. They have certainly discovered new “active ingredients” regularly. I am not sure how this relates to molecules (I have to educate myself here), but here’s a list from just 2018.

Anyway, if there’s some research you can share or can point me towards, that’s great. If not, that’s fine.

There is only one new AI named Indifilin in this report…that’s what I was mentioning ( one molecule in last 30 years)…rest are just code names. Looking at their past success ratio, I don’t think they would succeed in bringing 2nd or 3rd new AI , at least in next 10 years.

And ,also humbly speaking, I would not like to be discuss further about this company. For me it is cyclical generic company where parent is struggling and has a bad track record of last 1-2 decades. Hence would like to stay away as don’t want to waste more time on this.