And Pavecto, this is not one? - Sumitomo Chemical and Nufarm Limited Sign Agreement on New Fungicide Solutions for Germany, the United Kingdom and Poland – Sumitomo Chemical Agro Europe?

That’s neither here nor there, no? I had seen this chart which you posted earlier too. It’s good input and makes one think about it further. Of course, as @Chandragupta pointed out, Sumitomo is a diversified conglomerate. They are not that in India. So it’s not an apples-to-apples comparison.

My question was only about your point that was critical of their innovation capabilities. My reading indicates that is not the case and I wanted to be better informed. But since you haven’t shared specific inputs there, I guess we can leave it here.

5 Likes

Have to say, not quite the done thing to go back and edit an earlier post after we have exchanged messages subsequently. It’s ok if you don’t want to share and have a different opinion, but let’s be transparent here.

I am referring to this edit - “And ,also humbly speaking, I would not like to be discuss further about this company. For me it is cyclical generic company where parent is struggling and has a bad track record of last 1-2 decades. Hence would like to stay away as don’t want to waste more time on this.”

2 Likes

I think you are wrong here…

Nirmal Bang view on SCIL

We have marginally revised EPS estimates and raised target PE from 32x FY26E to 38xJune’26E based on healthy EPS CAGR of 40% over FY24-FY26 - implies PEG of 0.95x. The higher multiple is on the back of improved outlook for FY25E/FY26E in terms of margins and earnings growth. The new PE compares with median PE of 42.1x.

Key catalysts:

Healthy monsoon forecast – already the deficit has turned into a surplus for Kharif FY25,

as per latest rainfall updates.

La Nina is likely to set in over the next one month which is a positive for agronomical

conditions.

SCIL launched 6 new products in FY24 – 3 herbicides, 1 insecticide and 2 fungicides

Agrochemical input prices and de-stocking have mostly bottomed out, as per our channel

checks. Also, SCC Japan’s latest PPT has presented a bullish outlook based on

revival in its CPC business for April-March’2025 (FY24 as per SCC norm)

SCC Japan is also focusing on more sustainable bio and botanical products for crop

protection based on its vast experience and R&D expertise; this is in line with its focus on

regenerative agriculture, as per SCC’s April’24 strategy PPT.

SCIL’s new product launches as well as capacity creation are aimed at securing further

business in Agrochem and Specialty Chemicals. SCC Japan is shifting focus to

regenerative agriculture, specialty chemicals for mobile display (OLED) and power

semiconductors - according to SCC’s strategy PPT.

Discl : Not invested but invested in Punjab Chemicals, Dharmaj , Insecticides India and Astec

2 Likes

Some more random thoughts on Sumitomo:

-

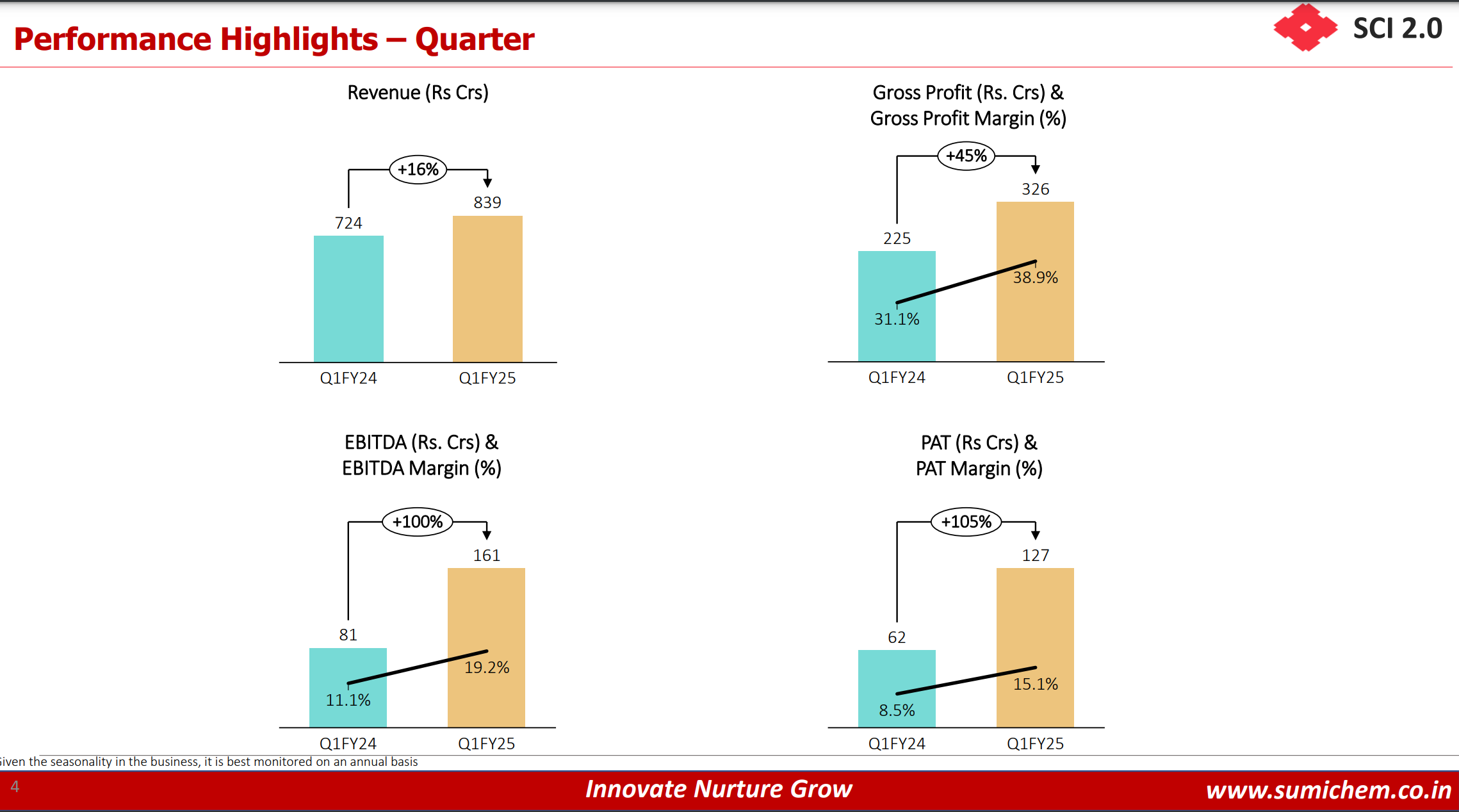

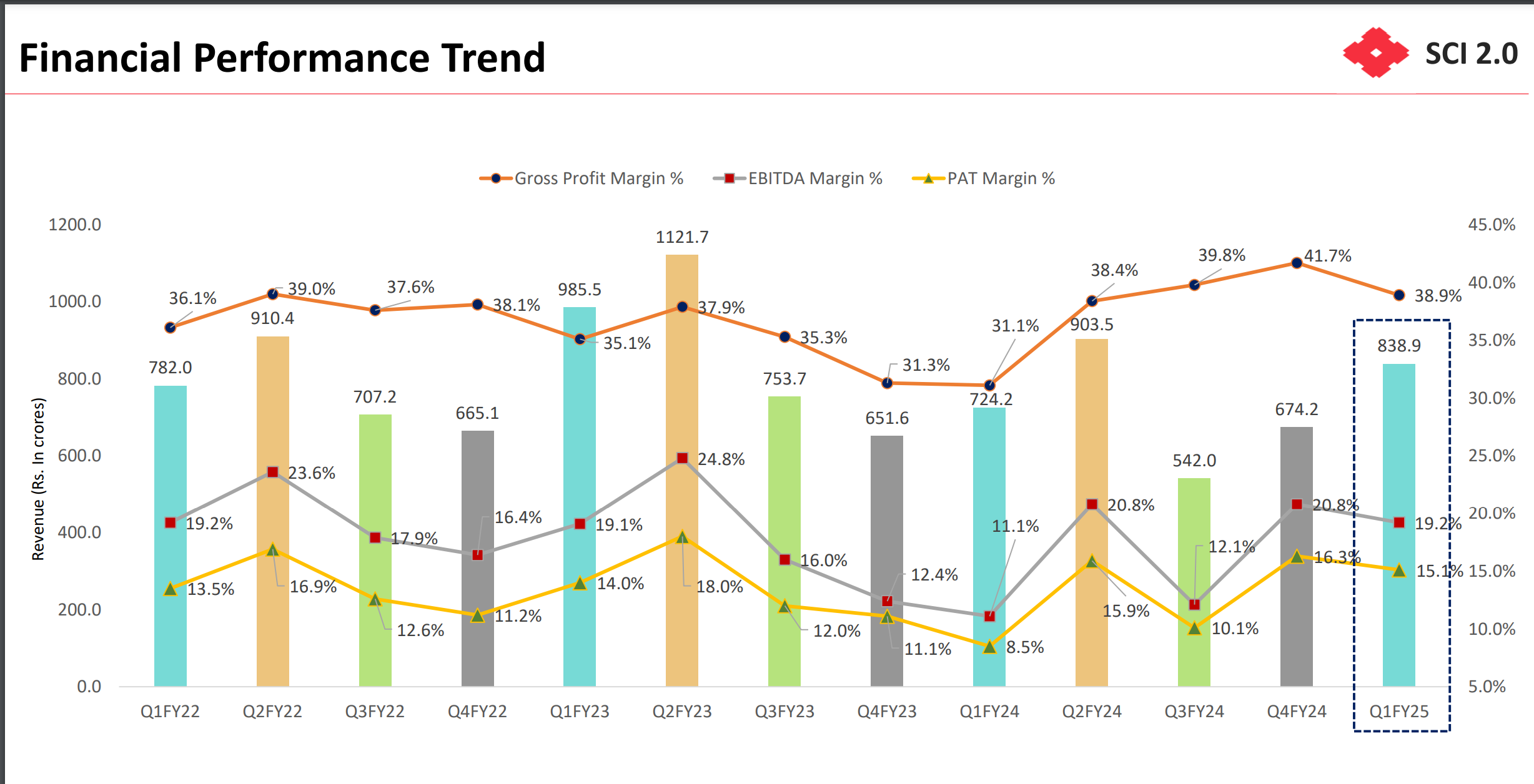

Sumitomo posted strong Q1 results as revenue growth accelerated to 16 %. Operating profits doubled after 5 consecutive quarters of decline. Gross margins, OPM and PAT margins were all at their highest in recent years.

-

Last year, the industry went through a very difficult time and Sumitomo was no exception. But with improved working capital, CFO came in almost at a Rs.800 crore and the cash balance has now swelled to Rs.1500 crore by the end of Q1.

-

At the AGM, the MD said FY23-24 had turbulence kind of which he has never seen in his long career. But now prices are by and large stable, at least they are not falling.

-

The sector seems to have come out of its downcycle and is on the path to recovery as is evident from the results of other domestic focused Ag-Chem companies as well. Monsoon has been benevolent so far, which augurs well for the year ahead.

-

Capacity utilization was lower last year but now stands at 80 to 85 % for technical products and 60 to 65 % for formulation plants. Since business is seasonal, formulation plants are designed for peak seasons and have larger capacities.

-

More than 40 % of the business comes from insecticides and 20 % + from Herbicides. Animal Nutrition was 10 % of revenues last year and will remain in the 7 to 10 % range in the long term, says the management.

-

It has launched 9 new products in the last 18 months. However, the full benefit of this could not be derived last year and these will be ramped up in the current year.

-

Dahej plant will hit full capacity utilization this year while Tarapur will also be set in motion.

-

Currently about 1/3rd of the RM supplies come from China. This will most likely remain as it is and unlikely to reduce any further. Within China, the company is well diversified across regions.

-

The sales target for FY25 is Rs.4000 crore.

-

Biologicals - Sumitomo also has biological products in its portfolio where it distributes products manufactured by Valent Bio-Sciences, an USA based affiliate, in the domestic market.

-

Currently all products are sourced from Valent and there are no plans to manufacture them in India. Presently, this is about 10 % of the business. However, the company wants to expand this significantly as Valent is a global leader in this. In India no one is doing R & D (and therefore manufacturing) in this field, which will give Sumitomo an edge.

-

For the coming year, the company plans to focus on ramping up recently launched products and on introduction of new products which are in the pipeline.

-

The immediate focus is to ramp up volumes from the two newly built plants. In parallel, it is working on medium to long term expansion of the manufacturing capabilities.

-

It has acquired a 50-acre freehold land parcel at Dahej and applied for environmental clearance for the upcoming Dahej site with comprehensive long-term view-point.

-

Glyphosate – The case drags on in court. My feeling is the issue has been consigned to cold storage and the government doesn’t seem keen to push it.

-

R & D - The Company introduced breakthrough technology for oomycetes disease control - Derecho which is a proprietary active ingredient of the parent company and an innovative advance liquid formulation of copper. It has plans to introduce three new patented products in India during the financial year 2024-25. The India R & D team is focussed on producing off-patent products for domestic use and global export. The company has 25+ patents granted across various geographies but their focus is on leveraging SCC Japan’s cutting-edge chemistries and create novel processes and combinations rather than new molecule discovery. The latter task is mainly done by the Japanese parent, who has its own extensive R & D, as well as collaborative agreements with other global majors such Monsanto - Bayer, BASF, DuPont (Corteva Agriscience) etc. Sumitomo Japan has the third highest number of issued patents in the world, after Bayer and BASF. Some of the new products developed by the parent - singly or in collaboration with others - in recent years include Indiflin, Oxazosulfyl, Pyridaclometyl, Pavecto, Rapidicil, Mandestrobin, and Accede. Considerable consolidation has happened in the industry globally in recent years, which works to the advantage of larger incumbents. As an industry size, ag-chem is smaller than Pharma, with lower revenues and lower R & D budgets. Future growth in the industry will come from biorationals, which is growing faster than traditional products.

-

Barrix - SCIL acquired 85 % stake in Barrix this year. It offers environment-friendly innovative pheromone traps, chromatic sheets, bio-stimulants, and plant nutrients suited for multiple crops. SCIL has infused about another Rs.20 crores in Barrix presently which is enough for 2-3 years at least. In fact, it is expected that Barrix may turn cash positive this year itself, hence no further funding will be required. Barrix products are going global as SCIL is in discussion with its affiliates for the same. Group executives from Japan and USA have visited Barrix facilities in India.

-

Drones - The Company has obtained drone application registrations for some products and endeavours to add more products for drone application. The first drone used in India was with a SCIL product for which the company collaborated with government officials for a long period. The products used in drone application are mostly the same, no new products specifically for drone-based application are required to be developed. However, they do not plan to have any drone-based service or start a new vertical. Management says drones will become a commodity soon.

-

Electronic Chemicals - This is the big thing IF it comes through, and possibly the main thing why the stock shot up more than a hundred rupees in a short span of time last month. The management says they have connected with I.T. Chemicals team of Tokyo, given them data basis which they will decide whether to come to India.

(Disc.: Holding)

9 Likes

Earnings are growing slow for Sumitomo… stock should have crossed ₹750 by now…

1 Like

Q4 results were disappointing as I thought the worst is over for the sector and a recovery had already begun in the earlier quarters. But Q4 saw flat revenues and a drop in margins for SCIL. The sector itself showed mixed results, but some companies still showing margin expansion as the table below shows:

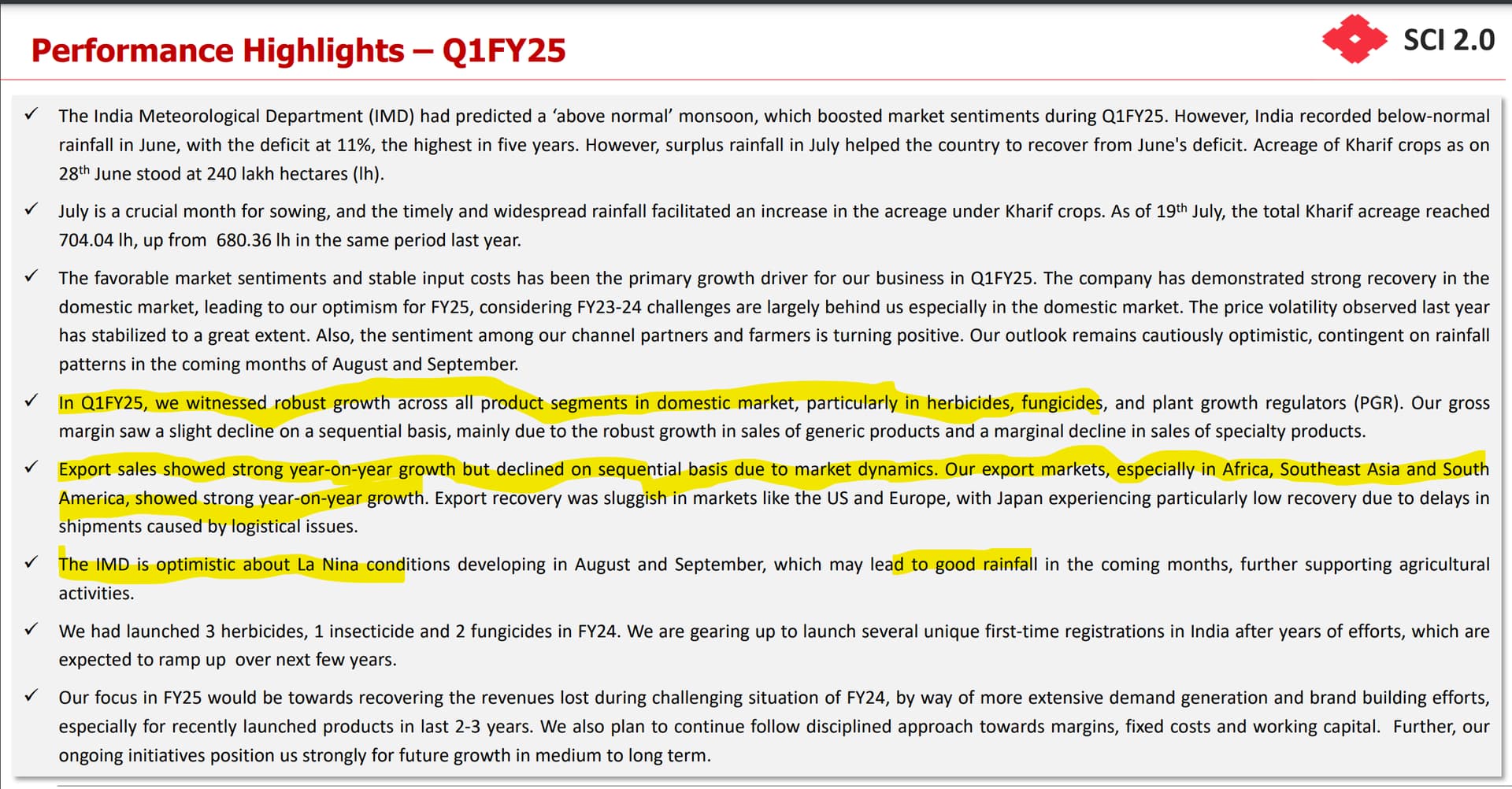

However, Sumitomo’s annual results still look good as the first three quarters had seen good recovery. A few pointers from the concall, with some comments added in-between:

-

On the global front, pricing pressure continues though channel de-stocking is largely behind us.

-

In FY25, SCIL delivered 20 % volume growth in domestic market and 30 % plus volume growth in exports. However adverse pricing trends impacted realization by approximately 10 % in both segments.

-

Gross margins hit all time high of 40 % plus. Company says they are very confident to be able to maintain and sustain these margins. EBIDTA margins have also touched 20 % and may go beyond this, since they are de-emphasising low margin products.

-

Q4 was disappointing mainly on account of LATAM exports where both prices and volumes dropped. Overall exports came in at Rs. 210-215 crore as against Rs. 260 crore last year. Domestic market grew almost 15 - 16 %.

-

During the year, SCIL launched several new products which includes products like Meshi, Portion and Ormie. Also commenced commercial production of CTPR (Chlorantraniliprole) at Tarapur facility advancing its backward integration strategy.

-

Barrix Agro turned around from a negative EBITDA margin to a positive 16 %. (Comment: This was expected, as mentioned in one of my earlier posts.)

-

Planning to launch INDIFLIN in India this year, a newly developed patented global blockbuster product by the Japanese parent. The product will be launched under the brand name “Excalia Max”.

-

The technical for this will also be made by SCIL in India within next 12 to 15 months at the Tarapur plant at an additional capex of Rs.10 crore. (Note: The accelerated launch of a patented molecule and plan to localize its production reaffirms the confidence of the parent in SCIL. The market for Excalia Max in India is estimated at around Rs.750 crore in 2024, with a robust projected CAGR of 14.3% — one of the highest globally for this segment and significantly above other product categories)

-

Excalia Max is being launched for paddy. but it also fits crops like cumin, groundnuts, soybeans, a few vegetables and fruits. It will be extended to them as well later.

-

SCIL also received registration for next generation molecule Lentigo, which is a rice herbicide.

-

Company is finalizing plans to set up a new Greenfield plant at Dahej for manufacturing multiple products for parent Company SCC Japan. There will be an initial investment of Rs. 300 crore to start with, which can be increased later. A range of products will be rolled out in a phased manner from FY27 to FY30.

-

SCIL is also planning brownfield expansion at Bhavnagar site for a “very important SCC global molecule” (name not revealed) at a cost of Rs.55 crore. This is expected to go on stream by Q4 FY27. It is for an insecticide the company started manufacturing two years back and are doubling the capacity now.

-

Foray into semiconductor related chemicals is still under discussion with the parent. Studies are going on and no decision has been made at this point of time. (Note: This is an important trigger for the company that the market must be expecting. Not that anything will happen immediately even if a favourable decision is taken, but given the hype surrounding the sector, it is important enough to keep the PE elevated.)

-

In the domestic market, the company is selling more of brands, less of technical. And in the export market, more of technicals and less of brands. Brand margins are typically higher than technical margins. But the margins between B2B domestic and export margins on technical would be similar.

-

Looking ahead, the management is not expecting any further pricing drop. They say prices are quite stable. Whatever has happened has happened and if at all prices can only inch up from this level.

E & O.E.

(Disc.: Invested)

7 Likes

Great Block buster Q1 results for Sumitomo…Q2 will be even better…great monsoon rains as well..

1 Like

Sumitomo Chemicals India -

They have 5 manufacturing plants in India located at -

Silvasa - 3 Acres - Formulations and Packaging of Glyphosates and other speciality products

Bhavnagar - 58 Acres - AIs and formulations - for pesticides

Vapi - 6 Acres - Formulations and packaging

Gajod - 120 Acres - Metal Phosphides and formulations

Tarapur - 5 acres - AIs

Company produces a total of 14 AIs ( in-house )

Some comments from previous Concalls -

Launched innovative products such as Meshi, Portion, and Ormie in last financial year. Recently received regulatory approval in India for two innovative patented high potential molecules of SCC ( Japanese parent ) - Excalia Max ( fungicide ) and Lentigo ( herbicide )

Their new product intro in India for FY 26 - Exalia Max ( a fungicide used in Paddy, Soybean, Groundnuts crops ) is a patented molecule ( developed by SCC - Japan ) and is already a global blockbuster. They will also be making its AI in India by FY 27 ( @ Tarapur )

Their second high profile launch in India for FY 26 - Lentigo ( its a Paddy herbicide ) is also a patented molecule from the stable of SCC

Exalia Max and Lentigo should do very well in India. At present, AIs for both are being imported and both are being formulated in India

Have also acquired an additional 20 acres near their Bhavnagar plant. Will be making another propriety molecule from SCC @ Bhavnagar ( its off patent now, but SCC continues to command a very high mkt share for the same - globally ). Will be spending 55 cr for this expansion. Should be able to complete this expansion by end of FY 27

Another brownfield capex of 10 cr is lined up @ Tarapur to make another patented molecule developed by SCC. Should be able to commence commercial production of this molecule by end of FY 27 ( just like Bhavnagar expansion )

SCC Japan intends to start manufacturing Semi Conductor chemicals in India. SMIL believes, they ll be considered by the parent for this opportunity

Q2 FY 26 outcomes -

Revenues - 930 vs 988 cr ( down 6 pc )

Gross margins - 43.1 vs 42.6 pc

EBITDA - 218 vs 245 cr, down 11 pc ( margins @ 23.4 vs 24.8 pc )

PAT - 178 vs 193 cr, down 8 pc

H1 FY 26 outcomes -

Revenues - 1987 vs 1827 cr, up 9 pc

Gross margins @ 40.4 vs 40.9 pc

EBITDA - 437 vs 406 cr, up 8 pc ( margins @ 22 vs 22.2 pc )

PAT - 356 vs 319 cr, up 11 pc

Product wise breakdown of H1 revenues -

Insecticides - 39 pc

Herbicides - 26 pc

PGRs - 9 pc

Metal Phosphides - 8 pc

Fungicides - 9

AND and END ( Animal health and Environmental health divisions ) - 9 pc

Domestic vs Export sales @ 85 : 15 ( In Domestic mkts, 80 pc of sales come from branded products. In export mkts, share of sales from branded products is far lower @ 34 pc )

Company’s major export geographies include - Africa, Japan, Asia, Latam, EU. Company also exports to US and Aus ( in smaller proportions ). Most of company’s export sales are AIs and share of Formulations in export sales is far lower

Q2 FY 26 highlights -

The South-West Monsoon, though strong overall, turned challenging during the key consumption period. After a brief dry spell in early July, persistent and widespread rains from mid-July through September disrupted normal agronomic activities, impacting pesticide applications across several regions. Farmers missed a few scheduled spray cycles in major kharif crops due to prolonged wet conditions and restricted field access. Excess moisture also caused localized crop damage in cotton, groundnut, soybean, rice, and chillies, leading to reduced pest incidence and subdued agrochemical consumption

The quarter witnessed a softer performance, largely reflecting the adverse weather impact. While price realization remained stable, lower volumes led to moderated operating leverage and margins

Despite this, the company’s disciplined channel management and prudent working capital practices ensured business continuity without material sales returns or collection delays — in contrast to broader industry trends marked by inventory build-up and payment stress

Export performance was impacted by softer offtake in select markets such as Africa and Latin America, though demand in the U.S. and Europe remained steady. The decline was primarily due to shipment deferrals and product-specific factors in certain geographies

The newly launched rice herbicide ‘Lentigo’ continued to gain encouraging traction, while ‘Excalia Max’ and other key molecules maintained strong market acceptance. Core brands across insecticides and herbicides sustained leadership positions and contributed to resilience in the overall mix. In the Environmental Health Division, branded and custom solution products registered healthy growth off a low base

Cash on books as on 30 Sep @ 2080 cr !!!

Company is bullish about the upcoming Rabi season due healthy reservoir and soil moisture levels

Company continues to work towards strengthening Sumitomo Japan’s supply chains and concentrating them in India for future exports to RoW with India as a key manufacturing base

Company is in the process of registering its formulations in various export mkts. Registration of these take time ( 2-3 yrs, depending on country to country ). As these registrations keep maturing, company’s share of formulations in their export business shall improve ( this segment has better margins vs AIs )

65 pc of company’s business happens in the Kharif season. That trend is likely to hold up in short to medium term

Prices of formulations in the domestic mkt are holding up well ( despite the pressure on volumes in H1 )

Company will develop a new Greenfield manufacturing facility @ Dahej. Work is expected to commence wef next FY. This will be funded via the large cash surpluses that the company currently holds. This site will be developed, keeping in mind Sumitomo Japan’s ambitions to develop India as their new manufacturing hub for their global business

Aprox 35 pc of company’s current revenues come from patented products

Company’s semiconductor chemicals shall be used in fabrication. Company is monitoring the progress of corporates ( specially TATAs ) setting up fabrication plants in India. Once that happens, company shall begin their Semi Conductor chemicals business

Company is evaluating manufacturing of 7 new products ( AIs ) @ Dahej Greenfield facility. Company has submitted feasibility reports iro these products to its parent in Japan. If all are approved to be made in India ( @ Dahej ), company may incur a capex of aprox 500- 600 cr over next 3 odd years @ Dahej

Disc: holding, added recently, not SEBI registered, biased, not a buy/sell recommendation, posted for educational purposes

1 Like

Sumitomo Chemicals -

Q4 and FY 26 results and concall highlights -

Q4 outcomes -

Revenues - 684 cr, up 1 pc

Gross margins @ 42.3 vs 40 pc

EBITDA - 134 cr, up 12 pc ( margins @ 19.6 vs 17.6 pc )

PAT - 112 vs 100 cr, up 12 pc

FY 26 outcomes -

Revenues - 3238 cr, up 3 pc

Gross margins @ 42 vs 41 pc

EBITDA - 671 cr, up 6 pc ( margins @ 20.7 vs 20.1 pc )

PAT - 543 cr, up 7 pc

Exports De-Grew 7 pc in Q4 and by 1 pc in FY 26. African business however did exceptionally well, going by 26 pc and 30 pc in Q4 and FY 26 respectively

Herbicides grew strongly in Q4 and FY 26, growing by 87 pc and 19 pc respectively. Metal Phosides grew by 16 pc and 11 pc in Q4 and FY 26

Product-led execution remained a key focus area during FY26. Newly launched products including Lentigo ( next generation Paddy herbicide ), Excalia Max ( next generation Fungicide for Paddy crop ), Powerpull ( broad spectrum insecticide ), Advika ( broad spectrum insecticide ), Envoy ( broad spectrum insecticide ) and Oslava ( received encouraging market response. Registration of Topgrain ( BioStimulant ) was also completed during the year - strengthening the future product pipeline

FY 26 domestic:export sales @ 79:21

Breakup of Branded:Bulk sales in domestic mkt @ 81:77

Breakup of Branded:Bulk sales in export mkt @ 40:60

Breakup of company level patented:generic mix of sales @ 29:71

Company makes 14 AIs in house, has 5 manufacturing facilities ( 3 AIs + 2 formulations ), has a field force @ 1500 employees

Key export destinations include - LatAm, Japan, Africa, Asia ( ex-India )

Notes from previous concalls -

Company continues to work towards strengthening Sumitomo Japan’s supply chains and concentrating them in India for future exports to RoW with India as a key manufacturing base

Company is in the process of registering its formulations in various export mkts. Registration of these take time ( 2-3 yrs, depending on country to country ). As these registrations keep maturing, company’s share of formulations in their export business shall improve ( this segment has better margins vs AIs ). At present, most of company’s export sales are AIs and share of Formulations in export sales is far lower

Have approved a Greenfield capex @ Dahej - to expand company’s manufacturing footprint for local and global supplies. Company is evaluating manufacturing of 7 new products ( AIs ) @ Dahej Greenfield facility. Company has submitted feasibility reports iro these products to its parent in Japan. If all are approved to be made in India ( @ Dahej ), company may incur a capex of aprox 500- 600 cr over next 3 odd years @ Dahej

Company’s semiconductor chemicals shall be used in fabrication. Company is monitoring the progress of corporates ( specially TATAs ) setting up fabrication plants in India. Once that happens, company shall begin their Semi Conductor chemicals business

Notes from Q4 concall -

FY 26 was one of the most challenging years in Indian Agrochemicals industry due persistent and prolonged rains well into Oct 25. PGRs, Biologics solutions were severely impacted. Exports were hit in Mar 26 due war in Iran. Consumption of insecticides was also affected adversely due unseasonal rains

Company’s share of revenues from Biologics @ aprox 10 pc vs industry avg of sub 5 pc. Should see accelerated growth in Biologics wef FY 27

Lentigo and Excallia Max are both patented molecules ( launched LY ) - both did exceedingly well LY

Products launched in last 3 yrs now contribute to 8 pc of their revenues

Will introduce another 2-3 patented products in India over next 1-2 yrs

Risks for FY 27 - constrained availability of Fertilizers due Iran war, El-Nino induced below normal rainfall, escalating RM prices

At present, aprox 56 pc of Indian net sown area is covered by assured irrigation facilities - making Indian agriculture relatively insulated by vagaries of weather

Have been passing on the RM prices in a calibrated manner. Demand continues to hold up in Q1 FY 27

Cash on books @ 2133 cr

India has been upgraded to same level as North America, Japan, LatAm - for testing and early stage introduction of new / patented molecules developed by company’s parent ( SCC Japan ). Have received 2 molecules for local trials. Its a very positive development

Discussing a new Royalty arrangement with their parent ( previously were not paying any royalty ) - in return for flexibility to SCIL to procure RMs/Technicals locally. At present, such arrangement will be limited to only 2-3 products

Insecticides share of company’s revenues is the highest @ 41 pc

Companys exports and RM imports are roughly equally matched @ aprox $ 70-80 million each - insulating them from currency movements

All the meetings with GoI wrt manufacturing and commercialisation of speciality chemicals for Semi Conductor manufacturings are being jointly attended by SCIL and SCC Japan. Should hear some good news in future

Custom synthesis revenues are roughly around 120 to 150 cr - company does this for their parent. Should see good growth in this segment in medium term

Committed to sustain their margins in FY 27 - despite the challenges in RM prices. Have already taken 3 price hikes post the breakout of war in the Gulf

Have deliberately over produced in Q4 - to insulate against supply shocks

Expect to launch TopGrain ( BioStimulant )+ 1 more speciality product in India in FY 27

Phase 1 of Dahej capex should cost them aprox 150 cr - to be completed over next 18 odd months. Expect a series of more announcements going forward

Company reduced its animal nutrition trading and distribution business in FY 26. Adjusted for that, their core agrochemicals business grew by 6 pc in FY 27

PGRs were affected in FY 26 due excessive rains that led to sharp decline in Grapes output. In addition, there were additional approvals as mandated by GoI for sale of PGRs in India. Company has completed most of them. FY 27 should be a good year for their PGR business

Similarly, fungicide and insecticide sales were badly affected due excessive rains

The cash on books shall be used for organic capex in both agrochemicals and semiconductor chemicals related expansion projects

In general, farmers are more concerned about electricity, fertiliser prices vs agrochemicals ( as agrochemicals r generally used at later stages when the farmer has a good visibility on the crop and their cost vs fertilisers r also lower )

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes

1 Like

Sumitomo Chemical India shares hit a day high of Rs 502.45 on Friday, 3 July, its best session in nearly two years, on parent’s Japan JV news.

Trading volumes told the real story here. Nearly 1.6 crore shares changed hands within the first few hours, more than 24 times the stock’s usual daily volume.

That kind of surge usually means something significant has happened, and in this case it had.

Sumitomo Chemical, the Japan based parent, announced that its South Korean unit, Dongwoo Fine Chem, has signed an agreement with Samsung Electro Mechanics.

Together, the two firms plan to set up a joint venture to make glass core substrates, a newer type of material used inside advanced semiconductor chips.

These chips power everything from AI systems to high performance computers and data centres.

In simple terms, glass core substrates are sturdier and more stable than the materials chipmakers currently use, which makes them useful for the next generation of powerful electronics.

The new joint venture is expected to be set up sometime in 2026, once regulatory approvals come through.

Commercial supply isn’t expected to start until the second half of FY28, so this is very much a long term bet rather than an immediate revenue driver for the India listed unit. The news fits into a bigger picture too.

Sumitomo Chemical has been building up its semiconductor materials business for a while now, and India Japan cooperation in this space has been picking up pace in recent months, with over a hundred business deals signed between companies from both countries.

1 Like