Agree… grain based ethanol plants are unviable at the current grain prices. Increasing the price of maize based ethanol has caused price increase of maize and all foodgrains !!

Sugarcane is the best source of renewable energy:

Cane based ethanol is cheaper than grain based ethanol

Bagasse is used to generate renewable energy which replaces coal based power

spent wash is used to generate biogas

And still the Govt is promoting grain based ethanol over sugarcane based ethanol. no sugar company will put up new ethanol plant for at least 3 years…

Founded in 1933 by Late Ram Narain Ji in a small town of Dhampur, the sugar mill started with the capacity of 300 tonnes per day. With time, the company expanded its capacity and integrated backwards to produce electricity, bagasse etc. With the new generations coming in, the Dhampur Bio Organics was finally carved out in 2022 with Mr Vijay Goel acting as a chairman of DBOL and Mr AK Goel getting the control of the Dhampur Sugars

Business Details

Not very different from Dhampur sugars, the company operates three plants: Asmoli, Mansurpur and Meerganj. The company boasts of the consolidated capacities:

29500 TCD for sugarcane crushing

2000 TPD of sugar refining

700 TPD of pharma grade sugar

800 TPD of low quality whites for exports in neighboring SEA countries

3,12,500 LPD of biofuels and spirits

4.2 million cases of country liquor

95.5 MW of electricity generation

The value added products in the form of biofuels and country liquor is processed only from Asmoli plant. In 2022, the company crushed 43.22 lac tonnes of sugarcane and produced 3.51 lac tonnes of sugar indicating a recovery of 9.42% (since 5.99 lac tonnes of sugarcane was diverted to ethanol).

There are 2 important things worth mentioning:

The company has repeatedly mentioned that they are not expanding ethanol capacity yet and are in the process of evaluating dual feedstock based distillery. This would help them avoid the heat faced due to government decisions on ethanol policy

The company ventured into country liquor due to the fact that the UP government is having a rule to reserve some portion of molasses for open sale so that country liquor can be produced. The molasses in open market fetch Rs 470 per quintal but these reserved molasses fetch Rs 80 per quintal. In order to avoid selling it at lower price, the company ventured into manufacturing country liquor itself

The current capacity at Asmoli is a dual feed capacity where the company can derive either ENA or B Heavy or C Heavy ethanol based on the demand by Oil Marketing Companies.

The company in the last concall mentioned that at current sugar prices, the viability of producing sugar is more economical than ethanol and hence they have paused the ethanol capacity expansion

Also the company has paused converting asmoli unit to multi feed stock since due to maize price increase, the ethanol production from maize would not have been economical. This indicates a very conservative stance for the company. A tonne of sugarcane yields 116 kg of sugarcane (considering 11.6% gross recovery). From ethanol phases, following is the breakup for 1 tonne of sugarcane crushed:

Syrup based ethanol: 78 l, sugar 0

Sugar 101 kg, B molasses based ethanol: 21 litres

Sugar 116 kg, C molasses based ethanol: 10 litres

FY22

Q1 23

Q2 23

Q3 23

Q4 23

FY 23

Q1 24

Q2 24

Q3 24

Q4 24

FY 24

Sugarcane Crushed

40.33

6.02

-

14.10

23.10

43.22

5.50

-

14.48

43.22

Sugarcane Diverted

1.92

0.39

-

2.41

3.19

5.99

0.31

-

2.80

3.11

Recovery

10.34%

9.24%

-

8.73%

9.89%

9.43%

9.63%

-

11.82%

11.60%

Sugar Produced

3.97

0.52

-

1.02

1.97

3.51

0.50

-

1.38

2.77

4.65

Sugar Inventory

2.54

2.14

1.06

0.96

1.47

1.47

1.06

0.10

1.06

2.06

2.06

Sugar Sales

3.29

0.99

1.03

1.08

1.43

4.53

0.97

0.95

0.31

1.77

4.00

We had done some calculations based on the current recovery% and by the fair guesstimate. The revenues from sugar segment only can contribute to 672 crores which is the best ever in company’s short history.

Few reasons to keep in mind:

El-Nino effect is prominent in Maharashtra which would transfer the demand to UP Sugar mills

The company will not sacrifice the production of ethanol from B-Heavy molasses which will contribute to another ~120 cr of revenues since the recovery of sugar from B heavy is minimal

This leads to a solid 792 cr of revenues and 2550 cr of revenue at the end of FY 24. We have considered the realization at RS 38 Per Kg. This can lead to atleast 80cr more profits than last year. Considering the current price, the stock is undervalued and can go up quite considerably.

Last year profits were 111 cr. This year is expected to be ~190cr

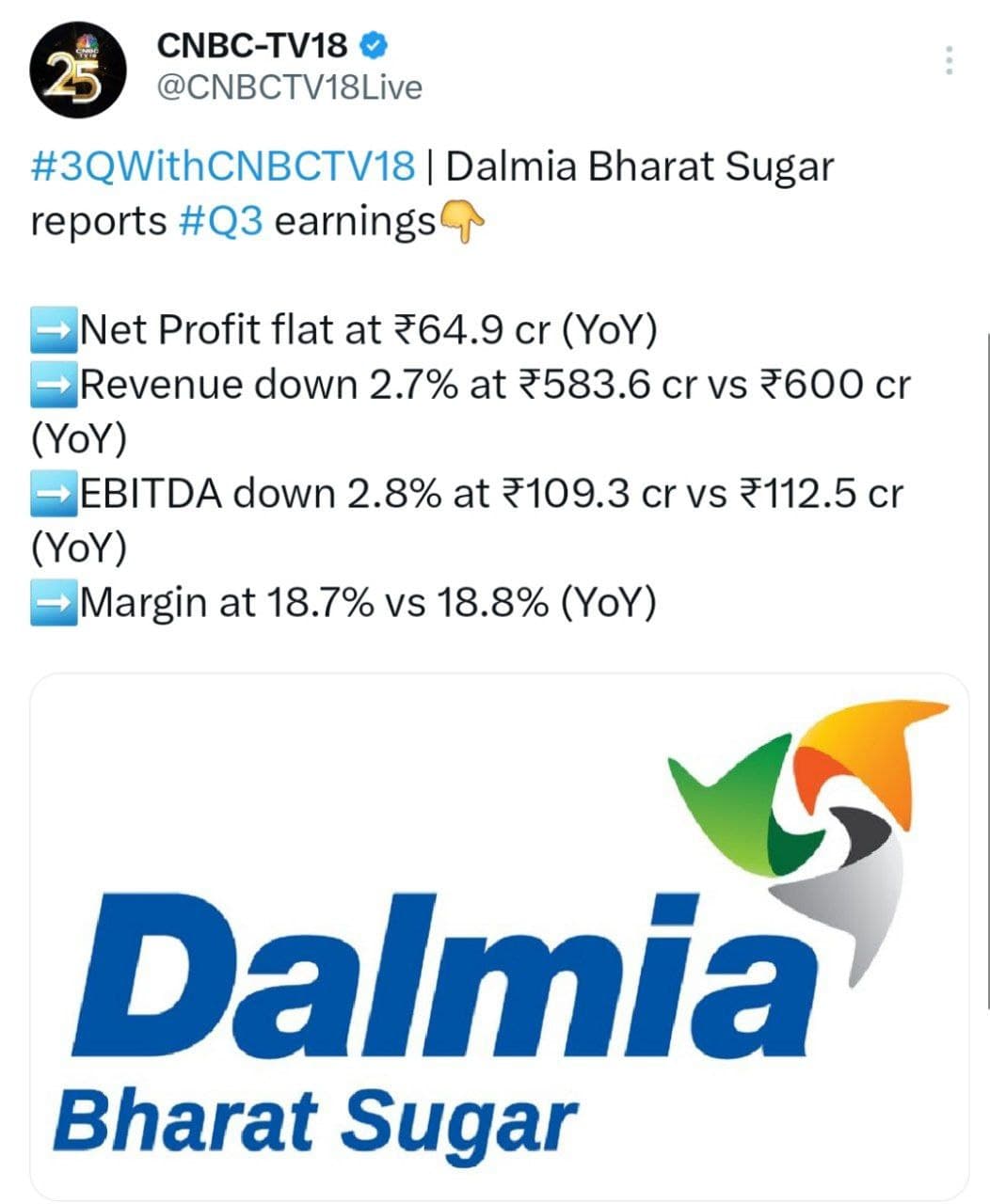

Might have to wait for Dalmia since it is fairly valued. But Dhampur Bio Organics can go a lot higher if @Aarti Ma’am’s prediction of Rs 3 reduction for every 0.1% recovery improvement is correct.

@Aarti Ma’am: Can you provide the source for the above stat?

@MANU_JINDAL

Good analysis done by you. While the numbers add up - which is evident by increase in recovery, increased cane crushed by 3% and high sugar and ethanol stocks, it is not reflecting in share price - this is only due to poor representation by the company (CFO). Even as per my estimates minimum share price should be Rs. 230 - 250 price in 6 months.

Regarding the recovery-cost calculation:

If cost of cane is Rs. 350 per quintal, if recovery is approx 10% then sugar production is 10 kg and cost of sugar is 35 (350/0.10) and if recovery is 11% - cost of sugar is 31.8 (350/0.11) so 1% improvement in recovery is Rs. 3.2 reduction in cost. In fact if the numbers are calculated more accurately, then the total margin improvement is higher at Rs 1.4 per kg and not Rs. 1 per kg (after improvement in recovery and increase in cane cost to Rs 370).

With higher volume, higher margin will have a multiplier effect.

The MD is very good - explains all numbers in detail and has answers to any questions asked- shows that he is very hands on. This is the biggest comfort for me. In turnaround cases hands of MD / promoter is most important for success. The best decision was to postpone the new ethanol plant. I am sure with his focus on cane development, energy efficiency projects, pharma grade sugar, etc DBOL could replace Dwarikesh as the most efficient sugar company.

But the CFO is surely not doing a good job of good investor presentation - even in the concall he just reads out from the presentation which everybody has already read !! Nevertheless I see this as an opportunity to make money when the numbers improve and stock price appreciates.

PS - there is one more reason for the share price to remain depressed. At the time of split, Dhampur Sugar Mills price was Rs. 300. After 1:1 split, Dhampur Sugar current price is 250 and Dhampur Bio is 150 - put together it is 400. so investors are selling Dhampur Bio and keeping Dhampur Sugar as it is believed to be the better company - which may be true at the time of split but with the new capacities DBOL will be better than Dhampur sugar - they have one more plant (and higher crushing capacity) which means more command area and more sugarcane. Implying that share price should be 250. In times of mkt volatility i think it is a very safe bet.

Balrampur and Avadh will also benefit from better pest control leading to improved recovery (Uttam i am not tracking). While Balramur is fairly valued, there could be upside in earnings from further recovery improvement, and also the regular buyback of shares - this is a very prudent measure which all profit making sugar companies should do. it makes sense to buyback rather than give dividend as the companies are undervalued. They should in fact increase debt.

Companies like Triveni, Dhampur Sugar are fairly valued (may be little higher than peers - as they are more ethanol focused including grain based).

I am positive on DBOL sheerly due to the valuation gap - its operations have improved along with good capacity addition. Mkt will realise this by nxt quarter so till then it is wait for DBOL.

Expected PAT of 103Cr. in Q4FY24 seems highly optimistic because:

Tax rate was 13% Q4FY23. Will it be same in Q4FY24?

Sugar sales were 1.43 [from your matrix] in Q4FY23. Per latest concall, sales quota for Q4FY24 would be similar minus the exports opportunity. However, your assumption for the sugar sales is 1.77 in Q4FY24.

Bio-Fuel profitability will be suppressed in Q4FY24 compared to LY.

Sugar sale quota will be higher by 10 to 15 % as compared to last year due to higher production in Q4 and higher closing stock in Q3. However, profit for FY 24 may not be 190 crs - but will be upwards of 150 crs - if sugar realisation increase to 41/42 then it could reach 200 crs !! Q1 FY 25 will be much better than Q1 FY 24 due to better recovery - recovery in April/May is lowest due to warm temperatures but this year crushing will end a month in advance as crushing capacity is higher by 30% and cane is only 8% higher.

Lower ethanol (and so higher sugar production) has messed up the sugar sales/ stocks calculations - quarter wise. But on annual basis it will average out.

regarding your points:

Tax rate was 13% Q4FY23. Will it be same in Q4FY24? - tax rate in Q4 is lower due to the perculiarity of the business of production / sale mismatch. In Q4 FY 22 it was 17%.

Sugar sales were 1.43 [from your matrix] in Q4FY23. Per latest concall, sales quota for Q4FY24 would be similar minus the exports opportunity. However, your assumption for the sugar sales is 1.77 in Q4FY24. - as above

Bio-Fuel profitability will be suppressed in Q4FY24 compared to LY. - will be more than compensated by higher profits in sugar

Its a pity these aspects are not explained in the investor presentation/ concall.

Triveni has also deferred their distillery expansion… going forward sugar companies will think many times before adding ethanol capacity !!! it is better to have sugar refining capacity and go for exports when international prices are high AND govt allows exports.

Uttam Sugar Q3 FY24 Results. Very good Results due to higher realisation from sugar sales.

Revenue Rs 517 Cr Vs Rs 471 Cr (Y-O-Y), Rs 604 Cr (Q2)

Margin Improvement. (Y-O-Y) despite RM cost increase

EBIDTA margin 14.66% Vs 11.26% (YOY)

PBT 11.27% Vs 7.47%

PAT margin 8.36% Vs 5.5%

Sugar Inventory 11.76 L Qtls valued at Rs 35.2 per KG

performance of sugar companies is difficult to compare on quarterly basis. Q3 numbers will depend on when crushing starts. Q4 is the only quarter which is comparable - best is annual comparison.

After Q4 numbers, share prices of all sugar companies should improve… after elections ethanol allocation will be restored and then we can look at huge upside from current prices.

we are missing out the CBG opportunity - if Reliance and Adani are setting up hundreds of CBG plants the first input will be spentwash from sugar mills. this will give good income (and no cost) for sugar companies. also budget has given subsidy for transportation of biomass (which includes spent wash).

Not sure how much of this ISMA report is accurate, looks like Maha has already crossed the 6.5M production estimate from earlier.

It’ll be difficult to expect sugar companies to manufacture & store cane juice, esp when food secretary refused any cane diversion this year 3-4 days back. I’m thinking distilleries will by & large be idle this sugar year except for some C-Heavy (which is miniscule vs total ethanol output last year) and grain prices have gone up.

Diversion can be expected only next sugar year when Govt has good handle on sugar stocks

I think govt. may reconsider by end of February when Maharashtra picture is clear. Even if they allow cane diversion from March onwards then distilleries can run on juice till April/ May and then on stored molasses till May/ June - so at least a few months of utilisation.

Nobody is benefiting from govt’s decision - apart from the fact that retail sugar prices are lower by 1 or 2 rupees - sugar is anyway a tiny part of the household expenses… grains are more important whose prices are going up !!

Dhampur Bio is converting existing ethanol plant to dual feed. To my mind this is the best thing to do at low capex of 50cr (funded 75% by soft loan). So full cane can go for sugar which is at higher margins and utilise the idle ethanol capacity using grains. Give the company another 6 to 9 months and performance will be among the best - EPS will double to Rs. 25 (annualised) and min share price 250 ( 70% upside).

Disclaimer - Please note this is not a recommendation to invest.

Balrampur Chini’s results were very good. Q4 will be even better taking the annual EPS to 31-32 levels. Hopefully they will come with buyback again next year which can take the stock back to 500 levels!! ( Disclaimer - Please note this is not a recommendation to invest.)

Next year all sugar companies will do better due to restoration of ethanol. FY 25 will see sugar as one of the better performing sectors. Risk-return is quite favourable at current prices.

Raw material for polylactic acid is Sugar. Wouldn’t this be vulnerable to govt directions to restrict sugar usage in case of production shortfall…thus risking the project in such a period.