it is in fact the opposite - going forward sugar industries will be derisked from govt policy flip-flops through bio-chemicals which use sugarcane based inputs cannot be controlled by govt - only cane price is out of the control of the companies. But if govt increases cane prices too much then sugar industry will shut !!

Govt can control cane prices, sugar quota and ethanol prices (thru PSU oil companies) and also molasses levy but cant control bio-chemicals. Sugar companies will control sugar production by balancing other products…

Sugar sector is going to be on upswing for next few years.

Govt. policies are not helping at all. If ethanol was to be stopped then the should not have encouraged sugar mills to set up ethanol plants (and take debt). they could have carried on with the way they were in the past.

Standalone grain based ethanol are sub-optimal and govt is promoting them - must be some political gains. but they will not be able to do well due to high grain prices. BCL industries is already showing decline in margins.

Hi, any idea on recent 26% stake acquisition of Sir Shadi Lal by Triveni Engineering?

It has huge land bank worth 800-900crs but marketcap is just 200crs. There are talks that the other promoter may use white knight option and bring a new partner (Renuka etc) to challenge Triveni.

they mentioned UP based co.s to have. Higher production by 6-7% where as co. Based in South (including Maharashtra) seeing production decline of nearly 2-3%. And on other side they degraded Balrampur chini… there analysis were not that much clear…

With elections round the corner and due to farmer’s protest, the government has increased FRP to Rs.340/quintal. Can anyone share the impact of this on sugar industry and it’s long-term impact on sugar companies??

The increase in FRP is for next year. By next year Govt will increase MSP and anyway market prices will be higher due to expected reduction in sugar production next year. Sugar companies should not be impacted.

Further, FRP increase is going to increase costs for mills in Maharashtra and Karnataka only as they purchase as per FRP. Other states have SAP which is already higher then FRP.

Sugar companies will benefit from grain based ethanol as Govt is ensuring supply of maize at low cost for ethanol production.

Which companies produce maize based ethanol today?

Why would the sugar production remain low for next crushing season or do you mean to say the current crushing season ( and hence some quarters of next year)?

sugar production will surely be down next year otherwise govt. would not have taken stance of no diversion when sugar production surplus expected this year is good (after stopping of ethanol).

Govt wants to meet the ethanol target through mazie - maize prices have already shot up. in a few months time they will realise that not much ethanol has been produced from maize and prices have shot up !! High maize prices will increase rice and wheat prices also.

But ethanol reduces imports and saves on forex.

Globally ethanol is mainly produced from sugarcane as it is most efficient land and water wise (based on per liter of ethanol produced). Govt. should not have stopped ethanol production - no sugar mill will set up additional capacity instead they will try to set up bio-chemicals like Dhampur sugar already has and Balrampur’s recent bio-plastic project, etc. Triveni, DBOL, Balrampur and others have cancelled their ethanol expansions. In a way it was good as bio-chemicals are more sustainable in long run and can also lead to rerating of the industry.

any one tracking this? @fundoo have you seen this white knight strategy before ? how do you think it plays out? if acquired is it indicated that the acquirer plan to liquidate excess assets and return cash?

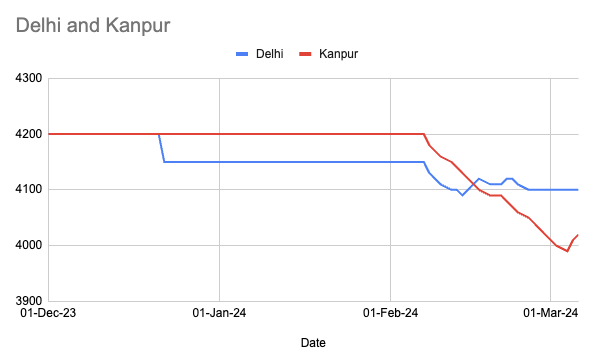

Any idea on sugar prices…

what i have found out it sugar prices had gone down in Feb but are going up again in March. Wholesale prices in UP more than 40/ kg and increasing small amounts every day… likely to reach 42 by march end.

Anybody has more information?

Inspite of all efforts of Govt to suppress sugar prices, they are increasing. As per traders wholesale price in UP is going to increase 42/kg (5% increase) by end of March and by Oct it could reach 45. Next year it could even go higher. Sugar supply is low for next 2 years. International sugar prices are going to stay at USD 600 plus levels.

Ethanol from grains will be possible but that too at low margins. Grain based ethanol companies like BCL could go into losses also.