Sugarcane production has gone up in UP - due improved acreage and yield. last year planting was up 7% in UP. Overall sugar recovery has also improved by 0.5%. Dhampur bio has increased crushing caparity by 30% from 22,500 to 29,000 tpa - this will not only help it crush about 10% more cane than last year but also finish crushing earlier by March instead of April /May - this improves recovery rate in last month of crushing.

At current sugar prices mills are ok making either sugar or ethanol (in fact sugar is better) but sugarcane supply is limited and they have to optimise. Govt may not increase ethanol as prices of sugar are surely going to jump once crushing in Karnataka Maharashtra stops in Feb / March - a month earlier than last year.

Share prices will keep keep fluctuating based on news like ethanol ban, etc but Q3 results of all UP sugar mills will be very good and Q4 will be best ever. Since these companies are undervalued they are going for buyback - Balrampur, Triveni and now Dhampur Sugar. I am sure Balrampur will come with another buyback by March/ April. Dhampur Bio also should come with buyback around that time.

Another question to you (considering your in-depth expertise) and to the broader audience is while reading Dhampur Bio Organics AR, we get to know that the company has only invested in ethanol capacities for B Heavy Molasses

How is it possible to achieve the syrup based ethanol from B Heavy mollasses machinery? Is it that the production facility is the same along with the process, only the raw materials are different?

If this is the case, then don’t you agree that the government decision would have minimal impact here?

Same plant can be used for B Heavy / C Heavy and in DBOL’s case even for syrup.

Through B Heavy output is usually 25% higher than C heavy. Through syrup output is even more and quality of ethanol is better.

Govt. decision will have impact as through C heavy output of ethanol is only 4% sugar equivalent. However since sugar prices are high sugar mills will anyway make more sugar and less ethanol. This will impact sugar mills in Maharashtra more where sugar prices are lower due to lower quality sugar output and hence they prefer to make more ethanol.

UP based mills will make good profits for next 2 years. You just have to wait for the results to come…

Convert entire Can Juice to Ethanol: Output Sugar “0” and High grade Ethanol " 78 Ltr.

2.Convert to Sugar and use B-heavy molasses for Ethanol (Normal case or current trend in industry) : Output 101 Kg and Medium grade Ethanol "21 Ltr.

3.Convert to Sugar and use C-heavy molasses for Ethanol : Output 116 Kg and Low grade Ethanol "10 Ltr.

Do anyone have any inputs on Bajaj Hindustan Sugar Ltd. ? Was the recent run backed by some developments (a month or so ago). Basis technical it was looking promising some time ago! Would be good to hear out on thesis/ antithesis pointers if anyone is tracking or had studied lately.

Output is higher as crushing capacity in mills has increased over the years. so output every month will be higher.

But the real picture will emerge when the crushing in mills of Maharashtra stop… which i anticipate will happen a month earlier this year… thats when prices sugar will jump…

Also with lower recovery at 9% in Maharashtra their cost of production will be much higher this year.

Agree… sales appear bad. but it is mainly due to lower sugar sales quota (from govt) as they had very low stocks at end of last quarter. next quarter (Q4 FY 24) it will be much higher than Q4 FY23.

overheads costs are fixed so margins are lower this quarter.

cane crushed appears to be 3% higher (cost of raw material - 532cr) which has gone into inventory (353cr).

concall will clarify these things…

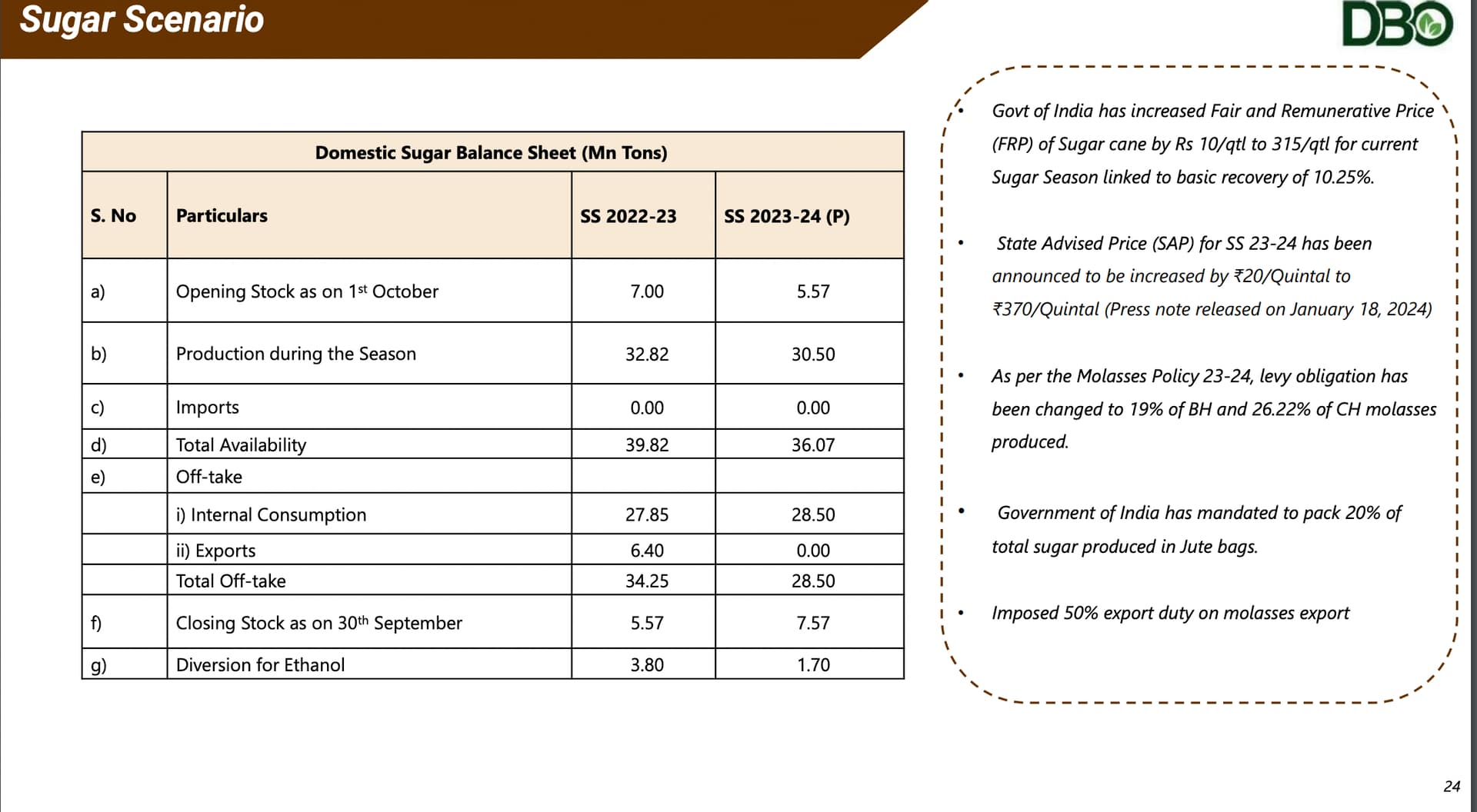

The Uttar Pradesh Government has recently raised SAP for sugarcane by Rs 20 per quintal, surpassing the market’s expected increase of Rs 15 per quintal. This move resolves the last major uncertainty in the sector.

Despite this, the sector has already factored in all the negative aspects. Currently, stock valuations are below one standard deviation from the average of the past three years, yet they maintain respectable ROCE of over 15%, even under challenging conditions.

The combined effect of two factors might balance each other out: (a) the additional remuneration for C-heavy ethanol and Maize ethanol at INR 6.87 and INR 5.8 per litre respectively, as announced by oil marketing companies in early January 2024, and (b) the SAP increase of INR 5 per quintal, which was more than anticipated.

Balrampur and Triveni are at less than 10x FY26 consensus estimates.

Govt. doesnt want to take a chance - as the production could be lower and so closing stock estimates can end up being wrong and sugar prices can shoot up. Only when Maharashtra mills stop crushing in Feb/ March when decision on ethanol will be taken.

As far as farmers are concerned they are quite content as SAP has been increased by Rs. 20 (industry was expecting Rs. 25) and sugarcane is the most profitable cash crop today.

Regarding Dhampur Bio - the stock has reacted negatively because the numbers are not presented well. Points to note for Q3 numbers:

Recovery has increased by 0.82% - this is big jump. I was expecting a 0.5% improvement this year and 0.5% next year. Company has done very well on this front.

Cane crushed is higher by 3%. Hopefully this will increase to 10% by March.

Sugar production has increased by 35%. Ethanol has come down.

Sugar realisation is > Rs. 40 per kg (at this price sugar has higher margin than ethanol)

Sugar and ethanol stocks are higher than last year. Sales was lower as per quota alloted. This could turn out to be better as prices are expected to increase going forward due to higher cane prices and expected early close of crushing in Maharashtra.

(I think the CFO should do a better job at presenting numbers - that too after they have appointed a Investor relations advisor !!) Information on C Heavy ethanol is missing. (there is lots of info which not captured…)

Recovery rate is the best metric to analyse a sugar company as that is what contributes to margins. Other factors like plant efficiency does not matter much now as all the mills have upgraded or are in the process of doing it over next year.

As per my estimates, Balrampur Chini, Dhampur Bio, Awadh will perform better as there is room for improvement on recovery and also efficiency. Sugar-ethanol mix for these companies are ideal ad also the single plant sizes are in the range of 7,000 to 10,000 tpa (crushing capacity). Companies like Dhampur Sugar, Triveni are already fairly valued and there is low scope on improvement on either valuation or financial / operation performance. Even ethanol capacity for these companies is on higher side.

Dhampur Bio call yesterday was informative in many aspects:

With SS22-23 as base year, Govt has flexibility to play with 10+ M Tons of sugar (export 6.4M, syrup/cane juice diversion 3.8M) to ensure lack of cane doesn’t result in less sugar (and hence sugar price rise). It might be even slightly more as B-Heavy molasses conversion to ethanol has also been “banned”, but offset by “1.7M Ton cane juice” allowed for ethanol conversion.

Management doesn’t expect sugar price to go up a lot even after elections.

Dhampur Bio recovery set to improve ~0.85% more vs last year due to higher crushing (they were guarded about numbers) and disease cleared from last year.

No expectation of more cane juice conversion even next sugar year.

My take-aways:

Dhampur Bio recovery improvement might offset the rise in input cane cost from UP SAP increase.

Profitability (high essentially due to cane juice/B-Heavy ethanol from last 2 years) to be muted for all mills in SS23-24 & SS24-25, might be offset by Govt raising minimum selling price of sugar if profits gets too low and mills can’t pay farmers on time.

No run-away sugar profits either this or next sugar year (as @Mehnazfatima foresaw).

Govt may be willing to take a hit on EBP even next year, or with enough stocks allow EBP at the cost of sugar exports.

Sugar mills profitability were because of both exports and EBP in previous years.

Any gains after 2 years will be based on betting on mills that will/are:

a) improving crushing capacity + cane availability (Dhampur Bio)

b) have spare distillery capacity + cane availability (Dhampur Bio, Dalmia)

c) have spare multi-feed distillery capacity (Dalmia)

Looks like Dhampur Bio may be a good potential turn-around candidate.

Agree, DBOL concall was very informative about the company and the industry.

Few key points:

Cost reduction : Increase in recovery rate (by 0.9 to 1%) will more than compensate increase in cost due to SAP price increase. As 0.1% recovery increase translates into cost reduction by Rs 0.35 per kg of sugar so due to 1% increase in recovery cost will come down by Rs. 3 and cane cost will go up by Rs. 2 so effectively margin will increase by Rs. 1 per kg. So on 4.5 lac ton sugar it should be Rs. 45 crs.

Revenue growth : Sugar prices will not jump but will increase to the extent of SAP increase ( which implies by Rs. 2 /kg) - even if Re 1 increase in price of sugar will translate in Rs. 45 cr for the year.

Cane crushed for full season will be 5 to 7 % higher than last year

So all in all, DBOL profits should be at least Rs. 100 cr higher than last year - on account of recovery improvement, cane volume increase and sugar price increase. Even if sugar prices dont increase the increase in profits will be Rs. 50 crores. Post depreciation increase/ other costs annual profit should be 150crs - EPS of 23 which is similar to Dhampur sugar). At a PE multiple of 10, fair value should be Rs. 230.

Further, if they convert the ethanol plant to dual fuel and maize is available at reasonable price then ethanol volumes and profits will be higher.

It was raised in the call, management said their board will discuss about the paused ethanol plant or converting current plant to multi-feed, but I felt they don’t see the economics of it currently as maize prices apparently have shot thru the roof after govt recently notified maize based ethanol price.

Dalmia have paused their Nigohi grain distillery plant (250 KLPD) which was supposed to come on stream in another 7-8 months. Dalmia is the best run sugar company (biased personal opinion), their next expansion is only in FY27, bringing on a new mill in UP acquired recently. But stock in my opinion isn’t under-valued, and if its upside is worth all the aggravation in this industry.