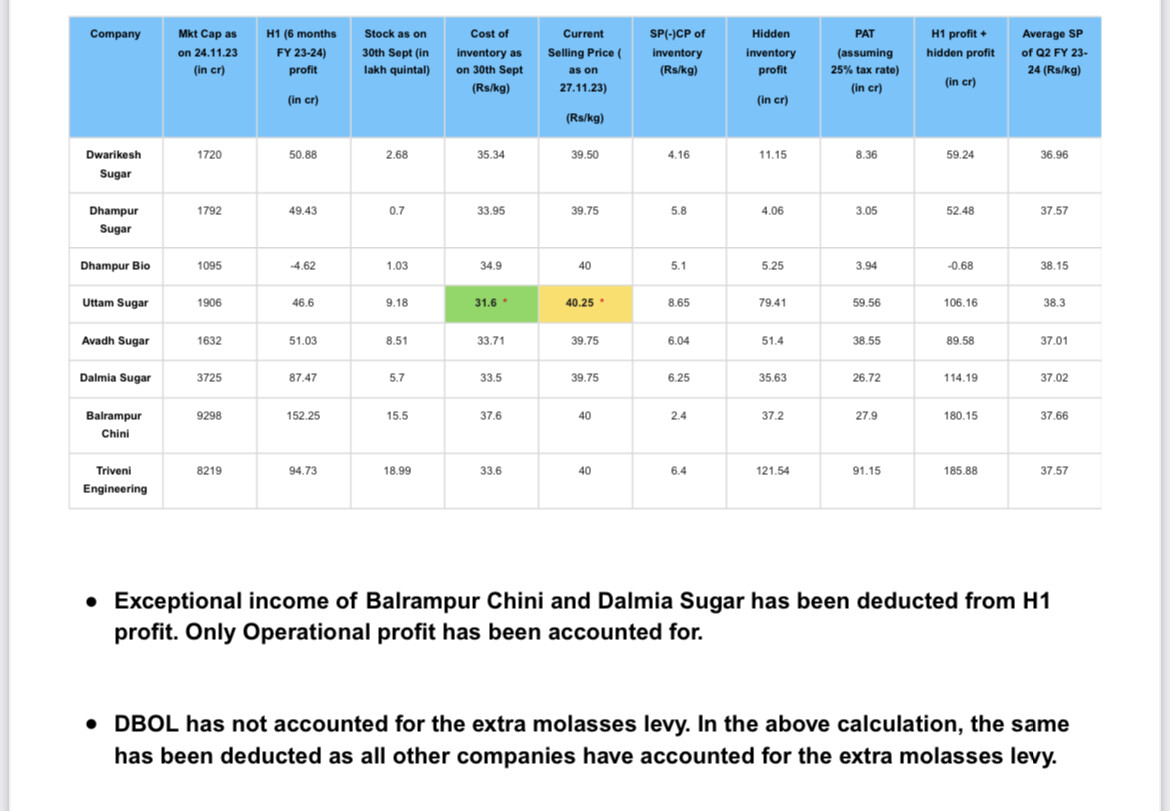

Source: Uttam Sugar presentation

Source: Credits Aman Sonthalia

Crushing capacity

Dhampur Sugar - 22,500 TCD

Dhampur Bio - 29,500 TCD (increased from 22,000 TCD last year).

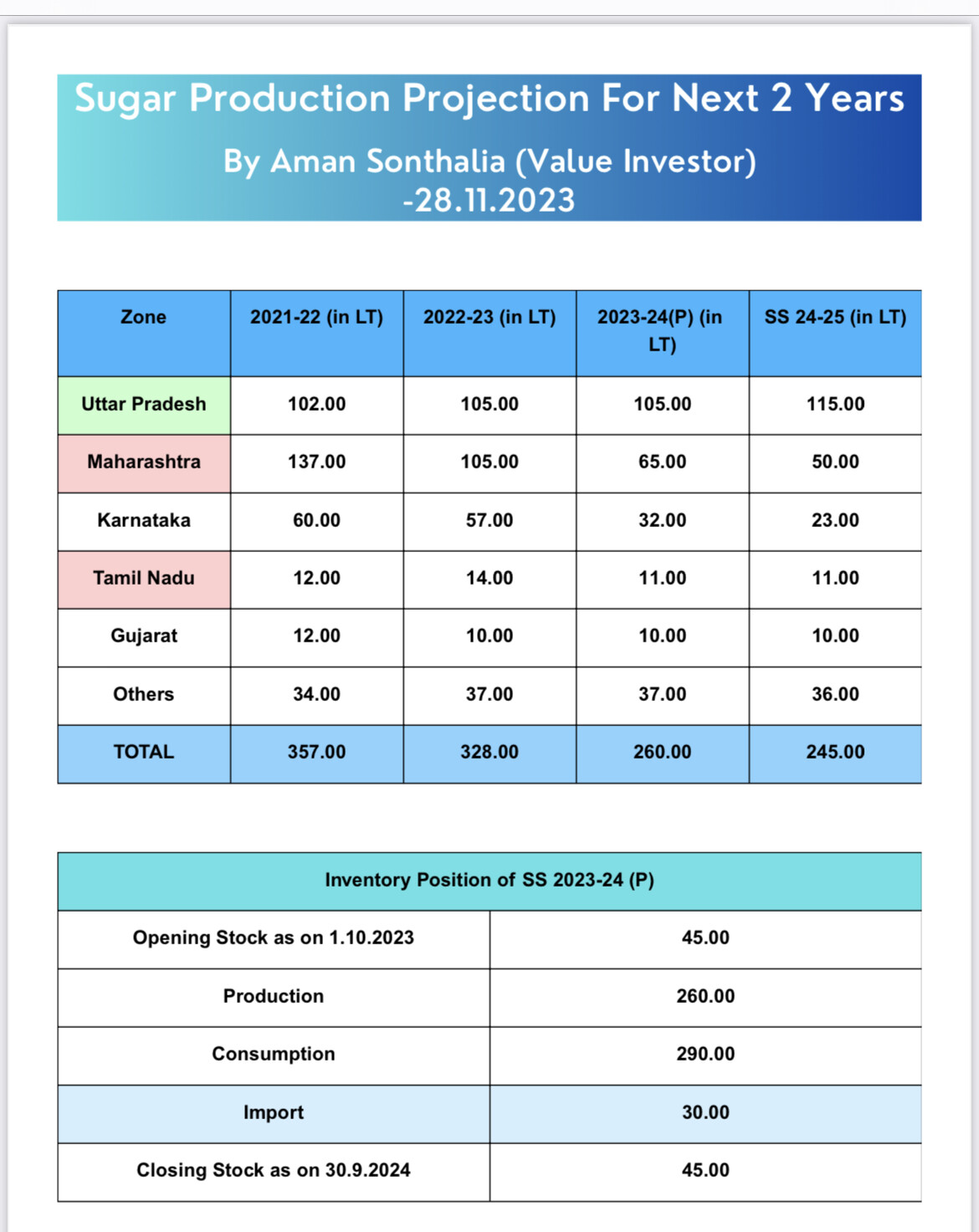

@Donald : What’s the confidence level for the Production Estimates [SS 2023-24] of MH as they seem way low when compared to ISMA’s projection? What kind of and how wide ground level checks were done to arrive at this conclusion?

Again as mentioned in posts, source credits are due Aman Sonthalia.

Discl: I am a learner here. Everything I have been posting here is learnt from the Sugar Specialists - but have questioned them hard - logically, and from datapoints.

So couple of pointers here from my side on your specific query:

We should ALL focus on getting to do our independent scuttlebutts now to confirm or deny above scenario being pointed to us by Aman Sonthalia.

Let’s keep asking folks we know/and their friends on ground reality in MH and KA, and keep reporting back here! That will be the right way to take things forward.

@Donald Sir, On one side there is Sugar shortage is being estimated and on the other side sugar cane is being diverted for ethanol…

What will be the impact on ethanol processing units… government will not allow diversion of sugar for ethanol as one of the reason for diverting ethanol to sugar was to absorb excess sugarcane. Profit from Sugar can get neutralised by under utilisation of ethanol plants of Sugar mills…

It’s a good question

Will work further on this, thanks.

@Mehnazfatima ?

As received from another sugar specialist friend

The only risk is disease and weather. For that, diversify amongst mills, don’t bet on single company!

Ethanol production will surely come down as Govt. will not increase ethanol rates this year - to prevent sugar prices from going up too much. Mills will first maximise sugar production and then remaining cane/ molasses will be used for ethanol - so ethanol capacity of all mills will be underutilized. Sugar will more than compensate by better margins.

Overall profits of UP based sugar companies will jump for next 2 years. After that ethanol will be used to balance excess cane production if any.

As the cyclicity of the sector is no longer going to be there it could lead to rerating of the sector. However mills focusing on cane yield & recovery and efficiency of mills will benefit rather than cos setting up ethanol plants (as margins are higher in sugar !!).

Dhampur Bio is going to be the dark horse in the sector:

Mcap of company is about 1,100crs and it is going to make profits of 350crs in the next 2 years!

Sugar is a highly regulated industry where every thing is regulated and controlled by the Governemnt and if some thing is presently out of purview than government can bring them under control at any time. In sugar Industry, Government controlls

input cost, Selling price, how much inventory you can hold, how much you can sell, how much you can export etc etc…

We should be very circumspective while calculating super profits for sugar mill. Government will never like/allow sugar mills to make money. Political parties want to serve their vote bank by providing additonal benefits to farmers who are their largest vote bank. If sugar mill are making extra ordinary profits then government can increase the FRP on sugar cane price even from retrospective date also …

Its very difficult to predict with certainity 2 to 3 year scenario in an industry which is highly regulated…

In my opinion Ethanol push was also mainly to absorb the excess inventory of Sugar so that cane arrears of farmers can be cleared easily… now the scenario has entirely changed and we have reached from excess sugar to sugar deficit and in my opinion ethanol has never been a viable proposition.

India is a water starved nation and Sugar cane is a highly water guzzling crop and it hardly makes any sense to promote growing excess sugar cane and divert it for Fuels…

There are many mills which still have cane dues to pay. Farmers and Govt. both have realised that price is one thing but they should get the money also !! a few weeks back farmers were protesting at a govt mill in UP for paying cane dues !!

For the sector to survive Govt has to take balanced view. Sugar companies have already put new ethanol plants on hold due to inconsistent ethanol policy.

The sector has to go the Brazil way or else it will not be good for farmers - sugar cane is the most profitable -low risk crop in India.

Dhampur Bio’s decision to postpone the ethanol plant is the right strategy as Govt is not increasing the ethanol prices and sugar prices are going up. As DBOL cane availability is increasing they have increased cane crushing capacity for making sugar. They are sitting on surplus cash as ethanol capex was postponed.

Their sugar recovery rate will be better (like in the case of Balarampur). DBOL will be the best performing sugar company due to the right capex and cane strategy.

Sugar companies in general will produce less ethanol this year. DBOL revenue from ethanol will be <10% this year.

In ESY 2023-24, no ethanol from sugarcane juice and B-Heavy will be procured by OMCs with immediate effect. Ethanol from C Heavy will be encouraged.

This decision by Govt takes care of sugar shortage, in the sugar season 2023-24.

No wonder, sugar stocks fell today.

there was no reason for sugar stocks to fall as this notification will have no impact on sugar prices. Sugar companies were anyway not using B-Heavy route this year due to:

This if true, is a huge REVERSAL in Policy - and a blow to the Structural story of Ethanol - and GOIs avowed claims of moving progressively and speedily towards clean, green energy!!

@Mehnazfatima Please point to the source of the news (as far as I know this has NOT yet been published, but is based on leaks to media).

Assuming above is true, and gets published in the next couple of days, I had some observations/questions:

That such a step is being taken points to (a ground study having been completed) the fact that actual shortfall on the ground is indeed likely to be BIG - belying ISMA claims; and is probably under compulsion of election-year policy-making

Direct IMPACT of this on the Sugar MIlls (not being able to produce Ethanol thru B-Heavy and Juice routes) will be in higher Working Capital requirements (to the extent of non-diversion)

Sugar prices may fall by Rs 1 or 2 per kg in the short term, but very likely to reverse once MH and KA Mills production falls as expected

Since Sugar prices will still make for profitable operations, why won’t Sugar Mills stop making Ethanol for SS 23-24, continue to make Sugar in order to maximise profitability?

Besides Ethanol thru C-Molasses route (in the course of normal sugar production) should continue to be taken in by OMCs; in fact there is a case for C-Molasses Ethanol to be priced higher by Government now (to incentivise more sugar production and thus reduce the likely shortfall)

Meanwhile Grain based Ethanol production may be suggested/incentivised as the way forward (primarily through Maize route, as otherwise there is shortage)?

In balance, there shouldn’t be any/much impact in profitability figures for UP Sugar Mills (with better financial strength).

Rather it’s a case of sentiment turning worse (which is equally important for investment thesis) for the Sugar Sector (and actually for GOI avowed policies - that these can be reversed anytime by this government !!).

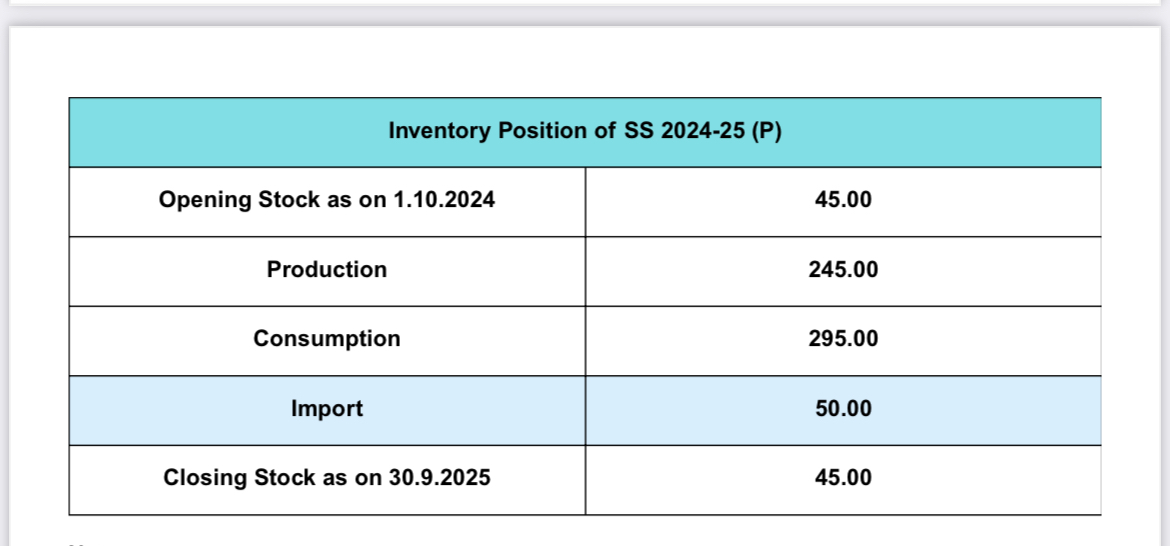

The govt also has additional lever of stock control limits to force mills and stockists to flood the market and hence drive down prices. This might work in a normal or near deficit scenario, but with the kind of deficits forecast even in conf calls (Balrampur, DBIO) for SS24-25 - while prices might go down in short term, but lower residual stock might trigger higher sugar prices further.

Maybe with the leak, govt is either testing the waters or it’s a short term decision till crushing is half-done and then may be reversed/extended.

The way Namo Govt has managed the sugar sector is exemplary. It can be taken as a case study in sectoral management …win win situatiin…keeping both farmers and mill owners happy.

There is a huge increase in sugarcane productiin and also a huge increase in ethanol procurement by the OMCs…and the price at which ethanol is procured is almost at sugar selling price parity.

We are expecting a shortfall in sugar production of just about 1.5 million tons. The govt has already banned sugar exports. A moderate tilt in production of sugar vis a vis production of ethanol will ensure that sugar price remains stable and there is no sugar deficit.

Those who are betting on sugar sector upcycle are basically betting on bungling of this sector by the Central Govt…that too in an election year.

Given the track record of this Govt in handling sugar sector, i do not think that its a good investment betting against the govt. A sugar deficit of just 1.5 million tons is not such a big deal…this govt has effectively tackled sugar deficit of 6 million tons and a sugar surplus of 8 million tons in the last 8 years.

I found this news article. A setback for sugar mills who invested in ethanol plants.

https://sg.finance.yahoo.com/news/india-plans-discourage-ethanol-production-172903058.html

In case of doubt, it better to look at the long term charts of the leading companies in the sector to find out if there is sectoral turnaround.

Stock prices of many companies turning bullish from a very similar technical set up …all at the same time is the surest indication of a sectoral uptrend.

In sugar sector such a thing happened in early 2021…after that many frontline sugar stocks became 3-4 baggers.

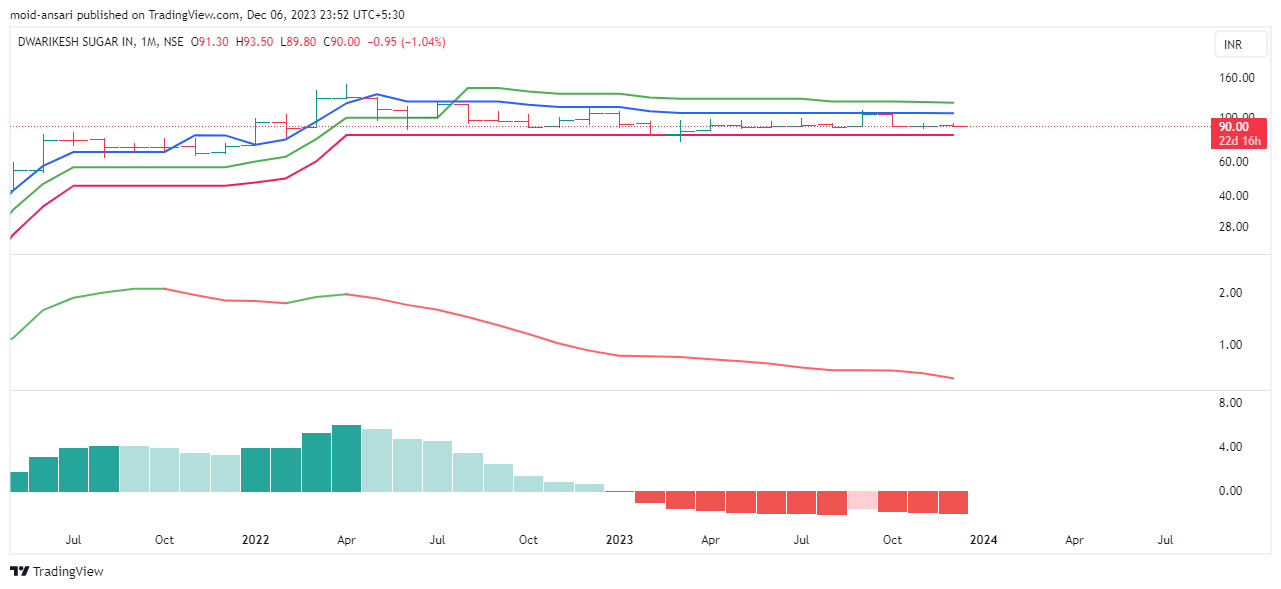

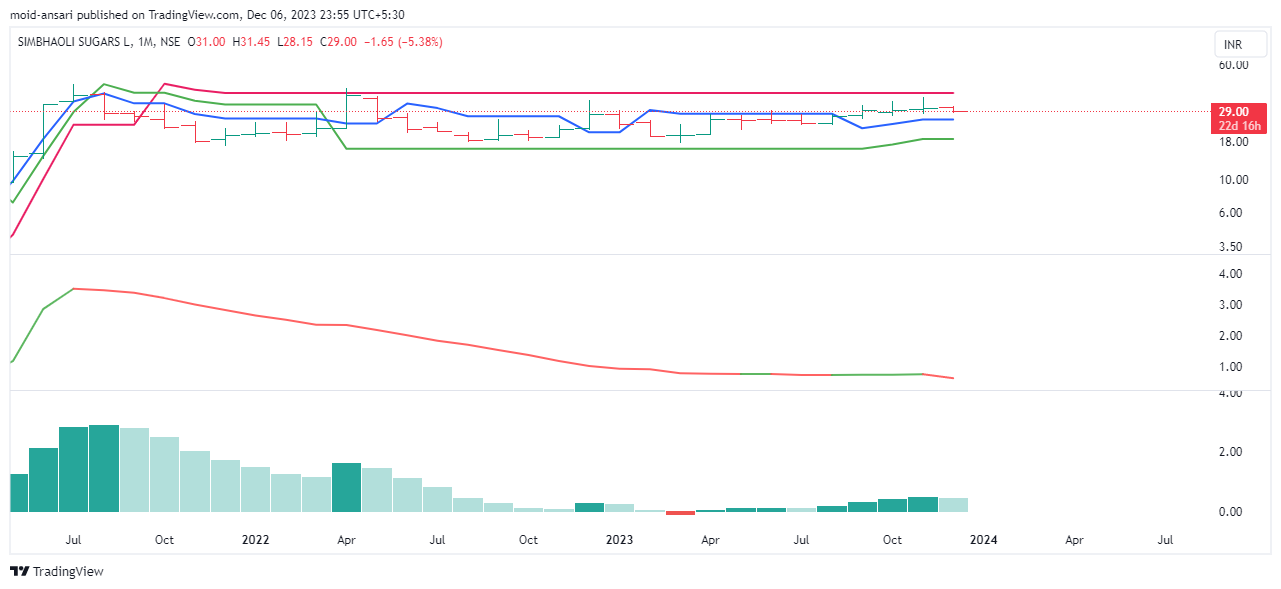

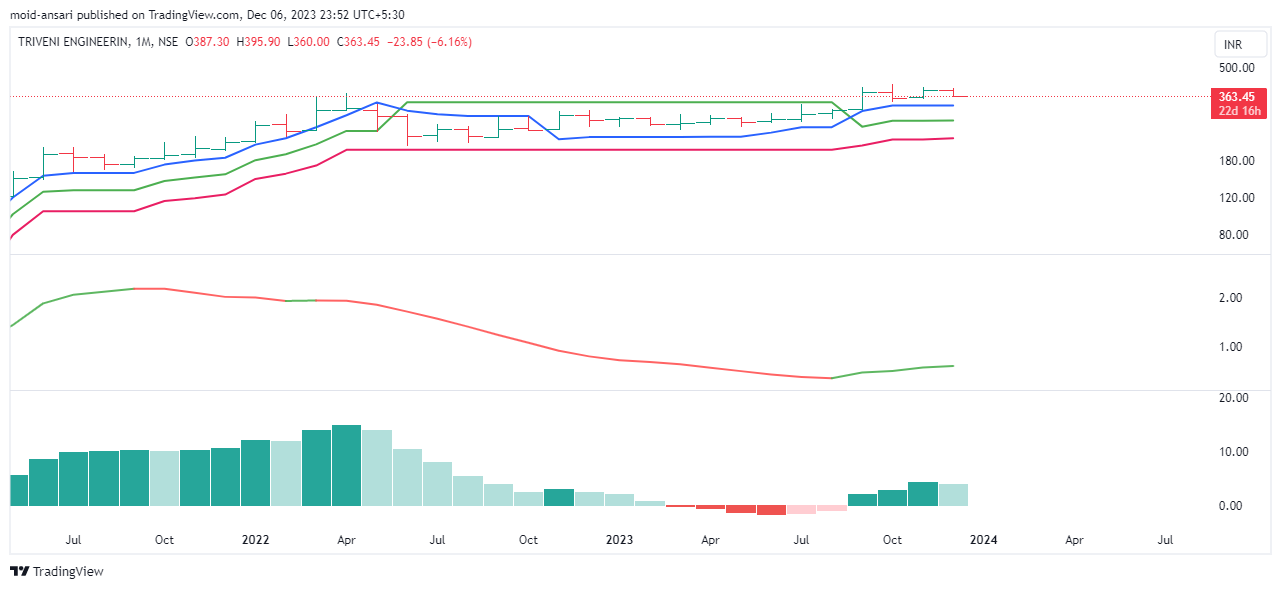

As of now, among sugar stocks only Triveni Engineering is worth making fresh investment.

Sorry to say this, but i do not find indications of sectoral uptrend in sugar stocks as of now. …long term price charts are an important component of my investment strategy for cyclical stocks.

Have a look at the monthly charts of the UP based sugar mills…as per my system only Triveni and Uttam are looking good

it is time to look at fundamentals…

sugar companies were anyway going to use C Heavy route this year as sugar is more profitable… this notification has no impact as sugar shortage will continue. the story has changed from ethanol to sugar… wholesale sugar prices will remain above 40 this year and 42 next year.

companies with higher sugar production will do very well. EID Parry, DBOL - they have less than 20% from ethanol.