Interview by Balrampur Chini MD today, even if EL nino comes, he does not expect anyimpact on production even in Maharashtra & south more than a marginal %, additionally he expects prices of sugar to move forward

Interview by Balrampur Chini MD today, even if EL nino comes, he does not expect anyimpact on production even in Maharashtra & south more than a marginal %, additionally he expects prices of sugar to move forward

no exports is going to restrict domestic prices (which can even go down) and there is huge risk on input cost due to reduced output of sugarcane and higher SAP - which is almost sure in an election year… i think all sugar stocks will correct 25%.

(Below data is taken from few sources and may not be very accurate)

Global sugar sector scenario:

Global production expected for S.S 2023-24 is around 175 MT compared to 177 MT during the current season.

Global consumption is also expected to be around 177MT leading to a potential deficit of 2MT.

Brazil sugar production is expected at 41MT compared to 31 MT last year.

Thailand production is expected to be reduced to 8 MT compared to 10MT last season.

The European Union is expected to produce 17 MT compared to 15.5 MT last year.

DOMESTIC SUGAR SECTOR:

S.season 2022-23 production ~ 33MT and 4 MT was diverted for ethanol.( Total 37MT) and sugar export of about 6.4 MT.

Opening sugar stock expected ~ 6 MT at the end of S.season 22-23.

Expected sugar production in India for the sugar season 2023-24 : 29MT and 4MT is expected to be diverted for ethanol production.(total sugar equivalent of 33MT)

Available sugar for next season will be ~35MT (29MT+ opening stock of 6MT).

Total domestic consumption is expected at 28MT.

Sugar export quota will be dependent on Govt policy which is expected to be announced in January. Considering the tight situation it’s expected that the Govt will restrict the export of sugar compared to last year.

Overall sugar prices are expected to remain firm.

The reason for drop in sugar production is due to potential reduction from Karnataka and Maharashtra states.

Discl: Not invested , tracking sugar sector.

Some Results will be out within couple of weeks from now. That is probably a better time to take stock

Domestic Industry data quoted (above) is likely Dwarikesh sourced/provided.

As per my current scuttlebutt work with some knowledgable folks in sugar industry, picture is probably worse;

Sharing for us all interested/invested in Sugar Sector to try and track the tight situation better by talking to more sugar domain folks

————---------------------------------------------------------------------------------------------------------------------

Domestic Sugar Industry

Opening 50L vs 60L T

Consumption 290 vs 280L T

Production 270 vs 290 LT

Opening Stock (270+50-290) = 30L T

So government will likely have to import minimum of 10-15 LT

40-45 LT min level has to be maintained as in Sep there is no crushing, and availability is only by End Oct or Mid Nov

————-------------------------------------------------------------------------------------------------------------------------

UP Sugar Company Updates

Dwarikesh, Dhampur, and Dhampur Bio better avoided.

a) New sugar units coming up near one unit of Dhampur and one unit of Dwarikesh and one unit of Awadh, so some acreage will be diverted to new players. Newer players also financially strong.

b) Dhampur, Dwarikesh, and Dhampur bio impacted due to heavy rainfall august and September

c) The other fallout of this excess rainfall is red rot disease has spread much wider (present in small pockets) in some parts of field crop due to the excess water flow. Yields and Recovery thus is badly impacted!

—————---------------------------------------------------------------------------------------------------------------------

Two of Uttam Sugar units is likely to be impacted due to heavy rainfall but least impacted by red rot disease, hence likely to make up shortfall due to a) higher capacity this season and b) excellent cane management (diversion/procurement)

——————---------------------------------------------------------------------------------------------------------------------

Awadh Sugar one plant effected but will be made up by other plants.

——————---------------------------------------------------------------------------------------------------------------------

Triveni Engg one plant affected badly by red rot. But other plants likely to make up. They will probably do as much as last year.

————-----------------------------------------------------------------------------------------------------------------------------

Dhampur bio Recovery rate is lesser and therefore RM cost/kg 2-3 Rs higher than other efficient players.

————----------------------------------------------------------------------------------------------------------------------------

Next SS forecast 24-25

El Niño Impact is predicted to be more severe. So UP based mills may be up for 2 good consequent seasons

Disc: Invested in Sree Renuka sugars from early 2021 till April 2023; shifted to Uttam Sugar in May 2023 courtesy this excellent VP Annual Conference Sugar Sector presentation; Studying Triveni Engg as another probably better longer-term sugar sector bet. Please do your own diligence before investing in Sugar stocks. Data may be good; situation is tight!

UP based Dwarikesh Sugar and Dhampur Bio Organics have pointed out negative impact of State Government order imposing additional levy obligation by treating both B and C Heavy molasses equally in recent Concall/Investor Presentation.

Dwarikesh has provided Rs 19.92 Cr as additional expenses due to additional levy order for the Molasses Year 2022-23.

Dhampur Bio Organics Ltd has not provided Rs 20.30 Cr on this account, since the matter is sub judice.

Dhampur Bio - promoters have bought shares from open market at Rs. 160. Last Nov also they had bought shares from market.

Company has increased cane crushing capacity (by 30%). As per concall they expect to crush 8% more cane this year. Extra capacity of 20% will help them crush cane faster and hence increase recovery (cane crushed in April/ May has low recovery).

They had commissioned pharma grade sugar plant few quarters back.

Ethanol they have postponed as margins in sugar will be higher for next 2 years. No capex no interest burden but higher margins through existing sugar capacity.

DBOL will be best performing sugar company this year.

An additional bit of information. They also mentioned in the concall was that they expect higher recovery of sugar in the current season as the crop is free of pest infestation unlike the last season.

What I have learnt is Cane availability for crushing comes out of acreage.

Acreage gets affected by many factors. This season is badly affected a) scanty rainfall till august b) excess rainfall in Sep (suspected will lead to lower yield and recovery) c) Red Rot disease spreading fast and wide in fields with excess rainfall flow contaminating fresh areas.

Cane crop is not a fresh plant every season. It is resprouted. So if one season turns out bad (rain or disease affected badly), it usually takes 2-3 seasons to come back even with good rainfall. SS2024-25 season is predicted to face a harsher El Nino effect (fir whatever it is worth)

Now add to these new plant coming up near a plant area - Government has to allocate some part of the cane availability to the new mills. As mentioned these are financially strong players - so they can easily lift their quota and actually try and divert more procurement their way (by way of influencing middlemen, which the stronger players always do around the financially weaker mills, I am told).

Anyone interested/invested in Dwarikesh - can do more scuttlebutt on this aspect to corroborate and/or demolish Management claims.

My reading is cane availbility for crushing will be at a Crunch in around factories which have more of these problems than those who face these to a much lesser extent (mentioned in above posts). Good to question in Analyst Calls coming up soon ![]()

How it pans out we will get more clarity by Mid Nov, and established by End Nov.

As per todays concall of Dhampur Sugar Mills, there will be some impact on cane availability due to new mill coming up near its unit. The new mill will start production from December. But the management was confident of maintaining its numbers even though there is some impact on cane availability.

Central and State Govts are two important actors in this business. How will they react in election year if yield (farmer earning) goes down? Which of these or all will happen?

As per our GOV guidelines the ethanol blending in fuel % will increase steadily. As more and more Sugar cos start making ethanol for this purpose, how will that effect the cyclic nature of the sugar industry?

In my humble opinion, the sugar cycle can be desribed in economic terms as the cobweb cycle / hog cycle.

The events which happened last year are more important for production next year.

The was deficit rainfall in August…and excess rainfall in September 2023…the issue is how will this impact the Sugar production in the present sugar season which has already started and in the next sugar season.

For the sugar production in the present season, the sugarcane yield may be affected to some extent due to water shortage and disease…but we must remember that sugarcane is a very very sturdy crop…the overall production does not get affected hugely due to the above adverse conditions…there may be a fall but it may not be more than 1-1.5 million tons.

Insofar as next sugar season is concerned, the planting in Maharashtra and Karnataka starts in March and end by May…the defining criteria for farmers is whether there is water available in irrigation reserviors in March…i think the excess /adequate rainfall in Sept 2023 will ensure that there is water availablility in march 2024 and may not lead to reduction in suagrcane sowing in March / April 2024 and hence the sugar production may not be in a huge deficit in the next sugar season too.

If there is a developing El Nino which may cause a drought in the monsoon season of 2024, that will in effect impact the sugarcane sowing in March April 2025…and frankly speaking its no use for retail investors to predict that long in a highly dynamic environment. I would rather let the market make its decision and follow the collective wisdom of the market in such cases. As of now the verdict of the market is that…there is no sign of bull run in sugar stocks or sugar price which is stagnant since 2017 @ 35 rupees per kg in Delhi wholesale market.

Still if anybody wishes to play the sugar theme, i think Triveni Engineering, Baja Hindusthan, and Dalmia sugar are good bets as of now…uttam sugar too is doing quite well but it has already run up a bit

International sugar price as reflected in Sugar 11 contract is very bullish and in uptrend…it can go up hugely to even 40-50 cents…but the Govt of India has shut out the the access to international market…otherwise, ISMA used to very cleverly overestimate the sugar production and force Govt to allow export of sugar …the Govt no longer appears to be falling for that bluff and ISMA is no longer bluffing about the sugar production estimates…but still i would scale down ISMA estimates by 1-1.5 million tons atleast

The impact of the output owing to meagre rainfall in Maharashtra shouldn’t be ignored.

Shortage of sugarcane, drought-like situation, the divergence of sugarcane for fodder and agitations by farmers for pending FRP will have a huge impact on Maharashtra’s 2023-24 sugar season which starts on Wednesday, November 1.

This year, 14.07 lakh hectares of total sugarcane area will be available for crushing and production of 88.58 lakh tonnes of sugar is estimated. The area under sugar cultivation has decreased by 6 per cent compared to last year. Last year, 211 sugar mills produced 105 lakh metric tonnes of sugar. Deficit rainfall in many parts of the State has resulted in drought-like situation and demand for fodder is on the rise.

Meanwhile, the Central Pollution Control Board (CPCB) has ordered the closure of 45 cooperative mills in the State for violation of the Environmental Protection Act. The sugar industry has expressed concern over these notices ahead of the beginning of the sugar season. The Sugar Federation in the State is gearing up to challenge these notices.

Meanwhile, the State government has decided to collect ₹10 per tonne from the sugar mills and give this amount to the Sugarcane Workers’ Welfare Corporation for the benefit of various schemes for the sugarcane workers, their families, and for the education of their children.

Thank you @Donald Donald. Would you mind explaining the impact on companies from other states ? Bring cyclical i still trying to understand this sector. I could see many sugar stocks had a good gains/Breakouts today.

Disc: not invested now or in the past ever in any sugar stocks. Still learning.

Thanks for putting me on the SPOT ![]()

Disc: I am invested. My views are biased. I am NOT the best person to answer this query.

I am observing, questioning & learning from sugar specialists like Aman Sonthalia presentation at VP (everyone must DIGEST this first to come on the same page), and recording data points as we experience first-hand. So I will make an attempt. But beware, there could be mistakes in my understanding and/or data points.

Would request sugar veterans like @Mehnazfatima and others to step in, correct as necessary, and educate us more.

A. Primary factor is Demand-Supply imbalance. When that is there prices rise, money is there to be made

B. Where Money is there to be made, depends on 3 aspects

a) Recovery Rate b) Inventory (low cost or not ) c) Crushing (in the district/near the mills, may vary across the state)

C. Highest Profits are likely to be made by Mill companies whose Production cost is lower - due to a) higher Recovery b) lower steam consumption (bagasse saving/reselling adds to bottomline c) more sugarcane availability/more crushing leading to higher economies of scale d) Low cost inventory sale (which probably gets liquidated in 2 months at start of SS like Sep and Oct (when ther is no crushing)

Having said that, let’s come to the specific query - India Sugar Shortfall SS23-24 impact for UP based MIlls

Sugar price generally falls at season start (Nov/Dec) when there is adequate/abundant production. This is because sugar production is over in 5-6 months, but sales are spread out over 12 months. During production mill owners have to pay out farmers, there is some liquidity crunch, so generally prices are kept low during this time.

This year there is shortfall not only in Maharashtra but also Karnataka and TN. MH and KA the shortfall is like 40% lower this year, and TN is like 20%. UP production will be marginally higher this year. After UP, MH is the largest producer, and then KA. (will try to get us state-wise production figures for SS 22-23 and SS23-24E, soon)

ISMA is saying Production will be around 290 LT in SS 23-24 (matching yearly consumption pattern). Ground checks are telling us it will be more like 260 LT, i.e. a shortfall of 30 LT

During Crushing period of SS 22-23 (last year), sugar price was 35.50/kg

Right now it is Rs 40-41/kg which indicates there is shortfall ahead

With this kind of shortfall, sugar price probably will NOT fall at season start and stay elevated for the season. Even if it falls by say Rs 1/ or 2/- now, it will be more than made up when CRUSHING gets over early in SS 23-24 (likely by Rs 5/-, so net Rs 3/). This is because

Crushing data points

If indeed there is shortfall of 30 LT, then government will have to import to meet the demand. Prices internationally are at 60-62/- per kg; domestically it is at 40-41/- per kg; Sugar Specialists are saying 40/kg can go upto 45/- kg

The sugar specialists are also saying Sugar Price will probably NOT fall from these levels for 2 years now, because

Next year SS 24-25 a) El Nino is predicted to be more severe b) Dams don’t have much water, water table is drastically down c) Planting to be done from Dec to May - MH and KN have less water

Sugarcane plantation in MH/KA is done of 3 types - 18 months crop, 12 months crop, and 9 months; 18 months “Adsali” plantation - for SS 24-25 season was to happen in July/Aug 2023 - when there was no water - so minimal planting; 12 months crop - there is less water; 9 months crop - less water; SS 24-25 sugar season will see big shortfalls

Sugar Mills in States producing more will make more, thus UP mills benefit

Inventory highest in Uttam and Avadh Sugar, and then Triveni Engg (inventory being sold now)

SAP (for Sugarcane in UP) likely to be raised by Rs 25/- per quintal which will impact cost of production by ~2.25 Rs/kg which may be easily passed on to the consumer

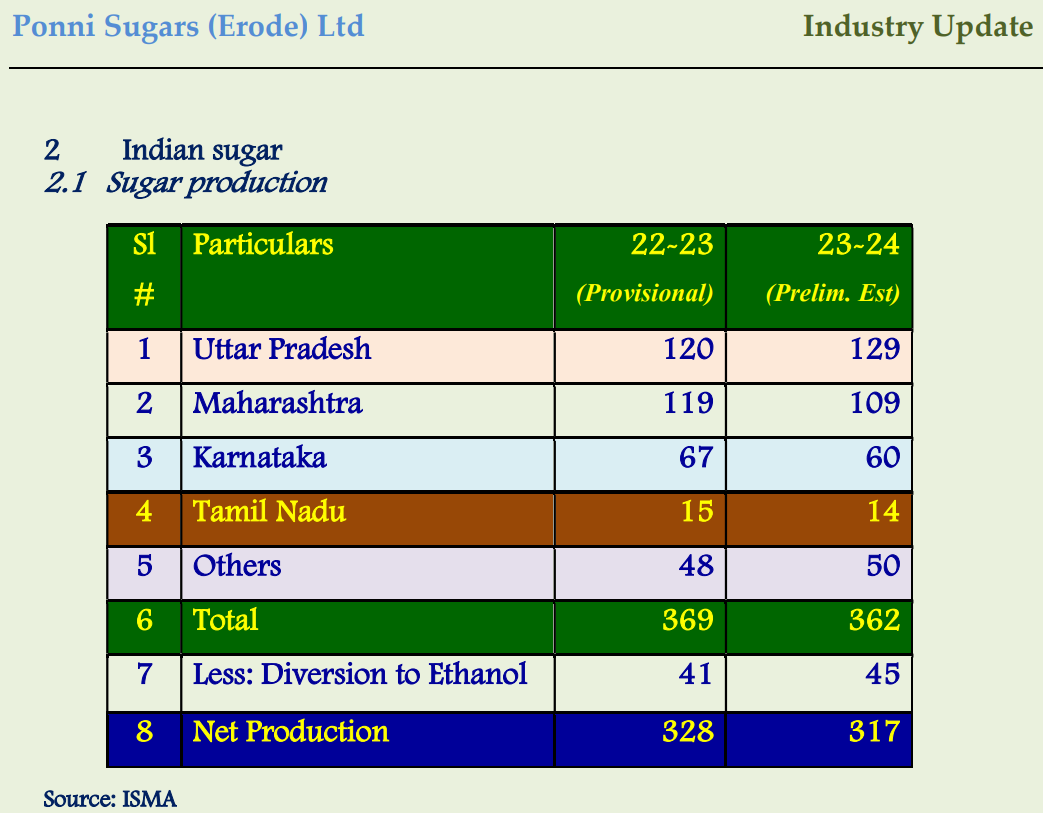

PONNI SUGARS provided the above for their November Industry Update:

Source:

https://www.ponnisugars.com/SiteImages/Announcements/35462652c60af37e7d15b5c7a91e680a.pdf

Listed and UP based Sugar companies (Collated Crushing Capacity from the public filings):

| Name | Cane Crushing Capacity, TCD |

|---|---|

| Bajaj Hindusthan Sugar Ltd | 136000 |

| Balrampur Chini Mills Ltd | 82000 |

| Triveni Engineering and Industries Ltd | 63000 |

| Avadh Sugar & Energy Ltd | 31800 |

| Uttam Sugar | 26200 |

| Dwarikesh Sugar Industries Ltd | 21500 |

| Dhampur | 15000 |