This article argues that given better margins and high sugar prices, “cane-based distilleries are more likely to process ethanol from B-heavy and C-heavy molasses, and not directly from cane juice or sugar syrup”.

Govt policy may simply be going with the market flow or at least trying not to obstruct it.

Prerna Sharma Singh, the author of the article, and director of a policy research firm, suggests removing controls on sugar. She says

-

artificially cheap sugar has health consequences

-

sugar has little weight in inflation, unlike cereals and horticulture.

-

larger future output requires higher capex. Denying access to profitable export markets will reduce the capex ramp-up. And will make price management harder in future.

-

export curb announcement signals shortages and leads to hoarding and higher sugar prices.

-

frequent export curbs create complications for foreign buyers and make India an unreliable supplier.

-

export curbs will not improve the supply for ethanol processing.

Therefore, export curbs have negative short-term and long-term implications.

Removing curbs will improve price realisation and ensure timely payment to the farmers

Link to article: Why India needs to relax curbs on sugar export

Sugar scrips bounced back from Today’s low levels. Uncertainty persists. Price levels may be struck at this level and range bound until firm clarity emerges from Govt.

Discl: Invested in Uttam Sugar and Triveni from lower levels.

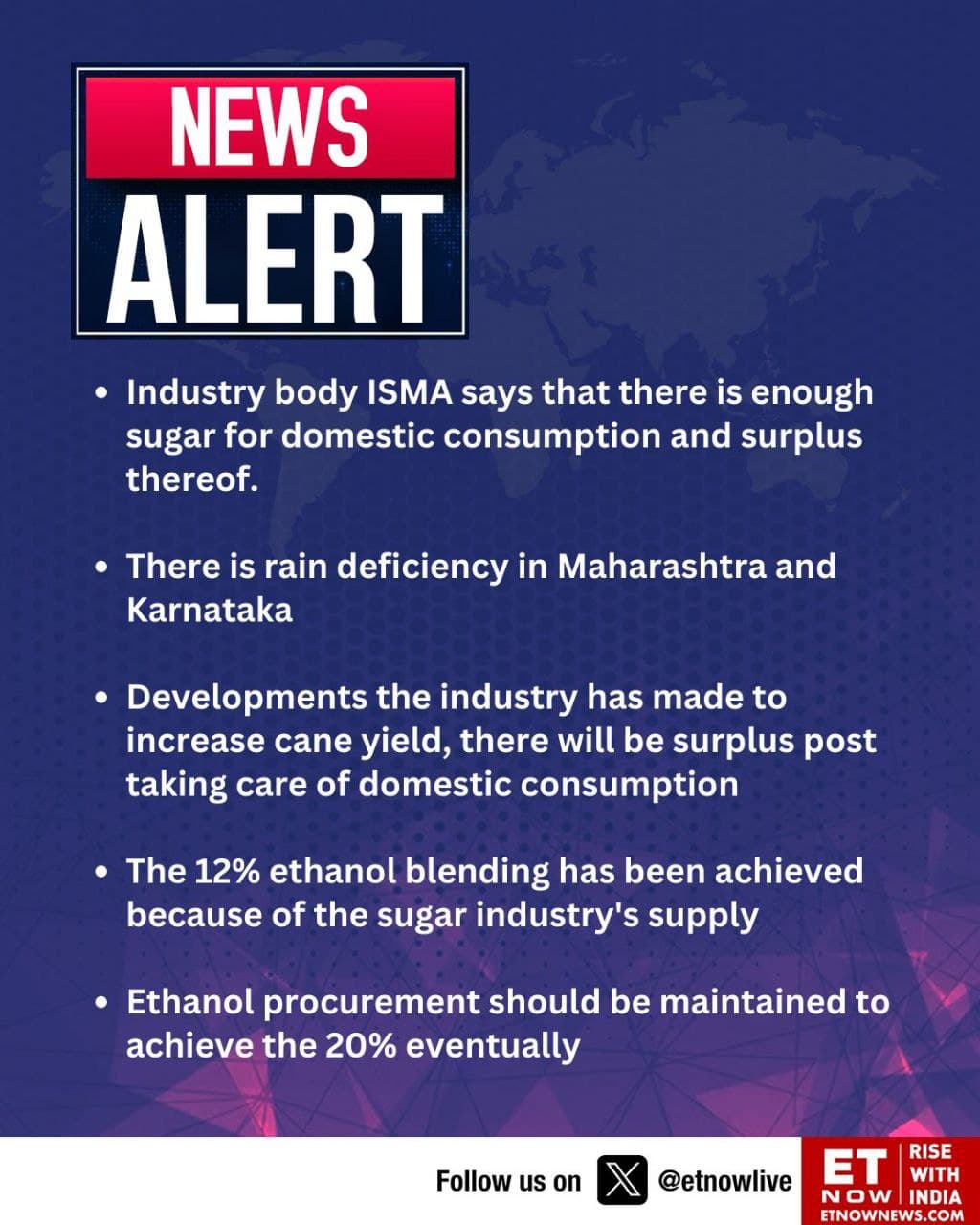

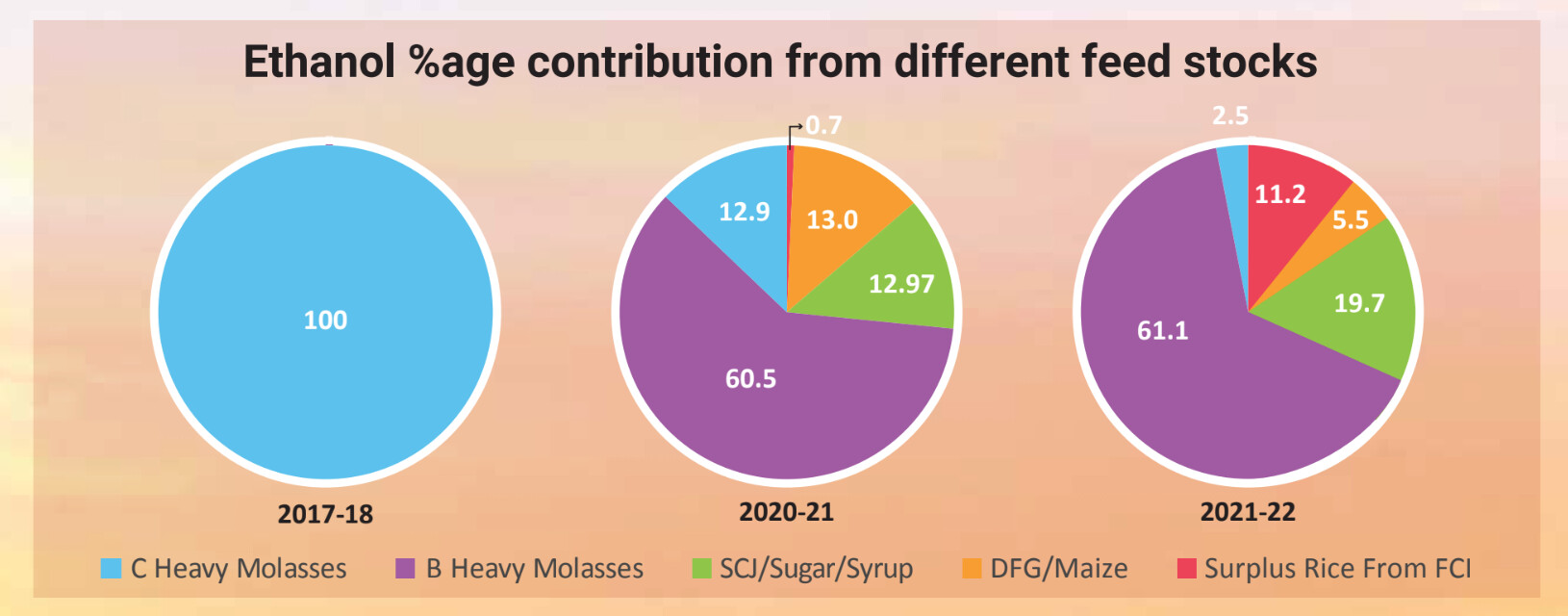

Let’s delve into the practical implications of this news. Currently, the sugar industry meets approximately 50% of the ethanol demand. If they cease procurement of ethanol from B molasses, C molasses, and sugarcane juice, achieving the targets of 15% blending, let alone the 20% blending goal for 2025, would be unattainable. This is especially critical as the expected contribution from sugarcane alone is around 1000 crore litres. Consideration must be given to the demand for alternative feedstocks in this scenario, with all feedstocks, except maize, already facing shortages. The escalation of prices for wheat and rice, which has already occurred, will intensify, leading to inflation.

Now, turning to the government’s decision to exclusively procure ethanol made from C molasses, this will result in a 20% reduction in ethanol production for sugar mills compared to B molasses and sugarcane juice. Despite the current state of sugar prices, it was anticipated that sugar mills would shift towards using C molasses. Even if they eventually halt this, the fundamental impact on sugar mills will primarily involve the loss of 20% of their revenues from the percentage of ethanol produced. Therefore, the long-term impact is not substantial, with no noticeable impact at the present moment.

Considering the existing scarcity of feedstocks and the escalating prices of other commodities, achieving the blending target is already a challenging task. Without altering the supply dynamics of rice, sugar, and wheat, it is practically improbable for the government to halt the sourcing of B molasses and sugarcane juice. It seems that the announcement is more geared towards creating hype, potentially helping to control sugar prices and prompting hoarders to exercise caution.

what do you say about dhampur sugar mills?

Dhampur sugar mills (as per the last concall) is already using maize instead of cane juice in its distillery. If maize is available at reasonable price then profits will be higher than last year.

Whatever is happening now in the sugar industry is not a surprise. sugar was more profitable than ethanol at Rs. 34-35. sugar prices have continued to rise for past many months and wholesale price will increase to Rs. 40/ 41 this year and Rs. 42/44 next year. Whatever the govt may do they cannot produce the sugarcane !! Maharashtra cane is actually 50% lower and recovery is hardly 8% - production will be 65% down.

Even if ethanol plants are idle, UP sugar mills will make higher profits than last year. If SAP is increased more than expected then sugar prices will go up accordingly.

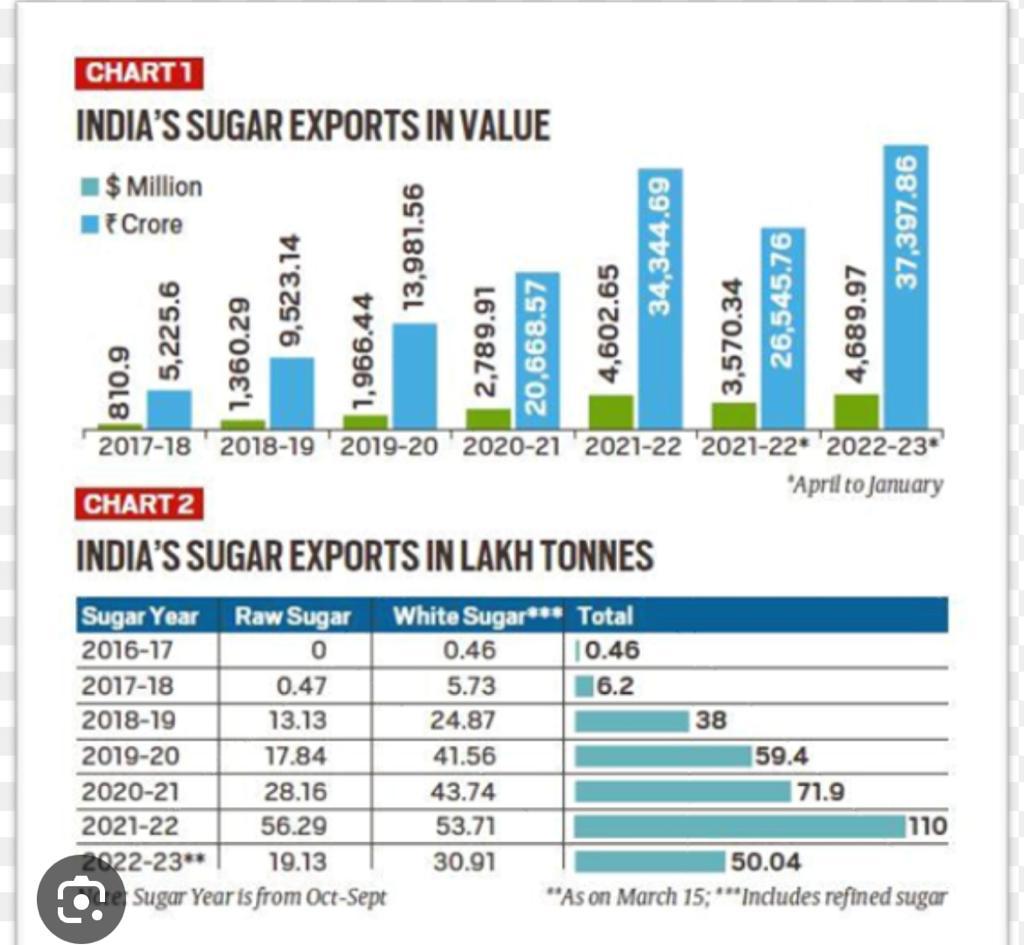

The overall SY23-24 estimate (from Triveni, Dhampur Bio latest conf calls) seems to be ~29 million tons country-wide sugar production (+ 4M diverted to ethanol, off the table now), assuming ~85-90 lakh tons from Maharashtra. But these are early days and maybe based on ISMA estimates which tend to be exaggerated towards over-production.

Even assuming 50% MH production decline, (now cancelled) exports & cane juice diversion for ethanol provide buffer for enough sugar.

But ethanol sales money is realized by mills within 15 days while sugar has a much longer working capital cycle, and hence could delay mills’ payments to farmers which is a bigger avoid for the govt in election season. It’s in the govt’s interest to “allow” a higher sugar price.

Will be a learning experience to watch this sugar year unfold.

Bought Triveni, Dhampur Bio recently, holding Uttam (after selling ~50%).

Newsflow of the last few days confirms sugar shortage. However, the hypothesis that the government will completely ban ethanol production based on Syrup/B-Hy Molasses seems extreme and might not be implemented. Why?

- Ethanol Year 23-24 targets 15% blending, and 70% of that demand’s procurement is forecasted from sugar based ethanol, which is almost entirely manufactured from Syrup and B-Hy Molasses. To cover for this much supply in a short span of time, activating alternative (plants and grains) sources seems impossible.

- It would be a bad policy decision - bad publicity to the ethanol mixing story, paralyzes ethanol industry infrastructure that was highly supported by the government till now, and chokes the quick source of earning for mills and in turn payment to the farmers.

A hybrid approach will be a better option- partial redirection from ethanol to sugar besides importing and subsidising the sugar.

Let’s see how it unfolds.

//…09-Dec-2024…//

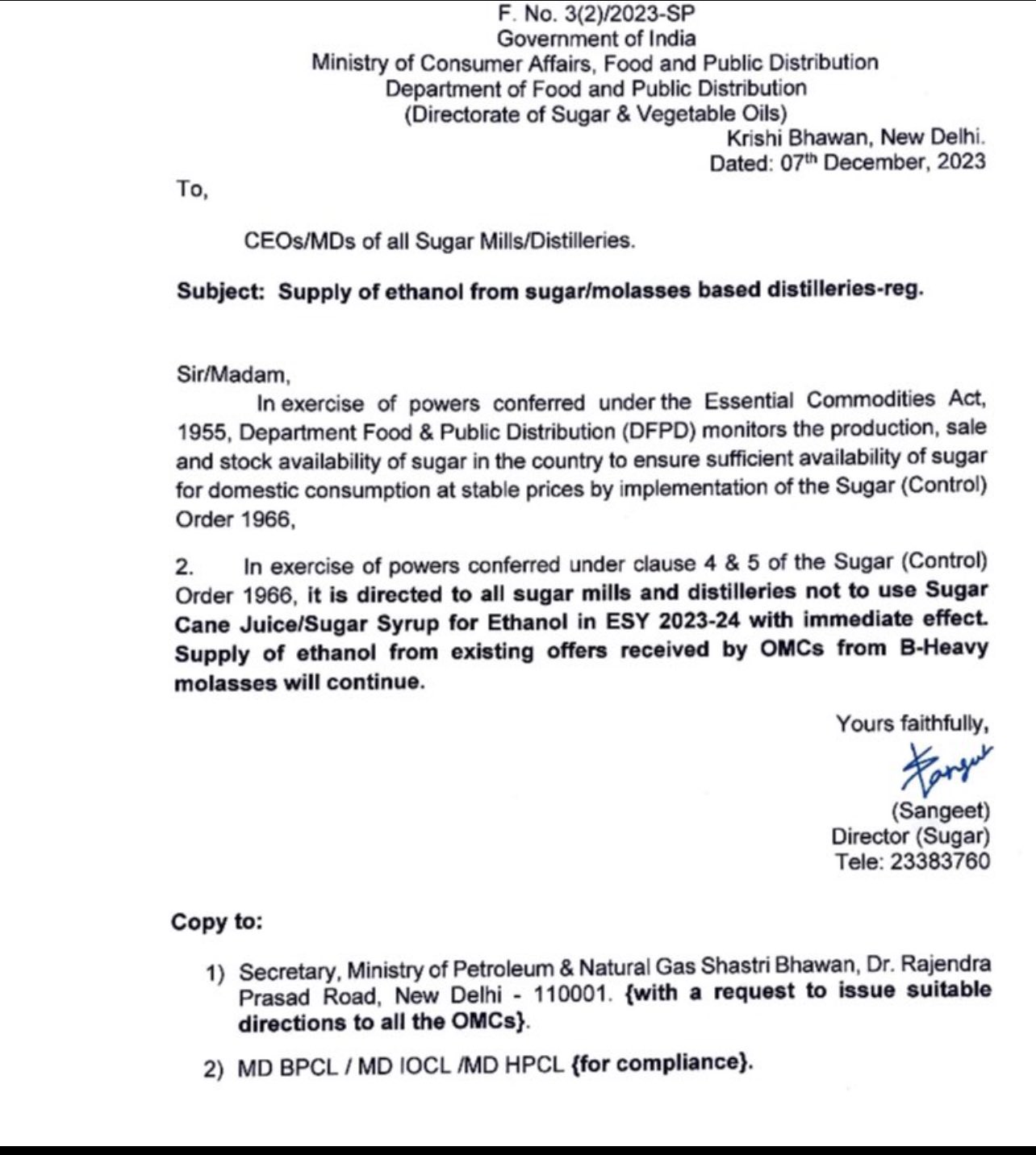

The Centre on December 7 banned the use of ‘sugacane juice and sugar syrup’ for ethanol production in the 2023-24 supply year.However, the government has allowed use of ‘B-molasses’ for ethanol production in 2023-24.

Source [Dated: December 07, 2023]: Government directs sugar mills to not use sugarcane juice for ethanol production to keep prices in check - The Hindu

Dhampur Sugar Concall page 2 of 10:

Total ethanol production during the quarter has been higher by more than 100% at 302.26 lakh liters versus 150.87 lakh liters in the corresponding quarter last year. Ethanol production during the quarter from B-Heavy molasses has been 264.19 lakh liters and from grain 38.06 lakh liters versus 150.87 liters from B-Heavy molasses in the corresponding quarter last year. There was no production from

grain in the last year as distillery from grain was commissioned in Q1 FY’24.

Sale of ethanol from B-Heavy has been 278.62 lakh liters during the quarter, 28.21 lakh liters from syrup route and 34.68 lakh liters from grain versus 154.17 lakh liters from B-Heavy and 2.93 lakh litres from syrup route in corresponding quarter last year. Production of ethyl acetate has been 89.25 lakh kg versus 62.92 lakh kg in the corresponding quarter of last year. Sale of ethyl acetate has been

90.21 lakh kg versus 63.1 lakh kg in the corresponding quarter last year.

As per understanding with notification 07.12.2023: Supply of ethanol from existing offers received by OMCs from B- Heavy molasses will continue. Question how much order quantity is pending is important?

Another way to understand the entire scenario.

Why is the Indian government taking such a bold step due to low oil prices and the government so confident of handling the import bill?

or

Want to encourage / boost to single ETHANOL manufacturers!

Though impractical and knee jerk kind of reaction, I think this will stay for next 6-7 months till elections are over.

Agree… this is for the elections. after elections ethanol procurement will be back. That is why the govt order is only for 1 year 2023-24 - while they very well know that cane shortage will be there for 2 years. Govt cannot take the chance of sugar price going up too much like onion or tomatoes. Sugar prices had gone up like this in 2017/2018.

Wholesale prices have gone up by Rs. 2 to Rs 42/ 43 over the last one month - this can be easily verified by just speaking to any trader in the wholesale mkt. In fact it has gone up further after the announcement of ethanol restriction. Most likely it will go up by a few more rupees by Jan/ Feb when the output from Maharashtra and Karnataka is known.

Ethanol production will be back in 2024/25 as Govt. has to reduce reliance on imported fuel - with rupee depreciation oil will become more expensive going forward. And farmers get much better returns from sugarcane. In UP, SAP was not increased last year but acreage has increased by 7 to 10%. It is well known that farmers are fine with Rs. 350 SAP also - but due to election year Govt will increase it. But again SAP wont be increased for many years and then ethanol margins will be high and stable. In period of high sugar prices (domestic or international) companies can switch back to sugar - like it is done in Brazil.

If you take a medium/ long term view on sugar sector, it is going to do well - it can be multibagger. You have to just stay put !!

Think we need to get some contexts right - that might help us think through this piquant situation better:

-

GOI’s primary prerogative has been to manage the surplus sugar production in such a way that prices don’t crash, sugar mills are profitable so that farmers don’t suffer and receive their payments on time. So whether it is the interest subvention schemes, Export quotas, export subsidies, B-Heavy Molasses route Ethanol, and Ethanol through sugarcane juice - it has all been to manage and nurture the sugar constituency and a very important vote bank.

-

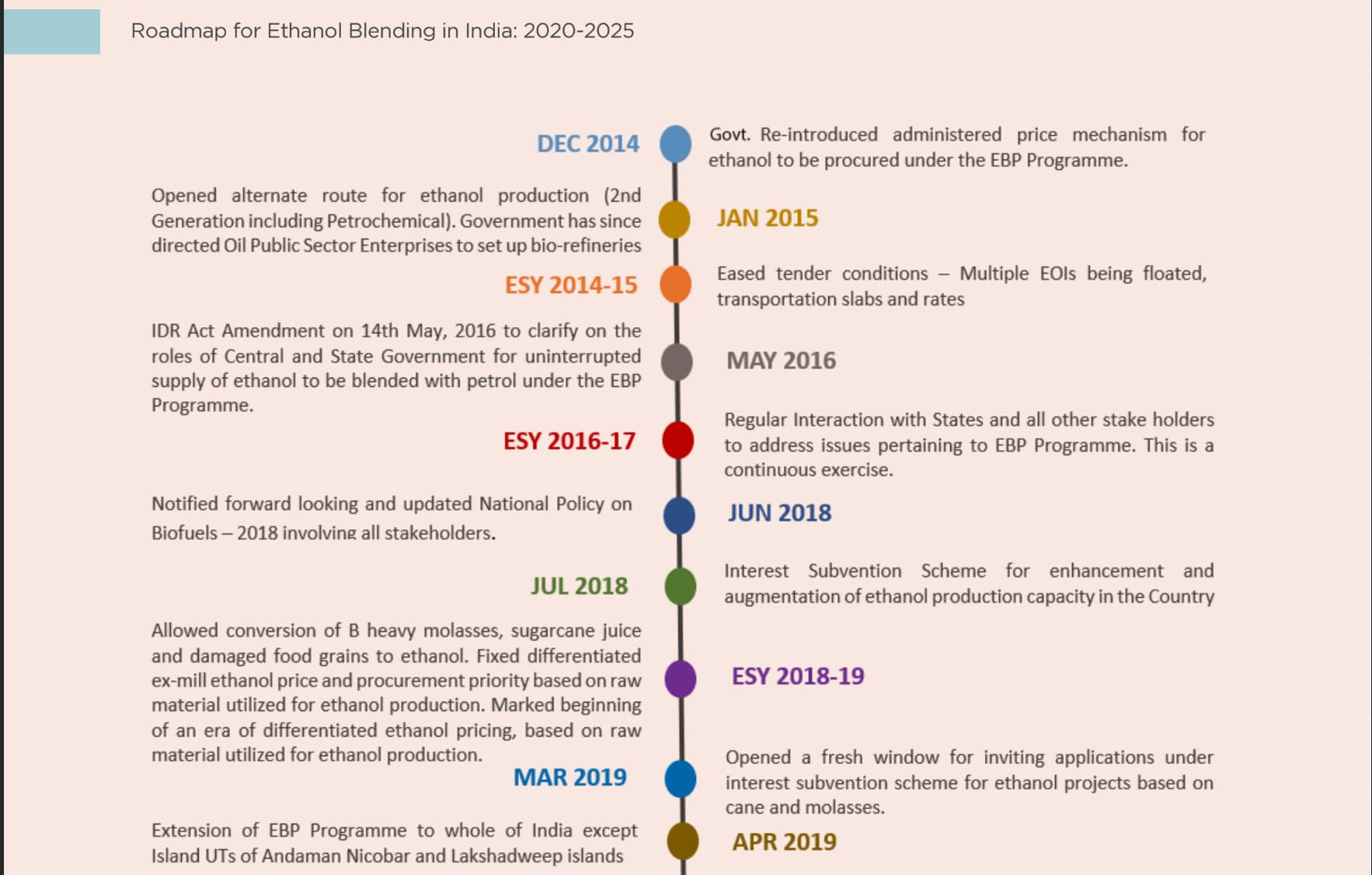

Since the start of a proper Ethanol Blending Program/execution for India, this is the first year that there is actual shortage on the ground - all other years till now there has been surplus production. And more and more Ethanol diversion was actually the way to manage sugar prices from falling, and ensuring farmers are happy. It would not be amiss to mention that the credit for India’s progressive Ethanol Blending Program had more to do with sugar-surplus years, than Clean-Green Energy drive by GOI. That will help explain better why GOI has done what it has

-

However, we have seen Managements of Renuka Sugar/Balrampur Chini giving interviews denying the shortage situation - production will still be 290 LT (with diversion). Mr Sarawagi went so far as to claim actual production will now be 315 LT (given the latest policy intervention by GOI of denying Sugrcane juice route ethanol diversion). Whereas the Govt’s actions clearly indicate that they find there is shortage - and this is a measure to plug the gap (less diversion to Ethanol so that costly Imports don’t have to be resorted to). And thus sugar prices can be kept in check (in the run up to elections).

-

I have been wondering what really is the incentive for Sugar Mill owners to be in DENIAL and actually plead the case - pretend that things are at a very sorry surplus sugar state; Maizapur sugarcane juice site (Ethanol) will close down; but the moment asked a more pointed question will there be losses - no no - things can be reset in 10 days (it actually has a sugar mill too), till then we will divert to other group companies.

-

The only plausible answer for this deceptive “rona-dhona” by Sugar Mill owners is for them to try and negotiate UP SAP prices (which are now going to be set) down by 5-10 Rs from the increase of Rs 20-25 being recommended by Government. FRP has already been set at Rs 10-15 higher (non UP states) which goes up every year. It is worth noting that UP SAP prices have not been revised upwards in last 3 years

-

As mentioned many times before in this thread - if sugar prices remain over 37(and 39 for B heavy), there is very little incentive for the sugar mill owners to go the sugarcane juice route. Most were NOT planning to in any case (in any significant manner). The B-heavy route tenders are out till April 2024. It is very likely that even these will NOT be renewed beyond April 2024.

-

We need to wait out another 2 months till Feb/Mar 2024 - for actual shortage situation to reveal itself. There might be temporary drop of Rs 1-2 in Sugar prices now, but should come back up from Feb/Mar 2024 emphatically.

-

We should understand GOI doesn’t mind a temporary reversal in Ethanol Blending program, so long as its primary objective of not letting sugar prices run away too much in the election year. It doesn’t so much care for setbacks to EBP. It is my feeling now that if GOI finds that payments to farmers are getting delayed because of existing EPB, farmers are annoyed and their vote bank is getting affected, they might not be even averse to reversing the EBP

-

That the same objectives could have been met through imposing Sugar Import Quotas or lower-capped ethanol blending targets, is another matter. The job has been done.

-

We must remember that the Economics of the UP based sugar mills will be only minorly hurt with this policy intervention. They will all do very well. Sugar production cost is likely to be Rs 33-34 (on an average thru SS 23-24). Sugar Prices on an average are likely to be Rs 39-40 for UP on an average in SS 23-24. That will make for big profits even adjusting for additional Working capital requirements. Every 1 Rupee rise in sugar price makes for additional 45 Cr (Uttam Sugar) to bottomline.

-

There is no denying that Sugar production in SS 24-25 without any diversion will still be lower than SS 23-24. This is because of the complete absence of 18 month Adsali crop plantation in MH and KA (due to no rains this year in July/Aug), let’s not forget that.

-

A 100 KL sugarcane juice distillery can be adapted to multi-feed distillery with additional expense of ~15 Cr

-

Having said all above, the latest policy intervention by Government is not making sense for MH and KA farmers. There are lots of small small mills with poor balance sheets. Certainly payments to farmers will be delayed here (unlike say the financially strong mills in UP), affecting the vote bank? Is there a case for even reversal of the policy intervention as it stands now - leading to a more consultative way of managing/capping sugar price rise??

References:

Recovery in maharashtra down to 8% in 2023-24 from 11% last year.

Cyclical investing involving an element of timing the purchase.

The best time to buy is when conditions look very bad and stock price starts to go up.

The worst time to buy into cyclicals is when the conditions look very good but the price starts going down.

In other words, Buy when PE is high (Distressed earning) and sell when PE is low (earning peaks out).This I have learnt from Jiten Parmar sir.

Monday sugar sector will be up again !!

make molasses without causing sugar shortage…so how is this a cyclical uptrend?