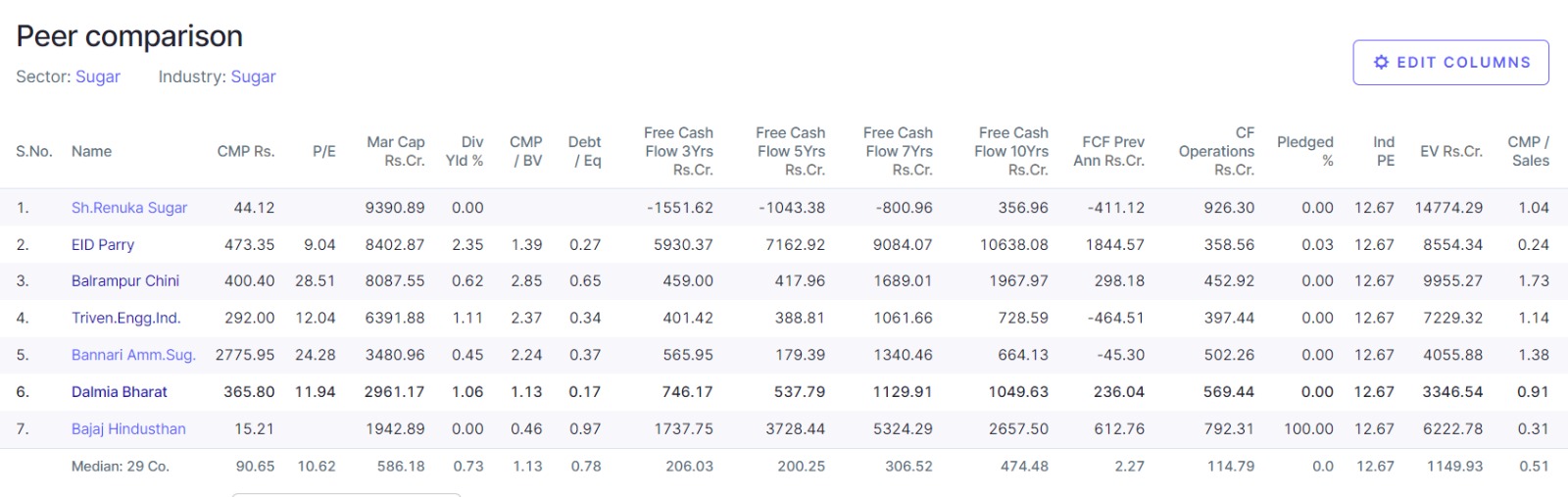

EID Parry - trading at 5.5-6 p/e lower than sector & murugappa group, debt is minimal & mostly short term, have a big stake in coromandel more than market cap, lowest debt/ equity & cmp/sales compared to ppers. Attaching herewith peer comparison & concall notes from screener, & recent management interview with CNBC. Want to understand what am I missing & how is etanol story poised for EID parry if experts can share their view.

Concall Notes - Jun 2023

Financial Performance:

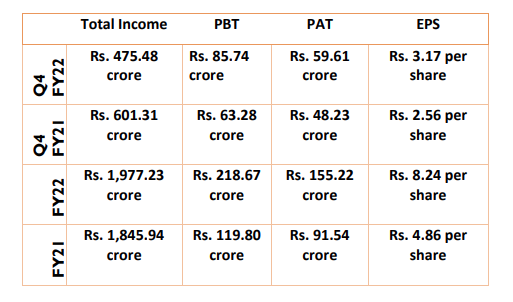

Q4 FY23 revenue was INR 807 crores, down from INR 921 crores in the previous year

EBITDA for Q4 FY23 was INR 327 crore, up from INR 309 crores in the previous year

Standalone profit after tax for Q4 FY23 was INR 83 crores, down from INR 225 crores in the previous year

Standalone revenue for the year ended March 31, 2023, was INR 2,895 crores, up from INR 2,489 crores in the previous year

EBITDA for the year ended March 31, 2023, was INR 527 crores, up from INR 492 crores in the previous year

Standalone profit after tax for the year ended March 31, 2023, was INR 197 crores, down from INR 284 crores in the previous year

Sugar Division:

Better sales realization and increased domestic sale volume

Cost pressure due to higher energy prices

Achieved a sales volume of around 5.19 lakh metric tons of sugar on a year-to-date basis, with an average selling price of INR 35.98 per kg

Closing stock of sugar as of March 2023 was at 2.45 lakh metric tons valued at around INR 33 per kg.

Ethanol Facility:

Completed the sale process of Pettavaithalai plant and commenced 120 KLPD ethanol facility in Sankili from sugar syrup

Nutraceuticals Division:

Registered a marginal increase in profitability despite a 13% reduction in revenue

Consolidated loss due to expenses on Flomentum and product loss from fire accident, but optimistic about insurance claim in subsequent quarter

Cogen and Distillery Operations:

Revenue from Cogen and distillery operations increased in Q4 and on a year-to-date basis

Distillery profitability affected by increased fuel prices and molasses transfer price

Distillery segment expects better margins in subsequent periods due to normalized fuel prices and efficiency improvements

Refinery Business:

Increase in sugar production but a loss in PBT

Lower sales volumes and forex losses contributed to the operating loss in the refinery segment

Refinery spread expected to improve with tightening demand supply in sugar market

INR 106 crore impairment charge for PSRIPL factored in forward possibilities of refinery investment

Refinery business has INR 200 crore long-term borrowings and INR 620 crore short-term borrowings

Expenses:

Employee benefit expenses and other expenses increased due to salary increases, headcount, and expansion

Finance costs reduced due to better working capital management

Outlook:

Energy prices are coming down, leading to lower finance and interest costs

White premiums are strengthening, leading to improved spread atmosphere

Refinery business outlook based on availability of spreads, cost of refining, and cost of money

The company expects to make up for the lower sales volume in the current year and doesn’t expect the forex losses to continue

Intent to run robust standalone EID Parry business and focus on strengthening it before considering dividend payout

Other Points:

The company exported more power in Q4 than the previous year, with a higher average tariff

No capital infusion is projected for other subsidiaries