What is the reason of intermittently reduction in acreage in MH , specially SS20, drought ?

Updating it as I get more information

Ponni Sugar 24th AGM- 2019-20 -Indian sugar – Current Status

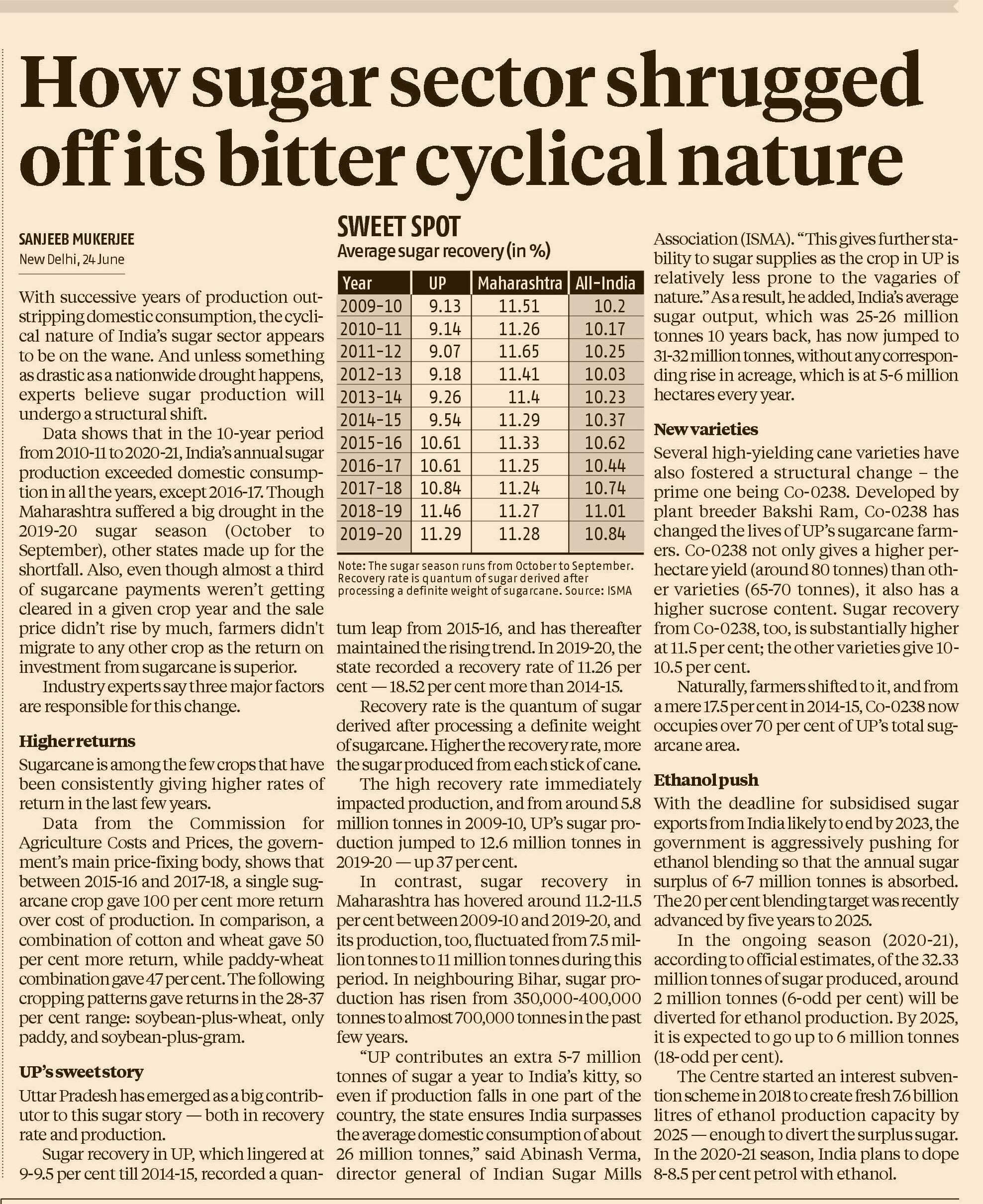

Historically India’s sugar production has been the least from the east, while the other three regions remained well balanced. There however appears a tectonic shift in this distribution during the past five years. The State of UP was always the largest sugarcane producer but the recently introduced new cane variety, that enjoys an enviable combination of high yield and high sucrose content, has catapulted UP as the undisputed leader in sugar production with little year-on-year variation. In contrast, the south has turned a victim of recurring drought and erratic weather and became a structurally low production zone with low sugar recovery that is challenging the very survival of sugar mills in the region. While so, the West comprising Maharashtra and north Karnataka go through weather induced cycle of high and low production with year-on-year swing too significant that eventually drives and determines the surplus or deficit in the country’s sugar balance.

Weak (non efficient) mills will benefit (most?) by recovering ethanol (otherwise lost value) though b-molasses?

What is the reason for low production cost in Brazil and Thailand?

Higher production per hectare?

Higher sugar yield?

Weak currency? or

any other cost factor?

From 2013 PONNI SUGARS AGM speech

India lags behind only Brazil as the second largest sugar producer but lacks considerably on cost competitiveness. Brazilian sugar mills own 60% of cane area and their typical farm size is 1000 acres and above. In India, factories cannot own land under land ceiling restrictions and average farm size is just about 5 acres. More importantly, Brazil is endowed with Amazon forests bestowing copious rainfall and rendering the cane crop totally rain-fed while irrigation costs are considerable for India. As a result, cane cost is roughly 40% lower in Brazil. In addition, Brazil has well stabilised its ethanol blend programme which is currently at 25% while India is yet to get over the glitches in the implementation of its maiden 5% ethanol blend plan.

So putting up a new mill or increasing capacity need govt permissions? Also demarcation of catchment area? where does a new farmers get to sell his crop?

Why a farmer not switch to cane from other crop if cane is much profitable?

Apart from grains, what are other untapped starch/sucrose source in India for ethanol conversion?

Value Unlock at Dhampur Sugar Asmoli, Mansurpur and Meergunj Units to be demerged and formed as Resulting Co.

*** One equity share of Rs 10/- will be issued in the Resulting Co for every share of Rs 10/- held in the Demerged Co (Dhampur sugar Mills.)*

Hi @varungoenka thanks for facilitating such an insightful session! Would you be so kind as to share the webinar & ppt links? Unable to access links shared earlier as they’re private

if the brazil crop of sugar comes out well … they can export to intl markets and indian exports may be impacted but subsidy on exports by indian govt to the tune of rs 4/kg still exists and production in thailand will be lower so india stands to benefit… main benefit is ethanol which will result in cane diversion and also no need of sugar exports in next 2 years

Consumption growth has decelerated from the average of 2.4% since 1960s to around 1.8% in the last decade.

World production in 2020-21 estimated at 169 mln tonnes would be recording its third consecutive decline, down by more than 10 mln tonnes since 2017/18. It is below the 10 year average output.

It looks 2021/22 would mark the fourth year of production decline which is exceptional that had last happened 19 years ago.

Brazil in marked departure from larger allocation of cane for ethanol in the preceding two years, opted for higher mix in sugar during 2020/21 (April-March). As a result, Brazil has achieved an all-time high sugar production but for which the global deficit would have been wider by over 4.8 mln tonnes.

ISO had earlier estimated the biggest deficit in 11 years for SS 2019/20 pursuant to the perceptible decline in crop from India and Thailand together contributing about 12 mln tonne fall in production. The advent of Covid-19 however annihilated this prognosis. Global oil price crash goaded and nudged Brazil to notch up cane allocation for sugar, while consumption growth dimmed and dried up during lock down times. In the end, the biggest deficit projected precariously petered out and global balance became near neutral for SS 2019/20. Ergo, the much taunted and most wanted inventory correction failed to fructify.

India:

Sugar production as expected rebounded in 2020/21 that is estimated at 302 lt. This is after swapping about 20 lt of sugar into its ethanol equivalent.

UP is notably the prime mover and principal contributor for this tectonic shift.

Maharashtra and Karnataka, having recovered from last year’s drought and been benefitted by good monsoon this year, bounced back with 71% and 22% rise in production for SS 2020/21.

Container shortage is an impediment in whites exports but raw sugar exports in bulk has come to the rescue.

Export subsidies for sugar may not continue beyond 2023 under extant WTO norms, our surplus sugarcane needs an alternative absorption route

Outlook:

Global sugar balance has remained negative for three years in a row that would seem to persist in the year ahead as well. Nonetheless, the huge inventory carryover dampens the prospects for global price resurgence. Given the current sugar balance outlook, global sugar prices may largely remain range bound with little prospects of rising above 20 c/ lb. With lower crop in Brazil and slower recovery in Thailand, India is well placed to seize larger share of global market and achieve its export targets. Likely resolution of Iranian currency problems would further lend strength to India’s sugar export program.

Very informative, thanks for sharing. Global and domestic prices are range bound and are not going up however all listed stocks are making new highs, any valid reason for that? Ethanol story is already priced in I guess.

While the entire basket of sugar stocks got a fillip after Govt.'s declaration of higher and earlier ethanol blending with petrol, is the Indian auto industry ready to embrace the changes that will be required in car engines? What happens to existing cars on the road?

Explained here: Engine Modification

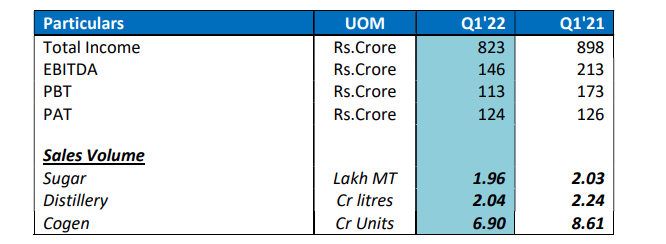

EBITDA is lower for the Qtr due to low vol offtake due to COVID and expected to be recouped in subsequent qtrs.

Topline and EBITDA are down Y-O-Y but PAT is maintained alomost at the same level due to write back Deferred tax .

15Cr Litres of Distillerry project is on Schedule barring Kolhapur (due to flood situation in Maharastra.)

*Two Grain based Distillerry are being set up for 6Cr litres of Ethanol which is expected to be commissioned in 15-18 months.

Management commentary is bullish on prospects due to less carry over stocks and diversion for Ethanol.