yes compared 4-5 sugar stocks after your message…!!dhampur looks quite attractive along with DCM shriraam…!!!..!!for future potential. if sugar prices remain firm for next 6-9 months.

Regards

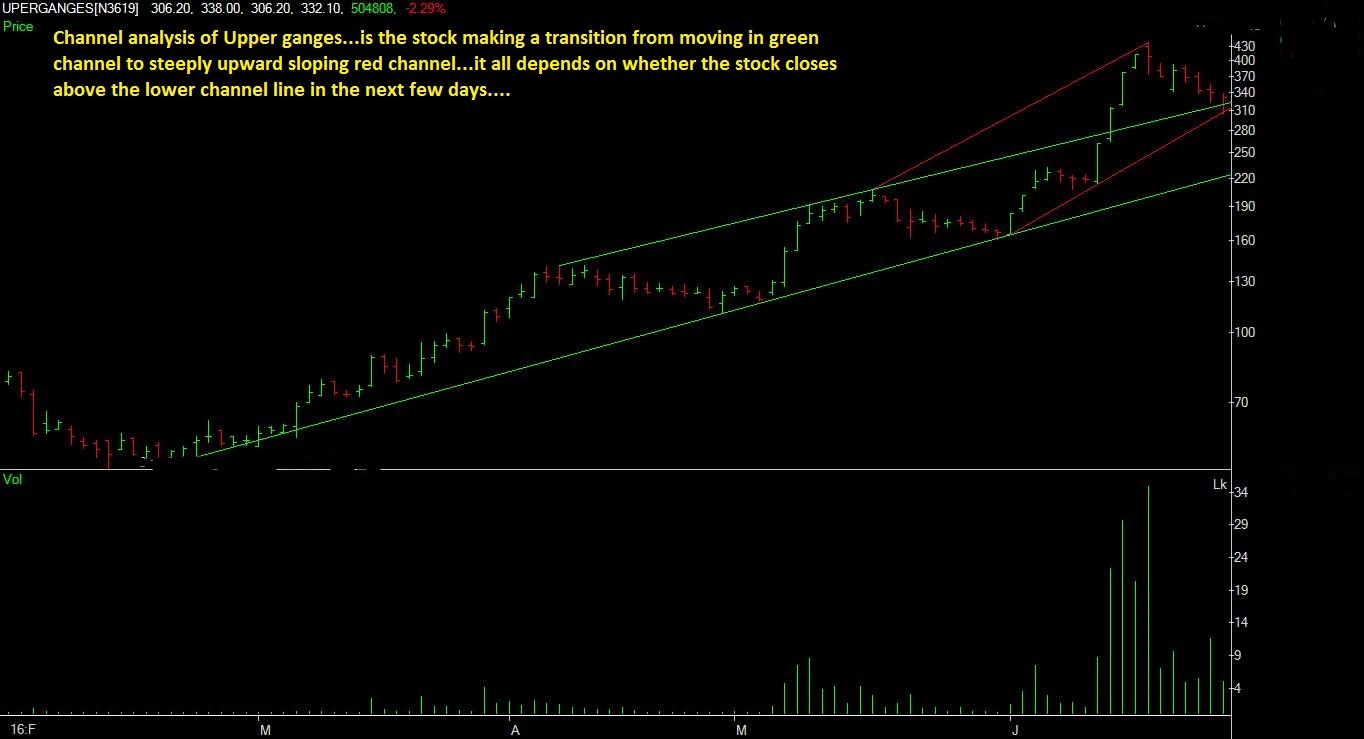

The fact that both the channel lines (green and red) are nearly parallel indicates that perhaps channel analysis is the more appropriate tool for analysing the price movement of Upper ganges…but as I said…it all depends on whether the lower red channel line is broken or not in the next few days…

In case the stock remains above the lower channel line, the it may rally to a new high price…

Hi Mehnaz

My assessment of Upper is that it should have EPS in the range of 40 -50 minimum for next 2 quarters. Hence even at a reasonable P/E of 5 , rate Rs.500+ is achievable.

But i do not have technical knowledge and as rightly pointed in some earlier message by you, you can’t just buy and sit in Sugar stocks. Need to be ever alert.

These inputs from technical point of view would be very useful for fellow investors like me .

.

Hi @Mehnazfatima ,thanks for posting regular updated charts. from few posts of yours it seems like ur bullishness on balrampur has come down? are you booking out of balrampur and buying Dhampur on declines? Just curious thats all … you can choose not answer

Invested (quite heavily) in Balrampur and Dhampur… no question of selling Balrampur.

4 Likes

Mehnaz ji

Will you please throw some light on dalmia sugar both from technical as well as performance and inventory point of view.Thanks in advance

Only short tern negative is QIB @98.8 by dhampur sugars…!!else all looks good…with inventory of 33 lakh bags that translates into unrealised profit of 130crores over a period of 2 quarters…(remember thats only inventory gain)

In Dhampur—Inventory is valued at 27 rupees… it will be sold at an average price of 34 rupees(minimum)… Thus profit calculation is 33 crores * 7= 231 crore rupees. The earnings from ethanol and cogen will take care of interest and depreciation.

So for an expected profit of around 200 crores, the present market cap is just 600 crores.

1 Like

For Balrampur the expected profit is around 500-550 crores (because interest payment is very less) and the present market cap is just 2700 crores…

The best, the most efficient and debt free sugar company deserves a P/e of around 20 (atleast) …which gives us a target price of around 400-450 in one year…not bad at all…so why would anyone want to sell it😃

Those who are more bullish estimate earnings of around 800-900 crores for Balrampur in the next financial year …and expect the stock to reach 600-700 range. But in stick market, it better to rein in our optimism. :)

3 Likes

Balrampur in its Q4 quaterly report mentioned the following

’During the quarter, sales volume stood at 18.06 lakh quintals as compared to 18.46 lakh quintals in Q4FY15. In the current quarter, realizations improved to Rs. 31.35 per kg as against Rs. 26.19 per kg in Q4FY15. As on March 31, 2016, sugar inventory stood at 57.16 lakh quintals.’

It has 56.16 Lakh Quintals at a price of Rs 27 per Kg including depreciation.

Assuming it is selling at 34 /kg, it is a cool 400 cr profit

Next year if due to shortage of sugar, if Balrampur is able to sell its sugar at 38-40 rupees, then what will be its profit…it earns above 200 crores from cogen and ethanol…

Fully agree. Wholesale Price of Sugar already at 36-37 / kg. I just considered Sugar details

What will be the bear case estimates of sugar price and profits for Balarampur chini???

Here is my estimate that can wrong badly

EPS will move from min 8 to max 16. Again depending on Govt action, things can go wrong. Please make your own judgement. I think @Mehnazfatima is tracking more closely

@Mehnazfatima- any idea what is the margin per L , for Ethanol ? and margin per unit for Cogen ? I saw the selling price ( 45 and 4.8 repectively)

Guys, it a waste going into minute details wrt financials…cyclical investing is a game of momentum. Try to ride the momentum and exit on strong exit signals in 2017…

Oudh sugar with a book value of minus 47 rupees has become a ten bagger…on what basis? It’s just momentum which is lifting the whole sugar pack…

2 Likes

One question…how much equity dilution happening in dhampur due to QIB…bcoz at place i read 66lakh shares @98/-…and at one place it was 200crore…if it is 200 crore than dilution will be very very high compared to 66lakhs shares.

Any one who knows the correct value pl do reply.

REGARDS

In the QIP offer document it is give as 66 lakh shares at 98 rupees per share.

May be i am being naive but would it be prudent to calculate target as a peak multiple to peak earnings for a cyclical business? Who would you expect to buy at that price?

3 Likes

major blast in all sugar stocks…!!!this is just the begginging of sugar supercycle…!!real deficit in SUGAR can be seen in next season…!!all sugar stocks are hold for next 3 Quarters.Regards