umcoming Q1 results will be good…!!!but Q2 & Q3 numbers will be best in decade

The only threat to all this Euphoria will be any Unrealistic FRP + SAP for Sugar.

I believe commodity cycles hould be played by buying at a very high PE and selling at a very low PE. Upside looks very limited as every positive has been already discounted well in advance.

Just my 2 bits, i may be wrong.

(Disc : No holding)

Amit

1 Like

Not yet as I believe Sugar prices are no way close to their all time high. There is still some room for sugar prices to go up. Till that time the top will not me made. Its been only 1 or 2 quarters of good results from sugar companies, I believe there is some more meat left to the story. Almost all the sugar production in Maharastra and other parts of the world is low and any improvement would take some time. Commodity cycles last some more time than its already (6 to 9 months of up move in sugar prices)

“I reserve my right to be wrong”

the profit figure of 200 crore you are talking i beleive will be achieved in 2 quarters only…!!yearly profit will be 400 crores minimum(upcoming Q1 will be 110 plus crore) if sugar prices remains here …!!and if in case they rises by only 10% from here in next 9 months than i cant imagine the share prices and EPS…!!very very good times ahead…!!!Regards

Noo…they get 200 crores profit if they sell the whole of their sugar inventory of 33 crore kgs…if they sell this inventory in first two quarters, the they wont have any sugar to sell in the next two quarters…that’s why in my opinion, the sale will be spread over all the 4 quarters…and the total profit over these 4 quarters will be 200 crores…in my estimate

There will be New sugar arriving from 1st october with less realisation or not that depends on sugar prices that time…currently sugar prices ex mill are above their breakeven so everytime they will make profit with present sugar prices though it will be less than the huge inventory gains…!!

So i firmly belive profit are not gonna less than 350crore yearly…200crore plus from inventory gains and 150 crore for last 2 quarters

And if data to be belived there will be much bigger sugar deficit next sugar season…so prices may shoot to 3900/’ quintal during march april next year as above that govt will not aloow to go them higher touching 4000/-physcological mark…

Regards

Dhampur margins are quite good at 26%…there sales this Q will also be above 500crore so according to you thier profit will be 50 crore (for 200cr yearly) i.e only 10% …that is not possible at all…result and profit will be higher than Q4…NET PROFIT will not be and can not be less than 3 digit markk in Q1.Regards

Mehnaji

I have different take on cyclicals like Sugar .

I think you get maximum % return if you bet on companies which are not the most efficient ones but which can have massive increase in EPS going forward .

Even our renowned Hiteshji has put forward the same argument in this same thread around 2013 i suppose .

Lets say a company which made losses earlier , this year will have an EPS of say 80+, then that company cannot be having a P/E of say 2 !! Many of the single digit shares are already 10-15 baggers .

So which companies will have massive increase in EPS in 2016-17 - I think the ones with following

- Company with very high inventories . I think many of the UP based companies fit this criteria.

- Company with a low or reasonably low equity .

- Company making substantial profit from other than sugar business.

- Company which will not PAY ANY INCOME TAX THIS YEAR ON THEIR PROFITS. - For me this is a very important factor to be considered this year as 33% tax will reduce the EPS of the company by 1/3 !!. I think most people are not looking at this aspect .

So Look out for companies having high Deferred TAX assets (DTA) in their balance sheets as on 31st March 2016. I think they will use this tax credit against the tax payable this year and hence no tax may be paid this year.

Based on this my high conviction bets are -

- Upper Ganges -equity -1.15 cr shares, Inventory - Rs.529 cr, Non-Sugar profit - Rs.72 cr for last year &

DTA - Rs.71 crs . - Oudh Sugar -equity -2.6 cr shares, Inventory - Rs.738 cr, Non-Sugar profit - Rs.80 cr for last year &

DTA - Rs.128 crs

mind you whole thesis is for investment horizon of say 10-12 months when valuations should be reach their peak and one should be getting out of these stocks by then.

I could not find any other quite matching upto these on above parameters,

Would like your view on the above as well as fellow borders as ICE futures have laready at 21 cents level today.

5 Likes

Prakashji: i fully agree with what you have said… This was first pointed out by the father of value investing - Benjamin Graham.

Recently, in his book titled - Behavioural finance and value investing, Parag Parikh devoted a whole chapter to cyclicals and proved with data that when there is a turnaround in cyckical sector the least efficient producers give their investors the maximum returns in percentage terms… This applies not just for sugar, but also for all cyclicals such as steel, paper, cement, shipping etc

But the only problem is that to get maximum returns, you are required to invest in the least efficuent producers at the depths of bear cycle. Thats the time when the least effucient producers are most likely to go bankrupt.

Even if we are very brave, we wont have the courage to invest a big amount of miney in the least efficient producers… investors make good returns but the amount invested would be quite less…

Anf finally this theory has not played out well in this sugar cycle… the least efficient and most debt laden producers - Renuka and Bajaj Hindusthan have given paltry returns to investors.

It is better to invest a big amount in undervalued but effficient sugar producers… one such company was Dalmia sugars… a very undervalued company but with very less debt and in profit during most of the downcycle… it went from 10 rupees to 140 rupees… and still going strong.

6 Likes

Mehnazji

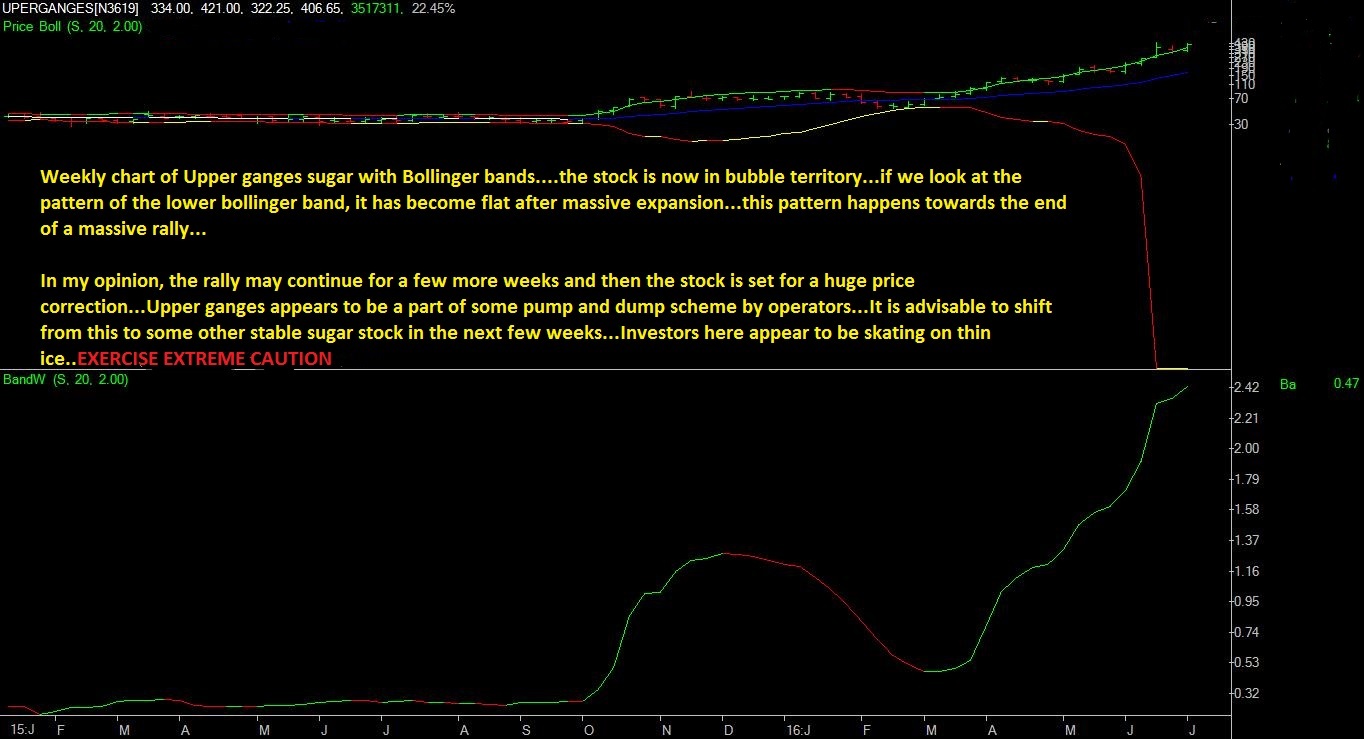

Hope you can spare few minutes to look at upper & oudh charts this weekend.

In my opinion, as soon as the band width starts contracting, investors of Upper Ganges are in huge problem.

Of course, I may be wrong and the stock may keep rising…

…but still…at some point of time this bubble will burst…and that will be indicated by the contraction in band width…

Thank you Mehanzji.

Might sound stupid to you … but could not make out how to read this …

Could you please let me know which are the lines i need to monitor in the above chart to monitor contarction or otherwise of bandwidth in the above chart ?

I can write in detail about bollinger bands but it wont be any better than the information contained in the numerous articles available on the internet…

2 Likes

Do we have similar threads for other cyclical goods like tea, chemicals on VP? Can someone help me locate?

I believe (Indian) tea is also in the middle of a recovery while dye chemicals have been turned around since 3-4 months now. Is anyone looking at these?

2 Likes

Alert for investors of Upper GAnges…stock has begun correcting…targets are 360…307…and 280…on daily charts the momentum indicator has turned down…

2 Likes

bad signs…!!hmmm…

whar about dhampur and ugar technical structure??pl share your view as you are technical analyst…i am only fundamental investor…!!fundamentally i sees no problem…techincally u can tell better.Regards

soon results will start for sugar stocks…!!

Infact this is an alert for almost all the sugar stocks…including stronger ones like Balrampur…the daily momentum indicators have turned down …the sugar sector may see a short term correction.

Stocks which have risen more post the brexit rally will fall more…stocks such as Upper Ganges, Oudh, Ugar, Uttam, Rana sugars which were in bubble territory and which are much higher from support levels may fall a bit more than other sugar stocks.

Fundamentally, the spot price of sugar in Delhi wholesale market has crosses 3800 rupees per quintal…on weekly charts the price has touched the lower channel line and bounced.

It is hoped that the rising sugar price in domestic market will make this correction a very short lived one…and an opportunity to buy more of sugar stocks.

5 Likes