Its surprising how theres NO followup discussion on this stock for well over 2 years now!

And i guess a lot of things have changed over the last 2 years which, on the contrary, should have evinced further interest in discussing the stock. After going thru the recently released Annual Report, i list down some of my observations as hereunder, hoping other forum members to catch upon and discuss further.

The last 2 years were marked with some interesting developments, starting with:

Induction of fresh blood

Fresh talent was brought in and the old team was reorganised which, hopefully, should address issues around corporate governance and business strategies that was plaguing the company earlier.

- Mr. Anil Singhvi gets appointed as the non-executive Chairman of the company in May ’17. For those uninitiated, Mr. Singhvi is the founder director of the proxy advisory firm IiAS (Institutional Investor Advisory Services), a firm dedicated to providing participants in the Indian market with independent opinion, research and data on corporate governance issues as well as voting recommendations on shareholder resolutions.

- Mr. Vinod Kumar Padmanabhan, serving with Subex for more than 20 years, gets appointed as the MD & CEO of the company in Apr ‘18

- Mr. G S Venkataraman, with more than 25 yrs of experience in the finance field (last 12 years in Mindtree), gets appointed as the CFO of the company in Sep ‘18

- Mr. Rohit Maheshwari, with over 20 yrs of experience in consulting, data analytics, business development, sales & delivery (of which 17 years with Subex), gets to head Strategy and Products in the company in May ‘18

- Mr. Shankar Roddam, having worked with Subex for 10 years where he was part of the executive team in the capacity of head – Emerging Markets and played a key role in establishing and setting up the Sales and Channel network in emerging markets, returns for a second stint (from Plivo) as a COO of the company in Oct ’18.

Formulation of a new strategy to take care of growth, over the longer term

The new team formulated a three-horizon strategy where

- List item

Horizon 1 – focus on core products (to take care of growth over the immediate term)

- With the exceptional performance in Horizon 1, put in place last year with their core products, the management claims to take on a more aggressive outlook to further expand their market share, y going after the smaller players in this fragmented market with an enhanced portfolio.

- This, in their opinion, should result in a growth rate higher than the previous year.

- List item

Horizon 2 – focus on newly launched products with huge potential (to take care of growth over the immediate to medium term)

- This consists of products in areas pertaining IoT security and analytics

- These products have already been proved in the market place and the management intends leveraging on the large market expansion

- List item

Horizon 3 – focus at aspirational growth areas and big impact use cases (to take care of growth over the longer term)

- To take care of their long-term growth, for the next 3-5 years, the management hopes for a sustained growth in the sales of existing Horizon 2 products and from some newly launched Horizon 3 products

- Their Horizon 2 and 3 products, such as IoT security and Anomaly detection, cater to an extremely large and growing market segments, in the managements opinion, which they hope to translate into significant revenue drivers going ahead.

- The management also claims that their subscription-based revenue model from these products to start contributing significantly (in the next couple of years)

Enforcing accountability and monitoring

The CEO has guided fast tracking selected components of their strategy to pursue a more aggressive growth. And some messages delivered by the CEO, in the annual report, implied accountability that the management intends attaching to their strategy.

- They have apparently broken down the strategy to specific Annual Operating Plans (AOPs), which is further simplified into what each team will have to work on.

- The management claims to have initiated an OKR (Objective Key Result) system which explores objective and key result areas to be achieved in 90 days which would eventually help the team to keep focus on vital goals, amidst daily operational compulsions.

In the same context, some examples were cited to display the effectiveness of these strategies - new business acquisition apparently was the strongest in Q4FY19, resulting in a 30% increase in yearly order booking; building on the competitive advantage in the IoT security space by enhancing and extending our honeypot to top research institutions in Singapore, Spain and the UAE etc.

Inducting financial discipline

A look at the movement in some key financial metrics, specially over the last one year, look encouraging… hinting at some success in the strategies implemented so far

- EBITDA to Operating Cash flow grew to 85% in FY 19, from 40% in FY 18

- EBITDA to Free Cash Flow grew to 79% in FY 19, from 34% in FY 18,

- Days Sales Outstanding (DSO) for FY 18-19 coming down to 100 days versus 120 days in FY 17-18.

- Efficient collection of receivables and optimal utilisation of cash has reportedly helped them to report good growth in operating cash flow and improved Days Sales Outstanding (DSO).

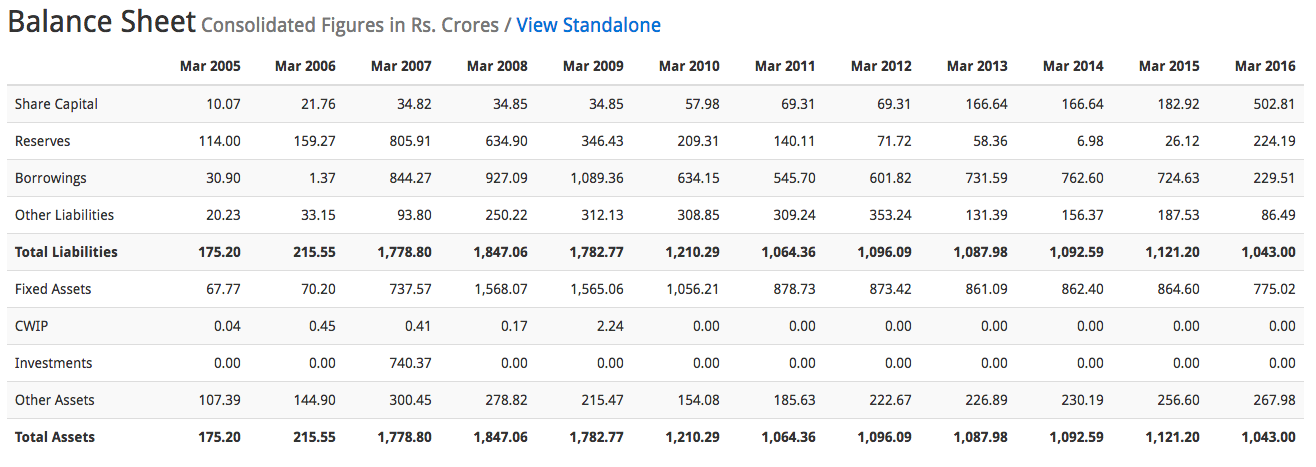

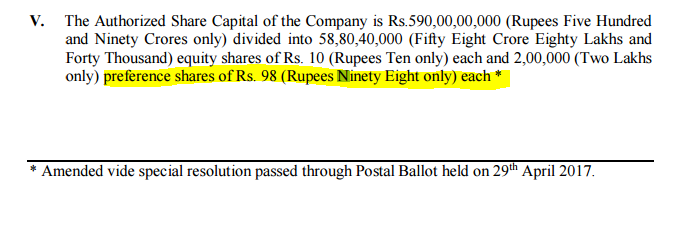

- 0 Debt - Having come out of the FCCB loans and related overhang which was on the balance sheet of the Company, they incrementally intend working on strengthening the balance sheet. The company has paid off Working capital loans from its banking partners in entirety, in Jan ‘19. As per the CFO’s guidance, the company intends looking at addressing their large equity capital base and make the balance sheet lighter

- The company has invested close to Rs. 14.7 Crores in IoT security and Analytics offerings – implying the intent of the management to invest into build required skill sets and capabilities for the newer businesses

- On the cost front, company is constantly monitoring and controlling IT costs using Cloud technology. At the same time, company will continue to focus on significant costs including Payroll and Travel costs and look at ways to optimise this further

These initiatives are apparently targeted to sustain profitability, without having to deviate from their focus from growth in their chosen areas.

While i shall continue to read and post my observations/comments in this forum, i would appreciate if other members (specially those who have been tracking this earlier) exchange their opinions as well.

P.S.: Ive initiated some small tracking positions in this stock.