Among the better concalls I have read this earnings season. Loved the clarity and candidness.

Arun Kumar has unequivocally and repeatedly said that the business bottom is behind, and that there will be a linear quarterly runrate of $60 million in the US starting Q1 (about 35% growth). This will come with improving margins due to liquidation of piled up inventory, leading to reduced warehousing costs and transportation costs, as manufacturing will adjust to demand.

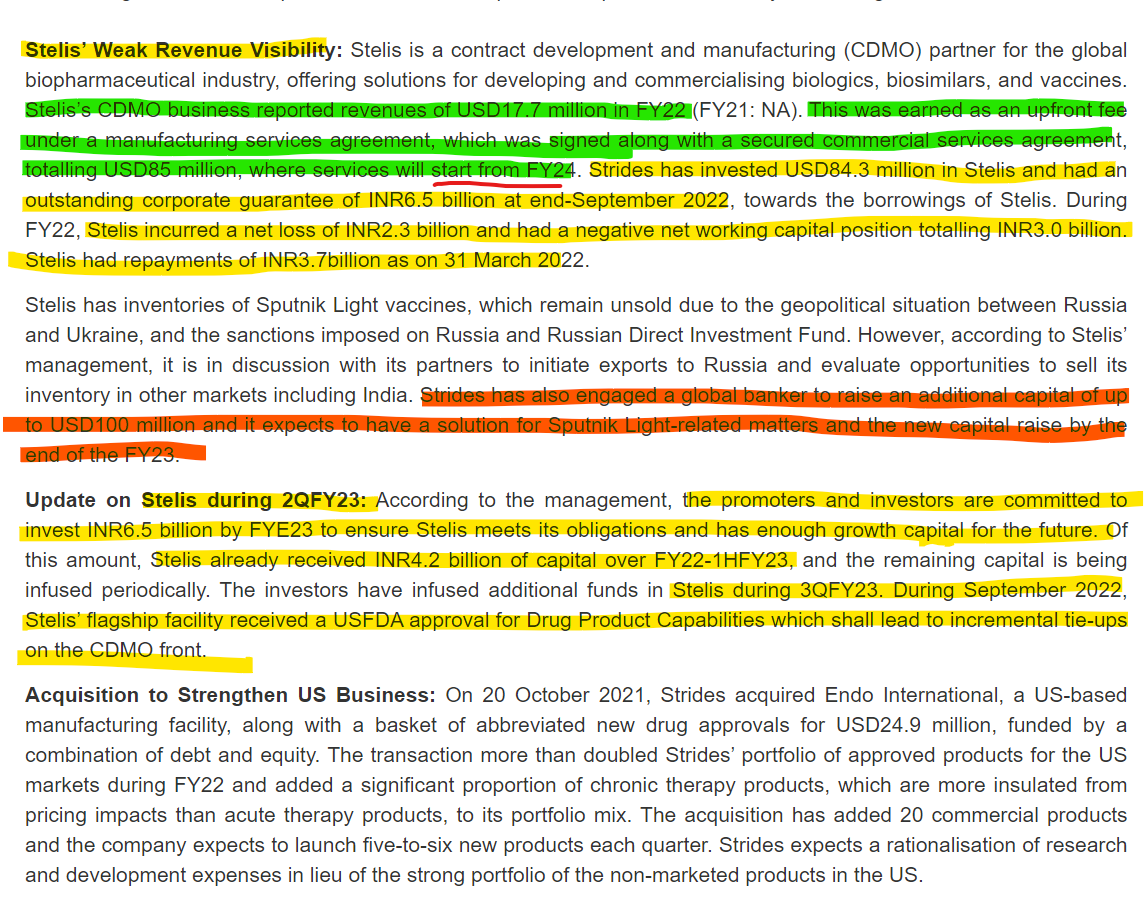

Other markets continue to grow, especially north Africa. Stelis has the overhang of Sputnik and RDIF, but apart from that the facility has scaled up well and has six customers signed for the coming year.

No major capex or R&D spends (in the US) over the next couple of years at least as they have a lot of approved products which will get commercialized. This will further improve free cash flow generation and they will use the money to reduce debt.

Disclosure: Invested from an average price of 550 odd and have been waiting for green shoots. Reasonably large position in the PF and has been a pretty painful hold. May add at the end of this quarter when numbers start reflecting the commentary.

Full portfolio Vineet Jain portfolio

5 Likes

Most Important snippet from the commentary for me -

This is an important step for us to bring our balance sheet size in order apart

from the fact that we have guided that we will reduce our debt by 1000 Crores. We have

requested and our partners in Australia have been very kind to bring forward our payments.

We expect to receive these payments in H1 against December 31 as previously contracted.

This is going to help our debt book quite a bit and also the fact that we have reset the

businesses to focus on large businesses where we have complete control on cash flows. We

would exit minuscule and tiny businesses, which do not move the needle for us for revenue

or EBITDA that and free cash generation will significantly help us achieve our stretched

target of reducing debt by a 1000 Crores and bring the company back to a very solid exit

run rate of EBITDA exit run rate to be under three times EBITDA. This is the task that we

have set for ourselves.

2 Likes

QFY22 Investor Presentation & Results

Concall Transcript

Strides

- Mr Venkatesh (ex CEO of Alkem and Microlabs) will take the charge of US operations, he will lead US sales and marketing activities

- Chestnut (Endo) merger is almost complete revenue contribution start from this quarter (Q1FY23, effectively from June 2022, will add $25 Million to the top line this FY)

- Endo has basket of 150 products that are ready to be launched along with another 20 new products from strides, so in total 170 new products

- Growth guidance of $250 Million for FY23 in US market, to achieve that they have to do a quarterly run rate of not less than $60 - 62 Mil.

- US volume pickup is strong, this will help to reduce the large piles of inventory (this will help in improving cash flows)

- Customer (Arrotex - 10 years supply agreement) agreed to pay 1000 crore (expected to receive this by H1 FY23) in advance of six months, which will be used to reduce the debt ( Gross Debt post this will be 3x of EBIDTA)

- Exit minuscule and tiny businesses, which do not move the needle for us for revenue or EBITDA and focus more or large opportunity size

- R&D spend will be reduced substantially instead focus more on the products that are approved but not launched or the ones that are in pending approval phase (new ones are picked based on the opportunity size )

- Exited few markets like Canada and Europe, appointed dedicated sales team in Europe (why they have exited and again they are investing in sales team ? )

- Next leg of growth mostly from African markets (some from partnering with big players who wants supply chain certainties)

- Gross margins range 60 to 65%

Stelis

-

Stelis has started operations with two divisions CDMO and Biologics (Vaccines)

-

In CDMO they signed up 6 customers in FY22 and they signed up 6 more recently so total 12 customers (what is the revenue contribution from these ? )

-

USD $100 Million order book in place

-

Year and half away to break even the business

-

Sputnik stock has another 12 months validity, working with the Indian government to push these stock to RDIF (Inventory value is $40 Million)

-

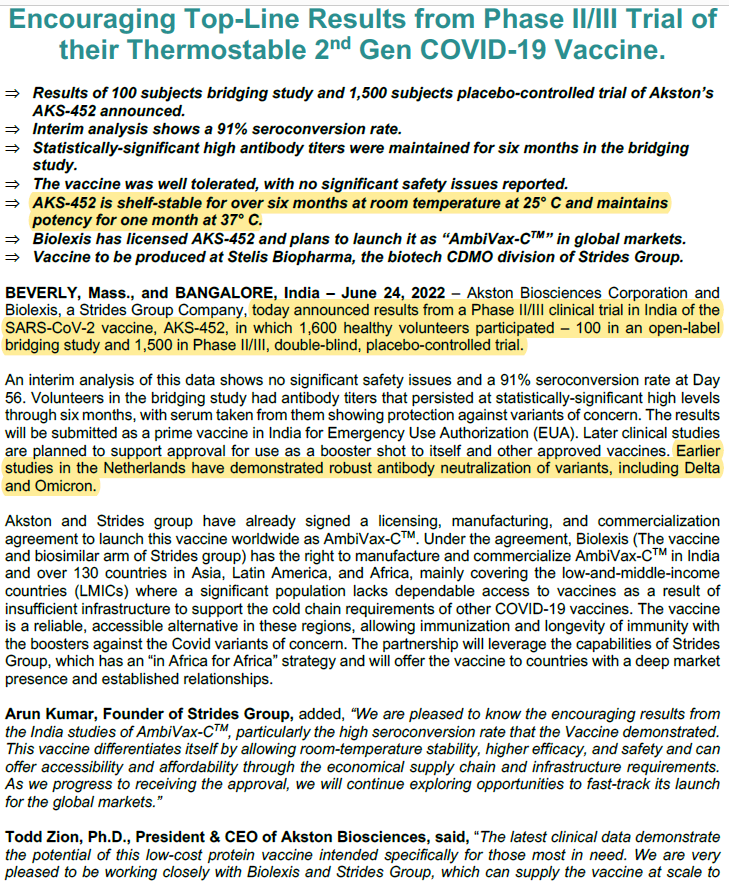

AmbiVax from Akston Bio vaccine is in the pipeline (waiting for the final approvals, this vaccine can be stored below 25*c temp)

-

Two plants are inspected by EU (approvals are yet to come) , USFDA audit is pending

-

Arun Kumar sounds desperate to win back the trust of the share holders , one bold statement " so we will be more than happy to take calls from any individual investors or analysts who may want to ask us questions "

Puducherry Plant still under regulatory concern

Company strategy is still inogranic growth (Endo), the only visibility is from Africa

Having capacities (Strides) doesn’t gurantee orders

Huge dent if they can’t make any money from Sputnik

Ambivax (there are many players and yet to receive approvals)

Edit : 16/6/2022

Vaccine Update Edit 24/6/22

Link

12 Likes

Hi @NIRAJ_5761, could you please share where you’ve got this information from and do share the document / source from where it can be verified? I don’t see anything in the company’s disclosures to this effect.

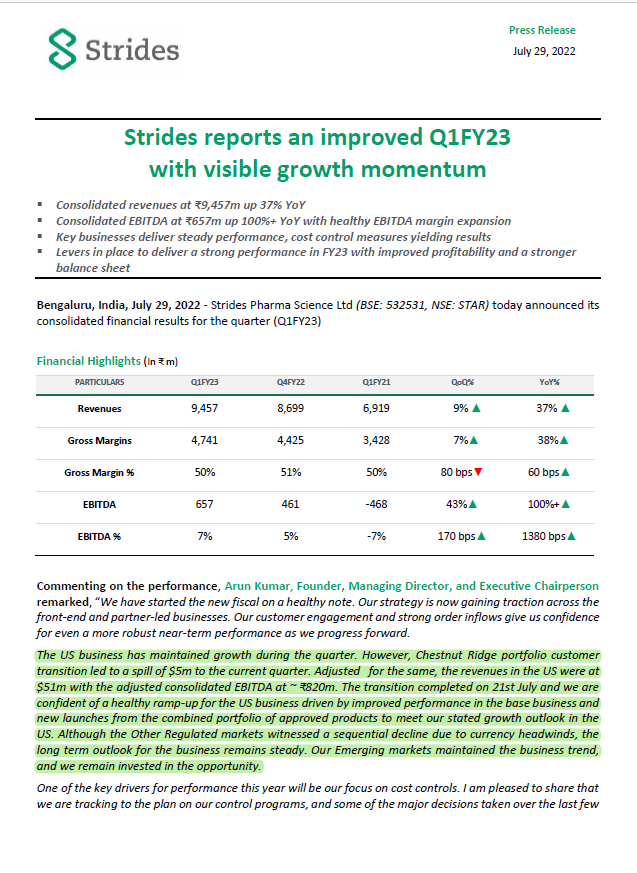

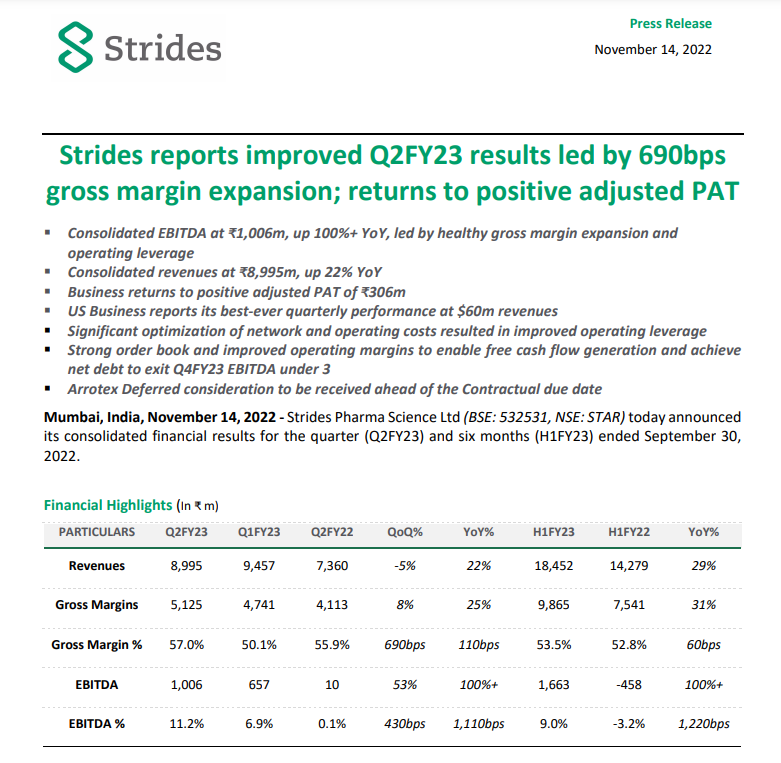

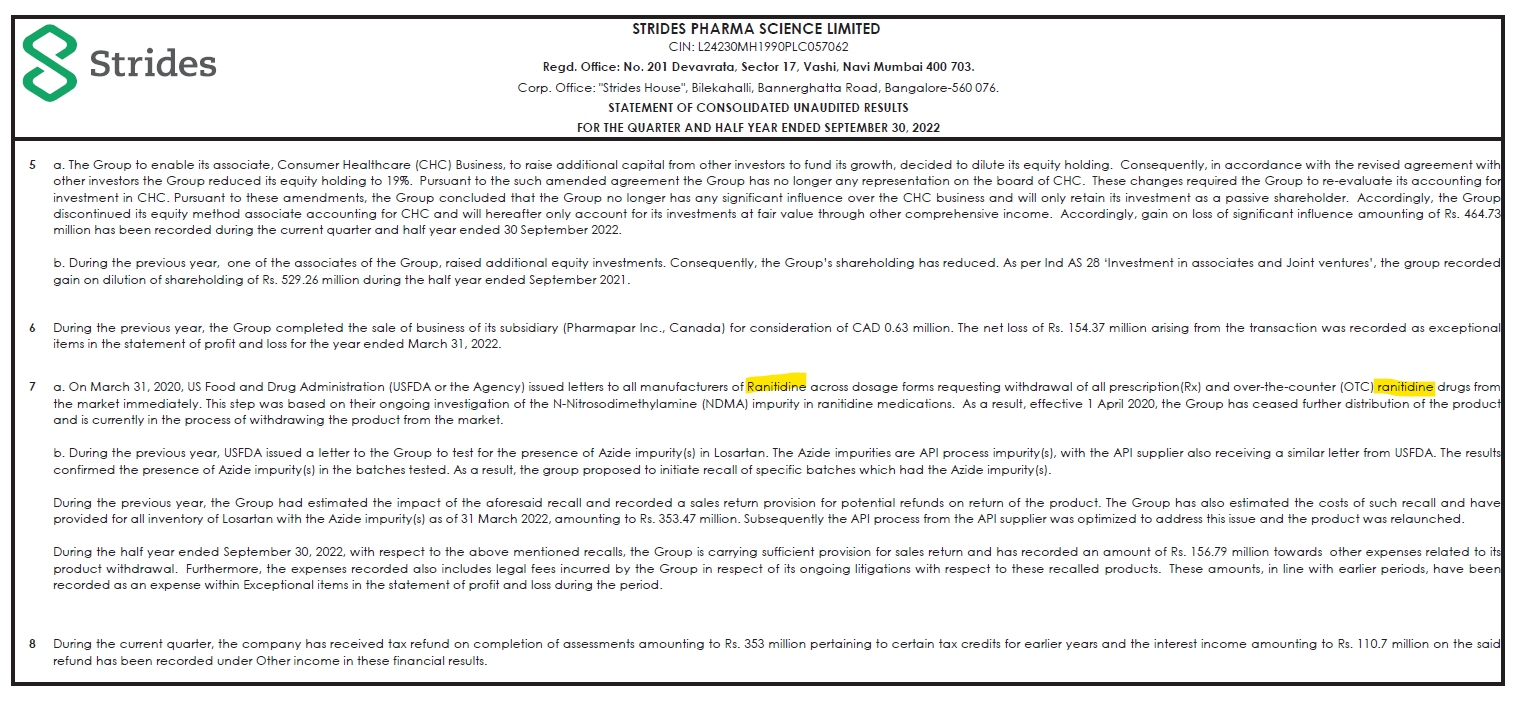

I tried a lot to find out PAT for the current quarter. They are talking a lot about all things except PAT in their press release.

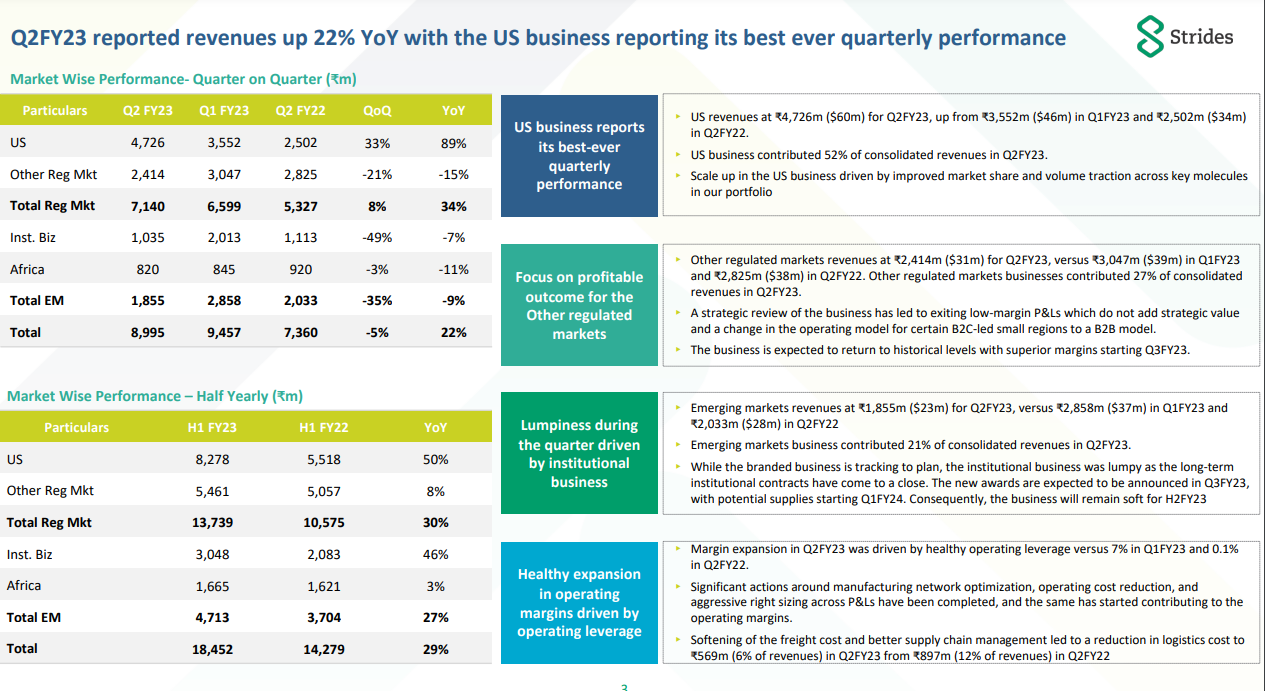

Attended the concall partially. They reiterated many of these points - US pricing pressure slowing, other regulated markets and emerging markets growing, Endo launches picking up etc. Spoke about moving back to their erstwhile strategy of focusing on complex / difficult to make generics as opposed to “me too” products which they had resorted to post covid to balance the over-reliance on their acute portfolio.

They will bring the gross debt down to 1000cr by this year. Arun Kumar has guided for 20% EBITDA margins by six quarters, which is where they used to be pre-covid. Essentially the business seems to have made a clean bottom and should be on the way up from here, barring any unforeseen events.

Stelis is scaling steadily but no news on Sputnik money yet. I think we as investors should write it off.

8 Likes

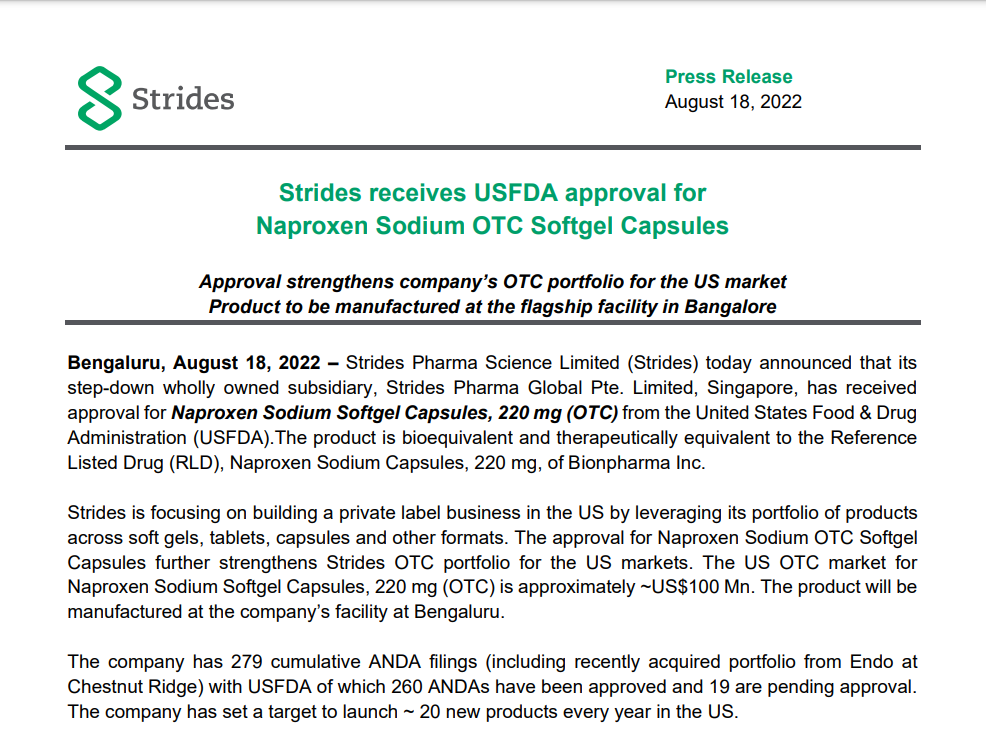

Press release on USFDA inspection for Singapore facility. Just as a reference - FY22 revenue from US was $157 Mn. This will support company’s outlook to achieve target of $250 Mn. revenue from US for FY23

3 Likes

ICRA has downgraded Long Term Rating whereas reaffirmed short term rating

https://www.icra.in/Rationale/ShowRationaleReport/?Id=115015

Some important snippets

Stelis had Sputnik vaccine inventory of 23 million doses (costing ~Rs. 280.0 crore) with a limited shelf life till March 2023. While Stelis is in discussions with Russia’s sovereign wealth fund, RDIF and the marketing partner, ENSO Healthcare LLP to liquidate the stocks, high uncertainty continues to prevail around the same. In the worst-case scenario, Stelis may have to resort to writing off the vaccine inventory, if the same is not liquidated within its shelf life.

Stelis needs to repay the working capital loan in Q4 FY2023 in addition to the scheduled repayments of its term loans, resulting in total principal repayment of Rs. 584.0 crore in FY2023. ICRA notes Stelis’ latest equity raise of USD 155 million, of which USD 90 million was received over FY2021 and FY2022, and Rs. 213.3 crore was received during April-August 2022, which was utilized for partially funding the vaccine project and debt repayment obligations. Further, the balance committed equity of Rs. 271.8 crore is expected to be received soon for meeting the upcoming repayment obligations as well as funding operating losses. In addition, Stelis has plans to raise further equity by Q4 FY2023 to support its business operations and fund its repayment obligations. However, given the current uncertainty in receipt of cash flows from the Sputnik vaccine and the nascent stages of its CDMO business, the timing of further equity raise to meet its sizeable debt repayment commitments remains extremely critical. Any delay in the same could weigh in on Strides’ cash flows as majority portion of Stelis’ term debt is backed by a corporate guarantee from Strides.

2 Likes

They have also spoken about how the 500 odd crores from Arrotex coming in, or the equity infusion from the promotors coming through soon will ease the liquidity position. They’ve alluded to improvement in business performance in not other regulated markets and the positive impact of the cost reduction measures. Nothing that we didn’t know coming up in this report IMO.

I believe that the business has bottomed and any positive surprise on Arrotex funds or reduction in price erosion could trigger a sharp rally.

Disclosure: Invested through a painful 12 months and hopeful of a turnaround.

3 Likes

The improvement continues. Back to profitability. US business has its best over quarter. Dare I say that the base formation is done and the stock is ready to break out?

6 Likes

Thanks for sharing @Rafi_Syed. A very important update!

This report summarizes the situation with Stelis well. No more money from Strides - separate investors and promotor warrants will put in capital as needed. A large part of the money needed is already raised. The business operates on negative working capital cycles and facilities are forward booked. The only unknown is what happens with the Sputnik stock and the timing of the Arrow receivables. Hopefully no more black swans and the numbers should continue improving and the balance sheet will start looking more healthy.

Half glass empty : Stelis right to win the business, having capacities doesn’t guarantee right to win. With zero past track record it is really very very hard to to win in BIO space. Stelis and Gland Bil infra. both are burning cash , where as later has comfortable cash levels.