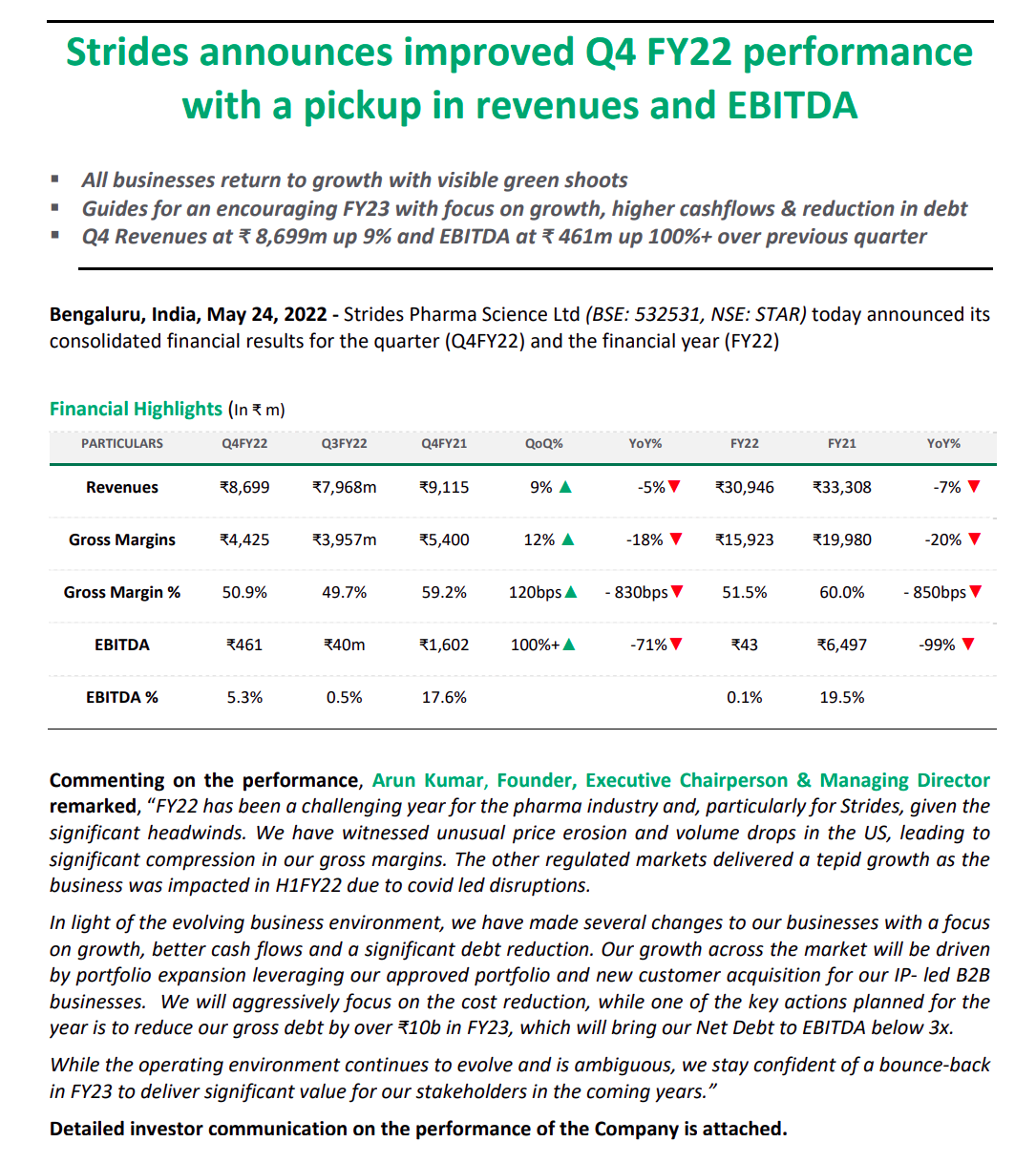

It was an upbeat commentary from management with following key highlights

US pricing has stabilised and they reiterated $ 250 M guidance for FY 23 starting from Q1FY23 itself.

High inventory cost is being absorbed in current execution and will normalise over next few quarters.

Freight costs is stabilising as they have started using Sea freights

Cost control measures are showing results and will improve as they go further

Chestnut facility was inspected by US FDA and was cleared with 2 minor observations. They will start adding to revenue from current quarter onwards.

Stelis demerger project is on schedule and bankers are looking at it for FY 23 implementation

Stelis is engaged with few key customers on CDMO deals

Overall on a stable basis US revenue will be around $ 60 M , Other regulated markets at $ 40 M, Emerging Market at $ 30 M in FY 23. Gross Margins in US would be at 55%

INR 534 crores tranche from Arrotex is likely to be received in March 2022. It was scheduled for Dec 2022 as per agreement

As operating leverage improves and with additional Equity infusion from promoters debt levels should normalise and reduce going forwards. Focus on Debt reduction and balance sheet strengthening is key area for management

Management is confident on FY 23 revenue and growth basis launch of new products and not dependent on approvals for new products. They have nearly 70 products approved and not launched earlier hence confident on revenue and growth overall.

Can’t agree more… Management was upbeat and they see green shoots in US businesses…which generally drives their profitability… They are happy with the products they have let go in past and on track with future plans…

Q4 of this year may not be so good though better than Q3 but from Q1 FY23… Things are expected to turnaround…

Gross Margin of 55% was the highlight of the call… 200 crores from promoter for 485 per share icing on the cake …

Disclosure: Invested and biased… following closely

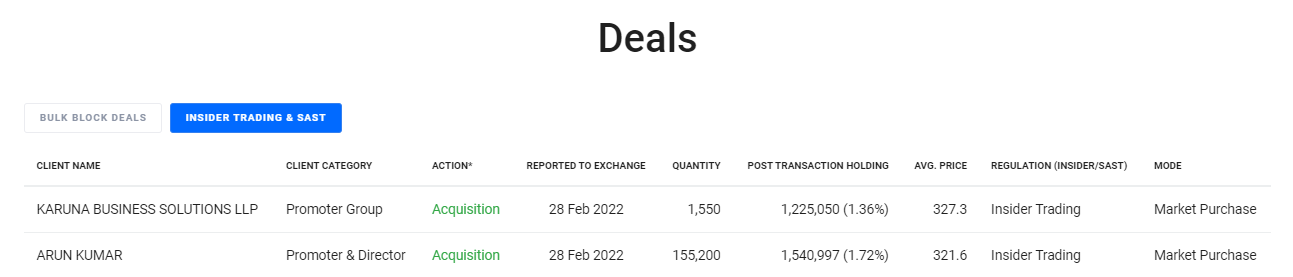

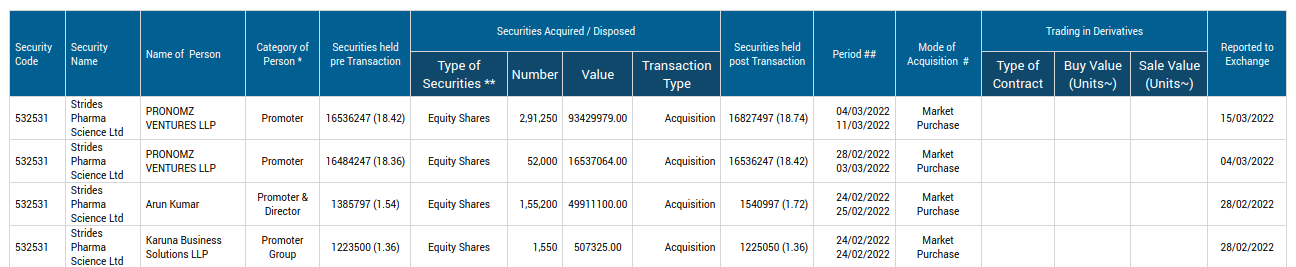

after buying the shares , this is pledge declaration , so is it something shares were purchased on loan and now loan security is based on this pledge , can someone please clarify significance if these events ( could be a novice type question as ive little understanding on these transactions , pls flag/delete if not adding any value, thanks)

He purchased 1.55 lakh shares and has now pledged 62000 shares. So it is unlikely that the entire purchase was on loan for which present pledged shares are acting as security. He could have pledged his shares for any reason, and potentially to apply to the equity warrants that they are going to infuse at about 50% premium to the present price. No point speculating in my opinion.

The purchase of a decent chunk by Arun Kumar is a big positive in my view, especially in the present times of peak pessimism.

Disclosure: Invested and adding. Not a recommendation.

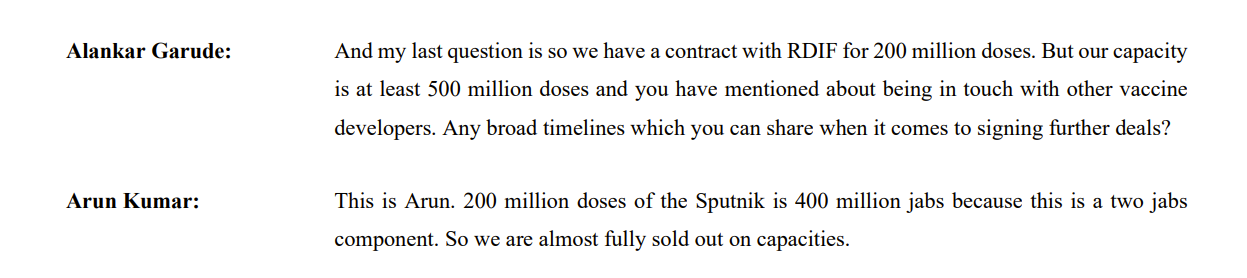

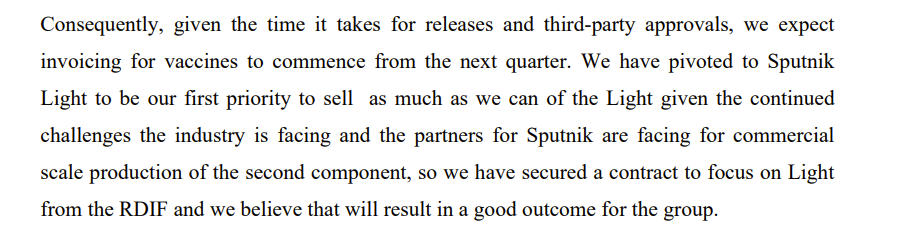

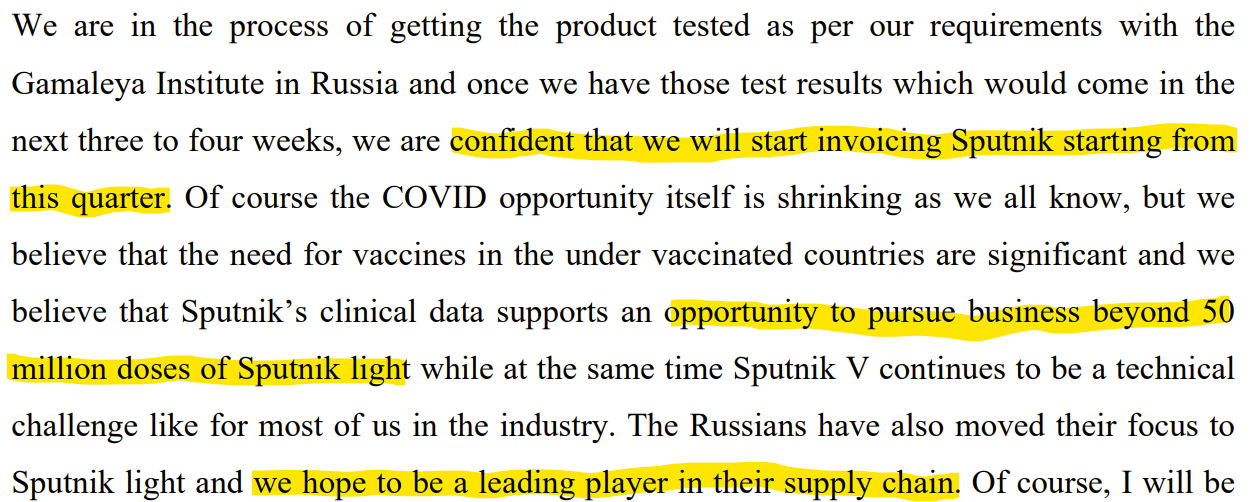

In Q2FY22, things were looking up, as they had solved the scaling problems mentioned higher up in this thread, and were tactically focusing on the Sputnik light contracts:

The story looks to be that Sputnik was the main path to profitability, allowing Stelis to achieve breakeven. They were going to eventually shift away from covid vaccine manufacturing to gene and cell therapy, transferring capabilities and leveraging the new CEO’s network. Now in the previous concalls, Mr. Arun Kumar said that the details of the contract such as payments and the effect on the balance sheet was confidential.

The recent sanctions on Russia question the RDIF’s ability to meet its financial obligations. The IDMA has said that receiving payments from Russia is now difficult, and likely to drag on for a while. This calls the entire contract with RDIF into question, and the future of the Sptunik vaccine. One asks if any dues need to be written off, and how much consideration Stelis received before Q3’s concall.

As a corollary, the plan was to list Stelis after it became profitable. If profitability is now delayed on account of the sanctions, it’s dependent on new CDMO contract wins with other clients. One also wonders if the timeline for listing will be pushed.

Inviting comments from those that have tracked this closely. It’s amazing how much bad luck Strides has had in the last year.

Promoter is buying from market ( and constantly pledging). Seniors, I dont get this logic of pledging just after buying. They are pledging with Kotak and IIFL. Is it “Heads I win, tails I dont loose” pledge shenanigan?

I think they are trying to increase their shareholding at the weakest point (price) by buying under leverage as they need only 50% cash to buy stakes in the above way. Just my hunch, I always thought Arun was very close to jumping ship after taking stellis public if this war did not happen. Now with the RM margin crunch, the Sputnik issue adding up to the long list of issues, as @Chins already told I cannot imagine how much bad luck this company can accumulate

All vaccine infrastructure is Fungible in nature, I think both Strides and Gland (who own the highest volumes) might loose big on initial investments. But this opportunity gave them to setup the much needed infra to take up future opportunities. More than infra. the technical know how and build the team and ready for next set of opportunities. Gland and Stirdes both mentioned this many times in their calls they are actively looking for Bio CDMO opportunities.

Apologies @Chins for not being able to respond to this earlier. The past few weeks have been a bit crazy at work and for the first time in the last two years I am realizing how difficult it is to do justice to investing with a full time job!

I pretty much agree with all your points and unfortunately have no more information. The ability for RDIF to make good on pending payments, if any, and the future of Sputnik as a whole are now completely uncertain. Like you mentioned, Arun Kumar has been extremely cagey about divulging details of monies received so far so unfortunately there is no way of knowing where things stand on this till the next concall. It is also likely that the operational break even achieved recently will fall back and the path to profitability will be delayed. I will not be surprised if the demerger gets delayed too. The bad luck just doesn’t seem to go away!

Most of this uncertainty, and more, is priced in though in my opinion. Especially with contributions starting to come from Endo facilities and the slow easing of price erosion that Arun Kumar spoke of in the last call. Also the pending 500+ crores from Arrotex due in March will help the cash flow situation. Hopefully this money will be used to repay some debt.

Arun Kumar certainly does believe that the bottom has been made which is evident from his trading activity in the past few weeks. I guess wait and watch is the only sensible approach for now.

Ananth quits in 2 years and that too when things were looking to bottom out, and turn around was supposedly around the corner. Arun Kumar’s statement that drug prices have hit their bottom, and they had completed acquisition of Chestnut facilty, it appeared that finally something was to happen. And now you get this news which casts the shadow on near term performance and strategy going ahead.

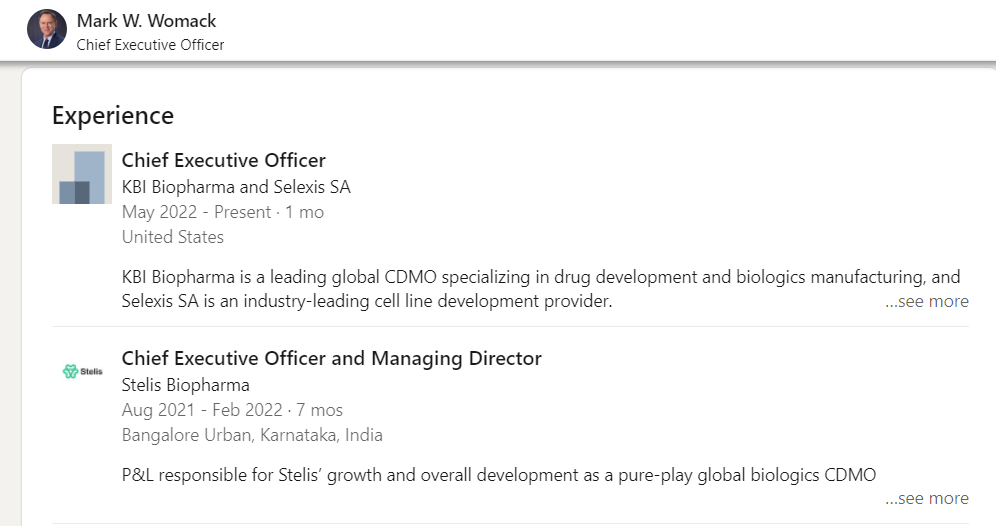

All three erstwhile Arun Kumar companies have had CEO changes in the past few months.

Is this a coincidence, or a planned strategy?

Did they all quit or were they asked to go?

There is no way of answering these questions till one hears from the company, probably on the next concall. That said, Arun Kumar is coming back into an executive role is a welcome step in my opinion. This does lay to rest, at least for the medium term, speculations of him wanting to take an exit and focus only on Stelis, which has been the popular theory for a while.

In my opinion, there is no point speculating. Best to wait and watch.

“We are proud to state that after having been granted due approvals by the Government of India, we started manufacturing Sputnik Light in India and produced no less than 2.5 crore vaccine doses. However, due to several constraints related to Russia, these vaccines are lying unsold with us at present.”

Kumar requested that the government should acquire the available doses, failing which these will get wasted and the company will face a huge financial loss. “We request the Government of India to procure our readily available vaccine and administer it to the people of India or donate it to other countries under the India Aid/Covid Maitri programme.”

They have less than a year to sell 25 million doses of the vaccine. Articles written a few months ago suggested that demand for Sputnik Light is weak, as hospitals administer boosters based on doses patients had previously. This works against Sputnik.

I’d imagine the probability is higher that these doses are left unsold, than the probability of them successfully getting Sptunik off the shelves.

To summarise what Arun Kumar has on his plate at the moment:

Ananthanarayanan has left Strides.

Mark Womack has left Stelis.

Major near term revenue driver for Stelis has fallen through.

Ramp up at Chestnut Ridge ongoing.

Aurore merger decisions at Solara, and subsequent focus on turning the company around.

That’s a significant amount of effort for any person’s bandwith.

As an investment, Strides is at an all time low on book value (and on price to sales):

It’s likely book value will deteriorate by around Rs.20-25 per share after Q4 results come out, but valuations are at rock bottom. On earnings, FY22 posts an incredibly low bar for FY23, and one wonders whether the company will be valued anywhere near what it did in the past, with the landscape of US generics being different to 5-6 years ago, the numerous missteps of FY22, and the crown jewel in the thesis facing near term headwinds.

At the same time, would be nice to follow the ANDA filings to see if they genuinely move towards complex products (by the CACTVS metrics Sahil shared), and also see how Solara improves.

Good update on the business getting back on track.

Headwinds seem to be going away and business is expected to do well going forward.

I like that management has its focus on reducing the debt first once the business normalizes. There can be a few triggers for business to perform well in future quarters.