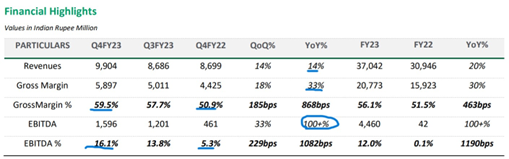

Strides reported strong Q4FY23 results and lay the foundation for a promising FY24

PAT impacted by one-time impairment at Stelis mainly related to Sputnik

The US market, led by new product introductions and solid base performance, generated its highest-ever revenue of $232 million with significant margin expansion.

With the receipt of Arrotex proceeds and cash from operations, the total gross debt has reduced in FY23, and Net debt to Q4FY23 Annualized EBITDA was at 3.4x, nearing the targeted net debt to EBITDA of under 3x. From 8.3x net debt to EBITDA in Q1FY23, Net Debt to Q4FY23 Annualized EBITDA is 3.4x, closer to the targeted ratio of 3x. This was mainly due to the increase in EBITDA.

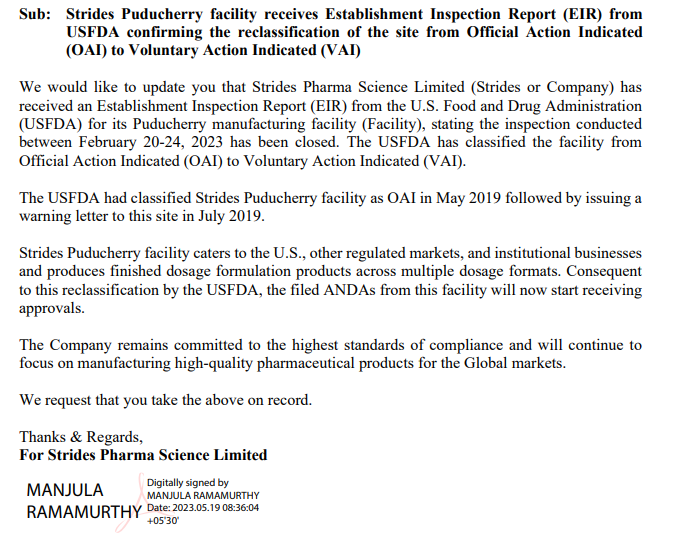

Received Establishment Inspection Reports (EIR) from the USFDA confirming the successful conclusion of inspections at four of their five USFDA-approved manufacturing sites (Bengaluru, Puducherry, Singapore, and Chestnut Ridge (US). Additionally, the USFDA has reclassified the compliance status at Puducherry after lifting the Warning Letter issued to the site in June 2019. Consequent to this reclassification by the USFDA, the filed ANDAs from this facility will now start receiving approvals.

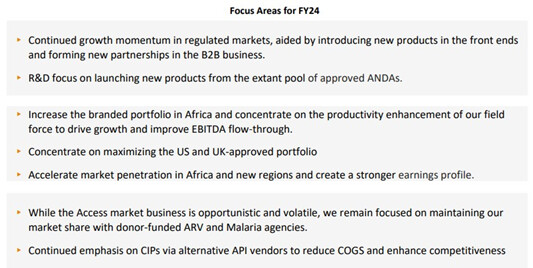

“We are confident in continuing FY23’s growth momentum and are on track to continuously improve the quality of our earnings while strengthening our balance sheet in FY24.”

FY23 Revenues in the US hit a record $232 million, surpassing pre-Covid-19 performance levels

19 of 60 commercialized products have been positioned as #1 in the market

Strides and Stelis combined target debt reduction of INR 5,000m in FY24

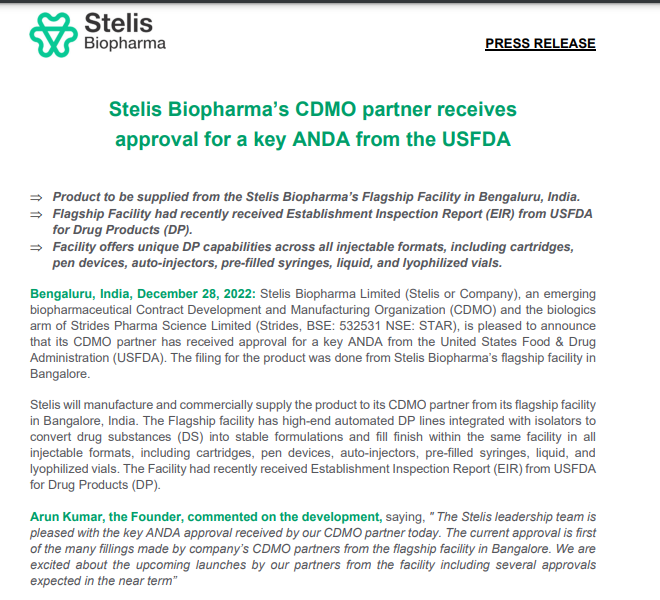

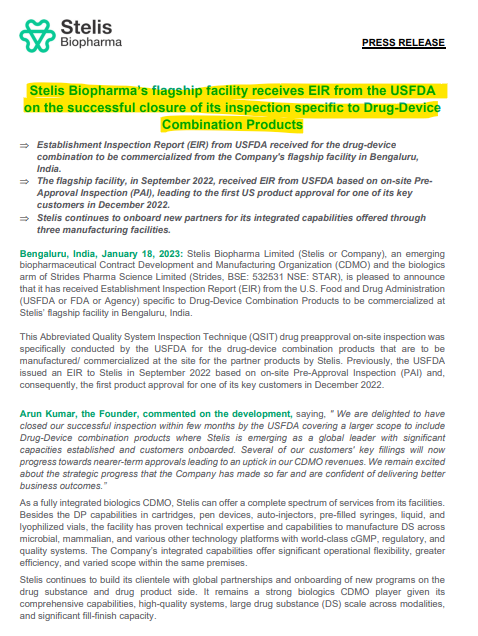

USFDA issued Establishment Inspection Report (EIR) to the Stelis Flagship facility for GMP and drug-device combination products. EU-GMP also approved the facility during the year. The facility also cleared several customer inspections, including from large global companies.

Considering that the first partner product for Stelis received USFDA approval, the company will begin generating revenue from commercial supplies (CSAs) in the second half of FY24.

Stelis is in losses and eating the cash flow from strides, as and when this loss situation turns around to profits or even a breakeven. It will lead to better cash flows, thus faster debt repayment and lesser interest payments. This will elevate the net profits and lighten the balance sheet. Another thing is Stelis is a higher margin than Strides, but is lumpy in revenue generation.

confident of increasing their EBITDA from INR446 crores to about INR750 crores in the upper range and INR700 crores at the bottom of the range.

Planning on reducing the higher cost loans with lower cost loans

The first commercial sales for stelis will start in June as the partners have now received 2 product approvals from this site for the inspection.

Strides and Orbicular enter into a strategic partnership to jointly develop, manufacture and commercialize nasal sprays for the global markets.

The partnership will commercialize four nasal sprays with a combined Global IQVIA market size of over $400m.

it will take 3 years to launch the product.

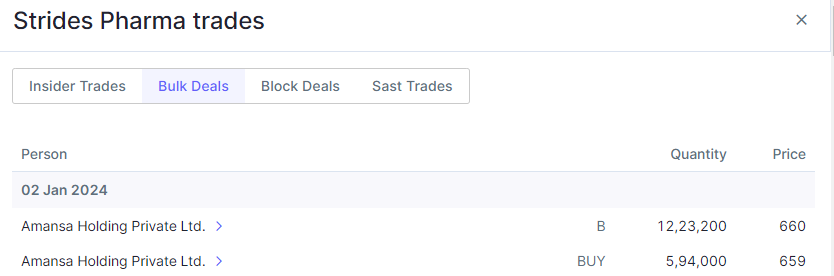

The stock has run up 50% from its lowest point at INR 268. Maybe all the reversion is done, maybe not.

Beware, even if the facilities of strides have been cleared by the USFDA, it doesn’t mean they won’t come tomorrow to shut their plant down again.

The USFDA risk is too big to ignore.