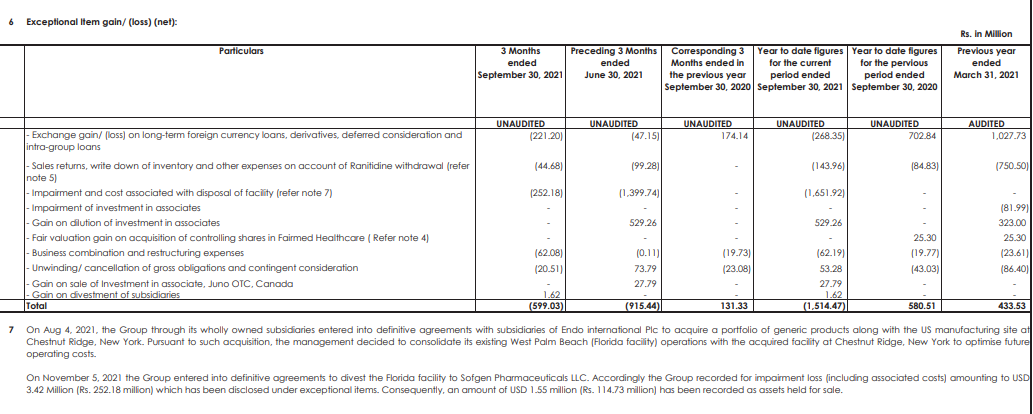

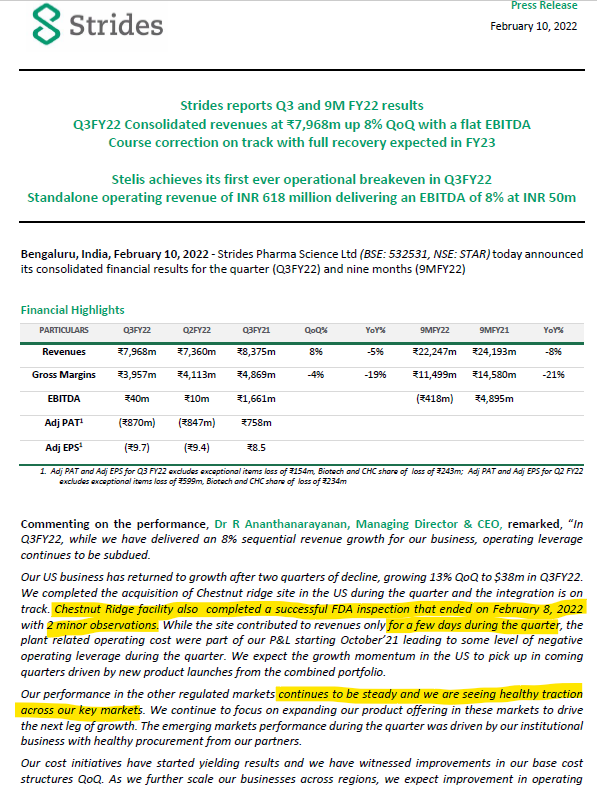

Details of the exeptional loss - 25cr impairment cost from divestment of Florida facility and 22cr exchange loss (not sure why this is so high). The company has also added 182cr of debt in the quarter.

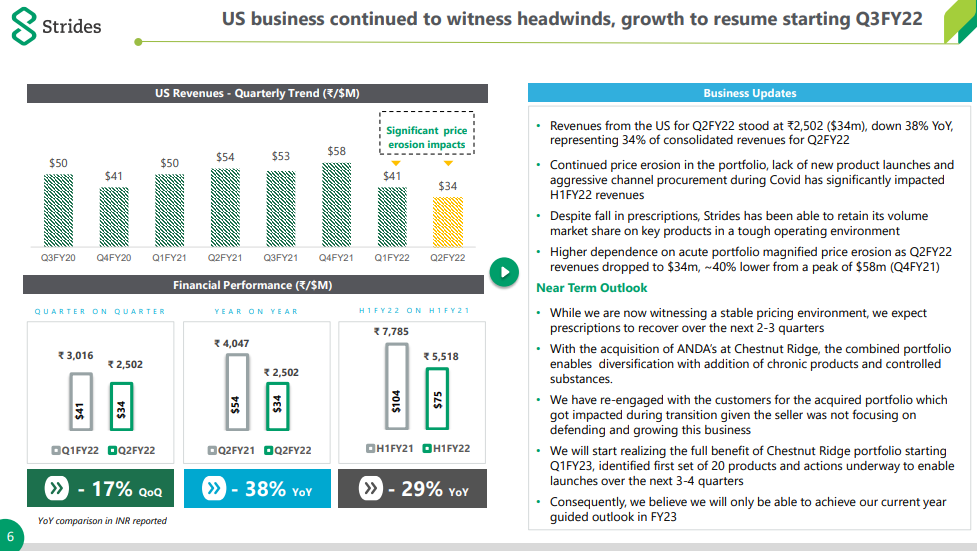

Other regulated markets and emerging markets did well. US business continues to struggle. CEO says “Given the volatile dynamics we believe we will only be able to achieve our current year guided outlook for US in FY23”

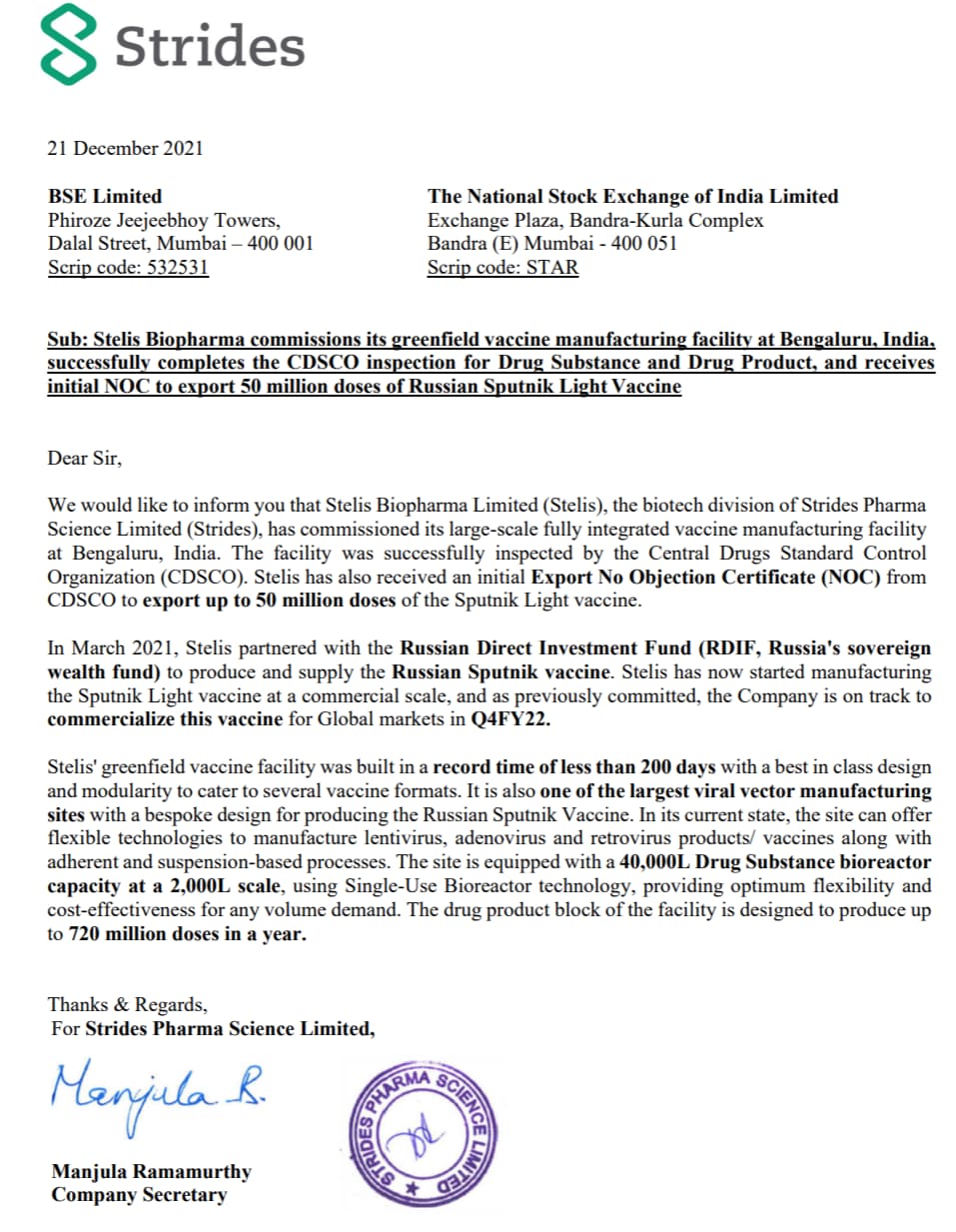

On the Sputnik manufacturing, they say that the first component has been manufactured at the commercial scale and they expect to commercially launch the vaccine within Q3FY22. Also on track to on-board at least one CDMO Contract on vaccines by Q4FY22.

No information on demerger.

I have work calls this afternoon so may not be able to atend the concall. If anyone does, please do post notes. Thanks

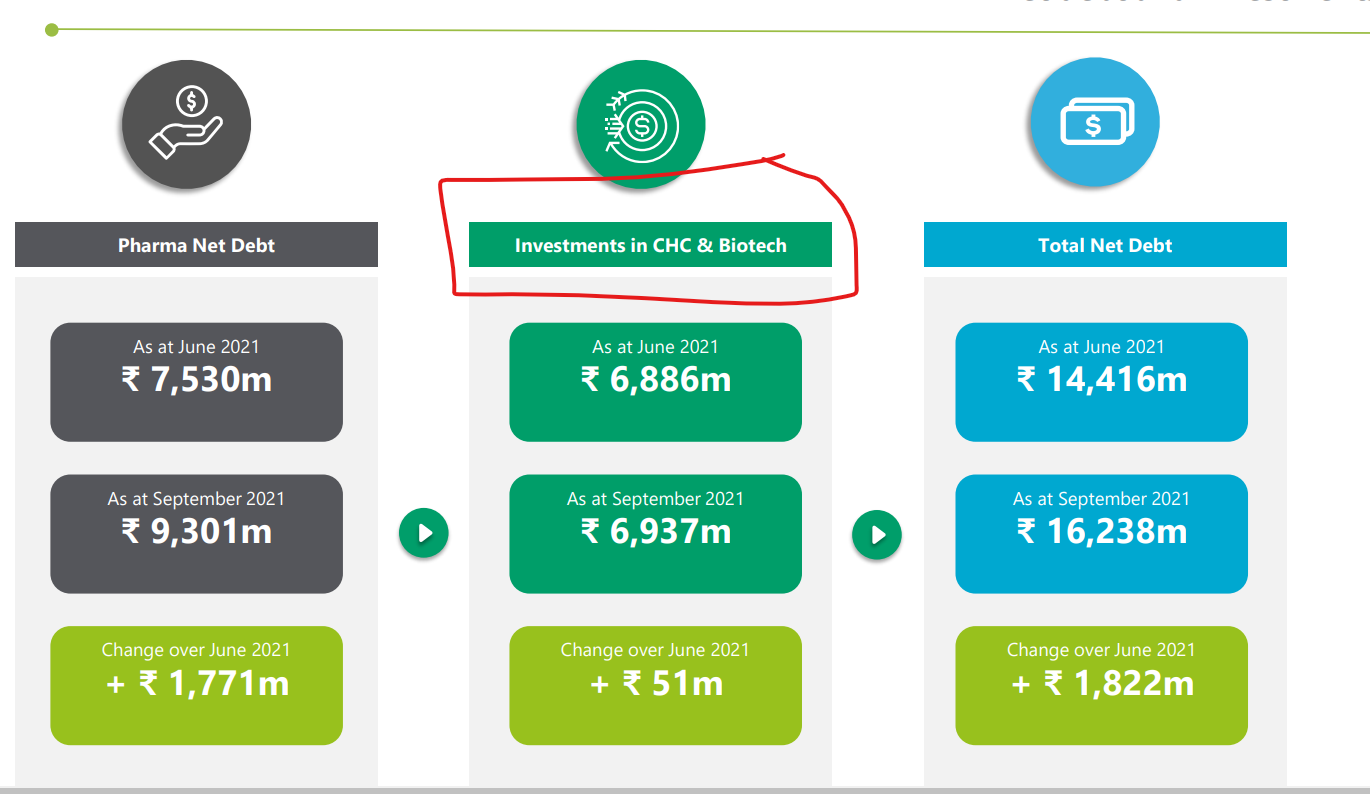

Any idea about this additional debt , what is CHC ? , I am assuming Biotech is Stelis , and promoters said they are not going to inject any Strides money to Stelis , capital is funded via equity dilution in stelis

Stelis demerger/listing still undecided. H1 FY23 is when we can expect this to happen- will do what is best for Strides shareholders.

Not sure what that means.

Pricing pressures to improve in the US markets going ahead Q-o-Q. Full recovery to take time and expected only by FY23.

Acute portfolio still highly affected- specially in the US and company is waiting for the prescription rates to pick up.

They believe the business bottom has been made in the USA. Expect stable pricing from now on. Though qualified saying covid can’t be predicted.

Endo has 60% chronic products which will start generating revenue from next FY onwards.

All in all a few tough months in store for shareholders.

@Rushil Any details on when Endo’s largely chronic portfolio will start contributing and by when will it be fully integrated?

Also did they say anything about improvement in realizations next quarter onwards? I understand that full recovery will take time, but I’m trying to assess if there is a chance for things to get worse or if the business bottom has been made. If it has, there can be operating leverage over the next few quarters, specially since freight costs have also started to come down.

Still a few quarters away from recovery in management’s view, target of $225m - $250m is poatponed from FY22 to FY23.

Acute therapy focus is not paying off well – dramatic drop in demand in US (30 -35% drop in certain products).

Prices expected to stabilize going forward, have probably bottomed out.

Endo:

Acquisition of ANDAs completed – too much aggression on pricing due to high buildup of inventory.

$50m revenue contribution expected now, down from $75m at time of acquisition, due to high competition pressure.

Endo portfolio has chronic products(90 products) and controlled substances(13), will help ease out pressure and diversify business.

Stelis/CDMO:

Company only has investment in Stelis, does not book revenue, reports it below EBITDA line in P/L.

Completed dedicated viral vector facility – Sputnik manufacturing here, have successful scale batches, invoicing in vaccines will commence from next quarter.

As soon as government allows exports of vaccines. company will start that.

CDMO is on track, and will break-even soon (break even is $20m).

Separate listing/demerger is possible in H1FY23. Management said “will do what is best for shareholders”

Logistics:

Logistics cost during the quarter were up 20% QoQ and up 135% YoY, logistics cost as % of sales at 12.2% for Q2FY22 versus 4.8% in Q2FY21. Has moved back to sea freight from air freight, and expects costs to come down next quarter.

Other Highlights:

Other regulated markets have improved – will continue to grow.

Pondi facility status continues to remain the same

182 cr net debt increase, but expect debt levels to come down

Strides remains a majority owner of Stelis(33%) alongside TPG Growth , Tenshi Life Sciences ,Route One, Think Investments etc

This might be the reason of delay and no clear indication of Demerger even after announcing it around Jan this year as they are not in position to decide it single-handedly …

Anyone has access to Stelis accounts ? We have to understand

Revenue / Gross Margins / EBITDA / PAT

Gross Block (They have spent massively )

Intellectual Capital (How many scientist / R&D staff )

Why kind of ANDA approvals do they have ?

In my opinion Sputnik is a non starter for Gland and Stelis, they keep on saying but I have my own doubts about the contribution by this much hyped (Vaccine cell line setup itself is not going as expected, all the major vaccine brands producing and selling covid vaccines without any issues ( in india we have covaxin, covishield and Zydus) . Other than sputnik no vaccine is produced in India via CDMO route that are innovated outside india with the exception of Covisheild ) . Covisheild is no longer given in UK(many people that I know are infected even after two shots , people say pfizer has more immunity than covisheild , again we have to see the data to understand this ) now they are giving either Pfizer and Moderna .

On disclsure side Arun Kumar failed once again, first by not disclosing the closure of Forida plant and then failed to manage the logistics cost / giving guidance, in the last concall they said they will announce more details about Endo (how much they paid and how many basket of molecules etcc) since then they haven’t gave any details . Details are only disclosed in today’s IP.

In order to command the valuation you have to support the then with numbers i.e that is your earnings (Nykya got that kind of response because it is the one of the few listed platform based asset light business that are profit making ) . At the moment nothing is clear on Stelis side, I think it will be a wait and watch game for both Strides (no doubt this will be lapped up by PE

Arun kumar wants decent valuation for his stake in Strides and then at the same time street valuations that are given to Biotech based companies.

Stelis Biopharma commissions its greenfield vaccine manufacturing facility.

NOC from CDSCO to export up to 50 million doses of the Sputnik Light vaccine. (no update on Sputnik 2nd dose)

Looks like now it has bottomed out at these levels. At 410, its around 1.12X sales of last year (assuming there will be no degrowth in topline from last fy.)

This interview with Reuters was held almost a year back from what I recall. Ambitions to list on Nasdaq have no bearing on demerging now. They can very well demerge now and also list through an ADR on the Nasdaq in the future. Lets not speculate and wait for more information on the demerger to emerge.

Looks like the business bottom is behind us. Chesnut Ridge facilities coming onstream should lead to operating leverage in the next few quarters, and if the pricing pressure continues to ease, we can see big improvements on low base in Q1 FY23. Any clarity on what s happening with Stelis will likely improve perception further. At one time sales, looks like good risk reward IMO.

Anyone attending the concall, please do share a brief of the discussion. I am at work and will have to skip.

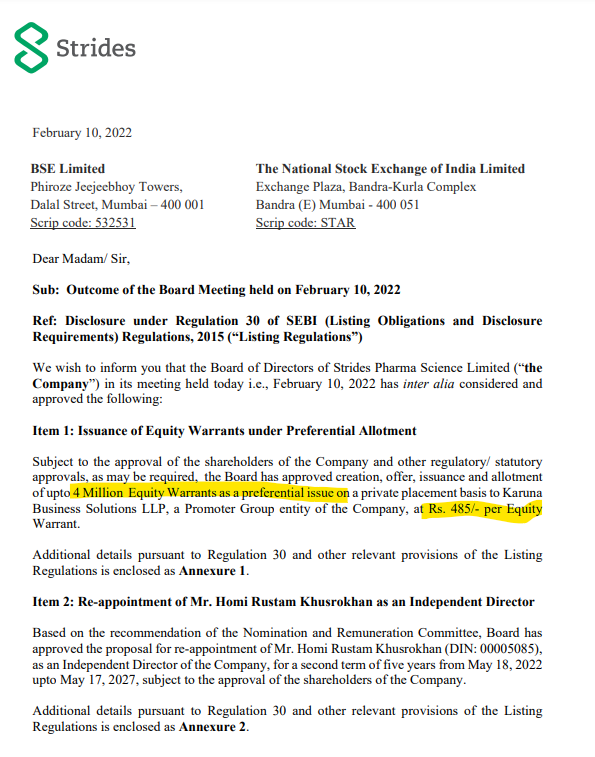

Why would the promoter entity subscribe to 4 mio equity warrants at INR 485 when they can purchase in the open market at 380 levels ? Anything that i am missing here or is it that the price has to be fixed on some average mkt price formula of a quarter or so ?