Can you elaborate this as per last Gland concall?

Thanks

Disc; not invested in strides but have in gland

Listen to the FY22Q1Concall Time Stamp : 23:20 , there are challenges in setting up the cell lines , Arun spoke about contamination etc…

1 Like

6 Likes

1 Like

Hey, so after listening into their Q1 concall, they are still not sure about how they plan to go about separating Stellis. The management said that they were looking into various avenues whether it be an IPO or a demerger. There is no new information and there was no specific road map given so my thinking is that it probably is a few years down the line. They said they would give more information when they could.

Hey ty for reply

But they approved demerger , now why they are not Sure of things ??

Absolutely no idea, but that’s what I got out of the concall. They were pursuing various avenues with Stellis. Sorry for the lack of info.

1 Like

The question to my mind is not earnings (which I believe will be extremely volatile given the unbranded nature of the business in US and hence the pricing strategy that these companies have to adopt). The issue is multiples. Would you value strides same as Aurobindo or same as DRL? Why in each case?

I am sharing my understanding of the US business of an average pharma company here: You decide the multiple.

Further, Do remember that OTC products in US can be branded (Pediacare for Strides, Natrol for DRL etc). But these are very insignificant in revenue terms when compared to their overall revenues in US (~95% unbranded generics).

21 Likes

I understand your point Aditya sir, in many ways this is a business like that of Moser Baer where the price of core product company is manufacturing by its nature will keep reducing each year and as such the companies have to keep protecting their margin by a) reducing costs b) launching new products. Both are expensive strategies and there is no alternative to price erosion.

As per Porters model, US generic business has following traits

- Rivarly among Competitors : High

- Barging power of Buyers : High

- Barging power of Suppliers : Low

- Threat of Substitution : High

- Threat of New Entrants : High

Based on the above there is absolutely no pricing power left for the companies participating in the industry. As such they are left with either

a) venture into niche products and hope no competitor enters that segment

b) become the lowest cost producer of a product and hope products gain market share

Maybe that’s why Strides went for a deal with Endo to enter into niche products.

Thank you for sharing your insights with us. Much appreciated

13 Likes

Price erosion can be there in covid vaccines segment going by the development of vaccines, capacity and availability. In India nobody goes to Sputnik. We are talking about exports for that there is no data available at this point to take a view. Is the deal with RDIF compulsory lifting or based on orders. But we have seen companies dishonoring contracts.

Has anyone attended AGM here? Any updates would be much appreciated

If you analyse this image, there is some strategy /game plan is there by acquiring a sub of Endo. A new generic take about 5 years to develop and commercialize and also it looks like the next decade pipe line is almost filled up

As per BCG Report Link

3 Likes

Had a legal question to the forum members.

If we see the shareholding of Strides it’s approx as below:

Promoters. - 30%

Public - 30%

FII - 26%

DII - 14%

In case the promoters say we want to do an IPO for Stelis- this would need to be voted on right?

Asking since I just don’t see an IPO being voted for by the public and the institutional investors unless there is an imminent cash crunch for Strides.

Can someone pls correct if I am wrong in my understanding of how an IPO would have to be agreed to.

Thanks.

5 Likes

The shareholders who needs to consent to the IPO would be that of Stelis (which is a separate company) and not Strides. Strides’ holding in Stelis is around 30% while the private investors hold the remaining stake. Per the law, the 3/4th majority of the Stellis shareholders will have to decide on the IPO.

4 Likes

a063ded0-cf15-4c4b-994f-b1745074c679.pdf (285.5 KB)

Termination of shareholders agreement. What does this mean?

We’re deep into October and still no news of what’s happening with Sputnik V yet from Stelis. Hadn’t they said that the first dose will be out by October?

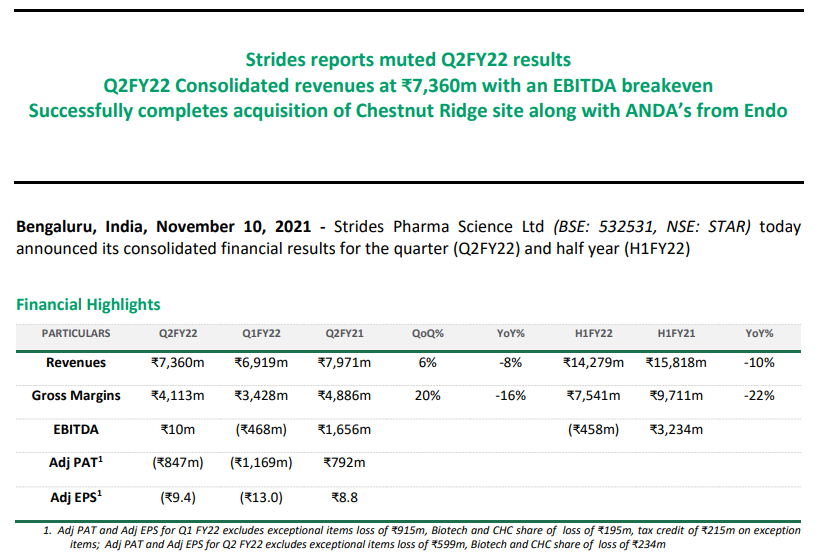

Q2 results are anyway likely to be soft as per the guidance in the last quarter (not sure if the Endo portfolio is already integrated). Plus there are some disruptions and costs may be high.

3 Likes

There is little to no demand for Sputnik atleast in India. Worldwide also I think US and UK made vaccines will take a large market share.

Strides (Stelis) will not be selling the vaccines on their own so market demand shouldn’t affect them.

They have got the order from RDIF to whom they’ll deliver.

2 Likes

I think same is the thing with Wockhardt

4 Likes