Lots of Covid specific headwinds like lower prescriptions, supply challenges, lower approvals etc. But the following point from the investor presentation does not seem to be covid specific and may be a continuing problem - the commodity nature of US generic generics:

“Witnessed double digit price erosion in our US portfolio with higher competitive intensity leading to significant drop in revenues”

Thoughts?

can you share source about IPO way , as it was demerger and strides stakeholder value creation statement from strides so far.

Several important developments from the concall.

1. There is a shift in strategy in US generics.

The plan to hit $400 million was reliant on the R&D pipeline generating 70-80 molecules, and timely rollout of ANDAs. This quarter saw price erosion due to fewer launches (Khemka’s treadmill analogy), and increased competition from players even in newly launched products.

The shift → They’ve acquired a manufacturing plant in Chestnut Ridge which belongs to a subsidiary of Endo International, along with a basket of 100 ANDAs, 20 of which are commercialised, 78 are approved and waiting to be commercialised. They have shut down the Florida facility and consolidated operations at Chestnut Ridge.

The additional basket of approved ANDAs secures their pipeline towards their $400 million goal, and current R&D focus will shift away from generics into complex molecules. Management claims the basket of ANDAs is in complex generics, in a segment that doesn’t see price erosions.

Key questions:

-

Competitor and price profile of these ANDAs in the pipeline. Management expects a muted Q2 and a rebound from Q3 onwards to meet the $400 million target.

-

Endo deal is to be finalised in 60 days. Both sides have published statements to shareholders on intent to sell. Endo has been wanting to sell Chestnut Ridge since late 2020, one wonders which side got the better deal.

-

The shift in R&D towards complex molecules needs to be understood clearly, especially whether they will target chronic or acute treatments going forward.

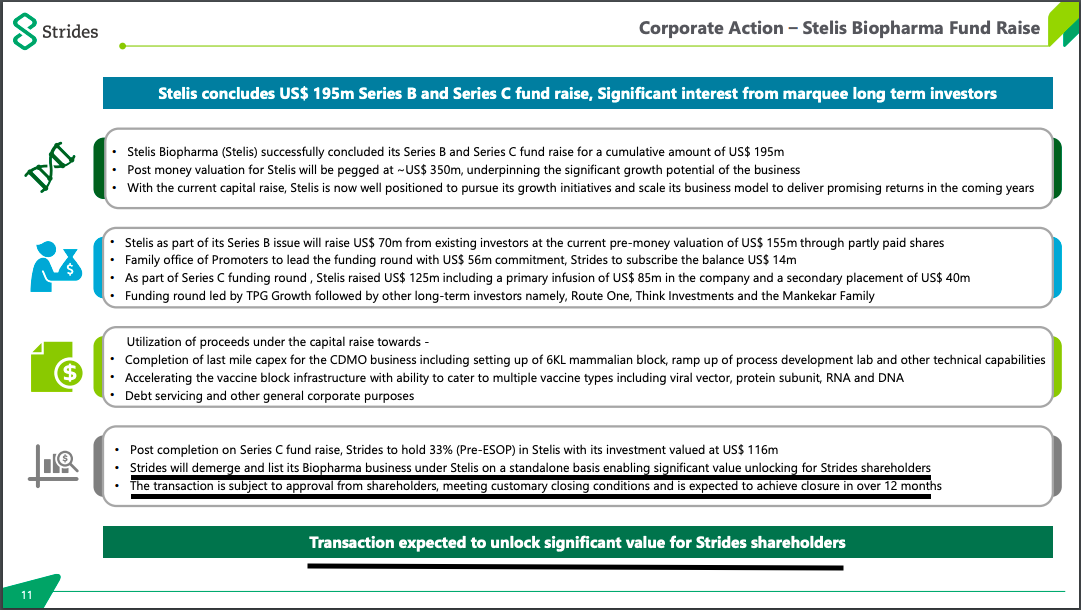

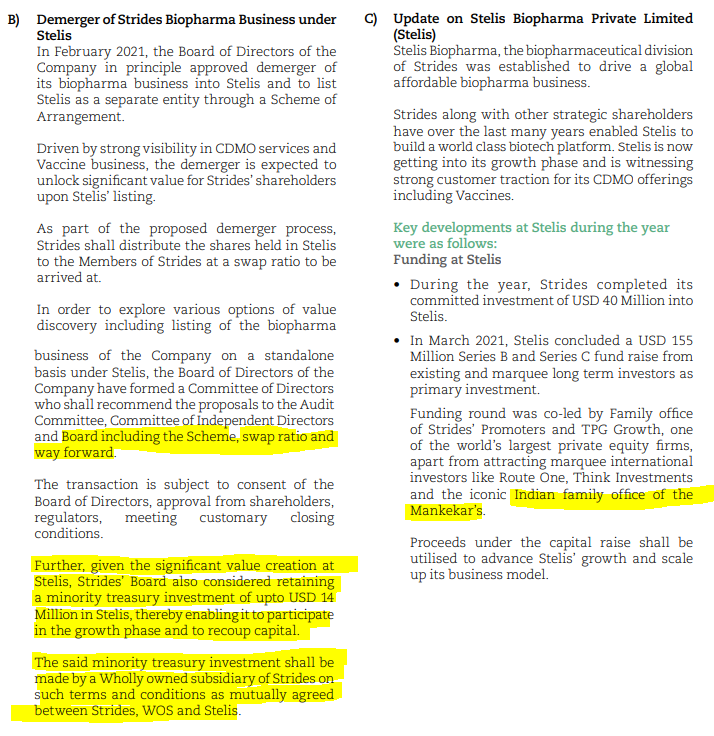

2. On Stelis

Mark Womack as the new CEO is a huge step forward for the company. He was a major figure at AGC Biologics, and brings with him knowledge on running a multi continent Biologics CDMO, a strong network, and is relocating to Bangalore, to work on site.

The management said they’re currently focused on the board, and are in talks with their bankers to explore all avenues of listing Stelis. There was no mention of an IPO specifically, and no clear timelines as of now.

As the investor presentation says, they’re in late stage talks with vaccine producers and are awaiting EU inspection for their new facility. It needs to be a physical inspection, and will take some time before products can be launched.

Happy to share other details of the concall. Invested.

As per their recent update, they are evaluating all options for unlocking stellis value (stance still not confirmed despite committing on it in February). While this bull market certainly can get them lot more money via IPO but it is not at all friendly to existing shareholders. I personally have never trusted the management as they don’t follow the goals they set for themselves even for short/medium term (eg) Australia , Demerger, Endo etc.) but still was invested since Stellis would have been very cheap.

Lesson learnt: Never trust a weak management even if they make formal announcements.

Disc: Invested with a small holding.

Update: No more holdings now.

I am wondering whether the Headwinds that they are facing & will quite possibly continue for some quarters, affect in any way the talks that have been going with PE firms on buying out the promoter’s stake in Strides.

Any Views ??

Can anyone share the concall link

I could not find it on the Web

Thanks in advance

Let’s assume that the generics business recovers this year and makes an EBITDA profit.

In a few years if the management delivers on their targets for US then the generics business can do a CFO of 400 crores 3 years down the line easily- it did 500cr last year. Easily worth 4-5k crore.

Regarding Stelis

The worst for Strides shareholders is that Strides is forced to sell in an IPO- though I don’t see how this pans out.

In this case Strides gets 33% of 5000 crore as cash=1700cr.

Taking 5000 crore as the IPO valuation conservatively- Private markets valued it at 2600Cr recently. If they deliver Sputnik and win some good CDMO contracts Stelis could be listed much much higher too in the current market.

If the markets turn bearish and the IPO market is bad then we get a demerger! That’s great for strides investors.

In the case that none of the above happens we get to keep a fast growing highly capable business under the Strides banner.

The results are really bad but these things happen in commodity businesses.

The amount of cash Stella listing would give/the de merged shares value is just too sweet. An IPO might even be the best thing for us if they get a huge seeking price like 10k crores. Just have to call it a biotechnology platform! Very serious here- it’s a great business and can be marketed like crazy in this environment.

My 2 cents and can’t really see myself not liking the opportunity this presents at this price.

Mr Arun Kumar always kept minority share holders in mind, the amount of wealth he generated right from

Giving dividends when their injectables (Agila) business were sold

Solara

Sequent

now is Stelis time, if they are taking time means there must be some reason. They are very serious about the Stelis execution and at the same time Strides management is also a competitive one and recently they acquired one company in US, we need to wait and see their strategy.

People talk big say "long term , coffee can etc… " but don’t have patience to go through 2-3 quarters of rough phases.

Recent updates on the Stelis as well as solara (Arun kumar is back along with Mr Puri ) , Mr Puri is chair of the board in both the organisations.

Strides has A grade management and it is known for wealth creation for minority share holders.

I have asked this question, "why stelis didn’t raise the capital from Strides from QIP or OFS ? ", the answer (one of the reason) is , PE fund raising route gives better valuations than former.

Disc : Invested, will add more on dips

I confirmed with the company, they said no for IPO, will be listing Stelis via demerger route only

Thanks for saying this out loud!

Even if someone is an expert analyst on the business or the future of the company, investing for a few months and then exiting with 1 quarter’s bad performance means they’re momentum investors and don’t really think of it as owning a business. Any business will go through ups and downs, we just need to make sure that the growth trajectory isn’t permanently broken and the management is clean / consistent in words and actions. Unless either comes true, why should I exit the business? Or only other reason could be if I didn’t do my homework properly the first time around and the entire investment thesis was incorrect.

As far as Stelis demerger / listing is concerned, just want to highlight Q4FY21 presentation where the management has clearly highlighted a couple of times that there is significant value unlocking for Strides shareholders. Till the time there is evidence to the contrary, I don’t have any reason to doubt the management.

However, I still have half a grudge against the management - the Q4 investor call was on 27th May, almost 2 months into Q1FY22 and coming out of the peak of Covid 2nd wave. In that call, the management has not given any indication whatsoever about the severe US pricing pressure, high competition inventory build-up, high failure to supply and Covid 2nd wave impact. Surely, they would have gotten an idea that Q1 will be a washout - they just didn’t want to give that advance warning to the street. As there was no major promoter selling - would just like to think of it as ignorant behaviour which could have been avoided and better managed street expectations.

Disc: Invested and patiently holding. As mentioned above, will wait for confirmed signals on breakdown in growth / management misgovernance / minority shareholder unfriendliness before making any exit call.

Both Ananth (CEO) and Arun Kumar kept on alluding in previous concall (Q4FY21, late May 2021) that even though price erosion is there, they will be able to meet the targets and growth rates. This was in late May’21, they obviously by that time knew that they will not be able to meet the target and Q1FY22 will be bad, yet they kept their commentary strong. This was number 1.

Number 2, my risks with this group always included a change in strategy. Before investing I did investigate their history and Arun Kumar was notorious for changing strategy of Strides on the fly from quarter to quarter. This was an open risk in my thesis - I just didn’t imagine that they would invest heavily into a manufacturing unit in Florida, get it approved by USFDA for VA business and then just abandon it all of a sudden, take a hit to PnL and move to another facility they acquired by paying almost as much as the value of their investment in Florida unit. All of it seems very haphazard to me and makes no sense.

Number 3, wrt Florida unit their commentary was bullish in previous quarter when they would have known that they were going to abandon it soon enough as it was already late May. The Endo deal wasn’t done overnight or in a few months, these deals take time and months of due diligence before they get finalized. Why give bullish or any commentary at all and make false statements when they were clearly privy to some knowledge and knew what they are saying is false.

These are the 3 main reasons. Don’t have as much trust on what they are saying in concalls now post this experience so I take everything they say with a pinch of extra salt.

My investment thesis included them growing or maintaining their performance of Q4FY21 with incremental products and business lines across. This will now obviously not happen this year and hence the drastic reduction in weightage.

I think, the business hasn’t changed fundamentally and a few quarters will be disturbed, this has happened with other generic players as well and most of the reasons were not in control of the management (supply chain disturbance, price erosion etc).

The good thing is that they are addressing the reasons affecting and trying to mitigate the business risks going forward (Optimizing the production cost by getting into new production units, Getting more ANDAs, etc). They have committed for a decent growth in business in FY22 and recovery in H2.

The management cannot have disclosed or even indicated that Q1 is going to be a washout or they are going ahead with an acquisition/disposal on a concall for previous quarter as these are price sensitive info and business secrets, and we as investors are responsible to gauge the direction of the business by reading the indicators, publicly available info and read between the lines of management commentary. Running a business is hard and with so many moving parts, not everything can be shared publicly. They have still gone ahead with the growth guidance/commitment for Fy22 for US and are acting accordingly.

Also, It is extremely hard to not get fixated on the significant price movements, especially if you have a concentrated position, without enough MOS and the roaring bull market does not help. A good strategy is to have hedge for those positions. These price movements tends to make us forget the reasons for investing which were too evident while shortlisting a Business to invest into, Its one’s own call to have correct position sizing and adjust according to conviction as events unfold.

My conviction is still intact in the business & management and I am willing to give a bigger rope to them for now and will watch the next Qrtrly and annual results.

Disc :- Invested and biased, further corrections will make it more attractively valued & I will keep nibling.

Please go through AR , concalls and compare the same with what is happening on the ground. Management energy is wasted on so many things like merger, acquisitions, etc. I would love a company with focus on the business which grows slowly rather in a hurry and rather acting like an Investment Banker. A doubt. But somebody is trying to protect the price going by the recent price action after the results and a big write-off. Most probably Q3 we will have an answer for all these questions and doubts.

Recently I have been trying to study special situations across markets.(Inspired by Stelis from Sajal Sir)

Since many Investors thesis on strides includes Stelis Bio Demerger, I have tried to compile list of all possible and upcoming demerger and Reverse mergers along with deleveraging that are currently playing out, I figured these post may be helpful for Strides thread Investors as many are well averse with Special situations.

Looking forward healthy discussion and frequent updates on Stelis and other companies.

Note: If these post is not relevant to Strides, I request fellow Investors to flag this post I will gladly delete it.

I have a hunch, Mr. Arun Kumar is waiting for the big moment i.e., Sputnik Delivery, this will give that extra edge (to take the business to break even level ) to demonstrate vaccine manufacturing capabilities along with other CDMO opportunities on biosimilar projects.

As long as Strides is concerned there are many news flying around where Mr. Kumar asked investment bankers to sell his stake, he wanted to exit with good money, historically he always made grand exits. So my guess is he will wait for few more quarters for Strides to turnaround and show better numbers which eventually drive the valuations for Strides.

Many of us raised this question for the past couple of months, “why promoters are selling”, may be this is the hint we (at least me ) all missed why they are selling, promoters know the numbers are going to be bad, and whoever in need of funds for their future ventures sold out at better valuations. Either we take this with a pinch of salt (kind of insider trading / not a great corporate governance )

Let us track the business for another 3-4 quarters to see how the new acquisition in US plays out and of course Stelis Demerger

At the moment everything is up in the air, none of the Indian players claimed they are ready to Sputnik vaccine. Biologics is a complex science , setting up the cell lines that too such a huge scale is not at all easy. The same is confirmed in latest Gland call.

Nothing against anyone. It’s your data and reasoning which has to be right. Prof Manenkar also invested in Mahesh Tutorials way back in 2013. Every bet has its own dynamic  Nonetheless, you’re sharing good stuff @Rafi_Syed

Nonetheless, you’re sharing good stuff @Rafi_Syed