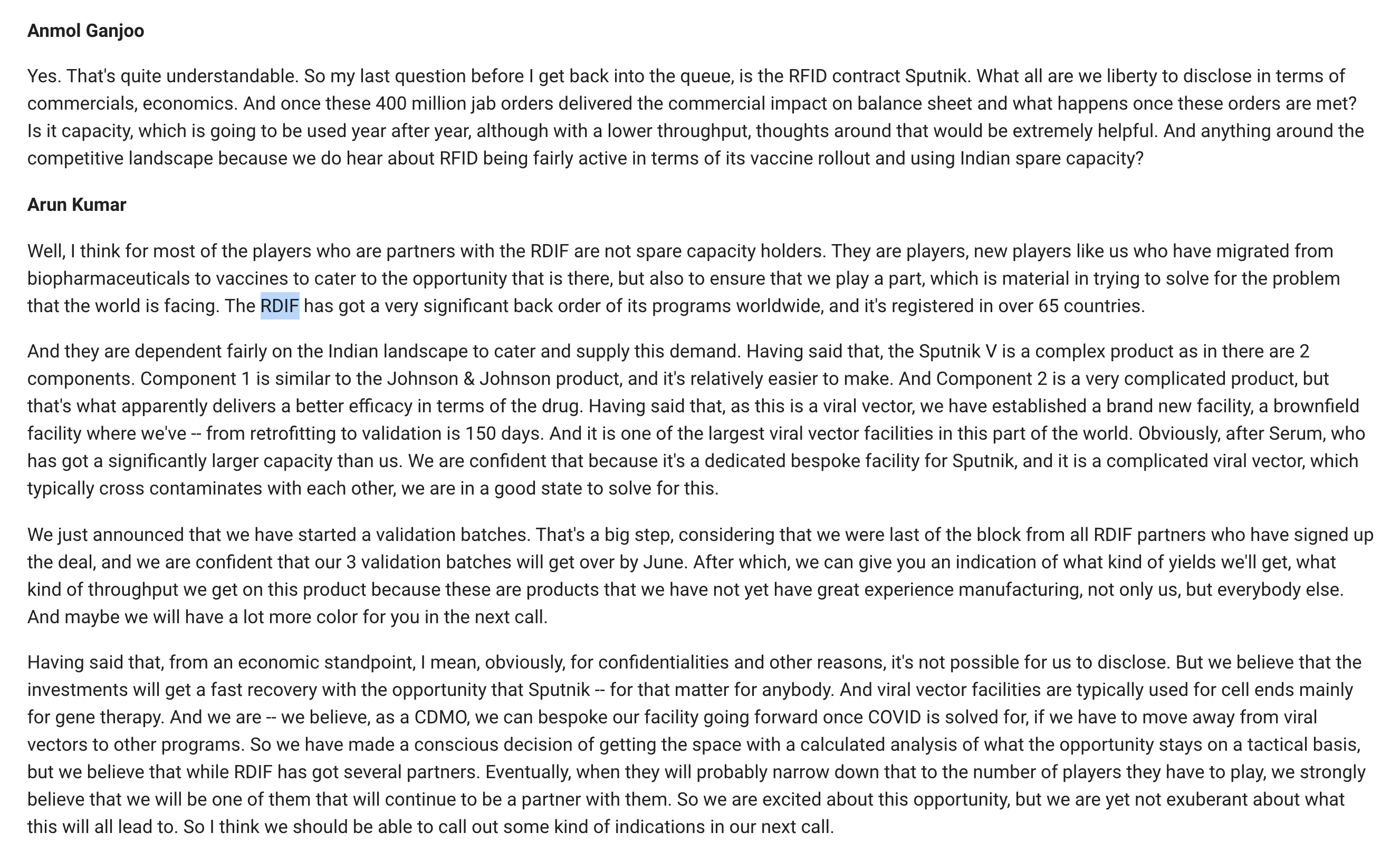

Does anyone has info on when will Stelis be de-merged ??

dont think mgmt has given any timelines on that

I am summarizing my research and investment thesis on Strides here, for everyone’s benefit. Please feel free to poke holes in this and pose questions/comments.

About the company

Strides Pharma is a global branded generics pharma company that sells products in 100+ countries and has manufacturing plants in over eight countries worldwide.

Strides main headquarters is in India with a global headquarters in Singapore. The reason they have a Singapore HQ is cause Singapore doesn’t have capital gains tax, so whenever Strides divests a business (which they do a lot) they tend to benefit by saving a large chunk in capital gains tax.

The same strategy is deployed by Flipkart and so many other savvy businesses.

Strides also has a Singapore manufacturing unit. The benefit of having a manufacturing unit in Singapore is that its one of the countries that has a good designation with USFDA and any pharma products manufactured in Singapore, gets USFDA nod relatively easier. (There are some other favorable Singapore specific policies as well, if someone is aware of them, please comment them here).

Divisions of the Company

Strides operates in three main divisions

- Branded Generics

- Pharma Generics

- Institutional Business

Branded Generics This is the main cash cow and most profitable part of business for Strides. Branded Generics simply means generic medicines that are sold under a brand. For example, Crocin Pain Relief is a branded generic. These products are like FMCG, they command loyalty from their customers, customers do not like to replace the product frequently and once a brand is established you can pretty much sell anything under it.

Strides sells majority of its products under branded generics. Here is an example of a brand Strides has created for children (for its regulated markets)

Pharma Generics This is simply a generic business, similar to the likes of Granules. Strides does earn some portion of its revenues from this business, not a lot. I believe branded generic business will keep getting stronger and as such this part of the pie should get smaller with time.

Institutional This is the tender driven business with tenders given out by WHO, GAVI etc. Very miniscule low single digit contribution of this business to Strides revenue pie. I imagine this along with Pharma Generics are there as complimentary businesses for Strides.

In all essence, Strides is a Branded Pharma Generics business that operates in a majority of countries worldwide.

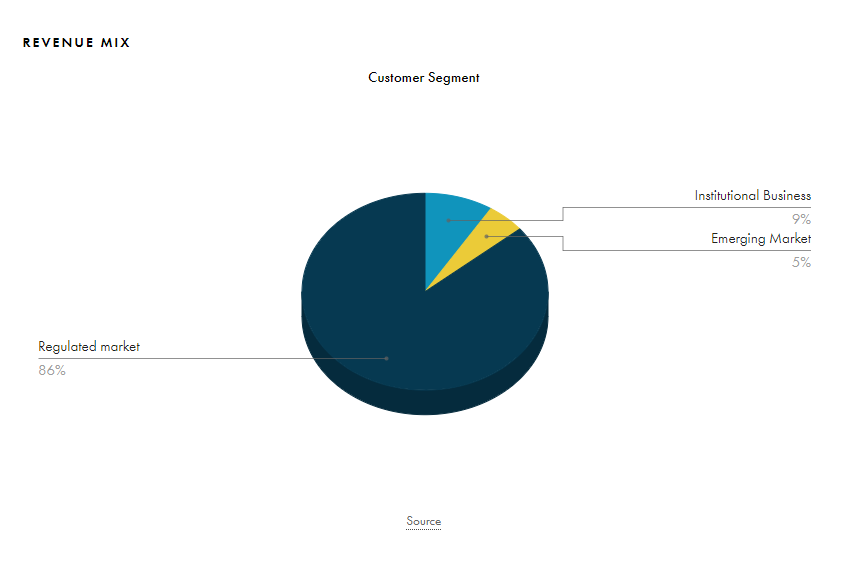

This is what the revenue pie of Strides looks like

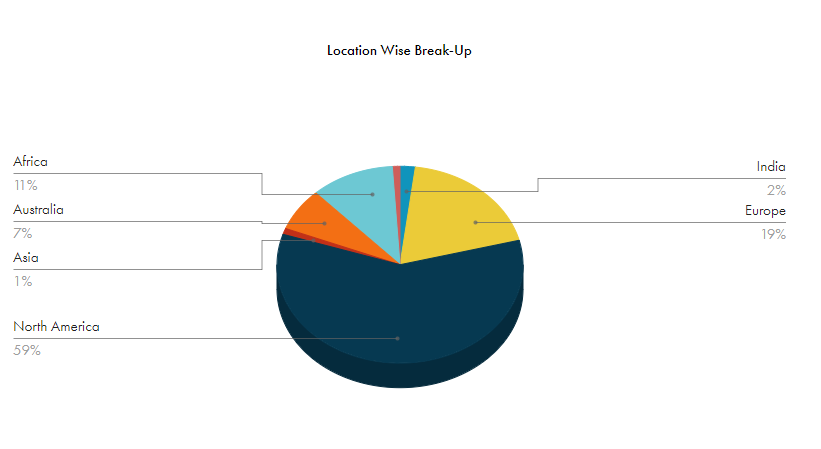

and this is how different geographies contribute to Strides Revenue

Regulated + Other Regulated Markets (Europe, Canada and Australia) make up about 85% of the total revenue pie for Strides. This is good cause Canada and Australia are highly profitable markets and both have a similar pharma market structure for generics. Strides once used to rule Australian generic market before they made several divestments (there are many divestments throughout the lifetime of the business which makes it hard to track as it loses continuity, if someone knows better then please highlight).

For each of its Regulated Markets, Strides has a front end (Pharma speak for a sales team). Having a front end is very important esp. for US Markets as its these pharma sales reps that reach out to doctors and help them substitute their products in prescriptions. In US markets, only what is written on the prescription can be dispensed to you by the pharmacist, its a crime to dispense something else.

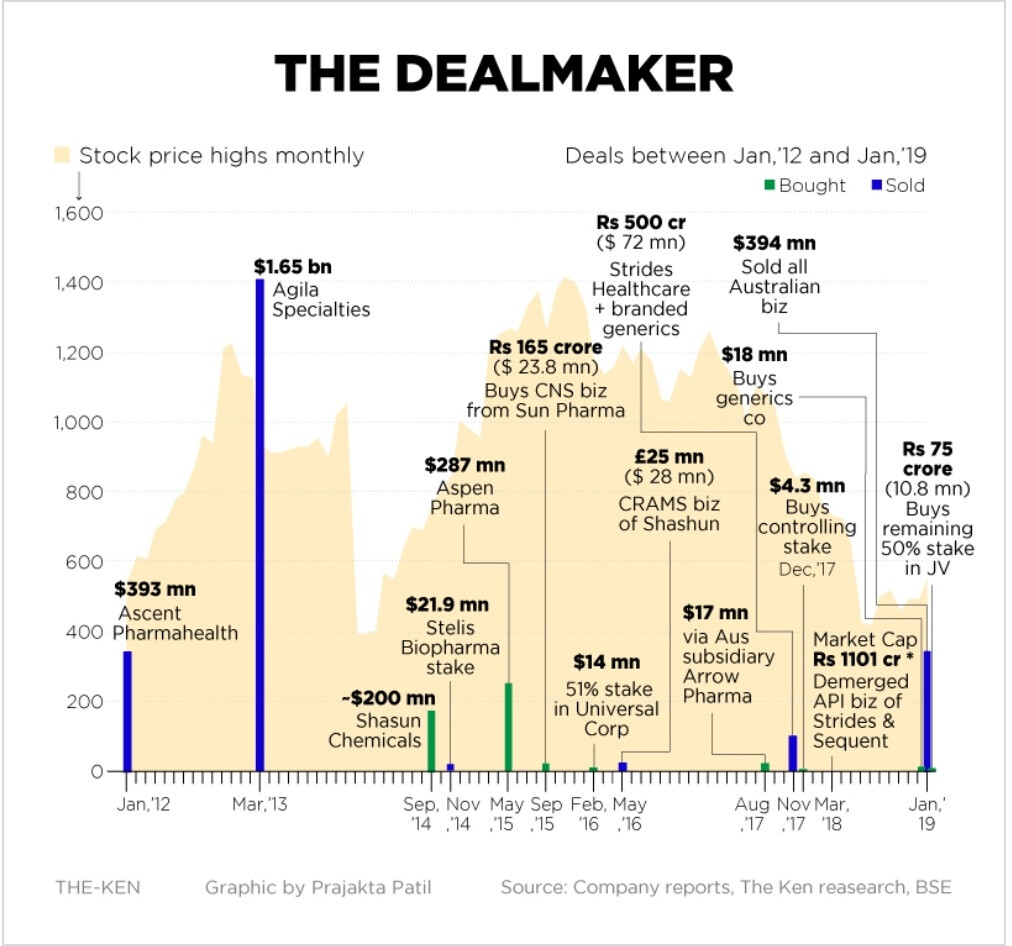

Here is a snapshot of everything Strides bought and sold during its lifetime.

Till 2020, Strides was better evaluated as a Pharma incubator business, as they consistently bought and sold businesses. Whoever is the new promoter (I write about it later in this thread) will definitely provide some stability to the business and maybe that’s why the top management team has been firmed up and represents a very strong professionally driven team recruited from top pharma names worldwide.

I am not going to write about the known parts about Strides, its financials etc. you can get those details from its investor presentation.

Here are some lesser known growth areas for Strides

US Veteran Affairs Business: US VA has an annual 100 Billion USD plus budget for sourcing generic medications for its members. Since this a govt sponsored budget, they usually want majority of sourcing to be done by American Firms that produce products in American Plants employing Americans and paying American Tax. For this purpose, Strides set up its Florida manufacturing plant, some part of manufacturing in Singapore is also routed to VA program. This should be a big revenue driver for Strides for its US business which is already 59% of its revenue pie.

Canada Business Strides has a well crafted and clear strategy to enter and gain market share in Canada. They are in execution mode and this business should show meaningful growth in the coming years for Strides. Same goes for their Australia business.

Africa Business This is the fastest growing area for Strides with revenue growing by over 65% last year for Strides in this region. Strides employs a ‘In Africa for Africa’ model which simply means that they are manufacturing employing and selling to Africans nations. Strides has a its own front end here as well. While this is a fast growing business, dollar wise it doesn’t amount as much as US or other regulated market business for Strides.

Sterile Injectables Strides is the leader in developing sterile injectables. Sterile Injectables simply refers to medicines that are given via injections to either veins or by IV. They cannot be consumed orally. Strides was a leader in this space when they built their Australia business and sold it off to Mylan for USD 1.2 Billion. 7 years since, their non compete with Mylan has ended and Strides wants to re enter this business. Interestingly, no one not even Mylan has been able to advance or replicate the sterile injectables business like Strides did. Manufacturing of Sterile Injectables (SI) is a difficult task, you need to have a separate manufacturing unit as the unit that produces oral medications cannot produce SIs and its a compliance nightmare to have both SI and non SI product manufacturing in the same unit. To counteract this problem, Strides is outsourcing all manufacturing of SIs to CMOs and simply using its in house technical and research expertise while outsourcing all manufacturing. This effectively removes any headache or investment from Strides into SI manufacturing and compliance while also allowing it to enter this market again. This business should deliver some revenue additions in next 2 years or so. Arun Kumar Family Office is also launching another company called SteriScience which will manufacture specialized SIs, Strides has the option to pick and choose which SIs it wants to participate in.

Transformation of the company Under the new CEO, company is on a transformational path with a professional leadership and management team in place. Gone are the days when Strides used to undertake huge investments on direction of Arun Kumar to incubate several pharma businesses and sell them off couple years later at a big profit. Strides now is a pure branded generic pharma business that operates in majorly regulated markets. This was evident when current CEO refused to put more money into Stelis or SteriScience.

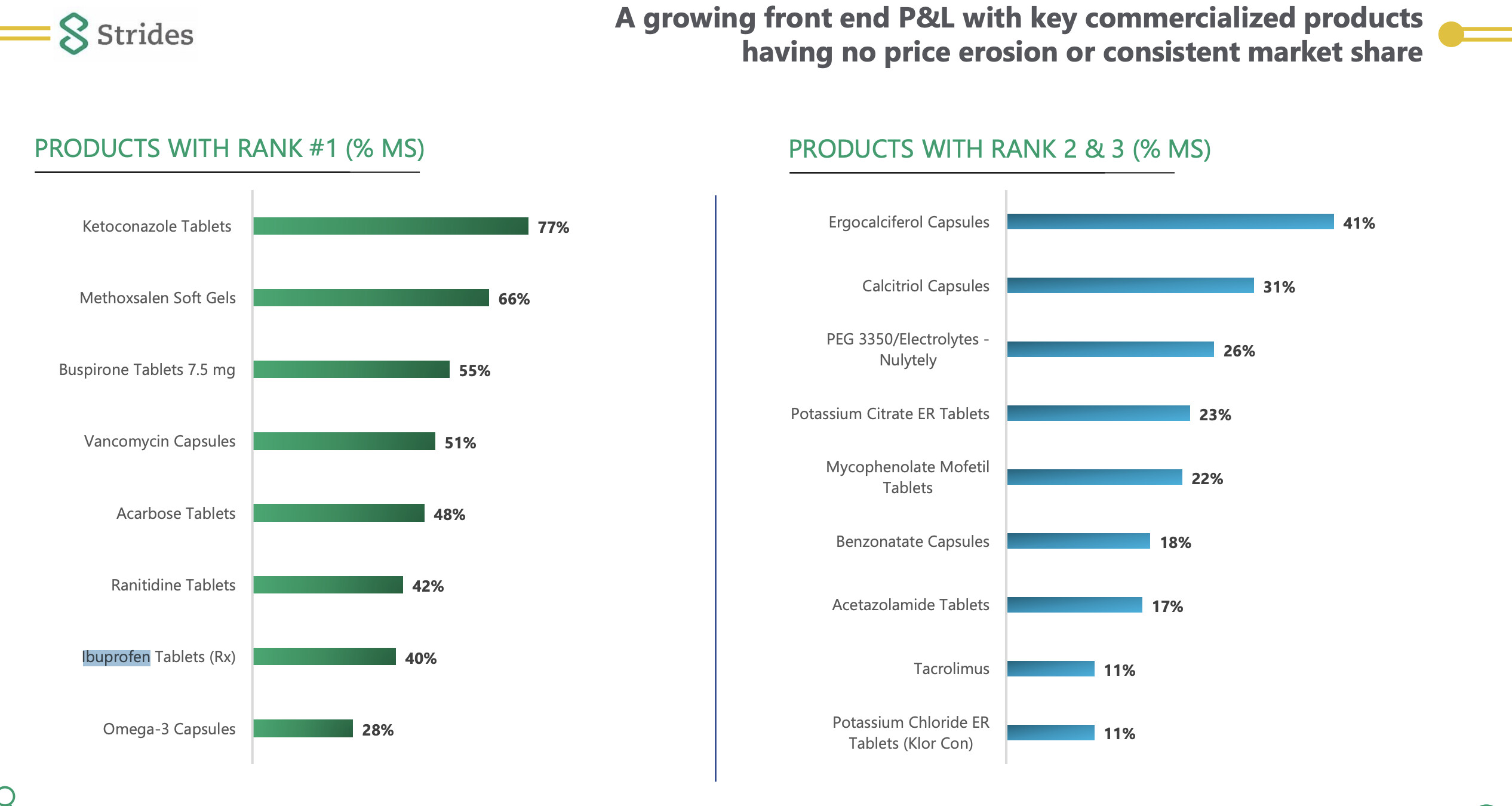

Products and Pipeline Strides has the maximum ANDA filings of any company in the world. It has over 120+ ANDA filings out of which 100 ANDAs are approved. Strides also has market leadership in majority of its products. Here are a few examples below

US FDA Compliance Strides has a good record of US FDA compliance with only 1 warning letter and observation in the history of the company for its Puducherry plant. Strides follows a two manufacturing site for each product method where every product is produced in over two sites globally, so the Puducherry observation didn’t drastically impact Strides ability to earn revenue. Further, Strides, has now divided the quality management role into two separate roles with quality assurance professionals having a direct reporting line to CEO. This should ensure no future instances of such cases.

Rest of the stuff is pretty well known for Strides and discussed multiple times in this thread so I won’t be repeating it here.

Short Term Risks Shipping costs is a major short term risk for the company, it dampened last Q margins and I expect it to impact this Q margin even more severely cause shipping costs have risen further 5 fold in last few months.

D: Invested and playing out a investment thesis, may exit anytime or may stay invested for long run, please do your own due diligence

Note I do not know why promoters are selling shares, I do not know which PE will take over, I do not know when Stelis will be demerged and I do not know what price will Stelis be demerged at

35 Likes

Hi, thanks for posting. Been studying the company recently based on your posts.

Wanted to quickly point out that Tijori’s data on Strides is quite outdated, and the market share information is from an investor presentation in Q1FY20, before Ranitidine was pulled from the US markets.

I noticed that they don’t explain how the topline is segmented according to the drug manufactured, and prefer to just explain the geography breakup, but an alternative way of understanding which ones to follow is based on what they list as their three key products in each annual report.

From the 2019 AR:

- Gabapentin Tablets

- LNZ Tablets

- Ranitidine Tablets

From the 2020 AR:

- Ibuprofen Tablets

- Ranitidine Tablets

- Buspirone Tablets

My understanding is that two months of Ranitidine supply was disrupted from September - November due to FDA tests, and hence it still remained in the 2020 annual report before its withdrawal on April 1st 2020. If my hypothesis of these three being the ones to track is correct, we know ibuprofen prices in general are expected to see a correction this year and should expect ibuprofen and ranitidine to be replaced in this list in the next annual report.

Will add on to your post soon on the insulin market that Stelis is aiming to address in the near future.

10 Likes

I didn’t purposely add anything related to Stelis, wanted to create a separate post on it since it’s going to be a listed company very soon and strides will only have a treasury stake post Demerger.

You can start a new thread on Stelis and I will help build on the same. Insulin, CDMO and their biologics for osteoporosis, vaccine platform are pretty exciting areas.

My investment thesis on Strides is mostly to capture value on account of PE buyout (I believe Carlyle will buy them soon, Aditya Puri coming on board earlier this year leads me to believe that) + free shares of Stelis. I also believe Stelis will list around 3k market cap but soon re rate downward as all shares that institutions receive in Demerger will be forced sell due to various covenants some of these firms have (not investing in companies below certain market cap or loss making companies)

15 Likes

@Tar - Would you explain a bit more on the above. If derating happens, is it not good to buy them from open market ? Apologies if it is a foolish question.

It definitely is better to buy from open market if it does happen.

My current thesis also accounts for Strides re rating to happen first given the incremental triggers for it in coming months. That gives me a decent return on my Strides position which also gives me free Stelis shares. I plan to reduce my strides position in chunks post demerger and eventually all my strides position will be invested into Stelis.

So by investing now, I lock myself into some free Stelis shares + capture all the upside in Strides. At Rs 760 (which is my avg price) there was incredible margin of safety. Strides sells for less than 2x sales (if I take out Stelis value) and 2.3x times its gross block. On every parameter, Strides checks off the margin of safety box, be it fundamentally or technically.

The whole investment is targeted to increase my initial investment into Strides so I can buy maximum shares of Stelis.

19 Likes

Could you both please explain why this is relevant to Strides as:

-

The NPPA sets prices in Indian markets, which constitutes less than 3% of Strides revenue.

-

They’ve withdrawn Ranitidine from their US markets as of April 2nd 2020:

- They don’t even produce Carbamazepine, but an alternative medication for epilepsy called Levetiracetam.

Thanks ![]()

2 Likes

As far as my understanding goes This is not true. If you have any source for your understanding, please share it. From what I know (watching seminars on the subject by sajal sir, Aditya Khemka sir) the way generics works in US is that it is paid for by insurance. The insurance provider ensures that pharmacist only dispenses the cheapest generic for whatever brand the doctor has prescribed. One can only buy the prescribed brand if they are paying out of pocket, which is a small fraction and bound to get smaller.

The whole purpose of ANDA filings and generics is that medicine get cheaper over time. Regardless of doctor pharma tie ups or incentives. In fact to say a company has a branded generic chemical entity presence in US is itself a statement I don’t think is true without some solid evidence. The term branded generics has a very very specific meaning in the Pharma context. While what they sell in US might be in a labeled box which has their name on it, it is not branded generic as far as I understand it. The term branded generic refers to the ability of the pharma co to command some premium due to their brand and for their market share and revenue to be ever increasing because of brand loyalty (similar to FMCG).

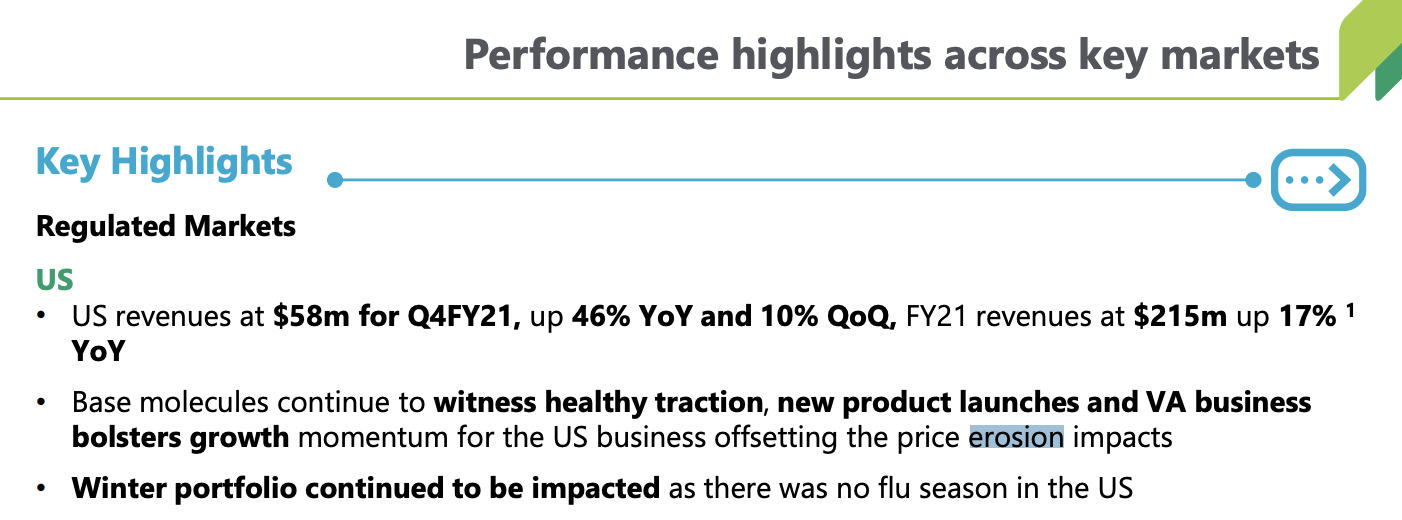

I present a few key reasons below why i think strides US biz is not branded generic: we see strides talk about price erosion in us market in the latest investor presentation.

That is the specific characteristic of generic generic and an anti characteristic of branded generic.

I think the reason stride invests into branding and sales a lot is that a lot of their products are OTC products where there is immense competition and gaining any market share is based on the sales marketting muscle.

Here is an extract from strides FY20 annual report. Se how they talk about regulated and unregulated markets differently.

When the founder describes the different business models, the word brand is not used to describe regulated market presence even once:

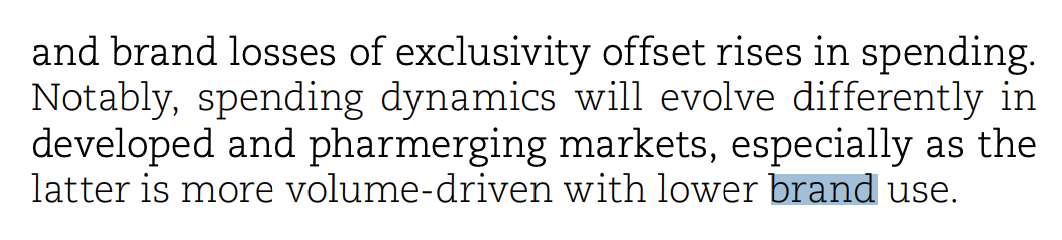

Another extract from Annual Report talking about how spending habits are evolving in different markets:

It makes sense to talk about brands in unregulated markets because people pay for medicine out of pocket as per prescription. In regulated markets health insurance covers these costs meaning insurance provider pays for it and thus generics become an important concept.

The only case I see for referring to a brand in regulated markers is the OTC business since there one can think about marketing directly to consumer. However, this space is bound to be very highly competitive. As an example see Ibuprofen in US which has 19-20 brands:

(im sure even this is an incomplete list).

Similarly one can see even Australia has 19-20 brands selling ibuprofen. Hence, even here i am not certain how much brand loyalty and willingness to pay up for a brand customers have, given how highly fragmented the market is.

Please see some of Aditya Khemka sirs videos if you haven’t to understand this better:

(Watch from 7:50 to understand how the pharma value chain works in US and the concept of generics)

Btw just to confirm I also posted this on Twitter and requested Aditya Khemka sir to reply:

He has confirmed that it is generic generic not branded generic :

https://twitter.com/sahil_vi/status/1411499549592481795?s=19

If after my post you still continue to believe that they do in fact get most of their us revenue from branded generics, please share your primary source which has helped you develop that understanding and I will study it in depth as well and develop my understanding ![]()

Btw just to be clear, I don’t have anything against strides biz. I am still studying already like stelis and what strides Has done with stelis. Just pointing out a factual inconsistency for benefit of all investors.

Disc: studying

31 Likes

Based on whatever you have presented, it do appears that Strides business in US is generics and maybe their other regulated markets business is branded generics. I haven’t really dwelled deep enough in each segment simply cause Strides is a tactical investment for me. At the same time I am not one of those folks that doesn’t change his mind when presented with facts. I am happy to be proved wrong.

No offense taken, Strides doesn’t belong to my father ![]() Its simply an investment to help me grow my wealth.

Its simply an investment to help me grow my wealth.

I do believe Strides has some sort of a Branded Generics business apart from Generics, simply cause the company says so and I have no reason not to believe them. I tend to cut a lot of slack and try to believe what companies are telling me (maybe naive on my part but it has worked for me well). Its the same reason I believe Laurus’s 250cr in Goodwill is on account of Richcore acquisition or RACL’s direct tax add to CFO is cause of advance taxes. If a company tells me they are into branded generics, I will believe them as they know more about their business than anyone else.

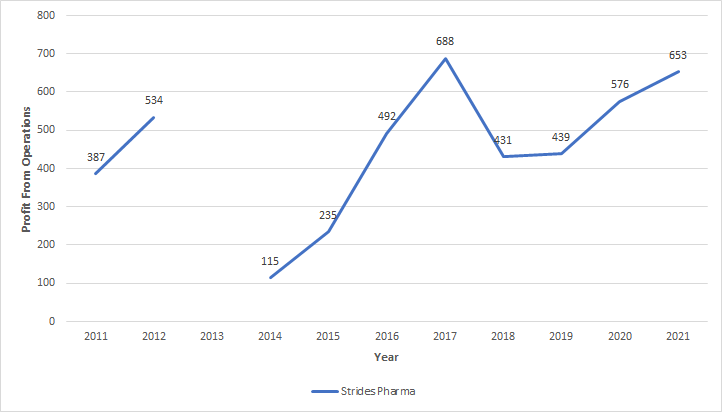

No matter what business they are in (whether generics or branded generics) they are profitable and growing rapidly. Here is what Profit from Operations looks like in last 10 years.

2021 figure is close to the peak profit generated by operations (mind you the previous peak had other businesses that have since been hived and sold off). Like you mentioned this profit from operations figure is after they witnessed price erosion, problems related to ranitidine and very high shipping costs. If a business can achieve peak profitability with so many headwinds, they can certainly do much better when the temporary headwinds disappear.

To add to this further, they are a professionally managed company now with very little involvement from Arun Kumar on direction of Strides business. Such a growing (25% growth in regulated markets and 65% growth in other regulated markets) professionally managed business is trading for less than 2x sales.

I personally cannot care less what they are selling, whether its generics or branded generics, as long as they are generating more cash and growing their business.

To reiterate, I am invested cause I see a growing professionally managed business selling for pennies on the dollar and I see incremental short and medium term triggers for the company to enable its re rating. If today Strides was selling for above 1500/share, I probably wouldn’t have invested in it and waited for demerger.

Thank you for research and adding on to this thread.

15 Likes

Yes it does, this is the emerging market biz. The Africa and india like economies. (Africa is definitely one of them).

Thanks for writing back and agreeing. I’ll continue to study and learn more.

3 Likes

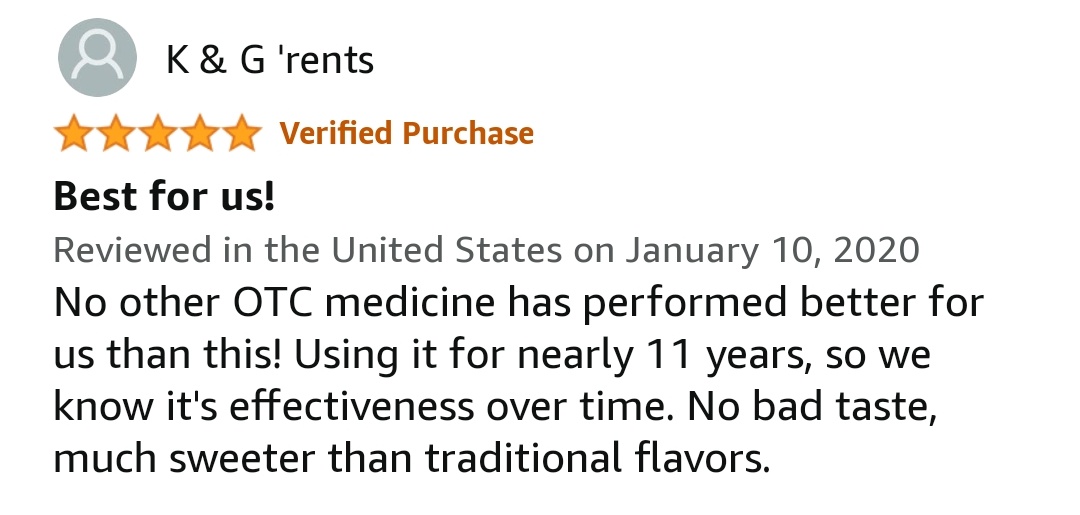

So I was researching about ‘PediaCare’ (https://pediacare.com/) the child centric brand from Strides for US markets and it does have some good sales and very high rated Amazon Reviews. Majority part of Strides in US maybe generics but there are certainly elements of branded generics even in regulated markets.

Review from US website of Amazon, couldn’t find extensive sales data for this brand

They even sell gummies in India under this brand on BigBasket, Amazon, Flipkart etc. I ordered some, will post how they taste and my scuttlebutt review here ![]()

7 Likes

I will summarize my understanding of the business of strides at a very high level. Business can be divided into 4 parts:

Regulated Markets

Generic Generics for US, Australia, europe, UK, South Africa. Co is able to grow due to topline despite pricing pressure and despite adverse USFDA observations due to a strategy of creating their own front end, due to having large scale in some of the molecules, due to focus on developing lots of ANDAs for these markets. One way in which they maximize revenue growth is by maximizing PF meaning once a molecule has been developed for US, they’d also try to file it in EU, Australia etc and thus maximize scale. The fact that they have large market share in some molecules means that they are the lowest cost producer for some of these FDFs at least which is one way to survive in a hyper competitive commodity like market. Co has claimed in concalls that in 70% of their portfolio they are the market leaders. Have been able to grow decently and aiming to grow ~20%+ CAGR topline in next 3 years. One change in strategy they have done is to create a front end in US and stop partnering with other front-end cos. By end of FY22 they envisage 100% of US sales to be driven by US front end (team of 20 people). This number was 86% in Q3Fy21.

Key question for me figure out: Why do they have a large market share, where they do?

Unregulated markets

This part of their portfolio focuses on Africa. They are shifting manufacturing from indian to African (Kenyan) facility. Part of their “For africa by africa” strategy. There is an institutional business as well which consists of Formulations like TLD (similar to what laurus does) being sold. This is a high growth market. In FY20 annual report they talk about tripling the branded generics business. Overall africa is one of most underpenetrated markets so this could end up being a long term growth story.

Blockquote Overall, medicine spending in Africa is set to reach US$160.7 billion by 2024, at a CAGR of 20.4% from 2018 [Source: Goldstein Research].

The key change in strategy here has been to shift from generic generics to branded generics which of course makes the cashflows much higher quality.

Key question for me figure out: What are these brands and what is their competitive standing in African countries?

Injectables

Strides had developed Ajila then sold it to Mylan in 2012. Their non compete ended in Dec19. it is interesting to see that a lot of those agila employees have now joined back Strides to create Injectables 2.0. they envisage this to be a 200-400M$ opportunity for the regulated markets in 2-3 years. 60% of all US drug shortages are injectables. Focus will be on developing those injectables which are difficult to develop or in high demand (shortage). They will take an asset light approach here with key parts of value chain being outsourced (CMO) leading to good profitability metrics. Focus will be to identify products with limited competition & high entry barriers – technical complexity/ API scarcity.

Key question for me figure out: Have they already filed any injectables? If so, is there any pattern visible? is management walking the talk wrt value added, difficulty of injectables filed?

Stelis

This is the largest value in strides. 350M$ of book value (assets constructed and under construction). This is roughly the same as syngene’s book value. They have 3 lines of business here:

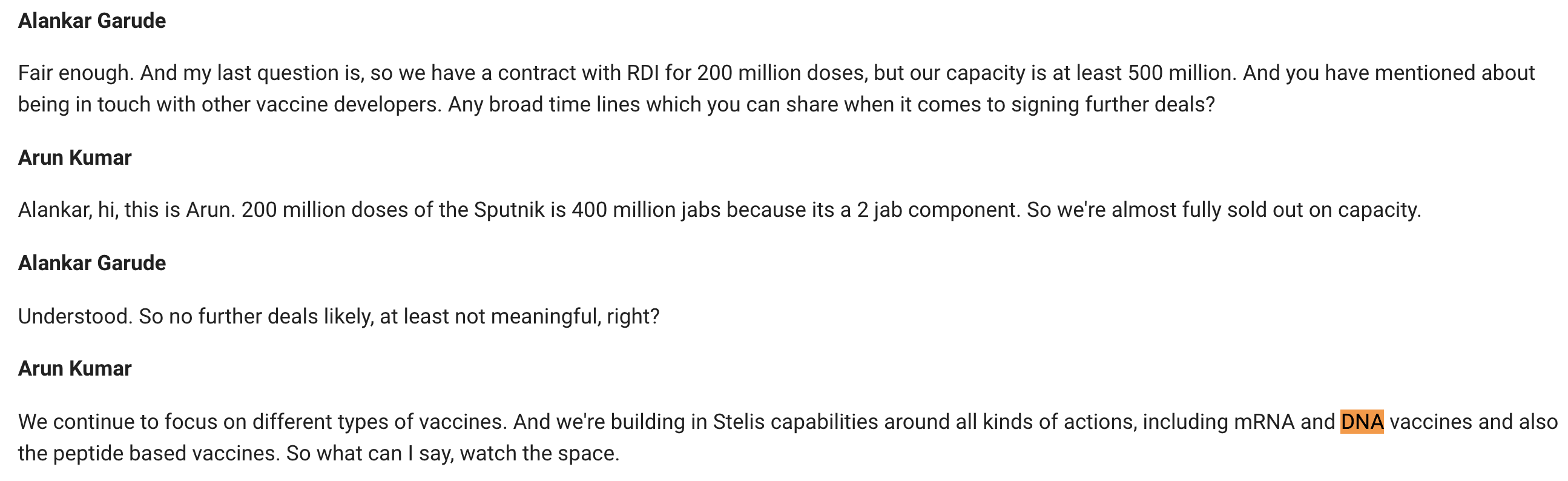

- Short term tactical covid-19 business opportunity: existing tie up with RDIF for 400M shots in FY21. Possibly more in subsequent years. Given that we see Arun kumar talk about mRNA and DNA vaccine capabilities in presentations i find it plausible that more tie ups might be announced in time to come. This tactical opportunity will generate some cool 100s of million dollars of growth capital for stelis to pursue the next 2 businesses.

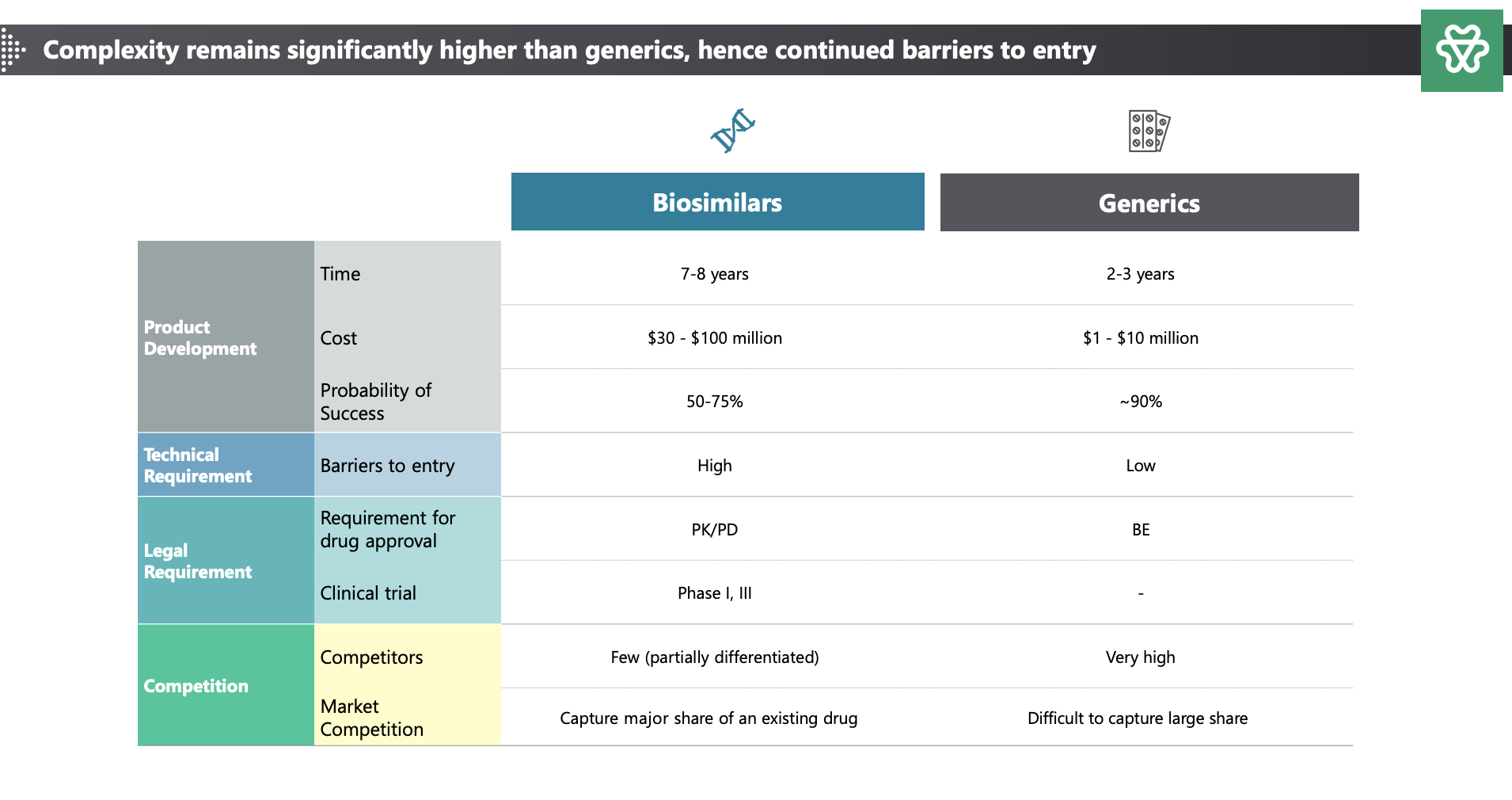

- A biosimilar and biologics division: the biosimilars opportunities are especially interesting with 3-4 tangible opportunities lined up already: Insulin (glargine and other forms): They are also Foraying into the generic insulin market through an acquisition of proprietary technology developed by ex-Eli Lilly scientists. Stelis’ technology is cost competitive with fewer purification steps, higher yield, greater recovery with high purity vs. competition; Biosimilar PTH (Teriparatide) targeting Osteoporosis with < 4 competitors; Drug-device Sodium Hyaluronate Single Injection – only 3 other market leading single injection brands, of which only 1 is close to stelis product. Total opportunity size > 15B$. If they can even capture 5% of market share, there is significant upside. The biosimilars division is not as interesting as the next division though.

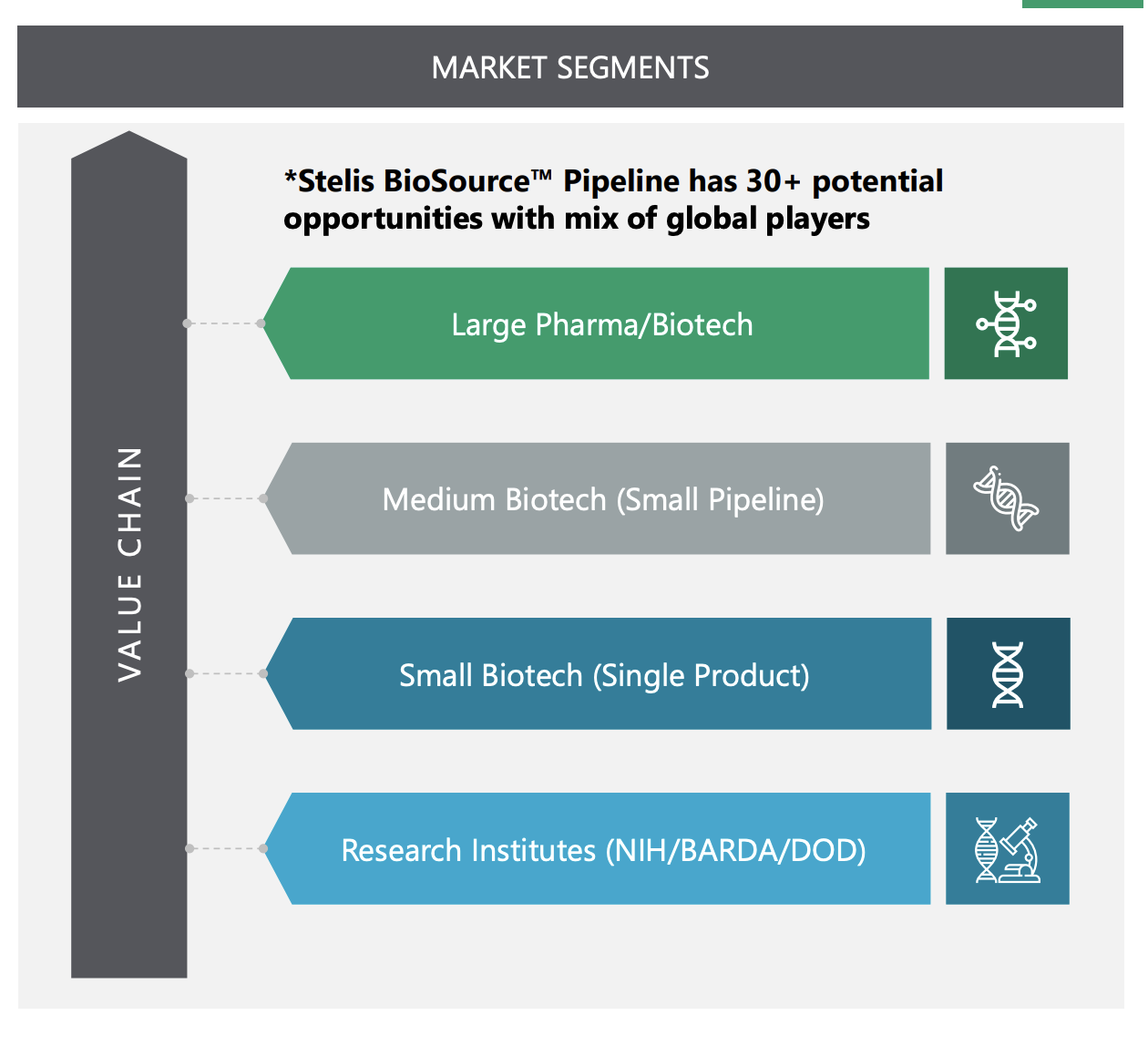

- Bio CDMO: In general, there is a shift from NCE to biologics development which is funding biologics R&D spending. Also, innovators do not want to do significant capex and dilute return ratios. There is also the rise of many virtual small and mid sized biotech innovators who dont have their own development or manufacturing capabilities… This is core tailwind for CDMOs sector. Bio CDMO in specific is difficult to develop. Stelis estimates one needs at least 250M$ investment to set up a scaled up manufacturing facility. USFDA Compliance and maintenance of sterile conditions is of utmost importance here. There are 2 parts to CMO biz here: the manufacturing of the drug substance, the filling & finishing of the doze (putting it into a syringe or pen). For this second part, their capacities have already been booked until FY26. They are also in talk with 30 other cos for their drug substance development part of the biz. Co expects hockey stick growth since FY25E and to break even in FY22. A demerger/ipo might also happen towards FY22 end as per management.

Key question for me figure out: How do innovators pick one Bio CDMO partner or another? WHat influences that decision?

PS: This 2019 corporate presentation is quite good.

Strides_Stelis Investor Day 2019.pdf (7.5 MB)

Disc: have a small tracking position, studying

20 Likes

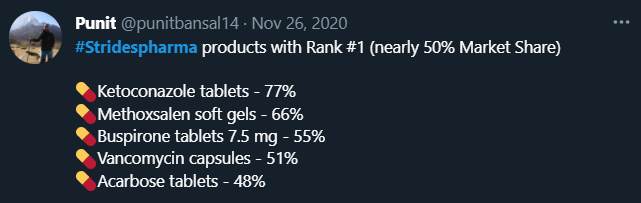

Thanks for sharing your thoughts, thought I’d add on to this. ![]()

- Ketoconazole Tablets - The USFDA is advising against the prescription of Ketoconazole unless absolutely necessary, as there are severe liver complications associated with its use that lead to death.

- Health care professionals should use ketoconazole tablets only to treat serious fungal infections when no other antifungal therapies are available. Skin and nail fungal infections in otherwise healthy persons are not life-threatening, and so the risks associated with oral ketoconazole outweigh the benefits.

My first guess is that this is such a risky / unattractive drug in the first place that a) other suppliers would stay clear of, and b) would be the first to go should there be any development of an anti-fungal that doesn’t have these risky complications. I’m not sure we should attach a lot of value for this particular drug.

- Methoxsalen Soft Gels - Used to treat psoriasis. I found the following information specifically for Strides’ formulation, which is a candidate explanation for their market share. Source:

This new dosage form of methoxsalen exhibits significantly greater bioavailability and earlier photosensitization onset time than previous methoxsalen dosage forms.

- Buspirone Tablets: used to prevent anxiety and panic with a slower release profile to Xanax. Found that different generics players have carved a niche in their own dosage forms. Sourced from an online pharmacy in the US, have a look:

| Company | 5mg 30 Tablets | 7.5mg 30 Tablets | 10mg 30 Tablets | 15mg 30 Tablets | 30mg 30 Tablets |

|---|---|---|---|---|---|

| Strides | - | $16 | $4 | - | - |

| Zydus | - | - | - | $6 | $15 |

| Teva | $6 | - | $7 | $9 | - |

| Accord | $4 | $14 | - | - | $12 |

| Unichem | $5 | - | $5 | $8 | $11 |

| Epic Pharma | - | $12 | - | - | - |

It looks like Strides is winning on pricing power in the 10mg segment, but is the most expensive player in the 7.5mg segment. The pricing difference between 7.5mg and 15mg is absurd, but the following snippet provides an answer. The next question to ask is which dosage is the most common/high volume for Buspar. (And also check pricing consistency with other pharmacies.)

The usual starting adult dose is 10-15 mg daily given in 2 or 3 doses.

The 5 mg and 10 mg tablets are scored so they can be bisected. Thus, the 5 mg tablet can also provide 2.5 mg dose, and the 10 mg tablet can provide a 5 mg dose. The 15 mg and 30 mg tablets are scored so they can be either bisected or trisected. Thus, a single 15 mg tablet can provide the following doses: 15 mg (entire tablet), 10 mg (two thirds of a tablet), 7.5 mg (one half of a tablet), or 5 mg (one third of a tablet). A single 30 mg tablet can provide the following doses: 30 mg (entire tablet), 20 mg (two thirds of a tablet), 15 mg (one half of a tablet), or 10 mg (one third of a tablet).

My takeaway is that if I were on a dosage of 10mg / day taken in two doses, it’s two-three times cheaper to buy a 10mg tablet and bisect it, rather than buy two 5mg doses (5mg tablets provide convenience by corollary and the convenience is priced in). By the same argument, it’s cheaper to bisect/trisect a 15mg tablet if you’re on a dose of 15mg per day. Thus in these two segments, my hypothesis is that both Zydus and Strides should be leaders on pricing power, offering the cheapest doses in their respective price range. This is then surprising that they claim the 7.5mg tablet is where they have the largest market share.

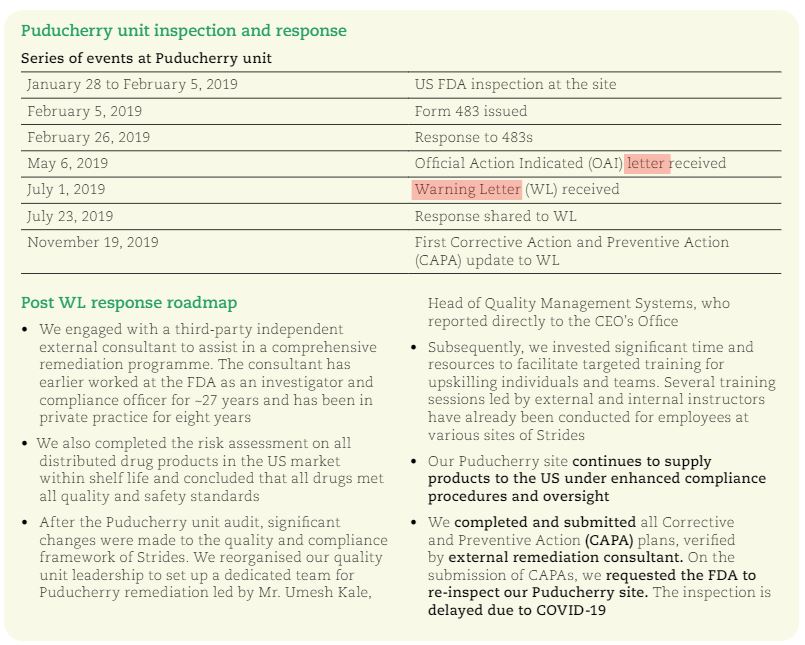

Would you still treat this as a red flag? My observation from the letter was the following:

During the inspection, our investigator observed discarded CGMP documents and evidence of uncontrolled shredding of documents. For example, multiple bags of uncontrolled CGMP documents with color coding indicating they were from drug production, quality, and laboratory operations were awaiting shredding. Our investigator also found a blue binder containing CGMP records, including batch records for U.S. drug products, discarded with other records in a 55-gallon drum in your scrap yard. CGMP documents in the binder were dated as recently as January 21, 2019: seven days before our inspection. Your QU did not review or check these documents prior to disposal.

Their response:

From their concall, they’ve been waiting for two years to get it reclassified as the warning letter doesn’t prevent them from producing things at the plant, but instead has halted the 4-5 ANDAs that are in the pipeline until it’s reclassified.

Puducherry has got no negative impacts. Whatever business we were doing before FDA issue, we’ll continue to do the same numbers. We do not have an import alert in this plant. We only have a warning letter, which allows us to continue to sell products. And all those products are produced in 1 or 2 factories. And therefore, there is no revenue impact. The only impact is that some of our approvals are pending, 4 or 5 approvals are pending, which once this inspection reclassification is over, will come through and which will start improving the numbers from that facility. But at this time, the Puducherry plant runs fully booked, is very busy and is doing things under heightened supervision. So there’s no negative impact on the numbers.

They recently got the same plant inspected by the EU regulatory board and cleared the inspection, so I think they’ve done enough.

My questions are to find out which drug constitutes the largest addressable market, where even a 10% share may lead to larger revenues than a 70% share of a smaller market.

8 Likes

Strides has a policy of not entering into any product unless they can win a majority of market share in that product. The company essentially keeps filing ANDAs and collecting them only to launch products when they know they can win the market share. Existing generic players like Teva are finding it hard to compete with increased flow of generics from India and as and when a major competitor quits the market, Strides swoops in to collect the market share.

This strategy is very similar to Deepak Nitrite’s ‘Right to Win’. Deepak too doesn’t enter a market until and unless it can win a significant market share. Ability to win market shares enables the company to be cost competitive and undercut competition.

Strides is also one of the largest filers of ANDAs with USFDA but has commercialized maybe less than 50% of those filings.

Another key area for Strides business is its foray into China market with a JV with Sihuan Pharma. China until very recently had not allowed any Indian or global player to enter it’s market cause it wanted the local generic players to flourish but local industry moved towards innovative drugs leaving the generic market open. Non availability of generics lead to a large healthcare cost increase. Chinese government realised this and allowed Indian companies to enter market by partnership with local firms as Joint Ventures.

This is very similar tactic used by Chinese government for many of their industries including investment banking. Goldman until very recently had a very successful partnership with a local Chinese firm to conduct business in the region. I believe they are trying to do the same with their generic industry.

The firm Strides has partnered with has a 8.3% market share in Cardio vascular therapies. Chinese generic market is also worth over $137 Billion annually. This is a very large unseen optionality for Strides. Most brokerage reports I have read do not mention anything about China JV at all. I believe Strides with its JV with local player will be very successful in this market given they already have a large product portfolio and are the lowest cost manufacturers in most of their products.

13 Likes

Not really. They seem to be very concerned about the warning letter and working overtime to correct the oversight. They were also rather straightforward in accepting the slip up. “A blemish is a blemish” comment from Mr Arun is famous now. At the same time, any future adverse warning letters will impact valuations and also, any adverse observations for stelis would be a severe setback. As per Pharma compliance expert Mr Amit rajan: seee the section on biologics specifically: Pharma compliance issues - #14 by harsh.beria93

Mr Rajan was of the view that biologics manufacturing cant be done in India because we simply do not have the hygiene standards as a people needed for meeting the requirements of sterile manufacturing.

Any investor in syngene, stelis is taking a contra view. Something to be aware of.

pharmacompass is your friend here. You can search for any drug and get addressable market.

Thanks for adding your thoughts on the smaller molecules large market share. Looks worthy of investigating more at a granular depth for all the molecules.

Can you plz share your company primary source of this info so that i can educate myself and also come to the same page. I have not come across this anywhere until now.

But what does this mean? How does company know when it can win market share? Yes, Mylan and Teva are shutting down plants, and this serves as a big tailwinds, but if you see latest concall there is still pricing pressure and i am not sure they are able to maintain market share for all molecules. So clearly all competition is not going away, competition from India is not going anywhere as an example.

Key question is why other indian generic players are unable to do it as well. IIUC their algo is:

- File lots of ANDAs and stay prepared.

- As soon as there is a demand supply mismatch due to supply going away (eg: Teva/Mylan shutting down plants), they utilize their fungible capacities to enter that market and capture large market share.

Only question is why wouldnt other players that are not closing their plants capture the market share first given they are the well entrenched incumbents in this molecule’s market and strides is the challenger new comer.

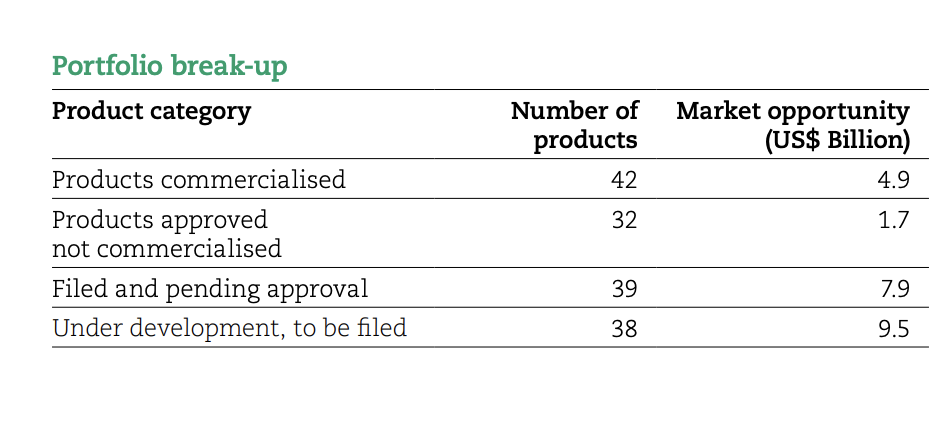

This is correct. At the same time 50% andas does not equal 50% opportunity. Some data here as of FY20 end

One key risk that all strides investors need to be aware of (this has already played out in strides once but still):

As a US facing pharma manufacturing co scales up in multiple manufacturing locations, it becomes increasingly difficult to enforce a common high compliance culture. Probability that at least one of the plants messes up and gets warning letter goes up linearly with number of plants and thus scale of the company. This is also why we see aurobindo get so many OAIs and VAIs. Please do read the compliance thread if you haven’t.

17 Likes

Most of the ANDAs filed by Strides with USFDA are for prescription dozes rather than OTC medications. Explains their need for a front end sales team for US markets.

This also means that Strides US Business has elements of brand. Get enough doctors to prescribe your medication and soon it will start getting treated as a brand (can’t do the same with OTC).

Here is a visual analysis I did for their ANDA filing with US FDA. Its an interactive dashboard so feel free to play around.

https://public.tableau.com/app/profile/vizbytar4004/viz/StridesANDAAnalysis/StridesANDAs

Data for the dashboard from USFDA GreenBook Database: Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations

15 Likes

7 Likes

The Pediacare brand indeed commands good reputation in many developed markets as I have heard frm people living in the US and also Gulf countries.

2 Likes