Following is my current view on as things stand -

ONESOURCE

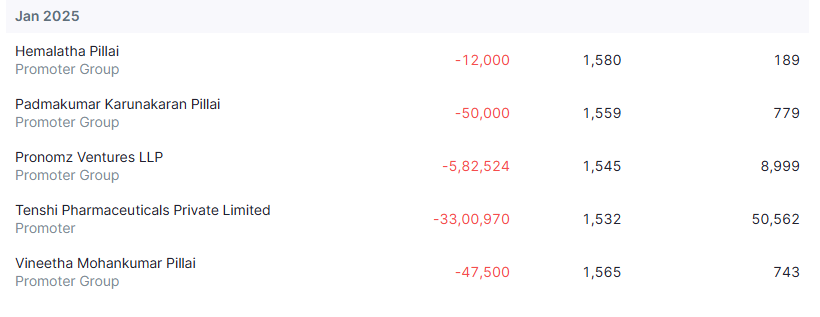

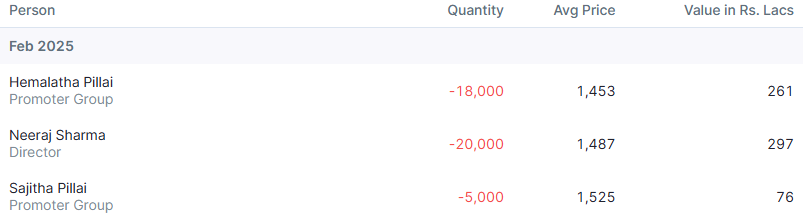

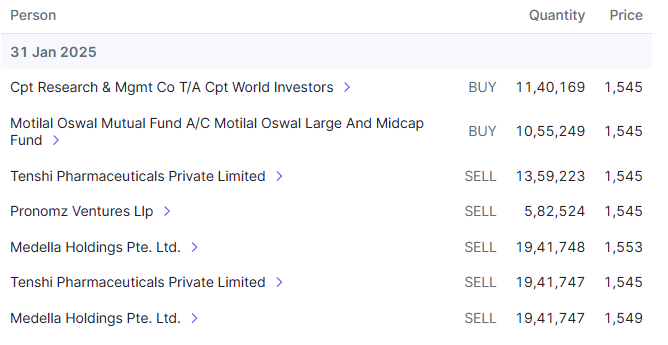

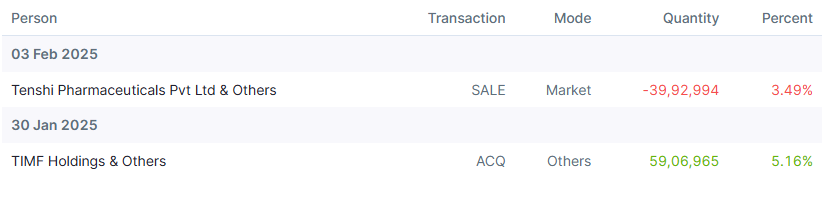

Promoter Selling

Promoter has sold roughly 600cr worth of stake so far and there might be some more to go. In my mind, this is nothing more than OFS sale in IPO that usually promoters do.

Promoter founded two platforms (non-conflicting with existing Strides business) - Stelis and Steriscience.

Stelis is into biological products and fill finish. It is a capex heavy business (100mn$+) with long gestation period of 6-7 years. The business also went through several upheavals - primarily COVID (elongation of business plans) and vaccine write off. Through all these upheavals, promoter had to keep funding this platform - privately and through Strides. I think a significant part of these were funded through debt/pledges at promoter level.

The second platform is Steriscience which was really restarted in 2020 when they bought back units from Mylan. This business also needed few years to come to a shape where it can be profitable. A lot of investments in this platform was also done by promoter privately through debt and pledge.

During this time, it was not like existing listed businesses were flourishing. Strides had two notable shocks - one was Ranitidine impurity issue and other was COVID inventory write off. Solara was stuck with its Vizag unit and continued to bleed. Promoter had to inject money in both of these businesses through his own resources.

When these platforms are now listed and where business visibility is good, promoter decided to list them. Is it really unfair or red flag that he is selling partial stake upon listing to probably take care of debt at promoter level?

In my opinion, it is a non-issue but to each his own!

As of today, the debt level is more than managable in all 3 of his companies.

OneSource - long term debt of 363cr on Jan 31, 2025

Strides - Net Debt of 1571cr as of Dec 31, 2024

Solara - Projected net debt of 560cr at Mar 25, 2025.

Sources -

OneSource credit report.

( 202502140245_OneSource_Specialty_Pharma_Limited.pdf)

To my mind, this shows resourcefulness of promoter and ability to work in the markets. I also hope in the same breath that - next 4-5 years are equally dull and boring as how eventful last 5-6 years have been.

Business

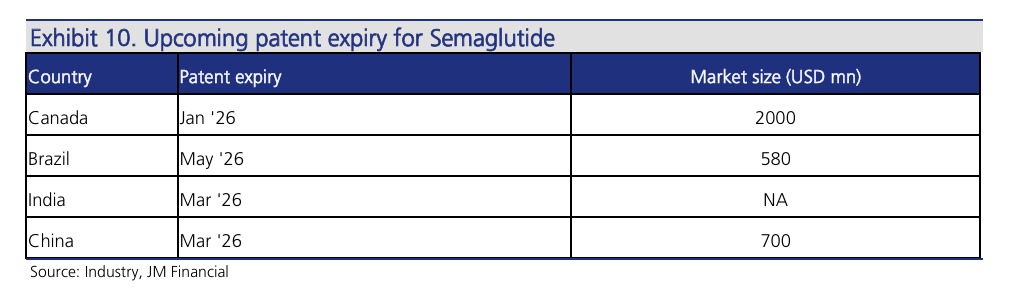

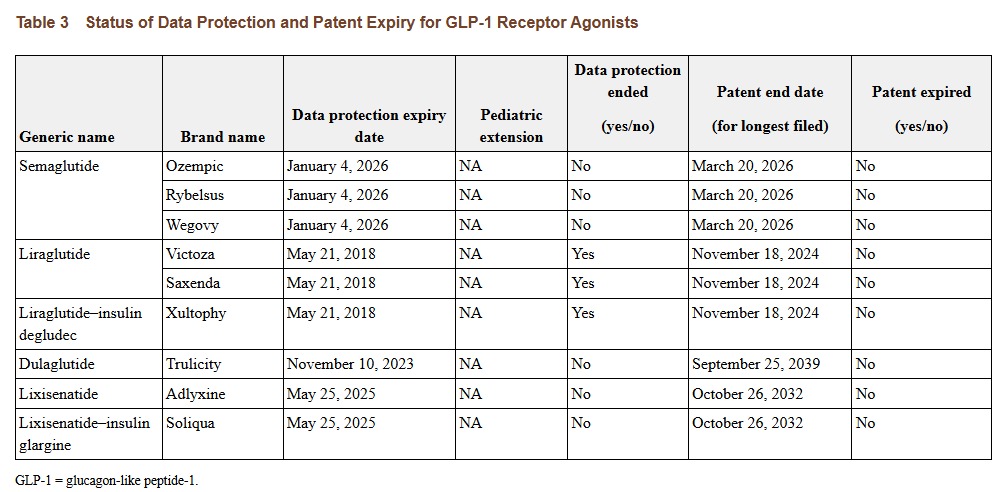

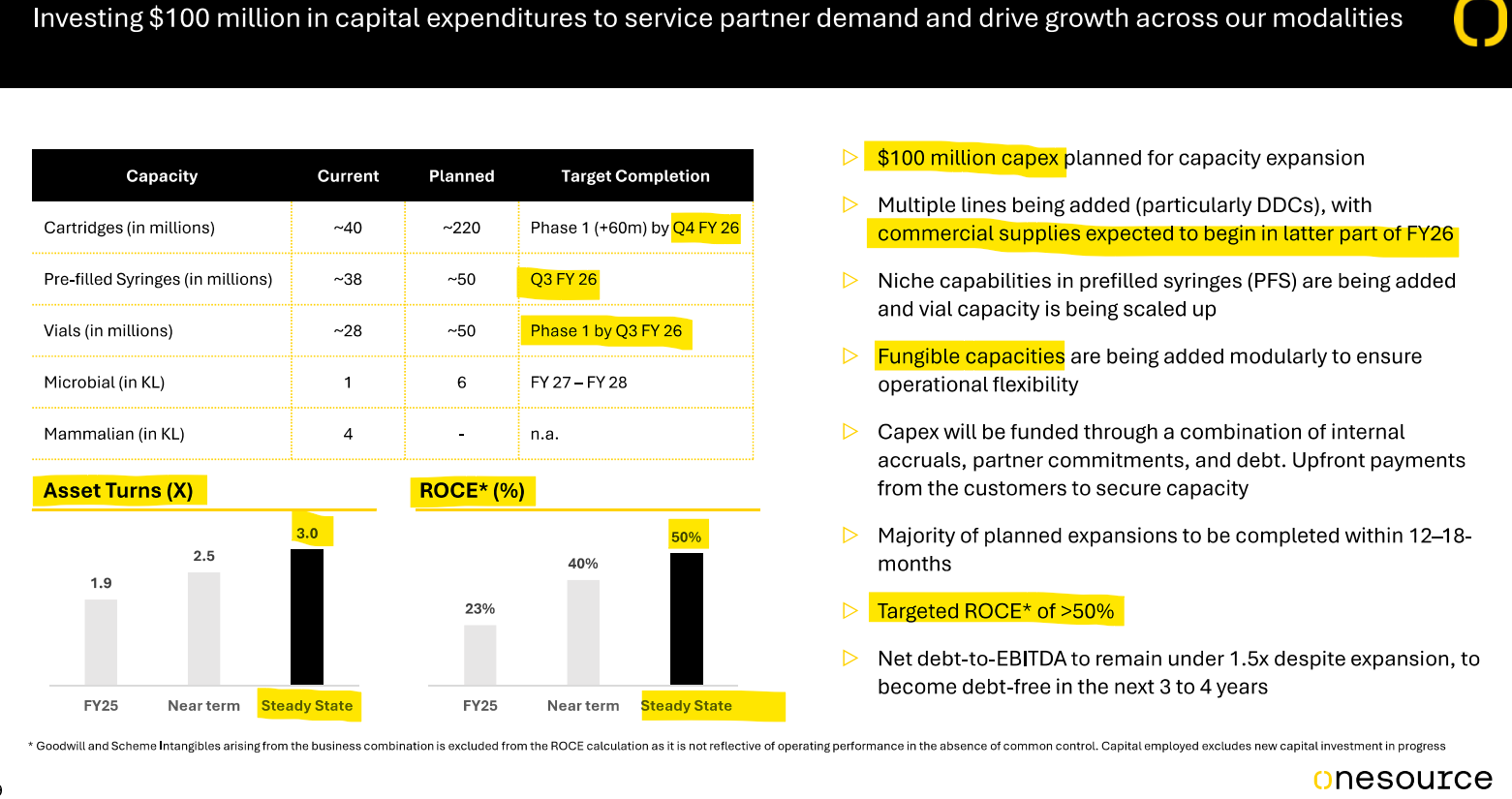

Coming to business, promoter has given exciting plan for expanding cartridge capacity for GLP-1 fill finish business. We need to be focused on figuring out their large customers and how these customers are progressing in getting approvals in Canada/India/Brazil/Middle East.

My understanding is that one needs to design specific fill finish lines for each device, and it takes time to get the lines. This thesis will get tested as more and more launches of GLP-1 start happening.

The softgel business capacity has moved from 0.8bn to 2.4bn. We need to track how the capacity ramp up is happening. Promoter had also mentioned plans for additional 1bn line in softgel business. Promoter had also mentioned that some large softgel products are going off patent over next 1-2 years and these can provide good opportunity. We need to work on figuring out these products.

GLP Patent Expiry Schedule -

Canada GLP Patent Protection Expiry Dates -

STRIDES

Tarriffs

Coming to threat of 25% tariffs on Pharma by Trump, although it is a major issue if it really were to happen in this manner, Strides is probably one of the better placed players as they have a formulation facility in the US (Endo Pharma). My feeling is that with not very large capex (something like 20-30mn$), they might be able to reconfigure US supplies rather quickly if it really comes to that.

Controlled Substances & Nasal Sprays

Other area that we need to track is launch of controlled substances and nasal spray products in the US and EU markets. These are lesser competition products and do have healthy EBITDA margins. I have spent some time of Endo’s approved products in US and a lot of them are controlled substances. We need to find 4-5 products in this list which can give 15-20mn$ type revenue to the company.

Endo_Pharma.xlsx (26.5 KB)

Endo_Operations.xlsx (283.9 KB)

Disc - I have bought shares of both the companies in the last 30 days. This is not a buy/sell recommendation. I am not a SEBI registered RA. Please do your own due diligence before investing.