I find it counter intuitive that a company deliberately makes inferior quality products to sell it cheaper. This would turn the LTV of a customer to zero. A customer after buying/ using a Pigeon product once would also migrate/shift to other brands if the quality is bad. She would rather spend some more money to get better value.

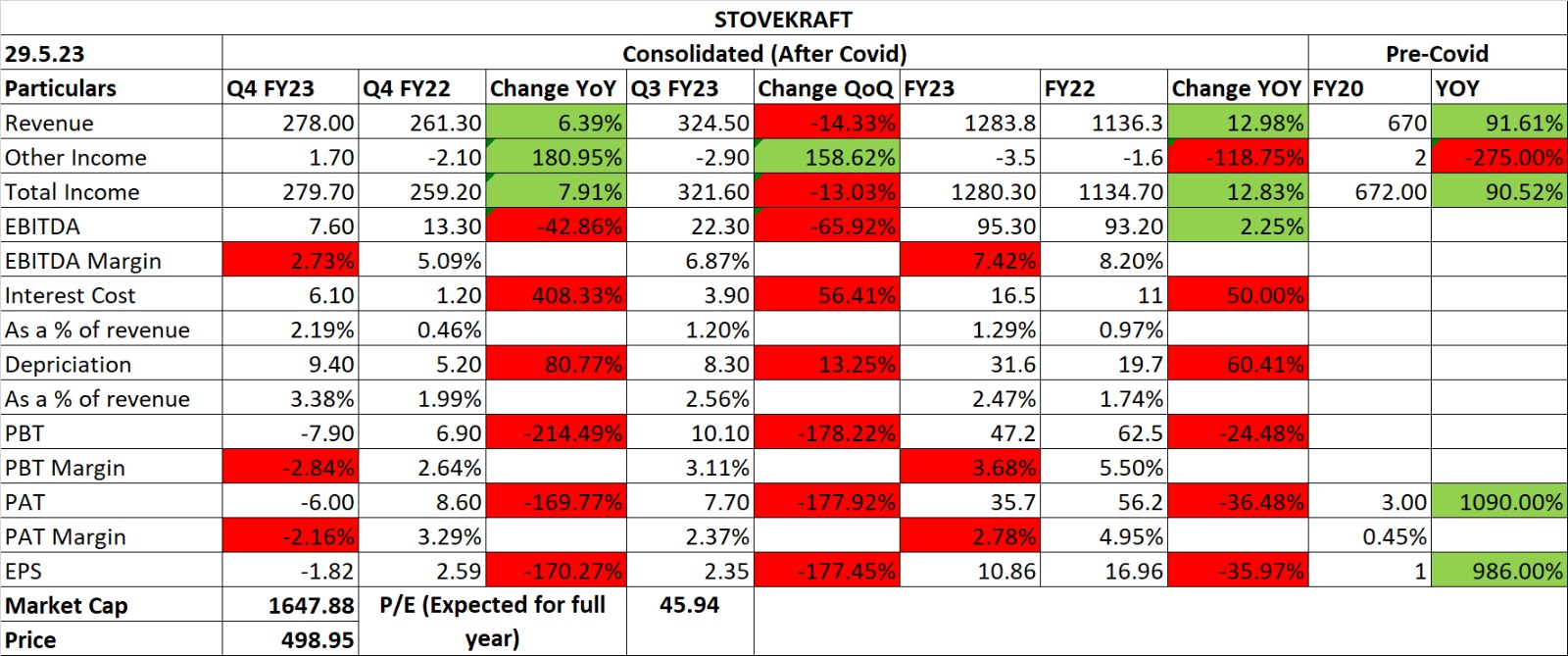

Company have reported loss in Q4. In investor presentation there is no mention about loss in Q4. They only presented data for last 12 months.

2 Likes

- Capex for the year is INR75 crores, with an additional INR20 crores being an advance for future spending. Capex for the year will not exceed 25% of PAT along with depreciation. Some of the planned capex in FY '24 will be staggered to early FY '25 due to the challenging business outlook.

- LED sales have grown 2.1% YOY.

- Channel mix for FY23: General trade - 42%, Modern retail - 10%, E-commerce - 30%, Corporate sales - 5%, Exports - 10%. E-commerce channels have been impacted by operational issues and consumer behavior, but are expected to return to earlier growth levels.

- Guidance: The company has successfully added 54 stores in southern markets and remains committed to accelerating store reach in FY’24. The company plans to open around 100 stores this year via Franchising, with 7-8 stores per month as the run rate. The company’s retail stores have a gross margin of 45-48%, with costs ranging from INR1.25 lakhs to INR3 lakhs and an average revenue of INR4 lakhs per month. Stores become profitable after the third month of operation. Gross Margins expected to improve 1% in this year. Plans to reach 20% ROE this year and EBITDA margin of 11%. They advise against sacrificing margins and ROE for growth in a tepid demand scenario. Advertising spend is not more than 3.5% and the company will continue to invest in marketing.

- The company is confident in demand for their products, particularly during festival seasons, and believes they can achieve their historic growth rate of 19% in a normal situation.

- The company assures investors that it is on a strong footing and will be able to deliver aspired EBITDA and margin numbers in the coming quarters.

2 Likes

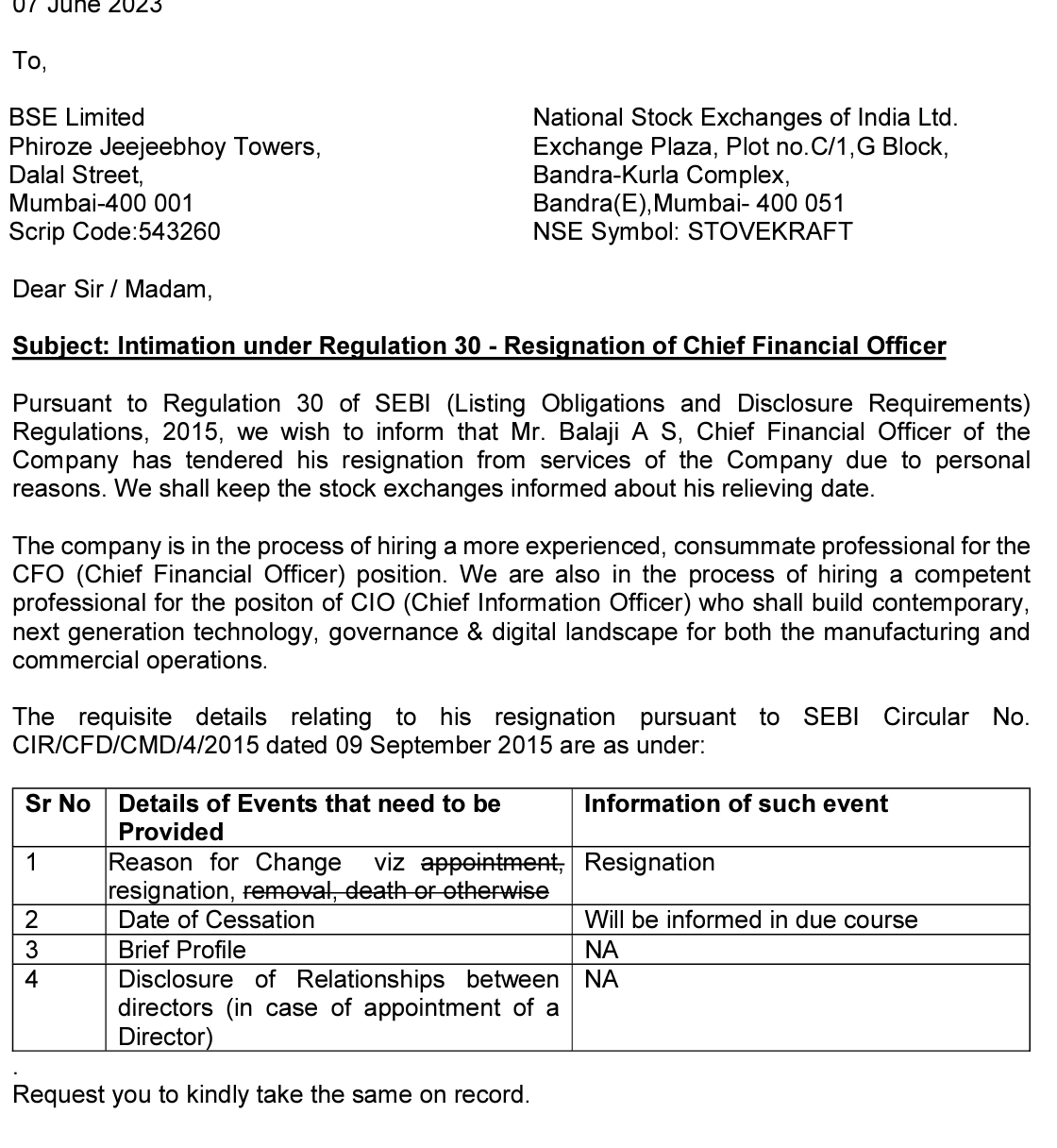

The CFO has quit (again). He was appointed only in Feb 2022. Along with the CEO quitting recently and the company’s inconsistent performance, as an investor, losing patience with this company. Reducing my holding by 75% and hoping for the best.

2 Likes

Company has expanded kitchen product lines with products manufactured at its Bangalore factory.

Some of the items as per press release are stainless steel bottles, rice cookers and air fryers.

Not much info on Skava acquisition which was to complement sales of LED bulbs. Or performance of Gilma brand.

Ebitda margins have improved.

By lower quality, I meant rather than lasting for 5-7 years, it would last for 3-4 years (which in itself is long time frame). In this scenario, each buyer as an individual doesn’t have data (both in terms of time frame as well as volume) to judge whether the StoveKraft product bought by the buyer is relatively good or not compared to other brands unless he/she goes and actually has two different brands being used simultaneously.

An average buyer would see “lower priced product, last for 3-4 years, good enough” at the time of buying. What do you think about this?

P.S. : I used 3-4 years as the lifespan of the stovekraft products as I have two pigeon products in my house and that is how long they last before “cracks” start showing up. This may vary upon different products/usage.

IT raid at company’s premises. Company notified exchanges for the same.

Not able to find any new news after the news came out anybody knows any update?

The raid by income tax officials has concluded. No material information has been disclosed yet.

The stock seems to have reacted positively after Income tax inquiries.

Now the company is expanding sales network in the North.

2 Likes

Unfortunately with every quarter Stovekraft management seems to be learning their business. The last quarter result is not so encouraging and the stock is bit of touching all time low!

Disc: Held the stock for a while and have divested now.

Resignation of CTO.

they are opening retail show rooms in karnataka so might possible they have entered in rented porperties

1 Like

Stove Kraft has made a significant investment in renewable energy by commissioning a 4 MWp solar power plant at its new Unit 3 facility.

This solar plant is expected to generate 20% of the company’s current electricity consumption, leading to annual cost savings of approximately Rs. 36 million. With this addition, Stove Kraft’s total renewable energy capacity now stands at a respectable 9.06 MWp.

1 Like

Is the stock overvalued on the current valuations ?

Stove Kraft Limited (SKL) Q2 FY25 Earnings Call Summary

Key Financials

- Q2 FY25 Consolidated Revenue: INR 418 crores, a 10% YoY growth from INR 379 crores in Q2 FY24.

- Q2 FY25 EBITDA: INR 49 crores, with margins improving by 120 basis points to 10.5% compared to Q2 FY24.

- Q2 FY25 Profit After Tax: INR 16.7 crores, slightly lower than Q2 FY24 due to the notional impact of indirect lease accounting.

- H1 FY25 Consolidated Revenue: INR 732.8 crores, an 8.2% YoY growth from INR 677.5 crores in H1 FY24.

- H1 FY25 EBITDA: INR 80.7 crores, with margins at 11% compared to 9.4% in H1 FY24.

- H1 FY25 Profit After Tax: INR 24.9 crores, with margins at 3.4%.

Key Pointers

- Own Manufacturing Strategy: SKL’s strategy to establish its own manufacturing facilities has started to yield positive results, leading to enhanced operational efficiencies and improved gross margins and operating profits.

- Stable Raw Material Costs: The company benefited from stable raw material costs in Q2 FY25, contributing to margin improvement.

- Retail Expansion: SKL continues to expand its retail footprint, adding 22 new stores in Q2 FY25, reaching a total of 213 stores across 13 states and 54 cities.

- Channel Mix: The company reported double-digit growth across all major channels in Q2 FY25, indicating robust demand. The channel mix was:

- General trade: 28%

- E-commerce: 40%

- Modern trade: 13%

- Corporate Sales: 5%

- Own Retail: 4%

- Exports: Exports constituted 10% of the company’s revenue in Q2 FY25.

Future Outlook

- Positive Demand Outlook: The company is optimistic about maintaining a strong market position, driven by the festive season, favorable economic conditions, and government policies.

- Volume and Realization Growth: The company reported growth in both volumes and realization in Q2 FY25 and expects this trend to continue.

- Quality Control Order (QCO) Advantage: The introduction of QCO for various small appliances is expected to further boost SKL’s revenue and margins as the company has already established the required manufacturing infrastructure.

- Retail Expansion: SKL plans to continue aggressively expanding its retail store network, aiming to add around 50 more stores by the end of FY25.

- EBITDA Margin Target: The company aims to achieve EBITDA margins in the range of 11% to 14% over the medium term (3-5 years) through operating leverage and improved gross margins.

- Exports Growth: SKL is working on developing new products for the export market and expects to achieve a 16-17% revenue contribution from exports with the addition of new global retail partners.

Challenges

- Working Capital Management: While working on reducing inventory and receivable days, the company saw an increase in working capital loans in H1 FY25 due to the festive season.

- Subdued Volume Growth in Certain Categories: Some product categories, such as induction cooktops and gas cooktops, experienced subdued volume growth in Q2 FY25.

- Competition: SKL faces competition from other established players in the kitchen and home appliances segment, particularly as new manufacturers emerge in response to the BIS standards and QCOs.

- Depreciation and Interest Costs: Depreciation and interest costs are expected to increase as the company continues to expand its retail store network.

- MFI Channel Slowdown: The rural MFI channel remains subdued due to pre and post-election restrictions.

Overall, it appears that StoveKraft has lower customer ratings than its competitors. There are recurrent quality issues raised. Other the other hand, Ikea monitors its returns, customer feedback, etc. Further, Ikea has international customer base which has high expectations from Ikea. If quality issues happen with Stove Kraft’s proposed Ikea range as well, I am wondering if the Stove Kraft - Ikea tie up will be long lasting. Ikea is not hesitant to change suppliers if they do not meet its quality standards. Even in India, I am wondering if Stove Kraft has repeat customers. It appears to have simply low priced products and price is the key driver rather than quality. Any thoughts?

1 Like