Well this time Mr Gandhi in interview has accepted margins going to be lower, better to be upfront rather than being in denial, explains the state of pricing power in this industry segment as well as demand scenario.

Sequoia seems to have sold out most of remaining stake as well.ast week.

Was Invested post listing, Exited post Q3 results, a good learning on promoter quality and guidance credibility

Still not confidence inspiring. It is a wait and watch situation on how Stovekraft saves it’s margins while growing Skava and it’s RTA kitchen business.

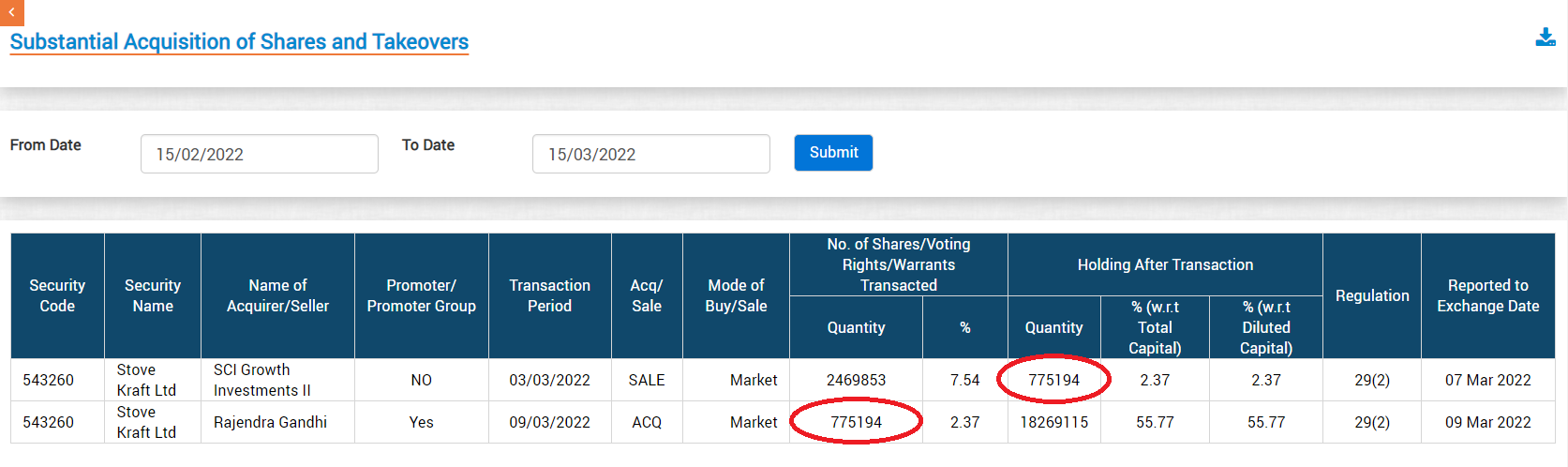

Rajendra Gandhi has pledged his shares and used that money to buy out remaining stake of SCI Growth (i.e. Sequoia). With this, the latter has completely exited the company.

Not sure why Mr. Gandhi had to do that – whether it was just to avoid Sequoia selling the stake in the secondary market or they had a put option not disclosed in the offer document. I say this because just a year back the promoters sold nearly an identical quantity (7.5 lac shares) in the IPO at Rs.385 per share. So why would they buy now so soon at Rs.650 per share.

It is most probably because there was a contractual agreement to buy at a minimum price. SCI was trying to sell down stake via a block trade and was sounding out instituitional investors. Looks like they did not have enough takers and promoter was forced to buy.

So it is better not to extrapolate future prospects based on this

The margins are falling. institutional investors are exiting. minority investors are also questioning the future growth prospects.

In such a scenario, it is prudent to look at how Butterfly Gandhimati got acquired by Crompton Consumer.

Stovekraft needs to look at Havells, Orient Electric, Bajaj Electricals, Voltas or CG Power (they have recently entered into fans and are already in switch gears) to get acquired by the bigger company.

With a strong brand in hand of Stovekraft, such an acquisition will be value accretive for all parties involved.

Just my two cents.

Stovekraft opening retail locations.

Promoter pledging shares of Stovekraft to buy shares of Stovekraft.

Expected to give a strong quarter if Onam sales were good.

He added that the consumer electrical segment is doing well. The base is smaller and hence the growth rate is much higher than the company’s growth rate in this segment.

He expects Stovekraft’s margin for the 2022-2023 financial year to come in at 11 percent.

Company published Sep 2022 results - Brief on Y-o-Y comparison, Almost 12% growth in topline, expansion in gross margins revenue (Y-o-Y), EBIDTA margin 9.3% and PAT growth despite higher Tax outgo. Increase in trade receivables (Sep 2022) due to higher sales (highest sales happens in Sep quarter for company) and corresponding increase in current liabilities. Improvement in Operating cashflow.

Considering seasonality in sales, Y-o-Y comparison in results is more meaningful. Important to watch for guidance on revenue and margin for Dec 2022 quarter results, otherwise looks negatives have been factored in for time being

I did some scuttlebutt (online reviews, talking to local dealers) when it comes to the products that Stovekraft manufactures and markets under the Pigeon brand:

- Pressure cooker - Hawkins, Prestige, Butterfly products are much better in terms of quality

- Gas cooktops - Many popular brands (Prestige, Sunflame, Faber, Butterfly) with good or better recognition compared to Pigeon

- Induction cooktops - Prestige, Milton, etc are preferred brands. There are many more.

The competition is significant and their are relatively low barriers of entry to these products. I can’t see any moat here for Stovekraft. What makes it standout or help it maintain its margins in the future?

Members, please share your views for the above points, if any.

Wholetime DIrector and CEO resigns.

As per the announcement “The company has implemented a new organization structure

to help achieve its strategic goals and support future growth. This revised structure has four new executive positions, viz., Chief Revenue Officer, Chief Operating officer, Chief Human Resources Officer and Chief Growth Officer, in addition to existing position of Chief Financial Officer, and the team has already started working towards achieving the organizational goal.”

I also had pigeon brand Stove, quality is not that great and definitely they have competition with many big players…

I did some analysis of the company and created a report on it.

I am sharing the report here and your suggestions are highly welcomed.

Feel free to contact me at vinoddalvi123@gmail.com If you have any doubts or questions.

Stove Kraft.pdf (1.5 MB)

Hi, good compilation.

There are a couple of additional pointers

- The quality of the StoveKraft is inferior but the price is also lower compared to its competitors.

- You had mentioned the following in pg 21 of your report. Can you clarify further on this?

The company is not profitable compared to its peers and has high debt so the company should reduce its debt by increasing its profit.

- You had mentioned the following in pg 21 of your report. Can you clarify further on this?

The company is not profitable compared to its peers and has high debt so the company should reduce its debt by increasing its profit.

Compare the profit margin and debt of the company with its peers/competitors.

Mr Gandhi has mentioned that they are a value brand where they are priced lower that the other mass market brands and hence the inferior quality but people especially the aspirers and lower middle class category want to buy branded products but don’t want to spend as much money.

As per a survey, aspirers (income upto 2-5 lakhs) are 52% of the housholds while the middle class (upto 30 lakhs) are 30% of the household in the country. The addressable market is ~65% for the company and India has ~25 crores of households. There is enough for everyone to go around. Make the business more recurring by making lower quality products and reduced prices.