My experience & conclusions haven’t been an extremely reliable indicator so far, at best I have a strike rate that is 5-10% higher than the usual 50%.

This is best explained with some examples -

Market peak in 2008 - We have equities making new highs at a dizzying pace, market was up almost 50% in 8 months. Bond yield was at 10 year lows though we were in a rate hike cycle then and the INR had appreciated to 40 against the USD. You could see that all three markets were flashing signs that India was a screaming buy - consensus buy

The market bottom in August 2013 - Post the taper tantrum in a matter of 30-40 days we say bond yields go past 9% (the highest they have been for some time), INR depreciate past 60 to the USD and NIFTY falling to a low of around 5600. All three market flashing signs that India was a consensus sell

Market bottom in Feb 2016 - Commodity crash took the NIFTY to 6900 on budget day while bonds and INR cracked too in a 15-20 day period. The reversal from this bottom was fast after the ferocious fall in the last leg

The key point to look for is resonance across all three markets which tell you the same thing. You can observe this in global markets too on specific event days, examples being -

One should apply this only when you see singe sided moves who are reflecting across all markets. Betting against the market once you see the signs of abject capitulation can work out to be very profitable - usually though buying a call/put option. In such a scenario writing options is too risky since one mistake can sink you, while buying an option keeps downside limited but gives you 3-4 times the payoff if you get it right.

How do credit spreads tie in?

Credit spread is an indicator of how easy it is for corporates to raise money from bond markets. If credit spreads (over G-sec of same tenor) are way lower than historical, one can see that financial stocks take a hammering since money is stock in trade for them. Throughout the run of 2017 credit spreads kept narrowing while equity markets kept going higher, till the trend no longer held good. From mid 2018 onward you can see that credit spreads widened and NBFC stocks started taking a hammering, no one could raise money other than HDFC Ltd and Bajaj Finance - those two stocks are standing tall amid the ruins.

Implications

Do not use this framework with a predictive mindset, will never work out. Always use reading from markets to read what the mood of the overall capital market segment is and then place bets/allocate capital accordingly. More like a reverse DCF approach than a DCF approach

I find it very perplexing that equity investors in financials do not have much of a clue about how bond markets work. Unless one has the network and resources to track how the company is being perceived and treated by the bond markets, one should not fool himself into thinking he/she understands banks.

Any crisis starts in some other asset class and then equity markets calibrate. 2008 was a credit crisis, 2013 was a central bank/sovereign bond event, 2016 was driven by fall in commodities. If bond/FX markets are telling you something else, chances of them being right is more rather than equity markets being right

In short this is a very complicated framework where by definition your strike will not be high - this is why macro economists usually get it wrong. More the number of variables involved, higher the range of outcomes and lesser the signal/noise ratio.

Some day when I finally have the inclination and bandwidth to trade options, I will further work on this framework. For the time being I just use this exercise as a barometer to get a pulse of what the markets in general are discounting and pricing in

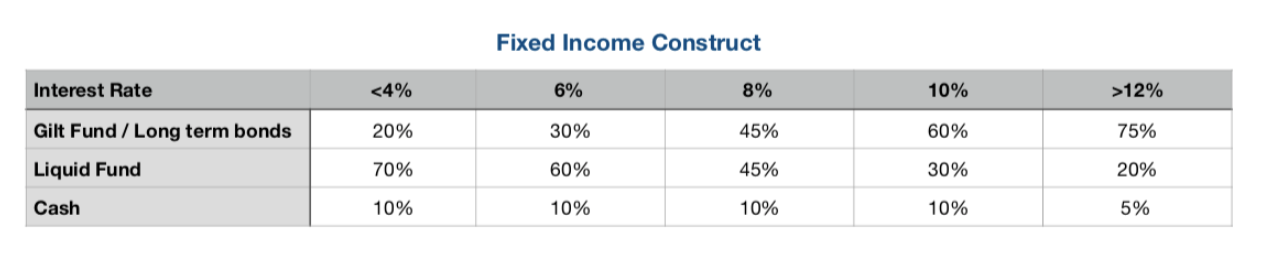

Fixed income Risk - Return strategy depends upon what role you want Fixed income to play in your portfolio

In my case since I am full time investor -

I have different strategy - I am more concern with return of capital in case of Fixed incomes rather than return - while in equity I am ok to take more risk for return …

Earlier I used to use Liquid funds ( for liquidity to invest in equity ) + Gilt / Taxfree bonds

Now as Interest rates are coming down - I have moved to Quasi Bonds ( pl read Portfolio Shailesh ) in place of Gilts

@zygo23554, @Yogesh_s, Any website where do you see credit spreads. Do share link. Also any bond specific website experience bond investors follow for Indian markets?

Recently going across debt mutual fund portfolios. I see they just mentioned the portfolio but not the coupon of each instrument (bond/cd) held? Even the website has no brochures detailing the coupon rates. Did some one face this. I am looking at “L&T Triple Ace Bond Fund”

I presume you are in US. So what exactly are you looking for? Do you want to invest in debt MF or invest directly in bonds? If debt MF, I would suggest to visit freefincal.com and go through the many articles written about debt MF. If directly in bonds like NCDs, CP etc. I have no idea about all the coupon rates, Value Research provides the details for some, and does not provide for some. I invest in debt MF, so I would not go deep w.r.t to the rate.

5 days back, Franklin India LD fund was down 1.98% in a day due to essel infra knock off as said.

Do you see any chances of NAV recovering that fall, as the fund house seems confident and does not intend to sell the pledged shares? does someone has any idea?

thinking of exiting from this…but if there is chances of NAV recovering, then can wait for a while

I am looking to add more bonds ( NCDs) to my portfolio and i want to add only PSU-sector bonds.

How safe are PSU bonds ? for example, IFCI bonds are trading at yields of 12+ . The company has interest coverage ratio of less than 1 and it is making losses too.

In an ideal world without government backing, it is a risky bond. But can the government default on the bond payments? Has it ever happened before ? Is it a big thing if the government defaults on the bonds or is it a normal and can happen from time to time?

I don’t think I’m the medium term at least the govt will let IFCI default on its debt, as it is a proper PSU (over 50% govt shareholding). But the thesis would surely rely on a bailout, seeing the stock price & market cap of IFCI.

The debentures of l&T finance and Tata capital are trading at mouth watering yields. The market considers them more risky. may be because of the credit defaults that are expected because of the corona crisis. What are the parameters to consider for default risk? Apart from profitabilitiy, NPAs , would it make sense to compare their long term interest ratios ?

Are there any restrictions on NRI’s to buy tax free bonds from secondary market. ICICI direct does not allow it through NRI/NRO PINS or NON PINS account. Can any one throw light on this.

Thanks.

Hi,

To boost demand and avoid deflation, RBI will almost surely be reducing interest rates in the near future

I am looking to park some money in GILT funds to benefit from the rate cut and would like to understand the risks involved.

While I understand there is very little credit/default risk while investing in government securities but there is a likelihood of ratings downgrade by credit rating agencies if fiscal deficit increases significantly…

What would be the impact of Sovereign rating downgrade on G-Sec prices and Gilt funds?

Not an expert, but there is a possibility that future expected RBI actions are already priced in. For that matter, even the risk of a downgrade might be already priced in. Just some food for thought.

With RBI introducing RBI Retail Direct, I am curious about how forum members are using this option to manage their portfolio allocation.

There are many articles about the pros/cons of retail investors investing in Gilt directly. Anyone here using this option in their portfolio?